|

市場調査レポート

商品コード

1405092

航空機用排気システム:市場シェア分析、産業動向・統計、成長予測、2024~2029年Aircraft Exhaust Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| 航空機用排気システム:市場シェア分析、産業動向・統計、成長予測、2024~2029年 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

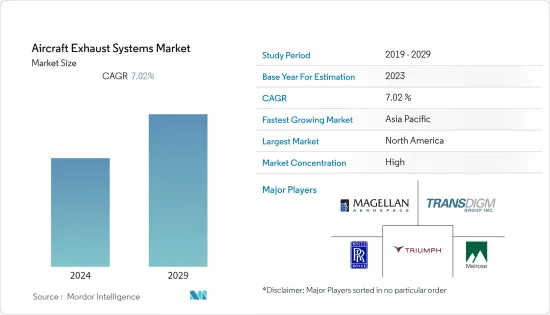

航空機用排気システム市場は2024年に10億6,000万米ドルと評価され、2029年には14億8,000万米ドルに達すると予測され、予測期間中のCAGRは7.02%を記録すると予想されます。

市場の成長は、予測期間中に多数の航空機納入が予定されている航空産業の有機的成長の成果です。航空機の排気システムは、適切な推進サイクルを確保するために不可欠です。新世代航空機とエンジンの統合は、排気システムの個々の部品に対する需要を促進します。

航空業界の既存企業は、新世代の航空機の性能特性を高めるため、新しい航空機推進技術の開発に熱心に投資しています。電子スラストリバーサー作動システム(ETRAS)のような新技術は、先進的なエンジン・サブシステムの開発に向けて投入される研究開発努力の原動力となります。ETRASは、電気機械式アクチュエータによって自動スラストリバーサ操作を可能にするハイブリッドシステムです。ETRASは、既存の電動スラストリバーサー作動コントローラー(ETRAC)と航空機エンジンのスラストリバーサーパワーユニット(TRPU)を物理的に1つのシステムに統合することで、エンジンの重量プロファイルを大幅に削減します。

航空機のターンアラウンドタイム(TAT)を短縮するために、自動ファイバー配置(AFP)のような新しい製造技術の使用が増加することが想定されています。ジェットエンジンの排気ダクトのような、T字型やY字型のチューブや円形のフランジを持つチューブなどの機体部品を製造するためです。

航空機用排気システム市場動向

予測期間では商用セグメントが市場をリード

商用航空は温室効果ガス排出の主な原因であるため、環境保護機関から世界の監視の対象となっています。航空機の燃焼サイクルは、排気システムなどのサブシステムを含むエンジン設計に直接影響されます。厳しい排出ガス規制は、高度な排気システムを備えた低燃費エンジンの設計における技術革新を促進すると予想されます。

さらに、排ガスレベルを抑制するために、航空用の電動パワートレインを開発するための研究開発イニシアチブが実施されています。例えば、2022年9月、調査チームは化学種トモグラフィーを用いて、商用航空機エンジンから排出されるCO2の画像を初めて撮影しました。研究者らは、新しい近赤外光イメージング技術を用いて、商用ジェットエンジンの排気プルーム中の二酸化炭素の断面画像を初めて撮影しました。この技術は、より環境に優しいエンジンや航空燃料の開発を目指したタービン燃焼研究を加速させる可能性があります。同様に2022年2月、米国のアーノルド・エンジニアリング・ディベロップメント・コンプレックスとメトロレーザーのエンジニアは、新しいタイプのレーザー測定システムを使用して、エンジン排気のガス速度をテストし、航空機からの騒音を低減する方法を見つけるのに役立っています。このような取り組みにより、予測期間中、商用航空機用排気システムのビジネス展望が高まることが予想されます。

予測期間中、アジア太平洋地域が最も高い需要を生み出す

アジア太平洋地域は、予測期間中に航空機用排気システム市場で最も高い需要を生み出すと予測されています。この需要は、同地域で増え続ける旅客輸送量に後押しされ、新しい航空機の発注が増加していることに起因しています。国際航空運送協会(IATA)は、2020年代半ばまでに中国が最終的に世界最大の航空市場になると予測しています。インド航空省によると、インドでは2030年までにヘリポートや水上飛行場を含む80~90の空港が新たに建設される予定です。巨大な市場ポテンシャルが、航空機OEM各社に、この地域への浸透を高めるための戦略的拡大計画を考案するよう促しました。その結果、航空機用排気システム市場の成長を支えることになります。

さらに、アジア太平洋地域は世界第2位の軍事支出を記録しました。この地域に蔓延する緊迫した地政学的シナリオは、各国の空中防衛能力を強化するための艦隊近代化プログラムの開始を促進しています。例えば、中国の2023年国防支出案は2,250億米ドルに上り、2022年予算を7.2%上回り、8年連続の軍事費増となった。同様に、インドは2023-24会計年度の国防費として726億米ドルを提案しており、前期の当初見積もりから13%増となっています。インドは戦闘機の増設を目指しています。

航空機用排気システム産業の概要

航空機用排気システム市場の特徴は、世界レベルで事業を展開する支配的なベンダーが限られていることです。市場競争は激しく、各業者は最大の市場シェアを獲得しようと競い合っています。航空機用排気システムの設計に関連する制約や、マクロ経済的要因による航空機受注のキャンセルが、市場の成長を阻害しています。ベンダーは、激しい市場競争の中で生き残るために、航空機OEMに高度なシステムを提供しなければならないです。市場を独占しているのは、GKN Aerospace(Melrose Industries PLC)、Triumph Group Inc.、Magellan Aerospace Corp.、Rolls-Royce plc、Esterline Technologies Corporation(Transdigm Group Inc.)などです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- 業界の魅力- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 航空タイプ

- 商用航空

- 軍用航空

- 一般航空

- システム

- エンジン排気

- APU排気

- その他

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- ロシア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- その他ラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- トルコ

- 南アフリカ

- その他中東・アフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Doncasters Limited

- Ducommun Incorporated

- Transdigm Group, Inc.

- Parker-Hannifin Corporation

- FRANKE Holding AG

- GKN Aerospace(Melrose Industries PLC)

- Magellan Aerospace Corporation

- Safran Nacelles(Safran)

- Rolls-Royce plc

- Sky Dynamics Corporation

- The NORDAM Group LLC

- Triumph Group Inc.

第7章 市場機会と今後の動向

The Aircraft Exhaust Systems Market is valued at USD 1.06 billion in 2024 and is anticipated to reach USD 1.48 billion by 2029, registering a CAGR of 7.02% during the forecast period.

The market's growth is an outcome of the organic growth of the aviation industry, as a large number of aircraft deliveries are scheduled during the forecast period. Aircraft exhaust systems are essential for ensuring a proper propulsion cycle. Integration of the engines with the new-generation aircraft will drive the demand for individual components of the exhaust systems.

The aviation industry incumbents are keenly investing in the development of new aircraft propulsion technologies to enhance the performance characteristics of newer-generation aircraft. Emerging technologies, like the electronic thrust reverser actuation system (ETRAS), will drive the R&D efforts divested toward developing advanced engine subsystems. ETRAS is a hybrid system that enables automated thrust reverser operation through electromechanical actuators. The ETRAS will physically combine the existing electrical thrust reverser actuation controller (ETRAC) and thrust reverser power unit (TRPU) of the aircraft engine into a single system, thereby reducing the engine's weight profile by a significant margin.

The increasing use of new manufacturing technologies, such as automated fiber placement (AFP), is envisioned to reduce the aircraft's turnaround time (TAT). It is to manufacture airframe components, such as tubes with a T-shape or Y-shape or tubes with circular shape flanges, like exhaust ducts, in jet engines.

Aircraft Exhaust Systems Market Trends

Commercial Segment to Lead the Market in the Forecast Period

Commercial aviation is a major source of greenhouse gas emissions and is, hence, being subjected to global scrutiny from environmental protection agencies. It led to the imposition of stringent emission norms to curb environmental degradation caused by the combustion of aviation fuel. In March 2017, the International Civil Aviation Organization (ICAO) adopted a new aircraft CO2 emission standard to be enforced on the new aircraft type designs from 2020 and the aircraft type designs already in production. The regulation also states the provisions for engine modification to ensure full compliance by 2028. The aircraft combustion cycle is directly influenced by the engine design, including subsystems, such as exhaust systems. The stringent emission norms are anticipated to drive technological innovations in the design of fuel-efficient engines with sophisticated exhaust systems. For instance, in July 2023, Power Flow Systems partnered with Maple Leaf Aviation to design dual exhaust system fairings for Cessna 180, 182, and 185 airframes. As per the agreement, Maple Leaf will produce the new set of exhaust fairings, while Power Flow will offer the specialized set at a 'combined package price' to its tuned exhaust system customers.

Moreover, in an effort to curb emission levels, R&D initiatives are being undertaken to develop an electric power train for aviation. For instance, in September 2022, Researchers captured the first images of CO2 emissions from a commercial aircraft engine using chemical species tomography. They used a novel near-infrared light imaging technique to capture the first cross-sectional images of carbon dioxide in the exhaust plume of a commercial jet engine. The technique could accelerate turbine combustion research aimed at developing engines and aviation fuels that are more environmentally friendly. Similarly, in February 2022, engineers at the Arnold Engineering Development Complex and MetroLaser in the US are using a new type of laser measurement system to test the gas velocity of engine exhaust and help find ways to reduce noise from aircraft. Such efforts are envisaged to enhance the business prospects of commercial aircraft exhaust systems during the forecast period.

Asia-Pacific to Generate the Highest Demand during the Forecast Period

The Asia-Pacific region is anticipated to generate the highest demand for the aircraft exhaust systems market during the forecast period. This demand can be attributed to the increasing orders of new aircraft, propelled by ever-growing passenger traffic in the region. The International Air Transport Association (IATA) projected that China will eventually become the world's largest aviation market by the mid-2020s. According to the Ministry of Aviation (India), 80-90 new airports, including heliports and water aerodromes, will be built by 2030 in India. The huge market potential encouraged aircraft OEMs to devise strategic expansion plans to increase their penetration into the region. It, in turn, will support the growth of the aircraft exhaust systems market.

Furthermore, the Asia-Pacific region registered the second-largest military expenditure across the world. The tense geopolitical scenario prevalent in the region is fostering the initiation of fleet modernization programs for enhancing the aerial defense capabilities of the countries. For instance, China's proposed 2023 defense spending rose to USD 225 billion, which is 7.2% higher than the 2022 budget and is the eighth consecutive year of increase in its military spending. Similarly, India proposed USD 72.6 billion in defense spending for the 2023-24 financial year, which is 13% up from the previous period's initial estimates. It is aiming to add more fighter jets. Such developments are anticipated to drive the market for aircraft exhaust systems during the forecast period.

Aircraft Exhaust Systems Industry Overview

The aircraft exhaust systems market is characterized by the presence of a limited number of dominant vendors operating at the global level. The market is highly competitive, with the players competing to gain the largest market share. Constraints associated with the design of aircraft exhaust systems and cancellation of aircraft orders due to macroeconomic factors impede the growth of the market. The vendors must provide advanced systems to aircraft OEMs to survive in an intensely competitive market environment. The dominant market players include GKN Aerospace (Melrose Industries PLC), Triumph Group Inc., Magellan Aerospace Corp., Rolls-Royce plc, and Esterline Technologies Corporation (Transdigm Group Inc.). These players compete mainly based on their in-house manufacturing capabilities, their global footprint network, their product offerings, their R&D investments, and a strong client base. The increase in the aircraft procurement rate, due to the rapid increase in air passenger traffic, is expected to fuel market growth during the forecast period. The competitive environment in the market is likely to further intensify due to an increase in product/service extensions and technological innovations. For instance, in March 2023, Power Flow Systems hit a milestone by delivering 6,500 systems since the first tuned exhaust system in 1999. To meet the growing demand and reduce the lead times for new orders, the company expanded its Daytona Beach and Florida branch production facility and workforce.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Aviation Type

- 5.1.1 Commercial Aviation

- 5.1.2 Military Aviation

- 5.1.3 General Aviation

- 5.2 System

- 5.2.1 Engine Exhaust

- 5.2.2 APU Exhaust

- 5.2.3 Other Systems

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Russia

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Mexico

- 5.3.4.3 Rest of Latin America

- 5.3.5 Middle East & Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Turkey

- 5.3.5.4 South Africa

- 5.3.5.5 Rest of Middle East & Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Doncasters Limited

- 6.2.2 Ducommun Incorporated

- 6.2.3 Transdigm Group, Inc.

- 6.2.4 Parker-Hannifin Corporation

- 6.2.5 FRANKE Holding AG

- 6.2.6 GKN Aerospace (Melrose Industries PLC)

- 6.2.7 Magellan Aerospace Corporation

- 6.2.8 Safran Nacelles (Safran)

- 6.2.9 Rolls-Royce plc

- 6.2.10 Sky Dynamics Corporation

- 6.2.11 The NORDAM Group LLC

- 6.2.12 Triumph Group Inc.