|

市場調査レポート

商品コード

1405078

モバイルゲーム-市場シェア分析、産業動向・統計、成長予測2024年~2029年Mobile Gaming - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| モバイルゲーム-市場シェア分析、産業動向・統計、成長予測2024年~2029年 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

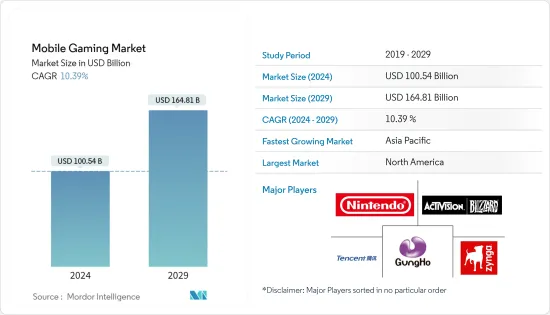

モバイルゲーム市場規模は2024年に1,005億4,000万米ドルと推定され、2029年には1,648億1,000万米ドルに達すると予測され、予測期間中(2024~2029年)のCAGRは10.39%で成長する見込みです。

COVID-19は世界のビジネスのあり方に影響を与えているが、ゲーム業界はパンデミックによりプラスの影響を受けています。このような困難な時代に、モバイルゲーム業界が果たした役割は、人々の安らぎを得る手助けをすることでした。モバイルゲームには、ストレスを軽減し、娯楽や社会とのつながりを提供する力があり、特に世界の検疫の際には、それが大いに必要とされました。

主要ハイライト

- 最近、モバイルゲーム開発部門に多くの変化が起きています。その結果、ゲームブランドはより多くのユーザーを獲得し、十分な市場シェアを確保するために、より多くの広告投資を行うようになった。しかし、開発プロセスのコストを削減する効果的な方法の1つは、早期にCTR(クリックスルー率)テストを実施することです。モバイルゲーム業界のハイパーカジュアルゲーム部門であればなおさらです。

- ゲーム産業は世界的に拡大しており、その中でスマートフォンが果たす役割は大きいです。モバイルゲームの発展は、ゲーム業界のスケーラビリティをもたらしました。フェイスブックやインスタグラムのようなプラットフォームも、高い製品差別化を確保し、広告戦略を強化するための魅力的なゲームから利益を得るために、革新的なモバイルゲームの開発に着手しています。

- スマートフォンのハードウェア性能は、ここ数年で急速に向上しています。ユニティ・技術ズ社によると、優れたモバイル・チップセットは、バッテリーの消耗を抑えながらより高いパフォーマンスを発揮し、現在では平均6インチのディスプレイ・サイズでより高い画面解像度を実現しています。さらに、エリクソンによると、5Gは驚異的なスピード(4Gの20倍)と低遅延(20ミリ秒から5ミリ秒)を可能にしました。そのため、市場では、制作価値の高いAAA品質のモバイルゲームがますます増えています。

- 地政学的な緊張にもかかわらず、スマートフォンの普及が進み、ゲームの選択肢が増えたことで、世界の多くの地域でモバイルゲームの普及も進んでいます。例えば、White Designers Game Studiosによると、人口8,200万人、スマートフォン普及率約54%(2023年)のイランでは、4,800万人以上のアクティブなモバイルゲーム参入企業がいるといわれています。

- ゲーム内課金、すなわちゲーム内で追加特典を購入するオプションは、モバイルゲーム業界にとって重要な収益創出チャネルです。また、ゲーム内での支払い方法の柔軟性も、世界のモバイルゲーム収益の成長を促進しています。

- さらに、クラウド・ゲーミング・サービスは、超大規模クラウド機能、世界のコンテンツ配信ネットワーク、ストリーミング・メディア・サービスを活用し、インタラクティブで没入感のあるソーシャル・エンターテインメントのための次世代プラットフォームを構築します。また、国内におけるエッジデータセンターの普及も、モバイルゲームの世界の成長を加速させています。

モバイルゲーム市場の動向

スマートフォン普及率の増加が市場成長を牽引する見込み

- スマートフォンの普及率は、モバイルゲーム市場に大きな影響を与えています。スマートフォンは便利で利用しやすいゲームプラットフォームを提供します。ハードウェア機能の向上と高度なグラフィックスにより、スマートフォンはリッチなゲーム体験を提供できます。このアクセシビリティは、ゲーム専用機やPCに投資しないカジュアルゲーマーを含め、より幅広い層にモバイルゲームをアピールしています。

- Google Play StoreやApple App Storeのようなアプリストアが広く利用できるようになったことで、開発者はモバイルゲームの配信や収益化を容易に行えるようになった。何100万台ものスマートフォンがこれらのアプリストアに接続されているため、開発者は膨大なユーザーベースにリーチし、アプリ内課金や広告を通じて収益を得ることができます。

- スマートフォンはソーシャル接続を可能にし、ユーザーは友人や世界中の他の参入企業とマルチ参入企業ゲームを体験することができます。このようなモバイルゲームのソーシャルな側面は、全体的な体験を向上させ、ユーザーの関与を促し、市場の成長をさらに促進します。

- スマートフォンの技術は進化を続けており、処理能力、グラフィックス機能、仮想現実(VR)統合が向上しています。これらの進歩により、開発者はより没入感のある洗練されたモバイルゲームを作成できるようになり、より多くのユーザーを惹きつけ、市場の成長を促進しています。

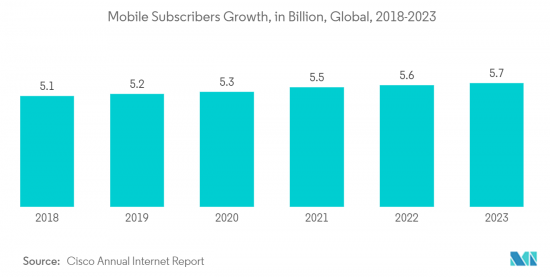

- シスコによると、世界全体のモバイル加入者数(携帯電話サービスを利用する人)は、2018年の51億人から2023年末には57億人に増加し、CAGRは2%になると予想されています。人口に換算すると、2018年には世界人口の66%を占め、2023年には世界人口普及率の71%を占める。スマートフォンの所有率が世界的に上昇を続けるなか、モバイルゲームへの需要が高まり、ゲーム開発者やパブリッシャー、業界のその他の利害関係者に新たな機会が生まれると予想されます。

- また、多くのゲーマーがスマートフォンでのゲームを好む中、高速5Gや無制限データプランのリリースも、世界のクラウドゲームの成功に向けた重要な要因になると予想されます。この成功には、5Gインフラへのサービス、開発、投資の増加が不可欠です。Ericssonによると、アジア太平洋の5Gモバイル契約数は、2025年までに約15億4,500万件に達します。

北米が大きな市場シェアを占める見込み

- 北米のモバイルゲーム市場は、世界最大かつ最も有利な市場のひとつです。北米は世界のモバイルゲーム市場に大きく貢献しています。同地域はスマートフォンユーザーの人口が多く、モバイルゲームはさまざまな年齢層で絶大な人気を博しています。スマートフォンの普及率の高さ、良好な経済状況、根強いゲーム文化が北米の市場規模を押し上げています。

- Ericssonによると、5Gコネクティビティは、データ速度の高速化、超低遅延、可用性の向上などの利点を備えた新しいモバイル技術であるため、今後数年間で北米のゲーム市場の成長を牽引すると予想されています。北米では2019年から2027年にかけて、5Gの契約数が107万件超から約3億9,999万件に激増すると予測されています。同地域はスマートデバイスの普及率が最も高いです。スマートデバイス、特にスマートフォンが市場の開拓に大きな役割を果たしているため、同地域は予測期間中に調査した市場の成長に大きな機会を提供しています。

- 北米のモバイルゲーム市場は競争が激しく、既存参入企業とインディーズデベロッパーの両方が市場シェアを争っています。 Electronic Arts、Activision、Blizzard、Zyngaなどの大手ゲーム会社は、この地域で強い存在感を示しています。さらに、インディーズゲーム開発シーンも盛んで、この地域から革新的で成功したタイトルが数多く生まれています。

- この地域は、多様なゲームプラットフォームで知られています。モバイルゲームのプラットフォームはスマートフォンが主流だが、タブレットやハンドヘルドゲーム機など他のプラットフォームも市場に貢献しています。さらに、この地域ではクラウドゲームサービスの動向も高まっており、ユーザーはモバイルデバイスでゲームをストリーミングしてプレイすることができます。

- 2022年7月、未来の決済プラットフォームであるNuvei CorporationとGAN Limitedは、GANのSaaS(Software-as-a-Service)のゲーミングプラットフォーム技術を統合することで、ゲーミングオペレーターがNuviの決済ソリューション一式にアクセスできるようにする戦略的提携を発表しました。この提携は、今年初めのオンタリオ州の規制ゲーミング市場のオープンに始まったもので、現在は米国とカナダ全土のオペレーターを支援するために拡大しています。

- 北米のモバイルゲーム市場には、カジュアルゲーム、戦略ゲーム、ロールプレイングゲーム(RPG)、多人数参加型オンラインバトルアリーナ(MOBA)など、さまざまなゲームジャンルがあります。また、AR(拡大現実)ゲームやVR(仮想現実)ゲームも登場し、没入感のあるゲーム体験を提供しています。

モバイルゲーム業界概要

モバイルゲーム市場は非常に細分化されており、Tencent Holdings Limited、Nintendo、Activision Blizzard Inc.、Zynga Inc.、GungHo Online Entertainment Inc.(SoftBank Group)などの大手参入企業が存在します。市場の参入企業は、製品提供を強化し、持続可能な競争優位性を獲得するために、提携や買収などの戦略を採用しています。

- 2022年11月-Nintendoはスーパーマリオラン制作会社との提携によりデジタル化を強化します。NintendoはモバイルプロバイダーのDeNAと合弁会社を設立し、Nintendo Systemsという新事業を展開すると発表、2023年4月に開業します。

- 2022年9月-Take-Two Interactive Software Inc.の100%子会社で、インタラクティブ・エンターテインメントの世界的パイオニアであるZynga Incは、モバイルグロースとApp Store Optimisation(ASO)ソリューションの世界的リーダーであるStoremavenの買収完了を発表。Storemavenのチームは、その画期的なモバイル技術とZyngaの大規模な世界ポートフォリオとChartboostの広告プラットフォームを組み合わせることで、Zyngaのイスラエルにおける現在の事業を拡大します。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 競争企業間の敵対関係

- 代替品の脅威

- COVID-19がモバイルゲーム市場に与える影響

第5章 市場力学

- 市場促進要因

- スマートフォン普及率の増加

- クラウドの普及拡大

- 市場抑制要因

- 政府規制によるユーザーのプライバシーとセキュリティの問題

第6章 モバイルゲーム市場動向

- クラウドゲーム

- 拡大現実ゲーム

- クロスプラットフォームペイ

- ブロックチェーンベースゲーム

- カジュアルゲーム

- マルチ参入企業・モバイル参入企業

第7章 市場セグメンテーション

- マネタイズタイプ別

- アプリ内課金

- 有料アプリ

- 広告

- プラットフォーム別

- アンドロイド

- iOS

- その他のサードパーティストア(Amazon Appstore、Samsung Galaxy Store、Garenaなどのサードパーティ製Androidアプリストア、とGoogle Playが利用できない中国国内の既存Androidアプリストアすべて)

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他の欧州(ロシア、北欧など)

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- その他のアジア太平洋(オーストラリア、パキスタン、東南アジア)

- ラテンアメリカ

- ブラジル

- メキシコ

- ペルー

- その他のラテンアメリカ(コロンビアなど)

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- その他の中東・アフリカ

- 北米

第8章 競合情勢

- 企業プロファイル

- Tencent Holdings Limited

- Nintendo Co. Ltd

- Activision Blizzard Inc.

- Zynga Inc.

- GungHo Online Entertainment Inc.(SoftBank Group)

- Electronic Arts Inc.

- Kabam Games Inc.

- Rovio Entertainment Corporation

- NCsoft Corporation

- NetEase Inc.

第9章 投資分析

第10章 市場機会と今後の動向

The Mobile Gaming Market size is estimated at USD 100.54 billion in 2024, and is expected to reach USD 164.81 billion by 2029, growing at a CAGR of 10.39% during the forecast period (2024-2029).

COVID-19 has impacted how the world does business; however, the gaming industry has been positively affected due to pandemics. During these challenging times, the role of the mobile gaming industry was to help people get some relief. Mobile games have the power to reduce stress and provide some entertainment and social connection, which was much needed, especially during the global quarantine.

Key Highlights

- Many changes occurred in the mobile game development department in recent past. Consequently, game brands have spent more on advertising investment to attract more users and corner sufficient market share. However, one effective way to reduce the development process cost is to conduct an early CTR (click-through rate) test. This is especially true if one is in the hyper-casual game sector of the mobile game industry.

- The gaming industry worldwide is expanding, and smartphones play a significant role in this expansion. The development of mobile games has resulted in scalability for the gaming industry. Platforms like Facebook and Instagram have also started to develop innovative mobile games to ensure high product differentiation and benefit from engaging games to enhance their advertisement strategies.

- Smartphone hardware capabilities have rapidly increased during the last couple of years. According to Unity Technologies, the better mobile chipsets provide greater performance with less battery drain, powering higher screen resolutions on display sizes that now average 6 inches. Furthermore, according to Ericsson, 5G allowed for incredible speeds (20 x 4G) and low latency (20 ms to 5 ms). Because of that, the market sees more and more high-production-value AAA-quality mobile games.

- Despite geopolitical tensions, the growing smartphone penetration and increasing gaming options are also increasing the mobile gaming penetration in many parts of the world. For instance, according to White Designers Game Studios, in Iran, with a population of 82 million and a smartphone penetration rate of about 54% (in 2023), there are more than 48 million active mobile gaming players in the country.

- In-game purchase, i.e., the option to purchase additional privileges within the games, is a significant revenue-generating channel for the mobile gaming industry. The flexibility for in-game payment methods also facilitates the growth of mobile gaming revenues worldwide.

- Further, cloud gaming services leverage hyper-scale cloud capabilities, global content delivery networks, and streaming media services to build the next generation of platforms for interactive, immersive, and social entertainment. The proliferation of edge data centers in the country also facilitates the accelerated growth of mobile gaming globally.

Mobile Gaming Market Trends

Increasing Smartphone Penetration is Expected to Drive the Market Growth

- Increasing smartphone penetration has a significant impact on the mobile gaming market. Smartphones offer a convenient and accessible gaming platform. With improved hardware capabilities and advanced graphics, smartphones can provide a rich gaming experience. This accessibility makes mobile gaming appealing to a broader audience, including casual gamers who may not invest in dedicated gaming consoles or PCs.

- The widespread availability of app stores, such as the Google Play Store and Apple App Store, makes it easier for developers to distribute and monetize their mobile games. With millions of smartphones connected to these app stores, developers can reach a vast user base and generate revenue through in-app purchases and advertisements.

- Smartphones enable social connectivity, allowing users to engage in multiplayer gaming experiences with friends and other players worldwide. This social aspect of mobile gaming enhances the overall experience and encourages user engagement, further driving market growth.

- Smartphone technology continues to evolve, improving processing power, graphics capabilities, and virtual reality (VR) integration. These advancements enable developers to create more immersive and sophisticated mobile games, attracting a larger audience and driving market growth.

- According to Cisco, Globally, the total number of mobile subscribers (those who use cellular services) is expected to rise from 5.1 billion in 2018 to 5.7 billion by the end of 2023, at a CAGR of 2 percent. In terms of population, it accounted for 66 percent of the global population in 2018 and 71 percent of global population penetration by 2023. As smartphone ownership continues to rise globally, the demand for mobile games is expected to increase, creating new opportunities for game developers, publishers, and other stakeholders in the industry.

- The release of high-speed 5G and unlimited data plans is also expected to be a critical factor toward the success of cloud gaming worldwide, as most gamers prefer games on their smartphones. The increasing services, development, and investment in 5G infrastructure are essential to this success. According to Ericsson, 5G mobile subscriptions in the Asia Pacific region will reach around 1,545 million by 2025.

North America is Expected to Hold Significant Market Share

- The mobile gaming market in North America is one of the largest and most lucrative in the world. North America is a significant contributor to the global mobile gaming market. The region has a large population of smartphone users, and mobile games have gained immense popularity across various age groups. High smartphone penetration, favorable economic conditions, and a strong gaming culture drive the market size in North America.

- According to Ericsson, 5G connectivity is expected to drive the growth of the North American gaming market in the coming years, as the newer mobile technology with higher data speeds, ultra-low latency, and increased availability, among other benefits. 5G subscriptions are forecast to increase drastically in North America from 2019 to 2027, from over 1.07 million to around 399.99 million subscriptions. The region has the highest adoption rate of smart devices. As smart devices, especially smartphones, play a significant role in the development of the market, the region offers a huge opportunity for the growth of the market studied over the forecast period.

- The North America mobile gaming market is highly competitive, with both established players and indie developers vying for market share. Major gaming companies like Electronic Arts, Activision Blizzard, and Zynga have a strong regional presence. Additionally, there is a thriving indie game development scene, with numerous innovative and successful titles emerging from the region.

- This region is known for its diverse gaming platforms. While smartphones are the dominant platform for mobile gaming, other platforms like tablets and handheld gaming devices also contribute to the market. Moreover, the region has witnessed an increasing trend of cloud gaming services, allowing users to stream and play games on their mobile devices.

- In July 2022, Nuvei Corporation, the future's payments platform, and GAN Limited announced a strategic partnership to enable gaming operators to access Nuvi's full suite of payment solutions by integrating GAN's software-as-a-service gaming platform technology. The collaboration began with the opening of Ontario's regulated gaming market earlier this year and is now being expanded to assist operators across the United States and Canada.

- The North America mobile gaming market encompasses various game genres, including casual games, strategy games, role-playing games (RPGs), and multiplayer online battle arena (MOBA) games. The market has also witnessed the emergence of augmented reality (AR) and virtual reality (VR) games, providing immersive gaming experiences.

Mobile Gaming Industry Overview

The Mobile Gaming Market is highly fragmented, with the presence of major players like Tencent Holdings Limited, Nintendo Co. Ltd, Activision Blizzard Inc., Zynga Inc., and GungHo Online Entertainment Inc. (SoftBank Group). Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- November 2022 - Nintendo would strengthen digitalization by collaborating with the Super Mario Run creator. Nintendo announced a joint venture with mobile provider DeNA to develop a new business named Nintendo Systems Co. Ltd, which will open in April 2023.

- September 2022 - Zynga Inc., a wholly-owned label of Take-Two Interactive Software Inc. and a global pioneer in interactive entertainment, announced the completion of its purchase of Storemaven, a global leader in mobile growth and App Store Optimisation (ASO) solutions. The Storemaven team would combine its breakthrough mobile technology with Zynga's large global portfolio and Chartboost's advertising platform, expanding Zynga's current operations in Israel.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Intensity of Competitive Rivalry

- 4.3.5 Threat of Substitute Products

- 4.4 Impact of COVID-19 on the Mobile Gaming Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Smartphone Penetration

- 5.1.2 Growth in Cloud Adoption

- 5.2 Market Restraints

- 5.2.1 User Privacy and Security Issues Along with Government Regulations

6 MOBILE GAMING MARKET TRENDS

- 6.1 Cloud Gaming

- 6.2 Augment Reality Gaming

- 6.3 Cross Platform Pay

- 6.4 Blockchain Based Game

- 6.5 Casual Games

- 6.6 Multiplayer Mobile Players

7 MARKET SEGMENTATION

- 7.1 By Monetization Type

- 7.1.1 In-app Purchases

- 7.1.2 Paid Apps

- 7.1.3 Advertising

- 7.2 By Platform

- 7.2.1 Android

- 7.2.2 iOS

- 7.2.3 Other Third-party Stores (Third-party Android App Stores such as Amazon Appstore, Samsung Galaxy Store, Garena, and All Existing Android App Stores in China where Google Play is Not Available)

- 7.3 By Geography

- 7.3.1 North America

- 7.3.1.1 United States

- 7.3.1.2 Canada

- 7.3.2 Europe

- 7.3.2.1 Germany

- 7.3.2.2 United Kingdom

- 7.3.2.3 France

- 7.3.2.4 Italy

- 7.3.2.5 Rest of Europe (Russia, Nordics, etc.)

- 7.3.3 Asia Pacific

- 7.3.3.1 China

- 7.3.3.2 Japan

- 7.3.3.3 India

- 7.3.3.4 South Korea

- 7.3.3.5 Rest of Asia Pacific (Australia, Pakistan, SEA)

- 7.3.4 Latin America

- 7.3.4.1 Brazil

- 7.3.4.2 Mexico

- 7.3.4.3 Peru

- 7.3.4.4 Rest of Latin America (Columbia, etc.)

- 7.3.5 Middle East and Africa

- 7.3.5.1 United Arab Emirates

- 7.3.5.2 Saudi Arabia

- 7.3.5.3 Rest of Middle East and Africa

- 7.3.1 North America

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Tencent Holdings Limited

- 8.1.2 Nintendo Co. Ltd

- 8.1.3 Activision Blizzard Inc.

- 8.1.4 Zynga Inc.

- 8.1.5 GungHo Online Entertainment Inc. ( SoftBank Group)

- 8.1.6 Electronic Arts Inc.

- 8.1.7 Kabam Games Inc.

- 8.1.8 Rovio Entertainment Corporation

- 8.1.9 NCsoft Corporation

- 8.1.10 NetEase Inc.