|

市場調査レポート

商品コード

1405372

民間航空機用頭上収納箱の市場:市場シェア分析、産業動向と統計、2024~2029年の成長予測Commercial Aircraft Overhead Stowage Bins - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| 民間航空機用頭上収納箱の市場:市場シェア分析、産業動向と統計、2024~2029年の成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

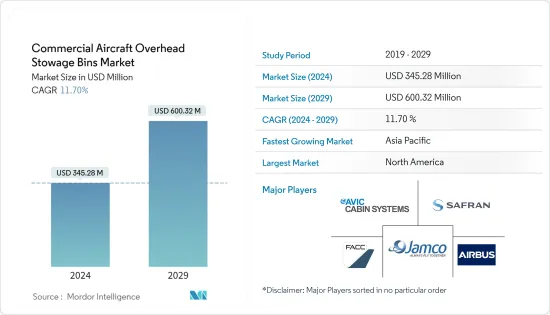

民間航空機用頭上収納箱の市場規模は2024年に3億4,528万米ドルと推計され、2029年には6億32万米ドルルに達すると予測され、予測期間(2024-2029年)のCAGRは11.70%で成長する見込みです。

頭上収納箱は、モーションコントロールと収納性の面で、イントロダクション以来長い道のりを歩んできました。設計は、乗客の機内持ち込み手荷物の種類と量、およびビンの容量増加に対する需要に合わせて進化してきました。航空会社は、より多くの旅行者が快適に過ごせるよう、機内スペースの最大化に注力しています。OEMは航空会社と密接に協力し、旅客の需要に合うような大型で軽量、そして美しいデザインの新しいオーバーヘッドビンを開発しています。これらの開発はまた、航空会社にプレミアム収納オプションを通じて追加収入を得る機会を提供します。

オーバーヘッド収納ボックスは、すべての民間旅客機に装備されているため、旅客機利用率の上昇につながる旅客数の増加に伴い、新型機の納入増加に伴い需要が増加しています。メーカーが航空会社と乗客の進化するニーズに応えようと努力しているため、新しい航空機プログラムと客室改修プロジェクトが市場成長の原動力になると予想されます。

しかし、搭乗離陸時間の短縮に伴い、多くの航空会社がチェックイン用手荷物設備のみの導入を推進しているため、航空機内の収納ボックスに対する航空会社の需要は減少しています。

民間航空機用頭上収納箱の市場動向

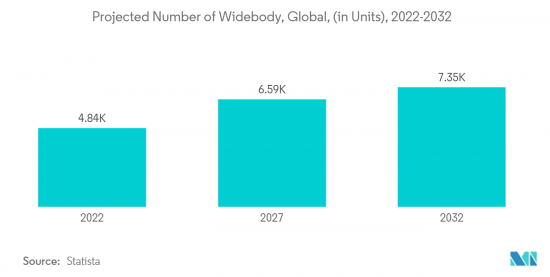

予測期間中、ワイドボディ機セグメントが主要シェアを占めると予測

ワイドボディ機は、移動時間が長いという特徴を持つ長距離便や国際便に主に選ばれています。このような旅では、乗客は大型の機内持ち込み手荷物を含め、より多くの手荷物を携行する傾向があります。そのため航空会社は、ワイドボディ機の余裕のある頭上収納力を利用して、こうした旅行者の収納ニーズに応えています。ワイドボディ機は、より広々とした座席配置と、より大きな頭上収納箱を提供するよう設計されており、より快適でリラックスした機内体験に貢献しています。満足度の高い乗客は、快適さのニーズを優先する航空会社を選ぶ傾向が高いです。例えば、A350にヒントを得たエアバスのA330neoの頭上収納は、大幅に大型化されています。より多くの荷物を収納できるよう、66%のスペースが追加されています。プレミアム・キャビンでは、A330neoの広々とした環境を増幅させるため、センター収納は設置されていません。エアバスA350は大型の頭上収納コンパートメントを備えており、乗客はより多くの手荷物(全クラスで乗客1人につき最低1個のローラーバッグ)を収納することができ、ストレスのない搭乗と飛行中のアクセスが容易になります。

同様に、ボーイングはB737MAX型機のオプション装備としてスペース・ビンを提供しています。スペース・ビンは標準サイズの手荷物を6個収納可能で、B737NG数機に搭載されている現行の大型のボーイング・スカイインテリア・ピボット・ビンを2個上回ります。世界中の様々な航空会社からワイドボディ機の発注が増加しているため、より多くの収納ボックスの需要が高まると思われます。例えば、2023年5月、エア・インディアは、ボーイングから20機のB787ドリームライナーと10機のB777X、エアバスから34機のA350-1000と6機のA350-900を含む70機のワイドボディ機を発注しました。

予測期間中、アジア太平洋地域が最も高い需要を生み出す可能性が高い

アジア太平洋地域では、急増する中産階級人口、可処分所得の増加、観光業の拡大などを背景に、航空旅行が大幅に増加しています。この旅客数の増加は、機内持ち込み手荷物の増加に伴う頭上収納箱の需要増に直結します。アジア太平洋地域は近い将来、航空市場において高い成長率を達成すると予想されています。国際航空運送協会(IATA)によると、2030年までにアジアの航空旅客数は、北米と欧州の2大市場を上回ります。このような旅客輸送量の高い成長率に伴い、この地域の航空会社は需要の増加に対応するために新しい航空機を調達する必要があります。

さらに、アジア太平洋地域の航空会社は、運航効率と旅客満足度を向上させるため、航空機の購入と近代化にますます投資しています。この近代化の一環には、頭上の収納ボックスを含む客室を、利便性と美観の最新基準に適合するようアップグレードすることも含まれます。中国、インド、日本、韓国の航空会社は、航空機の拡張と近代化プログラムの一環として、航空機OEMにナローボディ機とワイドボディ機を大量に発注しています。たとえば、ボーイングは2021年2月、タタ・グループとの合弁会社であるタタ・ボーイング・エアロスペース・リミテッド(TBAL)のハイデラバード工場(インド)に、B737 MAXファミリーの複雑な垂直尾翼を製造するための新たな製造ラインを設置すると発表しました。さらに、2023年2月現在、エア・インディア、インディゴなどインドの民間航空会社は、各航空機メーカーから1,100機の航空機発注を保留しています。航空機の受注と納入の増加に伴い、予測期間中、この地域から頭上収納箱の需要が同時に発生する可能性が高いです。

民間航空機用頭上収納箱産業の概要

民間航空機の頭上収納箱市場は統合されており、Airbus SE、FACC AG、Safran、AVIC Cabin Systems(UK)Limited、JAMCO Corporationなどの主要企業があります。これらは、民間航空機用頭上収納箱や関連部品のメーカーの一部です。新しい航空機モデルのイントロダクション伴い、革新的なソリューションや製品を提供できる企業は、長期的な契約を獲得できるという利点があります。また、航空機OEMが独自のオーバーヘッドビンを開発・設計するための投資を増やしていることは、オーバーヘッドビンメーカーの世界市場シェアにある程度影響を与える可能性があります。例えば、エアバスは2023年6月、A220ファミリーの顧客に新しいキャビン機能を備えた新しいAirspaceキャビンを提供することを決定しました。このため、ディール・アビエーションは、A220型機用の新しいオーバーヘッド・ビンとドア部分を開発する可能性が高いです。エアスペースXLビンと呼ばれるA220用のDiehlの新しいオーバーヘッドビンは、収納容量が20%増加します。軽量化されたAirspace XLオーバーヘッドビンは、ターンアラウンドタイムの短縮にも貢献し、キャビン構造全体の重量を約300ポンド削減します。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手・消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 航空機タイプ

- ナローボディ機

- ワイドボディ機

- リージョナル機

- フィット

- ラインフィット

- レトロフィット

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- フランス

- ジェミニ

- ロシア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- メキシコ

- ブラジル

- その他ラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- エジプト

- 南アフリカ

- その他中東とアフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Airbus SE

- FACC AG

- Safran

- The Boeing Company

- JAMCO Corporation

- AVIC Cabin Systems(UK)Limited's

- ITT Inc.

- Diehl Stiftung & Co. KG

- Hong Kong Aircraft Engineering Company Limited

第7章 市場機会と今後の動向

The Commercial Aircraft Overhead Stowage Bins Market size is estimated at USD 345.28 million in 2024, and is expected to reach USD 600.32 million by 2029, growing at a CAGR of 11.70% during the forecast period (2024-2029).

Overhead stowage bins have come a long way since their introduction in terms of motion control and storability. The design has evolved with the type and quantity of passenger carry-on baggage and the demand for increased bin capacities. Airlines are focusing on maximizing cabin space to accommodate more travelers comfortably. OEMs are working closely with airlines to develop new overhead bins that are large, lightweight, and aesthetically designed to suit passenger demands. These developments also provide airlines with opportunities to generate additional revenue through premium storage options.

Overhead stowage bins are provided on every commercial passenger aircraft, and hence, their demand is increasing with the increasing deliveries of new aircraft as an increasing number of passengers are taking to the skies, leading to higher aircraft utilization rates. New aircraft programs and cabin refurbishment projects are expected to drive market growth as manufacturers strive to meet the evolving needs of airlines and passengers alike.

However, in accordance with decreasing the boarding deplaning time, many airlines are promoting only check-in luggage facilities in their airlines, which offers a decrease in demand from such airlines for storage bins in the aircraft.

Commercial Aircraft Overhead Stowage Bins Market Trends

Wide-body Aircraft Segment is Estimated to Hold a Major Share During the Forecast Period

Widebody aircraft are predominantly chosen for long-haul and international flights, which are characterized by extended travel times. Passengers on such journeys tend to carry more luggage, including larger carry-on items. Consequently, airlines rely on the generous overhead storage capacity of widebody aircraft to meet the storage needs of these travelers. Widebody aircraft are designed to offer more spacious seating arrangements and larger overhead bins, contributing to a more comfortable and relaxed in-flight experience. Satisfied passengers are more likely to choose airlines that prioritize their comfort needs. For example, Airbus' overhead storage for the A330neo, inspired by the A350, is substantially larger. It offers an additional 66% space for more luggage. In the premium cabin, there is no center stowage installed to amplify the spacious environment of the A330neo. Airbus A350 features large overhead storage compartments; passengers can store more hand luggage - a minimum of one roller bag per passenger in all classes - for stress-free boarding and easier access in flight.

Similarly, Boeing offers its Space Bins as an optional feature on its B737MAX aircraft. Space bins can hold six standard-sized bags, which is two more than the large current Boeing Sky Interior pivot bins installed on several B737NGs. An increase in widebody aircraft orders from various airlines across the globe will likely fuel the demand for more storage bins. For instance, In May 2023, Air India placed orders for 70 widebody aircraft, including 20 B787 Dreamliners and 10 B777Xs from Boeing, as well as 34 A350-1000s and six A350-900s from Airbus.

Asia-Pacific Region is likely to Generate the Highest Demand During the Forecast Period

Asia-Pacific is witnessing a significant surge in air travel, driven by a burgeoning middle-class population, increased disposable income, and expanding tourism. This growth in passenger numbers directly correlates with higher demand for overhead storage bins, as more travelers carry cabin luggage. The Asia-Pacific region is expected to achieve a high growth rate in the aviation market in the near future. According to the International Air Transport Association (IATA), air travel in Asia will be greater than the next two biggest markets, North America and Europe, by 2030. With such a high rate of growth in terms of passenger traffic, the airlines in the region need to procure new aircraft to cater to the increasing demand.

Moreover, Airlines in the Asia-Pacific region are increasingly investing in purchasing and modernizing their aircraft fleets to improve operational efficiency and passenger satisfaction. Part of this modernization includes upgrading the cabin, including overhead storage bins, to meet the latest standards in convenience and aesthetics. The airlines in China, India, Japan, and South Korea have huge order books for narrow-body and wide-body aircraft to aircraft OEMs as a part of fleet expansion and modernization programs. For instance, in February 2021, Boeing announced a new production line at the Hyderabad facility (India) of its joint venture with the Tata Group, Tata Boeing Aerospace Limited (TBAL), to manufacture complex vertical Fin for B737 MAX family aircraft. Moreover, as of February 2023, Indian private airlines such as Air India, Indigo, and others have 1,100 pending aircraft orders from various aircraft manufacturers. With the increasing aircraft orders and deliveries, simultaneous demand is likely to be generated for overhead stowage bins from this region during the forecast period.

Commercial Aircraft Overhead Stowage Bins Industry Overview

The commercial aircraft overhead stowage bins market is consolidated and has a few key players like Airbus SE, FACC AG, Safran, AVIC Cabin Systems (UK) Limited, and JAMCO Corporation. These are some of the manufacturers of overhead stowage bins and associated components for commercial aircraft. With the introduction of new aircraft models, companies that can offer innovative solutions and products have the advantage of receiving long-term contracts. Also, the increasing investments by aircraft OEMs in developing and designing their own overhead bins can, to some extent, impact the market share of manufacturers of overhead bins globally. For instance, in June 2023, Airbus decided to offer their new Airspace cabin to A220 family customers with a set of new cabin features. For this, Diehl Aviation will likely develop new overhead bins and the door area for the A220 aircraft. The new Diehl overhead bins for the A220, which are called Airspace XL Bins, will offer 20% more storage capacity. The lighter Airspace XL overhead bins will also support faster turnaround times and will decrease the overall weight of the cabin structure by around 300 lbs.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Aircraft Type

- 5.1.1 Narrow-body Aircraft

- 5.1.2 Wide-body Aircraft

- 5.1.3 Regional Aircraft

- 5.2 Fit

- 5.2.1 Line-fit

- 5.2.2 Retrofit

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 France

- 5.3.2.3 Gemany

- 5.3.2.4 Russia

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Mexico

- 5.3.4.2 Brazil

- 5.3.4.3 Rest of Latin America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Egypt

- 5.3.5.4 South Africa

- 5.3.5.5 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Airbus SE

- 6.2.2 FACC AG

- 6.2.3 Safran

- 6.2.4 The Boeing Company

- 6.2.5 JAMCO Corporation

- 6.2.6 AVIC Cabin Systems (UK) Limited's

- 6.2.7 ITT Inc.

- 6.2.8 Diehl Stiftung & Co. KG

- 6.2.9 Hong Kong Aircraft Engineering Company Limited

7 MARKET OPPORTUNITIES AND FUTURE TRENDS