|

市場調査レポート

商品コード

1405704

遠隔兵器システム(RWS):市場シェア分析、産業動向・統計、成長予測、2024年~2029年Remote Weapon Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| 遠隔兵器システム(RWS):市場シェア分析、産業動向・統計、成長予測、2024年~2029年 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

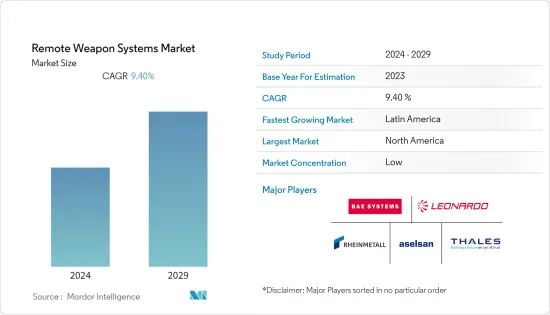

遠隔兵器システム(RWS)市場は2024年に107億8,000万米ドルと評価され、2029年には168億8,000万米ドルに達すると予測され、予測期間(2024-2029年)のCAGRは9.4%を記録すると予想されます。

RWSの使用は、特に非対称戦争の拡大によって、最近になって増加しました。非国家主体が非対称戦争の技術や戦術を採用し始めたのです。従来の軍隊は、現代の戦闘状況や紛争後のシナリオで成功を収めるために、新たな能力を必要としています。この点で、遠隔武器システムの使用は、いくつかの対テロ作戦や対反乱作戦で広まりつつあります。

近年、RWSや無人砲塔には、システムの保護や殺傷能力から大口径への対応に至るまで、いくつかの進歩が見られました。こうした開発は、今後数年間、新兵器システムの調達や既存プラットフォームのアップグレードの増加に役立つと期待されています。RWSは軍隊に防御火力を提供するための実行可能な選択肢として機能するが、設置や運用上の課題があるため、世界の軍隊は遠隔兵器よりも有人砲塔を好むようになっています。しかし、RWSへの先進技術の統合に向けて実施されている広範な研究開発を通じて、こうした運用上の制約が将来的に解決されることが期待されています。

遠隔兵器システム(RWS)市場の動向

陸上セグメントが、予測期間中に最も高いCAGRで成長する見込み

予測期間中、陸上セグメントが最も高いCAGRを示すと予測されています。陸上セグメントには、陸上車両に静止して搭載されるRWSが含まれます。最近、軍事基地や前哨基地への攻撃が増加しており、脆弱な地域を守るための遠隔操作定置型兵器ステーションの需要が高まっています。

予測期間中は陸上セグメントが市場を独占すると予想されているが、現在、2023年のRWS市場では空挺セグメントが最大のシェアを占めています。多くの国では、RWSを含む幅広い兵装を搭載した専用の攻撃ヘリコプターが導入されているが、兵器システムは実用ヘリコプターや輸送ヘリコプターにも搭載されています。後付けでRWSを搭載するための航空機のカスタマイズは、専用の攻撃ヘリコプターを調達する資金が不足している国々によって広く採用されており、このセグメントは現在最も高い市場シェアを獲得しています。

定置式の陸上RWS、特にセントリーガンは、一部の国の国境警備にも使用されています。加えて、装甲車や無人地上車両の調達増加により、これらの地上車両に搭載されるRWSの需要が必要となりました。無人の陸上車両の採用が増加していることから、予測期間中にこれらのシステムの高い採用が予想されます。これらすべての要因が、現在の陸上セグメントの成長に寄与しています。

北米が市場シェアを独占

米国とカナダは北米における遠隔兵器システム(RWS)の熱心なユーザーです。彼らは現在、既存の車両とそれに対応する能力のアップグレードに注力しています。

新たな脅威に対抗するために既存の車両の能力をアップグレードする必要があるため、軍隊の多様なニーズに対応するための契約が次々と結ばれています。例えば、米国陸軍は2022年11月、Kongsberg Defence &Aerospaceに15億米ドルの契約を発注し、共通遠隔操作武器ステーション(CROWS)の供給を継続させました。CROWSは、装甲車両内で遮蔽されながら、移動中の目標捕捉や火炎放射を行うことができる装甲マウントです。

このような調達プログラムは、他のアップグレードプログラムとともに、今後開始されることが予想され、予測期間中に北米遠隔兵器システム(RWS)市場の事業見通しを強化することが想定されています。

遠隔兵器システム(RWS)産業の概要

遠隔兵器システム(RWS)市場は、世界中の軍隊の遠隔兵器システム(RWS)の要件に対応する多くの世界および地域の防衛メーカーやサプライヤーの存在により、断片化されています。同市場では、約13社が市場シェアの約50%を占めています。THALES社、BAE Systems plc社、Rheinmetall AG社、Leonardo S.p.A.社、ASELSAN A.S.社が市場を独占しています。その他、中国兵器工業集団公司(China Ordnance Industries Group Corporation Limited)、ロステック社(Rostec State Corporation)、L3ハリス・テクノロジーズ社(L3Harris Technologies Inc.)、イスラエル航空宇宙産業社(Israel Aerospace Industries Ltd.)、パトリア・グループ(Patria Group)、KMW+ネクスター・ディフェンス・システムズ社(KMW+Nexter Defense Systems)などが、地方・地域市場の有力企業です。

例えば、2023年3月、ジェネラル・ダイナミクス・ヨーロピアン・ランド・システムズ(GDELS)は、ルーマニア軍の「ピラニアV」装甲兵員輸送車(APC)向けに無人砲塔、遠隔操作武器ステーション(RCWS)、迫撃砲システムを供給する1億2,000万米ドル相当の後続契約をエルメット・インターナショナルSRL(エルビット・システムズの子会社)に発注しました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 市場の課題

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- プラットフォーム

- 陸上

- 陸上車両

- 定置式

- 海上

- 空挺

- 陸上

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- フランス

- ドイツ

- イタリア

- ロシア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- トルコ

- 南アフリカ

- その他中東・アフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Kongsberg Gruppen ASA

- Elbit Systems Ltd.

- Rafael Advanced Defense Systems Ltd.

- RTX Corporation

- Saab AB

- Leonardo S.p.A

- Electro Optic Systems Pty Ltd.

- ASELSAN A.S.

- General Dynamics Corporation

- BAE Systems plc

- China Ordnance Industries Group Corporation Limited

- THALES

- Rostec

- Herstal Group

- Rheinmetall AG

- Hanwha Group

- Singapore Technologies Engineering Ltd.

- Moog Inc.

- Israel Aerospace Industries Ltd.

- Nexter Group

- Norinco Group

第7章 市場機会と今後の動向

The Remote Weapon Systems (RWS) Market is valued at USD 10.78 billion in 2024 and is expected to reach USD 16.88 billion by 2029, registering a CAGR of 9.4% during the forecast period (2024-2029).

The use of RWS grew over the recent past, particularly driven by the growth in asymmetric warfare. Non-state actors started employing the techniques and tactics of asymmetric warfare. Conventional forces require new capabilities to become successful in modern combat situations and post-conflict scenarios. In this regard, the use of remote weapon systems is becoming widespread in several anti-terrorist and counter-insurgency operations.

There were several advancements in RWS and unmanned turrets in recent years, ranging from the protection of the systems and lethality to the support of larger calibers. Such developments are expected to help the growth in the procurement of new weapon systems and upgrades of the existing platforms in the years to come. Though RWS acts as a viable option for providing defensive firepower to the armed forces, certain installation and operational challenges are influencing the global militaries to prefer manned turrets over remote weapons. However, it is expected that these operational limitations will be addressed in the future through the extensive R&D being conducted towards the integration of advanced technologies into the RWS.

Remote Weapon Systems Market Trends

The Land Segment is Projected to Register the Highest CAGR During the Forecast Period

The land segment is anticipated to show the highest CAGR during the forecast period. The land segment encompasses the RWS that is stationary and mounted on land vehicles. The increase in attacks on military bases and outposts in the recent past increased the demand for remotely operated stationary weapon stations for protecting vulnerable areas.

Despite the land segment being expected to dominate the market during the forecast period, currently, the airborne segment had the largest share in the RWS market in 2023. While many countries include dedicated attack helicopters that possess a wide range of armaments, including the RWS, the weapon systems are also attached to utility and transport helicopters. Customization of aircraft to include the RWS as a retrofit is being widely adopted by the countries that lack the funds for procuring dedicated attack helicopters, making the segment grab the highest market share currently. For instance, in November 2022, Kongsberg Defence & Aerospace teamed up forces with Thales UK to support the Protector Remote Weapon Systems (RWS) program of the British armed forces. The firms will collaborate on numerous capacities for the weapon system's maturity in the UK military and foreign markets under the terms of the agreement. The Protector RWS is promoted globally by Kongsberg and Thales, with around 1,000 of the weapon systems being integrated into British defense.

Stationary Land RWS, especially sentry guns, are also being used to guard the borders of some countries. In addition, the growth in the procurement of armored vehicles and unmanned ground vehicles necessitated the demand for the RWS installed on these ground vehicles. With the increasing adoption of unmanned land vehicles, high adoption of these systems is expected during the forecast period. All these factors are contributing to the growth of the land segment currently.

North America Dominated Market Share

The United States and Canada are avid users of remote weapon systems in North America. They are currently focusing on upgrading their existing vehicle fleet and their corresponding capabilities.

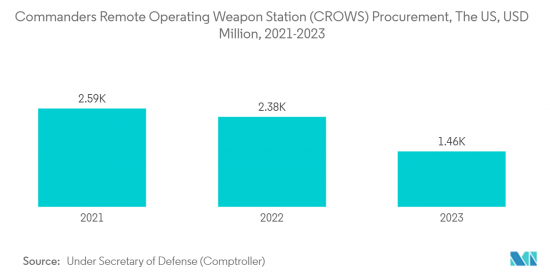

The need for upgrading the capabilities of the existing fleet to counter emerging threats resulted in a flurry of contracts being awarded to cater to the diversified needs of the armed forces. For instance, in November 2022, the US Army awarded a USD 1.5 billion contract to Kongsberg Defence & Aerospace to continue its supply of Common Remotely Operated Weapon Stations (CROWS). CROWS are armored mounts that can perform on-the-move target acquisition and fire-burst strikes while being shielded inside armored vehicles. The company will deliver its Kongsberg Protector remote weapon station family, which is also used by NATO and ally forces, under the five-year arrangement. Likewise, in January 2023, Rheinmetall Systems and Kongsberg Defence & Aerospace signed a framework agreement to produce subsystems for the US Army's Common Remotely Operated Weapon Station (CROWS) program. The five-year framework deal covers the provision of high-definition image-stabilized EO sensors (day cameras), weapon mounts, and other assemblies.

Such procurement programs, along with other upgrade programs, are anticipated to be initiated in the upcoming period and are envisioned to enhance the business prospects of the North American remote weapon systems market during the forecast period.

Remote Weapon Systems Industry Overview

The remote weapon systems market is fragmented due to the presence of many global as well as regional defense manufacturers and suppliers that cater to the requirements of remote weapon systems of armed forces around the world. About 13 players in the market account for approximately 50% of the market share. THALES, BAE Systems plc, Rheinmetall AG, Leonardo S.p.A., and ASELSAN A.S. are the dominant players in the market. Some of the other prominent players in the local and regional markets are China Ordnance Industries Group Corporation Limited, Rostec State Corporation, L3Harris Technologies Inc., Israel Aerospace Industries Ltd., Patria Group, and KMW+Nexter Defense Systems, among others. With the growing demand for remote-control weapon systems, the innovation of new systems with advanced sensor systems and optronic equipment in fire control systems to target, track, and hit the target is anticipated to increase. It is thereby helping the companies expand their geographical presence in emerging markets.

For instance, in March 2023, General Dynamics European Land Systems (GDELS) awarded Elmet International SRL (a subsidiary of Elbit Systems) a follow-on contract worth USD 120 million to supply unmanned turrets, Remote Controlled Weapon Stations (RCWS), and mortar systems for the Romanian Armed Forces 'Piranha V' Armored Personnel Carrier (APC).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Challenges

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Platform

- 5.1.1 Land

- 5.1.1.1 Land Vehicles

- 5.1.1.2 Stationary Structures

- 5.1.2 Marine

- 5.1.3 Airborne

- 5.1.1 Land

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.2 United States

- 5.2.1.3 Canada

- 5.2.2 Europe

- 5.2.2.1 United Kingdom

- 5.2.2.2 France

- 5.2.2.3 Germany

- 5.2.2.4 Italy

- 5.2.2.5 Russia

- 5.2.2.6 Rest of the Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Japan

- 5.2.3.4 South Korea

- 5.2.3.5 Australia

- 5.2.3.6 Rest of the Asia Pacific

- 5.2.4 Latin America

- 5.2.4.1 Brazil

- 5.2.4.2 Mexico

- 5.2.5 Middle East and Africa

- 5.2.6 United Arab Emirates

- 5.2.7 Saudi Arabia

- 5.2.8 Turkey

- 5.2.9 South Africa

- 5.2.10 Rest of Middle East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Kongsberg Gruppen ASA

- 6.2.2 Elbit Systems Ltd.

- 6.2.3 Rafael Advanced Defense Systems Ltd.

- 6.2.4 RTX Corporation

- 6.2.5 Saab AB

- 6.2.6 Leonardo S.p.A

- 6.2.7 Electro Optic Systems Pty Ltd.

- 6.2.8 ASELSAN A.S.

- 6.2.9 General Dynamics Corporation

- 6.2.10 BAE Systems plc

- 6.2.11 China Ordnance Industries Group Corporation Limited

- 6.2.12 THALES

- 6.2.13 Rostec

- 6.2.14 Herstal Group

- 6.2.15 Rheinmetall AG

- 6.2.16 Hanwha Group

- 6.2.17 Singapore Technologies Engineering Ltd.

- 6.2.18 Moog Inc.

- 6.2.19 Israel Aerospace Industries Ltd.

- 6.2.20 Nexter Group

- 6.2.21 Norinco Group