|

|

市場調査レポート

商品コード

1190390

複合材料市場- 成長、動向、予測(2023年-2028年)Composite Material Market - Growth, Trends, and Forecasts (2023 - 2028) |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| 複合材料市場- 成長、動向、予測(2023年-2028年) |

|

出版日: 2023年01月18日

発行: Mordor Intelligence

ページ情報: 英文 140 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

複合材料市場は、予測期間(2022-2027年)にCAGR4%以上で成長すると予測されています。

2021年の市場は、2020年と比較して増加しています。いくつかの国の閉鎖が解除され、多くの製造業や建設プロジェクトが再開された後、市場はパンデミックの悪影響から部分的に回復しています。Royal Institution of Chartered Surveyorsによると、2021年第3四半期の建設活動は2020年に比べて増加しました。現在の技術の向上と新しい作業形態や世界中の新しいプロジェクトへの適応により、調査された市場は予測期間中に恩恵を受けると予想されます。

主なハイライト

- 複合材料製造におけるナノテクノロジー、アウトオブオートクレーブ(OOA)キュアリングなどの最近の技術的進歩の改善は、市場の成長を促進すると期待されます。

- 航空宇宙、自動車、建設などの産業における技術の進歩に伴い、複合材料の需要が急増しています。

- 北米は最大の市場シェアの1つであり、アジア太平洋地域は予測期間中に最も高い成長率を示すと予想されます。

- 予測期間中は、輸送、建設用途が市場を独占すると予想されます。

主な市場動向

炭素繊維タイプが最も高い成長を遂げる見込み

- 炭素繊維は、自動車からスポーツ用品まで幅広い用途で使用される高度な複合材料であり、航空宇宙、防衛、その他の産業などの最先端産業でも使用されています。

- 炭素繊維は、様々な市場で大きな需要があるため、炭素繊維メーカーの数は年々増加しています。例えば、2021年には米国に58社の炭素繊維メーカーが存在し、10年前の17社から増加しています。

- 比強度や弾性率が高いことから、複合材料は長い間、未来の材料として歓迎され、航空機用途に魅力的な選択肢となっています。最新のボーイング787ドリームライナーでは、複合材の使用比率が50%に達しています。

- CompositesWorldのデータによると、2021年の炭素繊維の生産量は114,100メートルトンです。

- 風力エネルギー産業は、現在、炭素繊維の世界最大の消費者であり、2021年には28000トンに達する見込みです。

- したがって、上記の要因により、炭素繊維は予測期間中に最も高い成長率を記録すると予想されます。

アジア太平洋地域が最も高い成長率を示す

- アジア太平洋地域は、建設、自動車、電気・電子、航空宇宙・防衛、産業などのエンドユーザー産業からの高い需要によって、複合材料市場で最も高いシェアを占めています。

- アジア太平洋地域の複合材料に対する需要は、中国、インド、日本などの国々における急速な工業化の結果として、驚異的な速度で成長しています。

- 複合材料の需要は、様々な産業における用途の増加により、年々急増しています。CompositesWorldによると、先進的な複合繊維である炭素繊維の中国における供給量は、2021年には約19,250トンにのぼると推測されています。

- JECコリアによると、韓国には地元の加工業者や炭素繊維、樹脂のサプライヤーが存在し、強力な複合材料部門があり、韓国は今後も複合材料と方法の革新の最前線に立ち続けるだろうとしています。韓国政府は、同国の炭素繊維セクターの強化に多大な資源を投入しています。

- 軽量で非常に剛性の高い炭素繊維の使用は、環境規制の強化や、持続可能な開発目標(SDGs)およびパリ協定などの環境枠組みの改善によって促進されると予想されます。特にアジアでは、スポーツ・アウトドア、産業、航空機などの領域で需要が高まっていると言われています。

競合情勢

複合材料市場は、多くの企業がシェアを分け合っているため、適度に断片化されています。市場の主要プレイヤー(順不同)には、東レ株式会社、3M、キャボットコーポレーション、デュポン、オーエンス・コーニングなどが挙げられます。

その他の特典

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 材料科学分野における技術的進歩

- 航空宇宙・防衛産業における複合材料の利用拡大

- その他の促進要因

- 抑制要因

- 複合材料のコスト高

- COVID-19パンデミックの悪影響

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の度合い

第5章 市場のセグメンテーション

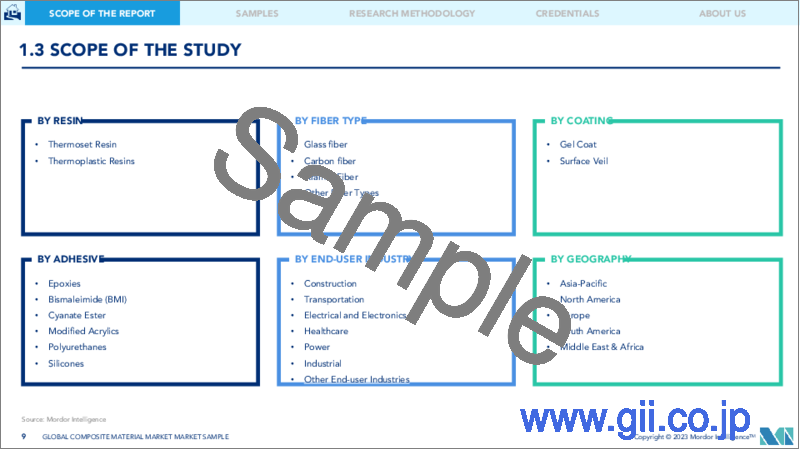

- 樹脂

- 熱硬化性樹脂

- ポリエステル

- エポキシ

- ビニルエステル

- フェノリック

- シアネートエステル

- ポリイミド

- その他熱硬化性樹脂(ビスマレイミド、ベンゾオキサジン)

- 熱可塑性樹脂

- ポリエーテルイミド(PEI)

- ポリエーテルエーテルケトン(PEEK)

- ポリエーテルケトン(PEK)

- ポリアミドイミド(PAI)

- ポリアリールスルホン(PAS)

- 液晶ポリマー(LCP)

- その他熱可塑性樹脂(PES, PPS)

- 熱硬化性樹脂

- 繊維の種類

- ガラス繊維

- 炭素繊維

- アラミド繊維

- その他

- コーティング

- ゲルコート

- サーフェスベール

- 接着剤

- エポキシ樹脂

- ビスマレイミド(BMI)

- シアネートエステル

- 変性アクリル

- ポリウレタン

- シリコーン

- エンドユーザー業界

- 建築

- 運輸

- 電気・電子

- ヘルスケア

- 電力

- 工業

- その他

- 地域別

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- ASEAN諸国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他の南米地域

- 中東・アフリカ地域

- サウジアラビア

- 南アフリカ共和国

- その他中東・アフリカ地域

- アジア太平洋地域

第6章 競合情勢

- M&A、ジョイントベンチャー、提携、契約

- 市場シェア**/ランキング分析

- リーディングプレイヤーが採用する戦略

- 企業プロファイル

- 3M

- DuPont

- DIT B.V.

- COMPOSITES UNIVERSAL GROUP

- Cabot Corporation

- Mitsubishi Chemical Corporation

- Owens Corning

- TEIJIN LIMITED.

- TORAY INDUSTRIES, INC.

第7章 市場機会と今後の動向

The Composite Material Market is projected to register a CAGR of more than 4% during the forecast period (2022-2027).

In 2021 the market has seen an increase when compared to the 2020. After the lifting off lockdowns in several countries and with the resuming of many manufacturing and construction projects the market has partially recovered from the negative affect of pandemic. As per Royal Institution of Chartered Surveyors construction activity in 3rd quarter of 2021 was rising in comparison to 2020. With the improvement in current technology and adaptation to new working format and new projects across the globe the market studied is expected to benefit in the forecasted period.

Key Highlights

- Recent improvements in technological advancements such as Nanotechnology, Out-of-Autoclave (OOA) Curing, and others in composite material manufacturing are expected to drive the growth of the market.

- With advancements of technology in industries such as aerospace, automobile, Construction and other such industries, the demand for composites is on a surge.

- North America is one of the largest market share and Asia-Pacific is expected to have a highest growth rate during the forecasted period.

- Transportation, and Construction applications are expected to dominate the market studied in the forecasted period

Key Market Trends

Carbon Fiber Type to Witness the Highest Growth

- Carbon Fiber is an advanced composite material used in a wide range of applications from Automotive to sports equipment's and even in most advanced industries such as Aerospace, Defense and other industries.

- The number of carbon fiber manufacturers are increasing year on year due to its heavy demand in various markets. For instance in 2021, there are 58 carbon fibre producers in United States, up from 17 in the previous decade.

- Because of their high specific strength and/or modulus, composites have long been hailed as the materials of the future, making them appealing choices for aircraft applications. In the latest Boeing 787 Dreamliner aeroplane, the amount of composites has climbed to 50%.

- According to the data given by CompositesWorld the production of carbon fiber in 2021 is 114,100 metric tonnes.

- The wind energy industry, presently is the world's largest consumer of carbon fibre by volume, summing upto 28000 metric tonnes in the year 2021.

- Hence, owing to the above-mentioned factors, carbon fiber is expected to witness the highest growth rate during the forecast period.

Asia-Pacific to Witness the Highest Growth Rate

- Asia-Pacific region accounts for the highest share of composite material market owing to high demand from end-user industries like construction, automotive, electrical & electronics, aerospace & defense, Industrial, etc.

- The demand for composite material in the Asia-Pacific region is growing at a staggering rate as a result of rapid industrialisation in countries such as China, India, and Japan.

- The demand for composite materials is surging every year with the increase in its application in various industries. In China the supply of Carbon fiber, which is an advanced composite fiber, amounted to around 19,250 metric tonnes in the year 2021 according to CompositesWorld.

- According to JEC Korea, South Korea has a strong composites sector, with local processors and carbon fibre and resin suppliers, and the nation will continue to be at the forefront of composite material and method innovations. The government of South Korea has committed substantial resources to bolstering the country's carbon fibre sector.

- Increased usage of lightweight and extremely stiff carbon fibre is predicted to be stimulated by more rigorous environmental restrictions and the upgrading of environmental frameworks, such as the Sustainable Development Goals (SDGs) and the Paris Agreement. Asia's demand is said to be increasing, particularly in the domains of sports and outdoor activities, industrial, and aircraft.

Competitive Landscape

The composite material market is moderately fragmented as the market share is divided between many players. Key players in the market (not in any particular order) include TORAY INDUSTRIES, INC., 3M, Cabot Corporation, Dupont, and Owens Corning, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Technological Advancement in the Field of Material Science

- 4.1.2 Increasing Use of Composites in the Aerospace and Defense Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 High Cost of Composite Materials

- 4.2.2 Negative Impact of COVID-19 Pandemic

- 4.3 Industry Value-chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION

- 5.1 Resin

- 5.1.1 Thermoset Resin

- 5.1.1.1 Polyester

- 5.1.1.2 Epoxy

- 5.1.1.3 Vinyl Ester

- 5.1.1.4 Pheonolics

- 5.1.1.5 Cyanate Esters

- 5.1.1.6 Polyimides

- 5.1.1.7 Other Thermoset Resins (Bismaleimides, Benzoxazines)

- 5.1.2 Thermoplastic Resins

- 5.1.2.1 Polyetherimide (PEI)

- 5.1.2.2 Polyetheretherketone (PEEK)

- 5.1.2.3 Polyetherketone (PEK)

- 5.1.2.4 Polyamide-imide (PAI)

- 5.1.2.5 Polyarylsulfone (PAS)

- 5.1.2.6 Liquid crystal polymer (LCP)

- 5.1.2.7 Other Thermoplastic Resins ( PES, PPS)

- 5.1.1 Thermoset Resin

- 5.2 Fiber Type

- 5.2.1 Glass fiber

- 5.2.2 Carbon fiber

- 5.2.3 Aramid Fiber

- 5.2.4 Others

- 5.3 Coating

- 5.3.1 Gel Coat

- 5.3.2 Surface Veil

- 5.4 Adhesives

- 5.4.1 Epoxies

- 5.4.2 Bismaleimide (BMI)

- 5.4.3 Cyanate Ester

- 5.4.4 Modified Acrylics

- 5.4.5 Polyurethanes

- 5.4.6 Silicones

- 5.5 End-user Industry

- 5.5.1 Construction

- 5.5.2 Transportation

- 5.5.3 Electrical & Electronics

- 5.5.4 Healthcare

- 5.5.5 Power

- 5.5.6 Industrial

- 5.5.7 Others

- 5.6 Geography

- 5.6.1 Asia-Pacific

- 5.6.1.1 China

- 5.6.1.2 India

- 5.6.1.3 Japan

- 5.6.1.4 South Korea

- 5.6.1.5 ASEAN Countries

- 5.6.1.6 Rest of Asia-Pacific

- 5.6.2 North America

- 5.6.2.1 United States

- 5.6.2.2 Canada

- 5.6.2.3 Mexico

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Rest of Europe

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle-East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 South Africa

- 5.6.5.3 Rest of Middle-East and Africa

- 5.6.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 DuPont

- 6.4.3 DIT B.V.

- 6.4.4 COMPOSITES UNIVERSAL GROUP

- 6.4.5 Cabot Corporation

- 6.4.6 Mitsubishi Chemical Corporation

- 6.4.7 Owens Corning

- 6.4.8 TEIJIN LIMITED.

- 6.4.9 TORAY INDUSTRIES, INC.