|

市場調査レポート

商品コード

1438287

シリコンフォトニクス:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Silicon Photonics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| シリコンフォトニクス:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

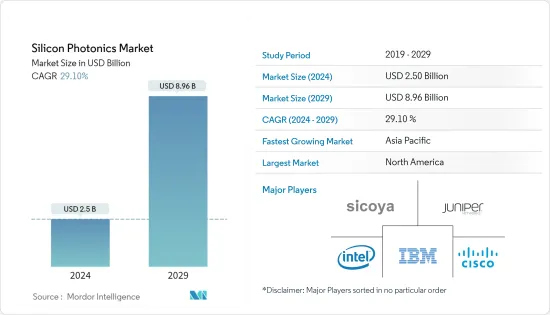

シリコンフォトニクス市場規模は、2024年に25億米ドルと推定され、2029年までに89億6,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に29.10%のCAGRで成長します。

主なハイライト

- シリコンフォトニクスは、高速伝送システムで使用される半導体で使用される導電体に比べて明らかな利点を提供するフォトニクスの発展分野です。この技術により、伝送速度が最大100 Gbpsまで向上すると予想されており、IBM、Intel、Kothuraなどの企業がこの技術を使用して画期的な進歩を遂げています。さらに、この技術は半導体業界に革命をもたらし、高速データ転送と処理を可能にします。

- 過去数十年にわたり、地上システムにとって光通信は重要になってきました。長距離のファイバー通信では、長距離にわたるデータ速度が大幅に向上しました。これらのシステムはチャネル容量の限界を押し広げ続けるため、世界中のビッグデータ転送のニーズに応えるために、より複雑な新しいテクノロジーが作成されています。シリコンフォトニクスはこれらの技術の1つです。確立されたシリコン製造技術を利用して実装された光コンポーネントは、低コスト、高歩留まり、小型フォームファクタ、低電力の光集積回路(PIC)を提供する上でかなりの可能性を示しています。

- クラウドサービスの普及により、近年データセンターの需要が急増しています。クラウドインフラストラクチャレポート 2021によると、回答者の57%がインフラストラクチャの半分以上がクラウドにあると回答し、64%が今後5年間で完全にパブリッククラウドになると予想しています。これらの動向は、期間中に調査された市場を推進する可能性があります。

- 2022年 1月、Qpisemiは、AI 2.0や、バイオインフォマティクス、創薬、AIモデリング、最適化、メタバース、製造などの他のさまざまなアプリケーションを強化するシリコンフォトニクスに基づくAIプロセッサーを発表しました。 AI 2.0プロセッサでは、ニューラルネットワークの計算を実行するために、電子ではなく光学プロセッサが使用されます。データセンターの場合、コード名AI20PXXのAI 2.0プロセッサは、GPUよりも100倍高速になる可能性があります。

- シリコンフォトニクスアプリケーションでは、熱やさまざまなノイズ源が光通信を妨害し、通常はフィルターで除去される周波数に光を押し込む可能性があります。これらのフィルターが変更されるまでデータは失われるか不完全になる可能性があり、ストリーミングデータの場合は再構築が複雑になる可能性があります。ただし、物理プロセスがいつ、どのように光を変化させるかを予測することは必ずしも簡単ではなく、そのため修正はさらに困難になります。

- 生産供給の面では、世界の半導体不足がCOVID-19のパンデミックと重なり、フォトニクスを含む大部分の産業に影響を及ぼしました。 AIM Photonicsによると、世界の半導体不足により、集積フォトニクスの革新が大幅に妨げられています。

シリコンフォトニクス市場動向

データセンターは最大の市場シェアを保持すると予想される

- 急増するハイパフォーマンスコンピューティング(HPC)アプリケーションやますます大規模化するデータセンターをサポートするために、特に高帯域幅の光トランシーバーで使用されるシリコンフォトニクスの需要が勢いを増し続けています。

- 企業と消費者からのトラフィックの増加により、2021年までにデータセンターの数が増加し、予測期間中にシリコンフォトニクス市場に巨大な範囲が提供される可能性があります。

- 企業内では、コンピューティングとコラボレーションがデータセンターのワークロードとコンピューティング需要の主な要因です。 Data Center World Global Conferenceによると、データセンターの平均数は3年以内(2021年までに)組織あたり約10.3となり、現在の組織あたり8.1から増加します。この急増により、全体としてパフォーマンスの向上が求められ、相互接続のボトルネックが解消され、シリコンフォトニクスの使用範囲が提供されます。

- データトラフィックの大幅な増加に加えて、Internet of Everything(IoE)をサポートするインフラストラクチャにより、人とオブジェクトの間のリアルタイム応答性の必要性が強調されています。データ処理とデータトラフィック管理では、クラウドコンピューティング、コグニティブコンピューティング、ビッグデータ分析をサポートする機能がますます必要になり、市場ベンダーにはタイムリーな対応を実現するために必要な速度と容量を提供するようプレッシャーがかかっています。

- シリコンナノフォトニクス技術は、光通信システムへの応用が進んでいます。シリコン光トランシーバ市場は、大規模データセンターと5Gテクノロジーからの需要により、今後数年間で大幅に成長すると予想されています。高速シリコンフォトニクスベースのテクノロジーにより、より高い帯域幅と改善された電力効率を備えたより小さなフォームファクタが可能になります。

- 消費者側では、ビデオ/メディアストリーミングが最も大きく貢献しています。潜在的なデータセンターのトラフィックを考慮して、Google、Facebook、Microsoftなどの主要企業は、地理的にデータセンターのボリュームを増やすことを計画しています。したがって、従来のエレクトロニクスと比較して長距離データ転送の必要性により、予測期間中にSiPの需要が増加する可能性があります。

アジア太平洋が最も急速な成長を遂げる

- 中国のシリコンフォトニクス市場は、成長する経済と高い世界エレクトロニクス市場シェアにより、アジア太平洋諸国の中でも大幅な成長率を示すと予想されています。中国は、著名なエレクトロニクス生産国および消費国の一つです。この地域では製造業が急速に成長しており、さまざまな製造技術や通信技術が継続的に導入されており、これが市場の成長を牽引すると予想されています。

- 「中国製造2025」計画などの中国政府のプログラムは、ファクトリーオートメーションと技術の研究開発活動とそれらへの投資を促進しています。ほとんどの自動化機器は他国から輸入されているため、「中国製」構想は自動化機器の国内生産を拡大することを目的としています。

- 日本はシリコンフォトニクス市場で大きなシェアを占めており、コラボレーションに対してよりオープンになってきています。大企業はトップの地位を維持したいと考えており、成長を促進するための投資を探しています。市場規模、新たな開放性、ダイナミックな業界は、日本の革新的な企業に確実に利益をもたらし、それによって日本の市場の成長を促進することができます。

- 韓国は市場に大きく貢献している国の一つです。人口の増加、シリコンフォトニクス製品の開発への投資の増加、最新のシリコンフォトニクス製品の開発に対する国内外のプレーヤーの注目の高まり、地域のデータ伝送速度を高めるための研究開発活動の増加も、市場の成長を促進しています。

- その他アジア太平洋地域地域として考慮される国には、インド、シンガポール、台湾が含まれます。 AI、5G、モノのインターネット、仮想現実、およびこれらの新技術の商業応用の急速な発展に伴い、データ処理と情報対話の需要が増大しており、これにより、この地域でのデータセンターの建設が加速され、業界の爆発的な成長につながります。 Cloud Sceneによると、データセンターの上位市場には、中国、日本、オーストラリア、インド、シンガポールが含まれます。

シリコンフォトニクス業界の概要

競合の度合いは、強力な競争戦略や企業の集中率など、市場に影響を与えるさまざまな要因によって決まります。この市場は、製品に多大な投資を行ってきた長年の実績のあるプレーヤーで構成されています。新しいプレーヤーが市場に参入しており、多額の投資が必要です。企業は強力な競争戦略を通じて維持することができます。したがって、調査対象の市場では、競争企業間の敵対関係は緩やかに高まっています。

- 2022年 2月- Intel CorporationはTower Semiconductorsを買収し、世界的に多様化した製品ポートフォリオで半導体需要の増大に対応できるようにしました。この買収により、同社は世界中の顧客ベースにファウンドリサービスを提供できるようになります。

- 2021年 9月- 帯域幅を大量に消費する高速通信ネットワーク向けのシリコンフォトニクスおよび高度なハイブリッドフォトニック集積回路ベースのレーザー、モジュール、およびサブシステムの開発会社であるNeoPhotonics Corporationは、新しい調整可能な高出力FMCW(周波数変調連続周波数)を発表しました。 レーザーモジュールと高出力半導体光増幅器(SOA)チップにより、帯域幅を大量に消費する高速通信ネットワークに対応します。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- シリコンフォトニクスベースのトランシーバーの使用による消費電力の削減

- データセンター間の高速接続と高度なデータ転送機能に対するニーズの高まり

- 市場抑制要因

- 熱影響の危険性

- 産業バリューチェーンチェーン分析

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 用途

- データセンター

- 電気通信

- その他の用途

- 地域

- 北米

- 欧州

- アジア太平洋

- 世界のその他の地域

第6章 競合情勢

- 企業プロファイル

- Sicoya GMBH

- Intel Corporation

- Cisco Systems Inc.

- NeoPhotonics Corporation

- IBM Corporation

- Juniper Networks Inc.

- Global Foundries

- Broadcom Limited

第7章 投資分析

第8章 市場機会と将来の動向

The Silicon Photonics Market size is estimated at USD 2.5 billion in 2024, and is expected to reach USD 8.96 billion by 2029, growing at a CAGR of 29.10% during the forecast period (2024-2029).

Key Highlights

- Silicon photonics is a developing branch of photonics offering a clear advantage over electric conductors used in semiconductors used in high-speed transmission systems. This technology is expected to push the transmission speeds up to 100 Gbps, with companies such as IBM, Intel, and Kothura achieving breakthroughs using the technology. Besides, this technology revolutionizes the semiconductor industry, enabling high-speed data transfer and processing.

- Optical communications have grown critical for terrestrial systems for the past several decades. Vast-haul fiber communications have seen significant gains in data speeds over long distances. New and more complicated technologies have been created to keep up with the need for worldwide big data transfer, as these systems continue to push the channel capacity boundaries. Silicon photonics is one of these technologies. Photonic components implemented utilizing established silicon fabrication techniques have shown considerable possibilities in providing low-cost, high-yield, tiny form-factor, and low-power photonic integrated circuits (PICs).

- Due to the widespread use of cloud services, the demand for data centers has surged in recent years. According to the Cloud Infrastructure Report 2021, 57% of respondents said more than half of their infrastructure is in the cloud, and 64% expect to be entirely in the public cloud in the next five years. These trends may drive the market studied over the period.

- In January 2022, Qpisemi unveiled AI processors based on silicon photonics to power AI 2.0 and various other applications, such as bioinformatics, drug discovery, AI modeling, optimization, metaverse, and manufacturing. Optical processors, rather than electrons, are used in AI 2.0 processors to perform neural-network calculations. For data centers, AI 2.0 processors, codenamed AI20PXX, may be 100 times quicker than GPUs.

- In silicon photonics applications, heat and various noise sources can disturb optical communications, pushing light into frequencies that are usually filtered out. Data may be lost or incomplete until those filters are modified, and reconstruction may be complex in the case of streaming data. However, forecasting when and how physical processes alter light is not always easy, making the modifications more challenging.

- On the production supply front, the global semiconductor shortage coincided with the COVID-19 pandemic and affected the majority of industries, including photonics. As per AIM Photonics, the global semiconductor shortage has hampered innovation in integrated photonics to a great extent.

Silicon Photonics Market Trends

Data Centers are Expected to Hold the Maximum Market Share

- The demand for silicon photonics, particularly used in high-bandwidth optical transceivers, continues to gain impetus to support proliferating high-performance computing (HPC) applications and ever-larger data centers.

- The rise in the number of data centers through 2021 due to the increased traffic from the enterprises and the consumers may provide a huge scope for the silicon photonics market during the forecast period.

- Within the enterprise, computing and collaboration are the main contributors to data center workload and computation demand. According to the Data Center World Global Conference, the average number of data centers will be approximately 10.3 per organization in three years (by 2021), which is up from the current 8.1 per organization. This surge calls for improved performance, on the whole, removing the interconnect bottlenecks and providing scope for the use of silicon photonics.

- In addition to the massive growth in data traffic, the infrastructure supporting the Internet of Everything (IoE) emphasizes the need for real-time responsiveness between people and objects. Increasingly, data processing and data traffic management require the ability to support cloud computing, cognitive computing, and big data analysis, pressurizing the market vendors to offer the necessary speed and capacity to deliver a timely response.

- Silicon nanophotonics technology is being increasingly applied to optical communication systems. The silicon optical transceiver market is expected to grow manifold in the next few years, driven by demand from large data centers and 5G technology. High-speed silicon photonics-based technologies are enabling smaller form factors with higher bandwidth and improved power efficiency.

- On the consumer side, video/media streaming is the most significant contributor. In the light of the potential data center traffic, key businesses like Google, Facebook, and Microsoft, are planning to ramp up their data center volumes across geographies. Therefore, the need for long-distance data transfer compared to traditional electronics may increase the demand for SiP during the forecast period.

Asia-Pacific to Witness the Fastest Growth

- China's silicon photonics market is expected to exhibit a significant growth rate among Asia-Pacific countries, owing to its growing economy and high global electronics market share. China is one of the prominent electronics producers and consumers. The manufacturing industry is rapidly growing in the region and is witnessing the continuous deployment of various manufacturing and telecommunications technologies, which is expected to drive the market's growth.

- The Chinese government's programs, such as the Made in China 2025 plan, are promoting R&D activities in factory automation and technologies and investments in them. As most automation equipment are imported from other countries, the 'Made in China' initiative aims to expand its domestic production of automation equipment.

- Japan holds a significant share in the silicon photonics market and is becoming more open to collaborations. Big corporations want to stay on top and look for investments to fuel growth. The market size, emerging openness, and dynamic industry can surely benefit innovative companies in Japan, thereby driving the market's growth in Japan.

- South Korea is one of the major contributors to the market. Growing population, increasing investments in the development of silicon photonic products, the rising focus of international and domestic players on the development of modern silicon photonic products, and increasing R&D activities to increase the region's data transmission rate are also fueling the market's growth.

- The countries considered under the rest of Asia-Pacific include India, Singapore, and Taiwan. With the rapid development of AI, 5G, the internet of things, virtual reality, and the commercial application of these new technologies, the demand for data processing and information interaction is growing, which would speed up the construction of data centers in the region and lead to the explosive growth of the industry. According to Cloud Scene, some of the top markets in data centers include China, Japan, Australia, India, and Singapore.

Silicon Photonics Industry Overview

The degree of competition depends on various factors affecting the market, such as powerful competitive strategies and firm concentration ratio. The market comprises long-standing established players who have made significant investments in the product. The new players are entering the market and require high investments. The companies can sustain through powerful competitive strategies. Therefore, the competitive rivalry is moderately growing in the market studied.

- February 2022 - Intel Corporation acquired Tower Semiconductors to enable a globally diversified product portfolio to meet the growing demand for semiconductors. This acquisition also enables the company to provide foundry services to a global customer base.

- September 2021 - NeoPhotonics Corporation, a developer of silicon photonics and advanced hybrid photonic integrated circuit-based lasers, modules, and subsystems for bandwidth-intensive, high-speed communications networks, announced a new, tunable high-power FMCW (frequency-modulated continuous wave) laser module and high-power semiconductor optical amplifier (SOA) chips for bandwidth-intensive, high-speed communication networks.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Reduction in Power Consumption With the Use of Silicon Photonics Based Transceivers

- 4.2.2 Growing Need for High Speed Connectivity and High Data Transfer Capabilities Across Data Centers

- 4.3 Market Restraints

- 4.3.1 Risk of Thermal Effect

- 4.4 Industry Value Chain Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Data Center

- 5.1.2 Telecommunications

- 5.1.3 Other Applications

- 5.2 Geography

- 5.2.1 North America

- 5.2.2 Europe

- 5.2.3 Asia-Pacific

- 5.2.4 Rest of the World

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Sicoya GMBH

- 6.1.2 Intel Corporation

- 6.1.3 Cisco Systems Inc.

- 6.1.4 NeoPhotonics Corporation

- 6.1.5 IBM Corporation

- 6.1.6 Juniper Networks Inc.

- 6.1.7 Global Foundries

- 6.1.8 Broadcom Limited