|

市場調査レポート

商品コード

1405075

UAVナビゲーションシステム:市場シェア分析、産業動向・統計、成長予測、2024~2029年UAV Navigation Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| UAVナビゲーションシステム:市場シェア分析、産業動向・統計、成長予測、2024~2029年 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

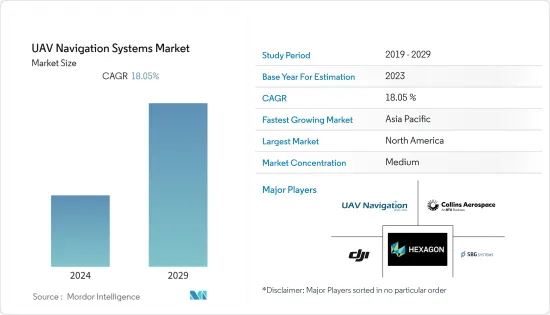

UAVナビゲーションシステム市場は、2024年に97億3,000万米ドルと評価され、2029年には223億1,000万米ドルに達すると予測され、予測期間中のCAGRは18.05%を記録すると予想されます。

民間および軍事用途の両方でUAVの普及が進んでいることが、市場の主な成長要因です。UAVの生産は、世界の産業の中で最も急速に成長し、ダイナミックに発展している分野の1つであり、政府投資にとっても商業投資にとっても同様に魅力的です。世界の先進国と発展途上国の大部分は、すでに必要な制度と法的枠組みを形成しています。また、民間および軍事目的でのUAV利用のシェア拡大を目指した国家プログラムも発表されました。

電子戦の進展により、無人機に自律機能を採用する必要が生じ、それが市場の技術開発を後押ししています。電子戦技術の使用は拡大しているため、新世代の攻撃に対処できる信頼性の高い飛行制御ソリューションが極めて重要になった。UAV各社はエンドユーザーの進化を予測し、さまざまな機能の研究開発に投資し、過酷な環境でも動作する堅牢なシステムを構築するための試験を行っています。電子機器の小型化は、UAV全体の重量をそれほど増やすことなく高度なナビゲーション・誘導システムを開発する上で重要な役割を果たしました。

UAVナビゲーションシステムの市場動向

軍事セグメントが2023年に最も高い市場シェアを記録する見込み

UAVナビゲーションシステム市場は、用途別では軍事分野が民間・商業分野に比べて高い市場シェアを占めています。このセグメントのシェアが高い主な理由は、地上部隊に状況認識を提供する機能が強化されたため、軍事分野へのUAVの普及が進んだことです。UAV市場では、軍事分野からの収益が市場の80%以上を占めています。これは、このセグメントが世界のUAV産業をいかに支配しているかを垣間見ることができます。軍事用UAVは、民間・商業用セグメントと比較して、複雑な戦術的任務を遂行する必要があるため、精密なナビゲーションとガイダンスを備えたより優れた操縦能力が要求されます。これが軍事用UAVのナビゲーションシステムが高コストである主な理由です。また、軍事用UAVの自律能力の向上は、ナビゲーションシステムの複雑なシステムレベルのアーキテクチャを要求しており、それによって市場収益が増加し、このセグメントの成長を支えています。例えば、2023年5月、I-CONIC Vision社はSpacemetric社とともに、スウェーデン国防省の軍事技術革新プログラムにおいて、GNSSに依存しない自律航法に関する契約を獲得しました。このプロジェクトは、ドローンによる長距離のGNSSフリーナビゲーションのためのさまざまな方法を調査することを目的としています。

予測期間中、北米が市場シェアを独占

現在、北米がUAVナビゲーションシステム市場で最も高い市場シェアを占めているのは、米国の国防軍によるUAVの使用率が高いためです。北米では、さまざまな用途でUAVが使用されるようになっています。その用途には、空撮、国境警備、法執行、気象調査、緊急対応、森林火災監視、科学データ収集、物流・ラストマイル配送、交通監視・管制などが含まれます。例えば、2021年1月、Black Swift Technologies LLC(BST)は米国海洋大気庁(NOAA)から契約を受注しました。これは、目視外(BVLOS)飛行中のUAVのGPSを無視したナビゲーションを可能にする商業的に実行可能な技術を開発するものです。Black Swift Technologies LLCは、多様なソースの全地球測位システム(DS-GPS)を使用して、堅牢な二次ナビゲーションオプションを通じてこのサービスを提供することを目指しています。しかし、米国軍は毎年多数のUAVを調達し運用しているため、軍事分野は北米におけるUAVの最大の需要発生源であり続けています。UAVの使用量の増加に伴い、この地域ではナビゲーションシステムのようなUAVサブシステムの需要が増加しています。この地域に多数のUAVメーカーが存在することも、UAVナビゲーションシステム市場で北米の市場シェアが高い主な理由です。例えば、2023年5月、Asio Technologies社(イスラエル)は、米国内の戦略的顧客に対する同社のNavGuard光学ナビゲーションシステムの複数のデモンストレーションを成功裏に完了しました。防衛および民間顧客の要望に応えて実施されたデモンストレーションでは、回転翼無人航空機(UAV)が使用されました。これは、GNSS信号に依存することなく、都市部や農村部での荷物の自動ポイントツーポイント配達だけでなく、空中ナビゲーション活動を実行するものです。

UAVナビゲーションシステム産業概要

同市場の主要企業には、Hexagon AB、SBG Systems、SZ DJI Technology、Collins Aerospace(RTX Corporation)、UAV Navigation S.L.などがあります。市場の製品は、小型ドローンの小さなGPSシステムからクラス5のUAVの完全なナビゲーションシステムまで、製品の大きな多様性は、市場に多くの中小企業から大手企業が存在することを意味します。しかし、主要なUAVメーカーに完全なナビゲーション・誘導システムを提供し、その収益が市場シェアの大きな割合を占める市場で高い評価を受けているプレーヤーはごく少数です。技術革新は、特に顧客基盤を支配している軍事用顧客との新規契約獲得に貢献すると思われます。軍事用顧客にとって、高度なナビゲーションと誘導能力は、戦場における軍隊の競争力を高めるために必要です。したがって、防衛軍は市場の革新的な製品と巨額の取引を行うことを望んでおり、これはプレーヤーにとって成長の機会となっています。例えば、2022年9月、UAVナビゲーションは新しいビジュアル・ナビゲーションシステム(VNS)を発表しました。主な飛行制御システム(FCS)のオプション周辺機器として提供されるこの小型軽量デバイスは、GNSSが否定された環境での無人航空機(UAV)の安全で効率的なナビゲーションを可能にします。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- 業界の魅力- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- UAVタイプ

- 自律型UAV

- 半自律型UAV

- 遠隔(人間)操作型UAV

- 用途

- 民間・商業

- 軍事

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- ロシア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- その他ラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- エジプト

- 南アフリカ

- その他中東・アフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Hexagon AB

- SBG Systems

- UAV Navigation S.L.

- SZ DJI Technology Co., Ltd.

- Collins Aerospace(RTX Corporation)

- AeroVironment, Inc.

- Honeywell International Inc.

- BAE Systems plc

- Cobham Limited

- L3 Harris Technologies, Inc.

- Elbit Systems Ltd.

- Leica Geosystems AG

- Parrot Drone SAS

- Trimble Inc.

第7章 市場機会と今後の動向

The UAV Navigation Systems Market is valued at USD 9.73 billion in 2024 and is anticipated to reach USD 22.31 billion by 2029, registering a CAGR of 18.05% during the forecast period.

The increasing proliferation of UAVs in both civil and military applications is the main growth driver for the market. The production of UAVs is one of the fastest growing and dynamically developing sectors of the world industry, equally attractive for both government and commercial investments. A significant part of the developed and developing countries of the world already formed the necessary institutional and legal framework. It also announced national programs aimed at increasing the share of UAV usage for civil and military purposes.

Advancements in electronic warfare necessitated the adoption of autonomous capabilities in drones, which, in turn, is propelling technological developments in the market. The use of electronic warfare techniques is growing, so a reliable flight control solution ready to face new-generation attacks became vitally important. UAV companies anticipated the evolution of end-users and are investing in R&D for different features and testing to create a robust system ready to work in hard environments. Miniaturization of electronics played a key role in the development of advanced navigation and guidance systems without adding much overall weight to the UAVs.

UAV Navigation Systems Market Trends

Military Segment is Expected to Register the Highest Market Share in 2023

In terms of application, the military segment holds a higher market share in the UAV navigation systems market compared to the civil and commercial segments. The main reason for the higher share of the segment is the increased proliferation of UAVs into the military sector due to their enhanced capabilities in providing situational awareness to ground troops. In the UAV market, the revenues from the military segment comprise more than 80% of the market. It gives a glimpse of how much the segment dominates the global UAV industry. Compared to the civil and commercial segment, the UAVs in the military require better maneuvering capabilities with precision navigation and guidance, as they need to perform complicated tactical missions. It is the main reason for the high cost of the navigation systems in military UAVs. Also, the increased autonomous capabilities of the UAVs in the military are demanding complex system-level architecture of the navigation systems, thereby increasing their market revenues and supporting the growth of the segment. For instance, in May 2023, I-CONIC Vision, together with Spacemetric, won a contract on autonomous navigation independent of GNSS within the Swedish Defence Materiel Administration's military innovation program. The project aims to investigate different methods for GNSS-free navigation by drones over longer distances.

North America to Dominate Market Share During the Forecast Period

Currently, North America holds the highest market share in the UAV Navigation Systems Market due to the high usage of UAVs by the defense forces in the United States. UAVs are increasingly being used in North America for various applications. The applications include aerial photography, border security, law enforcement, weather research, emergency response, forest fire monitoring, scientific data collection, logistics and last-mile delivery, and traffic monitoring and control. For instance, in January 2021, Black Swift Technologies LLC (BST) was awarded a contract by the National Oceanic and Atmospheric Administration (NOAA). It is to develop commercially viable technology to enable GPS-denied navigation of UAVs during flights beyond visual line of sight (BVLOS). Black Swift Technologies LLC aims to provide this service through a robust, secondary navigation option using their diverse-source global positioning system (DS-GPS). However, the military segment remains the biggest demand generator for UAVs in North America, as the United States military procures and operates a large number of UAVs every year. With the increasing UAV usage, the demand for UAV subsystems like navigation systems is increasing in the region. It, coupled with the presence of a large number of UAV manufacturers in the region, is the main reason for the high market share of North America in the UAV navigation systems market. For instance, in May 2023, Asio Technologies (Israel) completed several demonstrations successfully of its NavGuard optical navigation system to strategic customers in the United States. The demonstrations, conducted in response to defense and civil customer requests, involved a rotary-wing unmanned aerial vehicle (UAV). It is to perform aerial navigation activities as well as automatic point-to-point deliveries of packages over urban and rural areas without relying on GNSS signals.

UAV Navigation Systems Industry Overview

Some of the prominent players in the market include Hexagon AB, SBG Systems, SZ DJI Technology Co., Ltd., Collins Aerospace (RTX Corporation), and UAV Navigation S.L., among others. As the products in the market range from small GPS systems of a small drone to the complete navigation system of the class 5 UAV, a large diversity of the products means that there will be a lot of small to big players in the market. However, there are very few acclaimed players in the market providing complete navigation and guidance systems to the major UAV manufacturers, whose revenues comprise a large percentage of the market share. Technological innovations will help the players to gather new contracts, especially with the military customers who dominate the customer base. For military customers, advanced navigation and guidance capabilities are necessary, as they give the armed forces a competitive edge on the battlefield. Hence, defense forces are willing to trade huge amounts for innovative products in the market, which is an opportunity for growth for the players. For instance, in September 2022, UAV Navigation released its new Visual Navigation System (VNS). The compact and lightweight device, which is provided as an optional peripheral to the main Flight Control System (FCS), enables the safe and efficient navigation of Uncrewed Aerial Vehicles (UAVs) in GNSS-denied environments.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 UAV Type

- 5.1.1 Autonomous UAVs

- 5.1.2 Semi-Autonomous UAVs

- 5.1.3 Remotely (Human) Operated UAVs

- 5.2 Application

- 5.2.1 Civil and Commercial

- 5.2.2 Military

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Russia

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Australia

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Mexico

- 5.3.4.3 Rest of Latin America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Egypt

- 5.3.5.4 South Africa

- 5.3.5.5 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Hexagon AB

- 6.2.2 SBG Systems

- 6.2.3 UAV Navigation S.L.

- 6.2.4 SZ DJI Technology Co., Ltd.

- 6.2.5 Collins Aerospace (RTX Corporation)

- 6.2.6 AeroVironment, Inc.

- 6.2.7 Honeywell International Inc.

- 6.2.8 BAE Systems plc

- 6.2.9 Cobham Limited

- 6.2.10 L3 Harris Technologies, Inc.

- 6.2.11 Elbit Systems Ltd.

- 6.2.12 Leica Geosystems AG

- 6.2.13 Parrot Drone SAS

- 6.2.14 Trimble Inc.