|

市場調査レポート

商品コード

1406015

世界の在宅ヘルスケア - 市場シェア分析、産業動向・統計、2024年~2029年の成長予測Global Home Healthcare - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| 世界の在宅ヘルスケア - 市場シェア分析、産業動向・統計、2024年~2029年の成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

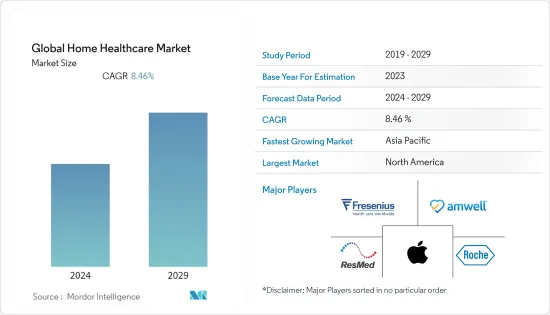

世界の在宅ヘルスケア市場は、2024年には3,090億7,000万米ドルと評価され、予測期間中のCAGRは8.46%で、2029年には5,003億9,000万米ドルに達すると予測されています。

COVID-19パンデミックは在宅ヘルスケア市場に大きな影響を与えました。在宅医療ハブ技術により、パンデミックの間、患者は自宅で安全に過ごすことが可能になり、病院、救急室、第一線の医療従事者への負担が軽減されたことが、市場にプラスの影響を与えました。例えば、2021年8月にLancet Regional Healthに掲載された調査研究によると、在宅医療は、病院の過密状態を緩和し、慢性疾患や重症でないCOVID-19患者が自宅で治療や監視を受けられるようにするために、パンデミックが始まって以来、高い需要があります。このように、パンデミックは在宅ヘルスケア市場にプラスの影響を与え、予測期間中も増加傾向が続くと予想されます。

在宅ヘルスケア市場の主な促進要因としては、可処分所得の増加、外科手術の増加、在宅ヘルスケアにおける急速な技術進歩などが挙げられます。例えば、2022年2月に発表されたPETERSON-KFF Health System Trackerのデータによると、米国のヘルスケア支出は2020年に前年比9.7%増の4兆1,000億米ドルに達し、約4.3%増加しました。この加速は、連邦政府の医療費支出が36.0%増加したことによるもので、パンデミック(COVID-19)への対応が主な原因です。また、同資料によれば、ヘルスケア支出全体に占める民間企業の割合は16.7%、州・地方政府の割合は14.3%、その他の民間収入は6.5%でした。このように、可処分所得の増加は在宅ヘルスケア需要を促進し、市場成長を加速させる可能性があります。

また、世界中で外科手術の件数が増加していることも、在宅ヘルスケアサービスの需要を生み出すと予想されます。例えば、2021-2022年に保健・家族福祉省と保健・家族福祉省が発表した報告書によると、2021年9月まで、インドのサフダルジュン病院では約829万人がOPDを訪れ、約3万3830件の手術が行われました。また同じ情報源によると、インドでは2020-21年に約25,101件の小手術が行われ、約9,327件の大手術が行われました。さらに2021年4月から9月にかけて、インドでは約7,223件の小手術と17,004件の手術が行われました。手術を受ける患者は、術後の厳重なケアと常時の健康監視を必要とするため、ほとんどの人が在宅ヘルスケアサービスを選択しています。従って、手術件数の増加が市場の成長を促進すると予想されます。

さらに、在宅ヘルスケア分野での技術進歩や在宅ヘルスケアサービスの増加も市場成長を後押しすると予想されます。2022年3月、Biofourmis社は、イリノイ州クインシーにあるBlessing Health System社に、患者の自宅で急性期病院治療を提供する最新プログラムの技術ソリューションパートナーとして選ばれたと発表しました。同様に、2022年12月には、ヘルステック企業のトゥモロー・ヘルスが、在宅ケアの一環として耐久消費財の注文を自動化する臨床ルールエンジンを発表しました。このような要因から、市場は予測期間中に大きく成長すると予想されます。

ただし、新興国や低開発国では認知度が低いため、予測期間中の市場成長は抑制される可能性が高いです。

在宅ヘルスケア市場動向

診断機器セグメントが予測期間中最大の市場シェアを占める見込み

効率的な治療のために継続的なモニタリングを必要とする感染症、糖尿病、関節炎、心肺疾患、心血管疾患などの慢性疾患の増加により、予測期間中は診断分野が最も大きな収益を占めると予想されます。近年の技術進歩の高まりにより、マルチパラメーター診断モニター、家庭用妊娠、不妊治療キットなど、自己モニタリング用の新製品が発売されるようになった。例えば、2022年1月24日から2022年2月6日までの期間にWHOが実施した調査によると、約12,368人がインフルエンザウイルス陽性と判定されました。その内訳は、インフルエンザA型が8,423人(68.1%)、インフルエンザB型が3,945人(31.9%)、さらにインフルエンザA(H1N1)が171人(6.4%)、インフルエンザA(H3N2)が2,483人(93.6%)となっています。このように、感染症患者の増加は、このセグメントの成長を促進すると予想されます。

さらに、スクリーニングプロセスに対する患者の意識レベルの上昇と技術の進歩、マイクロ流体、モノのインターネット(IoT)、センサー、スマートフォン、ウェアラブルの統合は、ポイントオブケア検査を患者にもたらし、高感度、低コスト、迅速、接続された診断を提供するための強力な機会を示しています。例えば、2021年6月、家庭内診断キット会社のRo社はヘルスケア・テクノロジー社に買収されました。この買収は、全国規模の遠隔医療、薬局、ラボ処理、在宅検査・ケアサービスなど、同社の既存の強みを基盤としています。この買収により、Ro社の垂直統合型プライマリ・ケア・プラットフォームの診断機能とラボ・インフラが拡張されます。キットの在宅自己管理型検査ソリューションの支援により、Ro社は、より広範な疾患に対する患者中心のプライマリ・ケア体験を促進しながら、仮想的に、また患者の自宅で慢性疾患や予防医療をサポートすることができます。このため、この診断機器に対する需要は高く、予測期間における同分野の成長を牽引しています。

北米は予測期間中にかなりの成長が見込まれる

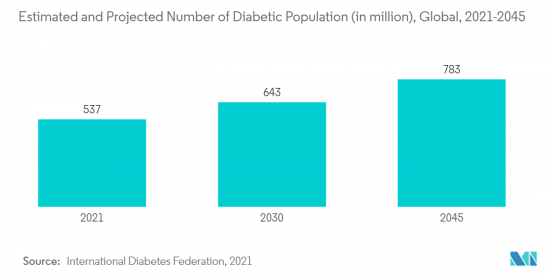

洗練された技術の高い導入、慢性疾患や生活習慣病、ヘルスケア支出の増加、医師不足、より良いヘルスケアサービスに対する需要の増加などの要因はすべて、北米地域の市場成長に寄与しています。例えば、2021年に発表されたカナダがん協会報告書によると、カナダでは2021年に229,200人以上の新規がん症例が報告され、同国の5年がん生存率は64%に達しました。さらに、同地域における慢性疾患患者の増加も市場成長を促進すると予想されます。例えば、国際糖尿病連合の糖尿病アトラス第10版によると、2021年には米国で約3,220万人が糖尿病に罹患しており、2045年には3,630万人に増加すると予測されています。従って、このような要因が北米地域の市場成長を促進すると予想されます。

主要製品の上市、市場参入企業やメーカーの集中、主要企業間の提携、米国における疾病事例の増加などは、同国の在宅ヘルスケア市場の成長を促進する要因の一部です。例えば、2022年2月、CVSヘルスケアは、同社のCVSヘルス製品ラインの延長として、6つのホームヘルスケア製品を発売しました。新製品には、コンバーチブルシャワーチェア、折り畳み式トラベルウォーカー、コンフォートグリップ付き杖などがあります。同様に、2022年9月、Innovative Health Diagnostics社は、DaaS(Diagnostics as a Service)プラットフォームを立ち上げ、ブランドがいつでもどこでも患者に在宅医療へのアクセスを提供できるようにしました。このように、製品の発売により、市場は予測期間中に米国で成長すると予想されます。

在宅ヘルスケア産業の概要

在宅ヘルスケア市場の競争は中程度で、複数の大手企業が参入しています。一部の企業は、革新的な製品を発売して世界市場での地位を固めるために、他社との合併・買収や調査協力など、さまざまな戦略を採用して市場での地位を拡大しています。現在市場を独占している企業には、Amwell、ResMed Inc.、Fresenius SE &Co KGaA、F. Hoffmann-La Roche AG、Apple Inc.などがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 可処分所得の増加と外科手術の増加

- 在宅ヘルスケアにおける急速な技術進歩

- 市場抑制要因

- 新興諸国および低開発諸国における認識不足

- ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(市場規模)

- 製品・サービス別

- 医療機器

- 治療用

- 診断

- モビリティケア

- ソフトウェア

- サービス

- リハビリテーション・サービス

- 呼吸療法サービス

- 輸液療法サービス

- その他のサービス

- 医療機器

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- 3M Healthcare

- Amedisys Home Health and Hospice Care

- Amwell

- Apple Inc.

- Arkray, Inc.

- B. Braun Melsungen AG

- Becton, Dickinson And Company

- F. Hoffmann-La Roche AG

- Fresenius SE & Co KGaA

- Hollister Inc.

- McKesson Medical-Surgical Inc.

- Medline Industries, Inc.

- Medtronic PLC

- Molnlycke Health Care

- Resmed Inc.

第7章 市場機会と今後の動向

The global home healthcare market is valued at USD 309.07 billion in 2024 and is expected to reach USD 500.39 billion by 2029 registering a CAGR of 8.46% over the forecast period.

The COVID-19 pandemic significantly impacted the home healthcare market. Home health hub technology made it possible for patients to stay safe in their homes during the pandemic while putting less strain on hospitals, emergency rooms, and front-line healthcare workers, which positively affected the market. For instance, according to a research study published in the Lancet Regional Health in August 2021, home-based care has been in high demand ever since the COVID-19 pandemic began to relieve hospital overcrowding and enable patients with chronic illnesses or non-severe COVID-19 to receive treatment and monitoring at home. Thus, the pandemic positively impacted the home healthcare market and is expected to continue the upward trend over the forecast period.

The major drivers for the home healthcare market include rising disposable income, increasing surgical procedures, and rapid technological advancements in home healthcare. For instance, according to the PETERSON-KFF Health System Tracker data published in February 2022, healthcare spending in the United States increased by 9.7% to reach USD 4.1 trillion in 2020, an increase of around 4.3% compared to the previous year. The acceleration was due to a 36.0% increase in federal expenditures for health care that occurred largely in response to the COVID-19 pandemic. The same source also stated that the private business share of health spending accounted for 16.7% of total healthcare spending, state and local governments accounted for 14.3%, and other private revenues accounted for 6.5%. Thus, such an increasing disposable income is expected to propel the demand for home healthcare, which may surge the market growth.

The increasing number of surgical procedures across the globe is also expected to create demand for home healthcare services. For instance, according to the report published by the Department of Health & Family Welfare and Ministry of Health & Family Welfare in 2021-2022, till September 2021, about 8.29 lakh people visited OPDs, and around 33,830 surgeries were performed in Safdarjung Hospital, India. The same source also reported that around 25,101 minor surgeries were performed, and around 9,327 major surgeries were performed in India for 2020-21. Furthermore, from April 2021 to September 2021, around 7,223 minor surgeries and 17,004 surgeries were performed in India. Patients undergoing surgery require rigorous post-surgical care and constant health monitoring; thus, most people opt for home healthcare services. Thus, increasing cases of surgeries is expected to propel the market growth.

Furthermore, technological advances in the home healthcare space and increasing home healthcare services are also expected to boost market growth. In March 2022, Biofourmis announced that it had been selected by Blessing Health System in Quincy, Illinois, as a technology solutions partner for its newest program that delivers acute hospital care in patient's homes. Similarly, in December 2022, Tomorrow Health, a health tech company, launched a clinical rules engine that automates orders of durable medical equipment as a part of homecare. Thus, owing to such factors, the market is expected to grow considerably over the forecast period.

However, a lack of awareness among developing and underdeveloped countries will likely restrain market growth over the forecast period.

Home Healthcare Market Trends

Diagnostic Equipment Segment is Expected to Hold the Largest Market Share Over the Forecast Period

The diagnostic segment is expected to account for the most significant revenue over the forecast period due to a rise in chronic disorders, such as infectious diseases, diabetes, arthritis, cardiopulmonary, and cardiovascular conditions, which require continuous monitoring for efficient treatment. The rise in technological advancements in recent years led to the launch of new products for self-monitoring, like multi-parameter diagnostic monitors, home pregnancy, and fertility kits. For instance, according to the survey conducted by the WHO for the period from 24 January 2022 to 06 February 2022, approximately 12,368 people tested positive for influenza viruses. Of these, 8,423 (68.1%) people were infected with influenza A and 3,945 (31.9%) with influenza B. Furthermore, 171 (6.4%) were influenza A(H1N1), and 2,483 (93.6%) were influenza A (H3N2). Thus, increasing cases of infectious diseases are expected to propel the segment's growth.

In addition, rising patient awareness levels towards screening process and technological advancements, integration of microfluidics, Internet-of-Things (IoT), sensors, smartphones, and wearables bring point-of-care testing to the patients and represent a strong opportunity for providing sensitive, low-cost, rapid, and connected diagnostics. For instance, in June 2021, Ro, the at-home diagnostics company Kit, was acquired by healthcare technology. The acquisition builds on the company's existing strengths, including nationwide telehealth, pharmacy, lab processing, and in-home testing and care services. It expands the diagnostics capabilities and lab infrastructure of Ro's vertically integrated primary care platform. With the help of Kit's at-home, self-administered testing solutions, Ro can support chronic and preventive care virtually and in patients' homes while facilitating patient-centric primary care experiences for a wider range of conditions. This resulted in high demand for this diagnostic equipment, driving the segment growth over the forecast period.

North America is Expected to Witness Considerable Growth Over the Forecast Period

Factors such as the high adoption of sophisticated technology, chronic and lifestyle diseases, rising healthcare spending, physician shortages, and increasing demand for better healthcare services all contribute to the market growth in the North American region. For instance, as per the Canadian Cancer Society Report published in 2021, over 229,200 new cancer cases were reported in Canada in 2021, and the five-year cancer survival rate in the country reached 64%. In addition, increasing cases of chronic diseases in the region are also expected to propel market growth. For instance, according to the International Diabetes Federation's Diabetes Atlas, Tenth Edition, in 2021, around 32.2 million people in the United States had diabetes, projected to grow to 36.3 million by 2045. Thus, such factors are expected to propel the market growth in the North American region.

Key product launches, high concentration of market players or manufacturer's presence, partnerships among major players, and increasing cases of diseases in the United States are some of the factors driving the growth of the home healthcare market in the country. For instance, In February 2022, CVS Pharmacy launched six home healthcare products as an extension of the company's CVS Health product line. The new products include convertible shower chairs, easy-fold travel walkers, and canes with comfort grips. Similarly, in September 2022, Innovative Health Diagnostics launched Diagnostics as a Service (DaaS) platform, allowing brands to provide their patients access to at-home healthcare anytime and anywhere. Thus, owing to product launches, the market is expected to grow in the United States over the forecast period.

Home Healthcare Industry Overview

The home healthcare market is moderately competitive and consists of several major players. Some companies are expanding their market position by adopting various strategies, such as mergers and acquisitions and research collaborations with other companies to launch innovative products and consolidate their market positions worldwide. Some companies currently dominating the market are Amwell, ResMed Inc., Fresenius SE & Co KGaA, F. Hoffmann-La Roche AG, and Apple Inc., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Disposable Income and Increasing Cases of Surgical Procedures

- 4.2.2 Rapid Technological Advancements in Home Healthcare

- 4.3 Market Restraints

- 4.3.1 Lack of Awareness among the Developing and Underdeveloped Countries

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Product and Services

- 5.1.1 Equipment

- 5.1.1.1 Therapeutic

- 5.1.1.2 Diagnostic

- 5.1.1.3 Mobility Care

- 5.1.2 Software

- 5.1.3 Services

- 5.1.3.1 Rehabilitation Services

- 5.1.3.2 Respiratory Therapy Services

- 5.1.3.3 Infusion Therapy Services

- 5.1.3.4 Other Services

- 5.1.1 Equipment

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United states

- 5.2.1.2 Canada

- 5.2.1.3 Mexico

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Italy

- 5.2.2.5 Spain

- 5.2.2.6 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 Japan

- 5.2.3.3 India

- 5.2.3.4 Australia

- 5.2.3.5 South Korea

- 5.2.3.6 Rest of Asia-Pacific

- 5.2.4 Middle-East and Africa

- 5.2.4.1 GCC

- 5.2.4.2 South Africa

- 5.2.4.3 Rest of Middle-East and Africa

- 5.2.5 South America

- 5.2.5.1 Brazil

- 5.2.5.2 Argentina

- 5.2.5.3 Rest of South America

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 3M Healthcare

- 6.1.2 Amedisys Home Health and Hospice Care

- 6.1.3 Amwell

- 6.1.4 Apple Inc.

- 6.1.5 Arkray, Inc.

- 6.1.6 B. Braun Melsungen AG

- 6.1.7 Becton, Dickinson And Company

- 6.1.8 F. Hoffmann-La Roche AG

- 6.1.9 Fresenius SE & Co KGaA

- 6.1.10 Hollister Inc.

- 6.1.11 McKesson Medical-Surgical Inc.

- 6.1.12 Medline Industries, Inc.

- 6.1.13 Medtronic PLC

- 6.1.14 Molnlycke Health Care

- 6.1.15 Resmed Inc.