|

市場調査レポート

商品コード

1405077

民間航空機用ラバトリーシステム-市場シェア分析、産業動向・統計、2024~2029年成長予測Commercial Aircraft Lavatory System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| 民間航空機用ラバトリーシステム-市場シェア分析、産業動向・統計、2024~2029年成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

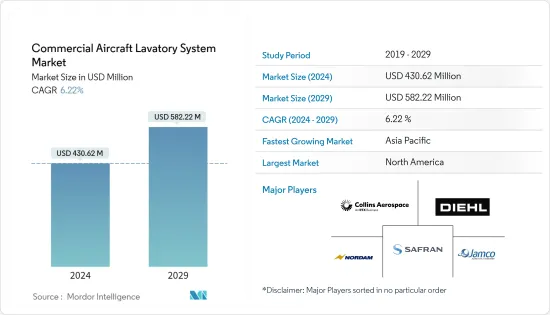

民間航空機用ラバトリーシステムの市場規模は2024年に4億3,062万米ドルと推定され、2029年には5億8,222万米ドルに達すると予測され、予測期間中(2024~2029年)のCAGRは6.22%で成長する見込みです。

この市場の主要促進要因のひとつは、世界的に航空旅行の需要が増え続けていることです。世界の人口が増え続け、経済が拡大するにつれて、より多くの人々が航空旅行を選ぶようになり、航空便数が増加しています。この旅客数の急増は、民間航空機の効率的なラバトリーシステムの必要性と直接的な相関関係があります。航空会社は旅客に機内での体験をより良いものにしようと努力しており、近代的で手入れの行き届いたラバトリーは、旅客の快適さと満足度を高める重要な要素となっています。

航空機のラバトリーは、全体の重量を減らすことで燃料を節約し、より多くの利益を生み出すために、航空会社がより軽量な構造を要求しているため、継続的な技術革新が行われています。節水技術や廃棄物削減メカニズムなどの機能を備えた先進的なラバトリーシステムは、二酸化炭素排出量を削減し、環境に優しい慣行を採用することに合致しています。さらに、特にCOVID-19パンデミックのような世界の健康懸念に伴う衛生の重要性は、タッチレス器具や抗菌材料を含むラバトリー設計の革新につながった。老朽化した機体の一部で客室内装を改修する航空会社はほとんどなく、新しいラバトリーシステムの需要を生み出しています。

航空安全と衛生基準を管理する厳しい規制環境。航空機のラバトリーは、乗客の安全と衛生を確保するため、厳しい規制と認証を遵守しなければならないです。市場に導入される新しいシステムや部品は、厳格な試験を受け、これらの規制要件を満たさなければなりません。このため、メーカーにとっては、開発期間の延長やコスト増につながる可能性があります。さらに、既存の航空機に新しいラバトリー・システムを導入して最新の規制に適合させることは、複雑でコストのかかる取り組みとなる可能性があり、航空会社とメーカーの双方にとって課題となります。

民間航空機用ラバトリーシステム市場動向

予測期間中、ワイドボディセグメントが市場シェアを独占

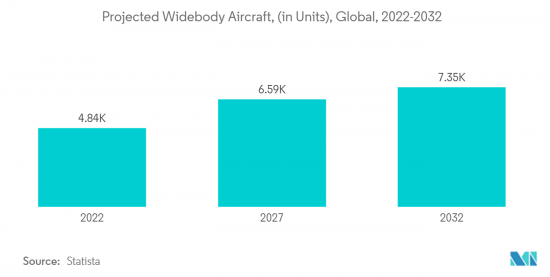

航空機に設置されるラバトリーの数は、航空機の旅客輸送能力によって決まる。そのため、ナローボディ機に比べ、ワイドボディ機のラバトリーの数ははるかに多いです。ワイドボディ機は、何時間にも及ぶ大陸間フライトによく使用されます。このような長時間のフライトでは、乗客が何度もラバトリーを利用するため、効率的でメンテナンスの行き届いたラバトリーシステムの必要性が高まる。また、ワイドボディ機にはビジネスクラスやファーストクラスの乗客がいます。これらのプレミアムクラスの乗客は、より広いスペース、高級アメニティ、衛生面の強化など、質の高いラバトリー設備を期待しています。航空会社は、乗客の体験を向上させるため、ラバトリーにさまざまなブランドの製品やデザインを採用しています。さらに、一般的に、ワイドボディ機はナローボディ機よりも室内空間が広いです。この余分なスペースにより、より大きなラバトリーを設置することができ、利用者の快適性と使いやすさを向上させることができます。世界中の様々な航空会社からワイドボディ機の発注が増加しているため、より多くの収納ボックスの需要が高まると思われます。2023年5月、Air IndiaはBoeingから20機のB787ドリームライナーと10機のB777X、Airbusから34機のA350-1000、6機のA350-900を含む70機のワイドボディ機を発注しました。

アジア太平洋が予測期間中に最も高い成長を遂げる

アジア太平洋の航空産業は、力強い経済成長の継続、中間所得層の増加、世帯所得の向上、人口統計の組み合わせにより、成長を続けています。航空旅客輸送量の伸びに関しては、アジア太平洋は2040年に4.5%以上のCAGRで推移すると思われます。観光産業の成長もまた、同地域の民間航空市場の状況を決定づける。アジア太平洋の航空旅客輸送量の増加は、主に中国とインドによるものです。インドネシア、マレーシア、ベトナム、タイ、シンガポールなどの他の国々も、世界中のさまざまな地域から膨大な数の旅客を引きつけており、航空会社はより良い接続性を提供するために新しい路線を導入しています。国際航空運送協会(IATA)によれば、2030年までにアジアの航空旅客数は北米と欧州を上回るといわれています。このような旅客輸送量の高い成長率に伴い、この地域の航空会社は需要の増加に対応するために新しい航空機を調達する必要があります。さらに、アジア太平洋の航空会社は、運航効率と旅客満足度を向上させるため、航空機の購入と近代化にますます投資しています。この地域での受注と納入の増加に伴い、航空機用ラバトリーシステムの需要も大きな伸びを見せると思われます。2023年2月現在、エア・インディア、インディゴなどのインドの民間航空会社は、メーカーからの航空機発注を1,100機保留しています。航空機の受注と納入の増加に伴い、予測期間中、この地域からラバトリーシステムに対する需要が同時に発生する可能性が高いです。

民間航空機用ラバトリーシステム産業概要

民間航空機用ラバトリーシステム市場は統合されており、少数の参入企業で構成されているが、2023年には一部の有力参入企業が大きな市場シェアを占めています。市場の主要企業には、Diehl Stiftung &Co.KG、JAMCO Corporation、Safran、The NORDAM Group LLC、Collins Aerospace(RTX Corporation)です。しかし、OEM間の競争は激しく、さまざまな企業がこの市場に製品を投入しています。地域拡大、新製品開拓、長期的な人脈の獲得などの重要な戦略は、この市場での競合を高めるために主要企業によって実施されています。企業は、航空会社がフライトあたりの収益を改善するために航空機あたりの座席数を増やすことができるように、客室スペースを増やすためのコンパクトなラバトリーシステムの開発に多額の投資を行っています。空港のラバトリーでは、主にCOVID-19の流行によって加速された、かなりのエンジニアリングと設計の見直しが行われています。例えば、Collins Aerospaceは、物理的なタッチポイントを最小限に抑え、衛生状態を最大限に高めることを重要視しています。Collins Aerospaceは、ラバトリーアメニティへのハンズフリー接触をサポートするタッチレス・ソリューション、ライラックUVや表面コーティングなどの機能的な抗菌機能、衛生に焦点を当てたその他の機能のリストを設計しています。さらに現在では、より差別化された外観を作り出し、以前のような労働集約的な使用を減らすために、デザイナー・プラスチック・シートの熱成形が適用されています。また、カウンタートップや羽目板部分へのハイドロ・ディッピングも、カスタム・デザインに高度に利用されています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- 業界の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 航空機タイプ

- ナローボディ

- ワイドボディ

- リージョナルジェット

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- ロシア

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- ラテンアメリカ

- ブラジル

- メキシコ

- その他のラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- カタール

- 南アフリカ

- その他の中東・アフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Diehl Stiftung & Co. KG

- JAMCO Corporation

- Yokohama Aerospace America, Inc.

- Collins Aerospace(RTX Corporation)

- Safran

- Hong Kong Aircraft Engineering Company Limited

- Geven SPA.

- The NORDAM Group LLC

- Satys

- CIRCOR Aerospace

第7章 市場機会と今後の動向

The Commercial Aircraft Lavatory System Market size is estimated at USD 430.62 million in 2024, and is expected to reach USD 582.22 million by 2029, growing at a CAGR of 6.22% during the forecast period (2024-2029).

One of the primary drivers in this market is the ever-increasing demand for air travel worldwide. As the global population continues to grow and economies expand, more people are opting for air travel, leading to a higher number of flights. This surge in passenger traffic has a direct correlation with the need for efficient lavatory systems on commercial aircraft. Airlines strive to provide passengers with improved in-flight experiences, and modern, well-maintained lavatories are a crucial aspect of passenger comfort and satisfaction.

Aircraft lavatories are going through continuous innovation as the airlines demand lighter structures to generate more profits through fuel savings by reducing the overall weight. Advanced lavatory systems with features like water-saving technologies and waste reduction mechanisms align with reducing their carbon footprint and adopting eco-friendly practices. Additionally, the importance of hygiene, especially in the wake of global health concerns such as the COVID-19 pandemic, led to innovations in lavatory designs, including touchless fixtures and antimicrobial materials. Few airlines are refurbishing the cabin interior on some of their aging fleet, generating demand for a new lavatory system.

The stringent regulatory environment governing aviation safety and hygiene standards. Aircraft lavatories must adhere to strict regulations and certifications to ensure passenger safety and hygiene. Any new system or component introduced to the market must undergo rigorous testing and meet these regulatory requirements. This can lead to extended development timelines and increased costs for manufacturers. Moreover, retrofitting existing aircraft with new lavatory systems to comply with updated regulations can be a complex and costly endeavor, posing a challenge for both airlines and manufacturers.

Commercial Aircraft Lavatory System Market Trends

Wide-body Segment is Dominate Market Share During the Forecast Period

The number of lavatories installed in an aircraft depends on the passenger-carrying capacity of the aircraft. Hence, the number of lavatories present in wide-body aircraft is much higher compared to narrow-body aircraft. Wide-body aircraft are commonly used for intercontinental flights, which can last for many hours. Passengers on these long flights will likely use the lavatories multiple times, increasing the need for efficient and well-maintained lavatory systems. Also, wide-body aircraft have passengers traveling in Business and First Class. These premium passengers expect high-quality lavatory facilities, which may include more space, upscale amenities, and enhanced hygiene features. Airlines, to improve the passenger experience, are adopting different branded products and designs for their lavatories. Moreover, Wide-body aircraft generally have more interior space than their narrow-body counterparts. This extra space allows for the installation of larger lavatories, which can improve user comfort and accessibility. An increase in wide-body aircraft orders from various airlines across the globe will fuel the demand for more storage bins. In May 2023, Air India placed orders for 70 widebody aircraft, including 20 B787 Dreamliners and 10 B777Xs from Boeing, 34 A350-1000s, and six A350-900s from Airbus.

Asia-Pacific to WItness Highest Growth During the Forecast Period

The aviation industry in Asia-Pacific continues to thrive on a combination of continued robust economic growth, increasing middle-class population, improvements in household incomes, and demographic profiles. Regarding air passenger traffic growth, Asia-Pacific will register a CAGR of over 4.5% over 2040. Tourism growth also defines the state of the commercial aviation market in the region. The increase in Asia-Pacific air passenger traffic is primarily due to China and India. Other countries, like Indonesia, Malaysia, Vietnam, Thailand, and Singapore, among others, are also attracting vast numbers of passengers from various regions around the world, making the airlines introduce new routes to offer better connectivity. According to the International Air Transport Association (IATA), air travel in Asia will surpass North America and Europe by 2030. With such a high rate of growth in terms of passenger traffic, the airlines in the region need to procure new aircraft to cater to the increasing demand. Moreover, the airlines in the Asia-Pacific region are increasingly investing in purchasing and modernizing their aircraft fleets to improve operational efficiency and passenger satisfaction. With the growing orders and deliveries in the area, the demand for aircraft lavatory systems will also witness significant growth. As of February 2023, Indian private airlines such as Air India, Indigo, and others have 1,100 pending aircraft orders from manufacturers. With the increasing aircraft orders and deliveries, simultaneous demand is likely to be generated for lavatory systems from this region during the forecast period.

Commercial Aircraft Lavatory System Industry Overview

The market for commercial aircraft lavatory systems is consolidated and comprises a few players, with some prominent players accounting for a significant market share in 2023. Some of the leading players in the market are Diehl Stiftung & Co. KG, JAMCO Corporation, Safran, The NORDAM Group LLC, and Collins Aerospace (RTX Corporation). However, rivalry among the OEMs is high, with various companies encompassing their offerings in this market. Important strategies such as regional expansion, new product development, and achieving long-term contacts are being implemented by the top players to advance the competitive edge in this market. Companies are significantly investing in developing compact lavatory systems to increase cabin space so that the airlines can squeeze in a more significant number of seats per aircraft to improve their revenue per flight. A considerable engineering and design overhaul is taking place in airport lavatories, accelerated mainly by the COVID-19 pandemic. For instance, Collins Aerospace significantly emphasizes minimizing physical touchpoints and maximizing hygiene. Collin Aerospace is designing touchless solutions to support hands-free contact with lavatory amenities, functional antimicrobial features such as Lilac-UV and surface coatings, and a list of other features focused on hygiene. Moreover, now, to create a more differentiated appearance and to reduce the previous intensive usage of labor, thermoforming designer plastic sheets are applied. Another area observing a high degree of use for custom designs is hydro dipping for countertops and paneling areas.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Aircraft Type

- 5.1.1 Narrow-body

- 5.1.2 Wide-body

- 5.1.3 Regional Jets

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.2 Europe

- 5.2.2.1 United Kingdom

- 5.2.2.2 Germany

- 5.2.2.3 France

- 5.2.2.4 Italy

- 5.2.2.5 Russia

- 5.2.2.6 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Japan

- 5.2.3.4 South Korea

- 5.2.3.5 Rest of Asia-Pacific

- 5.2.4 Latin America

- 5.2.4.1 Brazil

- 5.2.4.2 Mexico

- 5.2.4.3 Rest of Latin America

- 5.2.5 Middle East and Africa

- 5.2.5.1 United Arab Emirates

- 5.2.5.2 Saudi Arabia

- 5.2.5.3 Qatar

- 5.2.5.4 South Africa

- 5.2.5.5 Rest of Middle East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Diehl Stiftung & Co. KG

- 6.2.2 JAMCO Corporation

- 6.2.3 Yokohama Aerospace America, Inc.

- 6.2.4 Collins Aerospace (RTX Corporation)

- 6.2.5 Safran

- 6.2.6 Hong Kong Aircraft Engineering Company Limited

- 6.2.7 Geven SPA.

- 6.2.8 The NORDAM Group LLC

- 6.2.9 Satys

- 6.2.10 CIRCOR Aerospace