|

|

市場調査レポート

商品コード

1405357

軍用ナビゲーションシステム:市場シェア分析、産業動向と統計、2024~2029年の成長予測Military Navigation Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| 軍用ナビゲーションシステム:市場シェア分析、産業動向と統計、2024~2029年の成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

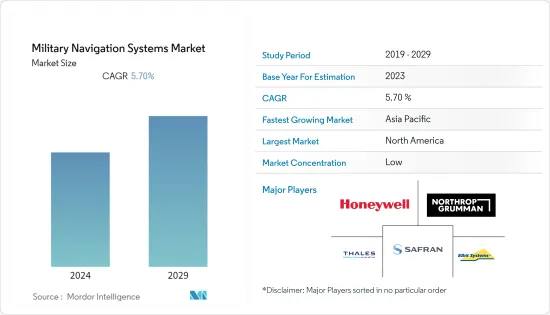

軍用ナビゲーションシステム市場は、2024年に92億5,000万米ドルと評価され、2029年には122億1,000万米ドルに達すると予測され、予測期間中(2024~2029年)のCAGRは5.7%で成長する見込みです。

各国の軍事費の増加は、情報、監視、偵察から戦闘、戦場に至るまで、軍事作戦のための幅広い製品に対する各国政府のそれぞれの調達計画を支えています。このような有人・無人システム、精密誘導弾の調達計画は、今後数年間、軍事分野におけるナビゲーションシステム市場の需要を牽引すると予想されます。

軍備をアップグレードするための軍隊の近代化計画は、予測期間中にナビゲーションシステムの販売をさらに推進すると予想されます。小型、軽量、低消費電力で、(GNSS妨害やスプーフィングがあっても)正確な測位が可能な新しいナビゲーションシステムの開拓は、予測期間中、市場の成長を生み出し、強化する上で企業の助けになると予想されます。

軍事用ナビゲーションのイントロダクションは、無人システムの誘導特性だけでなく、武器の選択、戦場での物資の運搬、指揮、制御の改善に役立った。航空分野の多くの用途に使用される高性能ナビゲーションシステムは、非常に特殊な誘導と精度を必要とし、需要が高まっています。幅広い用途に精密に配置されたこれらのシステムは、航空・海上航行を含む多くの種類の戦争で採用されています。

軍用ナビゲーションシステム市場の動向

航空セグメントが市場シェアの優位性を維持すると予測

世界中の軍隊は、新しい航空機やUAVの調達に多額の投資を行っています。航空機の多くはGNSS(GPS)とTACANの測位・ナビゲーションシステムを使用しています。このセグメントの収益の大部分は、老朽化した航空機を新しく正確な位置・ナビゲーションシステムで近代化することによるものです。例えば、2023年6月、Airbus Helicoptersは、フランスとスペインの軍隊が配備する航空機用のSkyNauteナビゲーションシステムをSafran Electronics &Defenseに発注しました。SkyNauteは、サフランの特許技術であるクリスタルHRG(半球共振ジャイロ)技術をベースとした超小型ハイブリッド慣性航法システムです。SkyNauteは非常に軽量かつコンパクトな設計で、高い信頼性と精度を兼ね備えています。SkyNauteナビゲーションシステムは、衛星ナビゲーションの信号がない、あるいは妨害されている環境においても、卓越した信頼性を発揮します。様々な軍による同様の取り組みが、予測期間中のこのセグメントの成長を促進すると予想されます。

さらに、航空機用の新しい航法補助装置の開拓は、企業にとって新たな市場機会を開くと予想されます。同様に、2023年5月、米国空軍は、B-2爆撃機から発射するための赤外線シーカー技術を搭載したJASSM-ER GPS誘導ミサイルを製造するために、ロッキード・マーティン・コーポレーションに7億5,000万米ドルの契約を発注しました。JASSM-ERは2,250ポンドの巡航ミサイルで、悪天候、昼夜を問わず精密な経路誘導を行う。アンチジャムGPSに加えて赤外線シーカーを使用し、標的の特定の照準点を見つける。

予測期間中、アジア太平洋が最も高い需要を生み出すと予測されています。

中国、インド、韓国などの国々における軍事費の着実な伸びが、軍備の調達と近代化計画を大きく後押ししています。中国には、日本、韓国、台湾との地域的な緊張関係があります。こうした対立が、中国とその周辺国の軍事近代化計画への投資につながった。アジア太平洋諸国の大半は、軍事プラットフォームの近代化を進めています。各国は新たな航空機を調達して航空戦力を増強し、新たな艦船を調達して海上ISR能力を強化しています。現在、有人能力とともに、各国は無人能力の開発とアップグレードにも取り組んでいます。例えば、2022年9月、ロシアと中国は、ロシアのグロナス局を中国に、中国の北斗システム局をロシアに配備する契約に調印しました。ロシアのグロナス・ステーションは長春、ウルムチ、上海に、中国のステーションはオブニンスク、イルクーツク、ペトロパブロフスク・カムチャツキーに設置されます。米国の全地球測位システム(GPS)に代わるBeiDouとGLONASSは、システムの性能を向上させる。これは、軍事・民生両方の目的で、精密・航法・タイミング(PNT)サービスを提供するものです。同様に2023年7月、Elbit Systemsは、無名のアジア太平洋諸国に長距離哨戒機(LRPA)2機を供給する5年契約1億1,400万米ドルを獲得しました。LRPA航空機は、ミッション管理システム、電気光学、レーダー、信号情報(SIGINT)、通信を含む包括的なミッション・スイートと統合されます。

軍用ナビゲーションシステム業界概要

軍用ナビゲーションシステム市場は細分化されており、多様な軍事作戦のためにさまざまな軍事プラットフォームにさまざまなナビゲーション・コンポーネントを提供する多くの参入企業が市場に存在します。軍用ナビゲーションシステム市場の主要企業は、Northrop Grumman Corporation、Safran、THALES、Honeywell International Inc.、Elbit Systems Ltd.です。同市場における収益シェアを拡大するため、各参入企業は新製品を開発し、さまざまなプラットフォームに製品ポートフォリオを拡大しています。例えば、Northrop Grumman Corporationは、固定翼や回転翼の航空機、船舶、水中車両、陸上車両、衛星、ミサイルなど、さまざまなプラットフォームにナビゲーション・測位システムを提供しています。このような膨大なポートフォリオを持つ同社は、様々なプラットフォームメーカーの要求に応えることができると期待されています。

さらに、低消費電力、小型軽量で先進的な新型ナビゲーション・測位システムの開発が、企業の成長を後押しすると予想されています。例えば、2023年1月、エンタープライズSaaS企業であるSandboxAQは、量子ナビゲーション技術を研究するため、米国空軍からDirect-to-Phase-II Small Business Innovation Research(SBIR)契約を獲得しました。この契約により、AQの量子センサーのプロトタイプが米国空軍との緊密な連携のもと最適化されます。同様に2023年7月、オーストラリア国防省は、軍事プラットフォーム用の量子センサーを開発するため、Q-CTRL(オーストラリア)に数100万米ドルの契約を発注しました。このプログラムは、Q-CTRLのソフトウェアで堅牢化された量子センシング技術をベースに、量子的に強化された測位・ナビゲーション能力を構築することを目的としています。これは、加速度や重力場の微小な変化を検出し、信号からノイズを除去することができます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手・消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- プラットフォーム

- 航空

- 陸上

- 海上

- 宇宙

- 用途

- コマンド&コントロール(C2)

- 情報、監視、偵察(ISR)

- 照準と誘導

- 捜索・救助

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- フランス

- ドイツ

- イタリア

- ロシア

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- ラテンアメリカ

- メキシコ

- ブラジル

- その他のラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- エジプト

- 南アフリカ

- その他の中東・アフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Northrop Grumman Corporation

- Safran

- Elbit Systems Ltd.

- Honeywell International Inc.

- THALES

- Collins Aerospace(RTX Corporation)

- KVH Industries, Inc.

- CMC Electronics Inc.

- General Electric Company

- Israel Aerospace Industries Limited

- Anschotz GmbH

- Moog Inc.

- Lockheed Martin Corporation

第7章 市場機会と今後の動向

The Military Navigation Systems Market is valued at USD 9.25 billion in 2024 and is expected to reach USD 12.21 billion by 2029, growing at a CAGR of 5.7% during the forecast period (2024-2029).

The increasing military spending of the countries is supporting their governments' respective procurement plans for a wide range of products for military operations from intelligence, surveillance, and reconnaissance to combat and battlefield. Such procurement plans for manned and unmanned systems, along with precision-guided munitions, are anticipated to drive the demand for the navigation systems market in the military sector in the coming years.

The modernization plans of the armed forces to upgrade their military equipment are anticipated to further propel the sales of the navigation systems during the forecast period. The development of new navigation systems that can provide accurate positioning (even in case of GNSS jamming or spoofing), with compact size, lightweight, and low power consumption, is anticipated to help the companies in generating and bolstering the growth of the market during the forecast period.

The introduction of military navigation helped to improve the selection of weapons, delivery of supplies on the battlefield, commandership, and control, as well as guidance characteristics for an unmanned system. High-performance navigation systems for a large number of applications in the aviation sector require very specific guidance and accuracy and are increasingly in demand. These systems, which are precisely placed for a wide range of applications, are employed in many types of warfare, including air and sea navigation.

Military Navigation Systems Market Trends

The Air Segment is Projected to Retain Market Share Dominance

The armed forces around the world are significantly investing in the procurement of new aircraft and UAVs. Most of the aircraft use GNSS (GPS) and TACAN positioning and navigation systems. The majority of the revenue of the segment is through the modernization of the aging fleet of aircraft with new and accurate positions and navigation systems. For instance, in June 2023, Airbus Helicopters awarded a contract to Safran Electronics & Defense for the SkyNaute navigation system for the aircraft to be deployed by French and Spanish armed forces. SkyNaute is an ultra-compact hybrid inertial navigation system based on Safran's patented Crystal HRG (hemispherical resonator gyro) technology. SkyNaute offers an extremely lightweight and compact design, combining high integrity and precision. The SkyNaute navigation system delivers outstanding reliability, even in environments where satellite navigation signals are absent or jammed. Similar initiatives from various armed forces are anticipated to propel the growth of the segment during the forecast period.

Furthermore, the development of new navigational aids for the aircraft is anticipated to open new market opportunities for the companies. Similarly, in May 2023, the US Air Force awarded a USD 750 million contract to Lockheed Martin Corporation to build JASSM-ER GPS-guided missiles with infrared seeker technology for launch from B-2 bombers. The JASSM-ER is a 2,250-pound cruise missile that uses precision routing and guidance in adverse weather, day or night. It uses an infrared seeker in addition to the anti-jam GPS to find a specific aim point on the target.

Asia-Pacific is Projected to Generate the Highest Demand During the Forecast Period

The steady growth of military spending in countries such as China, India, and South Korea, among others, is majorly driving the procurement and modernization plans of military equipment. China includes regional tensions with Japan, South Korea, and Taiwan. These conflicts led China and its neighboring countries to invest in military modernization programs. The majority of the Asia-Pacific countries are modernizing their military platforms. The countries are procuring new aircraft to increase their air strength and strengthen their sea ISR capabilities by procuring new ships. Currently, along with manned capabilities, the countries are also involved in developing and upgrading their unmanned capabilities. For instance, in September 2022, Russia and China signed contracts for the deployment of Russia's GLONASS stations in China and China's BeiDou system stations in Russia. Russia's GLONASS stations will be in Changchun, Urumqi, and Shanghai, and the Chinese ones will be in Obninsk, Irkutsk, and Petropavlovsk-Kamchatsky. BeiDou and GLONASS, which are alternatives to the United States' Global Positioning System (GPS), will improve the performance of their systems. It provides precision, navigation, and timing (PNT) services for both military and civilian purposes. Similarly, in July 2023, Elbit Systems won a 5-year USD 114 million contract to supply two long-range patrol aircraft (LRPA) to an unnamed Asian-Pacific nation. The LRPA aircraft will be integrated with a comprehensive mission suite, including a mission management system, electro-optics, radar, signals intelligence (SIGINT), and communication.

Military Navigation Systems Industry Overview

The market for military navigation systems is fragmented, with many players in the market who provide various navigation components to different military platforms for diverse military operations. The prominent players in the military navigation systems market are Northrop Grumman Corporation, Safran, THALES, Honeywell International Inc., and Elbit Systems Ltd. To increase their revenue share in the market, the players are developing new products and expanding their product portfolio into various platforms. For instance, Northrop Grumman Corporation provides its navigation and positioning systems to a variety of platforms, such as fixed and rotary-winged aircraft, ships, underwater vehicles, land vehicles, satellites, and missiles. With such a huge portfolio, the company is anticipated to cater to the requirements of various platform manufacturers.

Additionally, the development of new and advanced navigation and positioning systems, with low power consumption, small size, and lightweight, is anticipated to support the growth of the companies. For instance, in January 2023, SandboxAQ, an enterprise SaaS company, was awarded a Direct-to-Phase-II Small Business Innovation Research (SBIR) contract by the US Air Force to research quantum navigation technologies. As per the contract, a prototype of the company AQ quantum-powered sensors will be optimized in close coordination with the US Air Force. Similarly, in July 2023, Australia's Department of Defence awarded a multi-million contract to Q-CTRL (Australia) to develop quantum sensors for military platforms. The program aims to build quantum-enhanced positioning and navigation capability built on Q-CTRL's software-ruggedized quantum sensing technology. It can detect minute changes in acceleration and gravitational field and also remove noise from the signal.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Platform

- 5.1.1 Air

- 5.1.2 Land

- 5.1.3 Sea

- 5.1.4 Space

- 5.2 Application

- 5.2.1 Command & Control (C2)

- 5.2.2 Intelligence, Surveillance & Reconnaissance (ISR)

- 5.2.3 Targeting & Guidance

- 5.2.4 Search & Rescue

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 France

- 5.3.2.3 Germany

- 5.3.2.4 Italy

- 5.3.2.5 Russia

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Mexico

- 5.3.4.2 Brazil

- 5.3.4.3 Rest of Latin America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Qatar

- 5.3.5.4 Egypt

- 5.3.5.5 South Africa

- 5.3.5.6 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Northrop Grumman Corporation

- 6.2.2 Safran

- 6.2.3 Elbit Systems Ltd.

- 6.2.4 Honeywell International Inc.

- 6.2.5 THALES

- 6.2.6 Collins Aerospace (RTX Corporation)

- 6.2.7 KVH Industries, Inc.

- 6.2.8 CMC Electronics Inc.

- 6.2.9 General Electric Company

- 6.2.10 Israel Aerospace Industries Limited

- 6.2.11 Anschotz GmbH

- 6.2.12 Moog Inc.

- 6.2.13 Lockheed Martin Corporation