|

|

市場調査レポート

商品コード

1273524

失禁器具とオストミー市場- 成長、動向、予測(2023年-2028年)Incontinence Devices and Ostomy Market - Growth, Trends, and Forecasts (2023 - 2028) |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| 失禁器具とオストミー市場- 成長、動向、予測(2023年-2028年) |

|

出版日: 2023年04月14日

発行: Mordor Intelligence

ページ情報: 英文 115 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

失禁とストーマケア製品市場は、予測期間中に10.1%近いCAGRで推移すると予想されます。

COVID-19パンデミックの発生は、失禁器具とオストミービジネスに大きな影響を与え、発生後に行われたのは最も急性なオストメイト手術のみでした。ストーマケアは見落とされがちな側面であり、パンデミック中に特定のストーマケアに関する勧告は発表されていません。2022年3月に国立医学図書館から発表された研究によると、2020年3月から2021年2月までの間にオストメイトは19.5%減少しています。このように、パンデミック時にはオストメイトに関連する手術の減少が市場の成長を阻害しました。しかし、ほとんどの患者が自宅での治療を選択したため、同時期に自宅ケア用のストーマケア製品の需要はかなり増加しました。したがって、COVID-19は市場の成長に大きな影響を与えました。しかし、COVID-19の症例が沈静化するにつれて、市場は非常によく回復しており、予測期間中も同じ傾向を維持すると思われます。

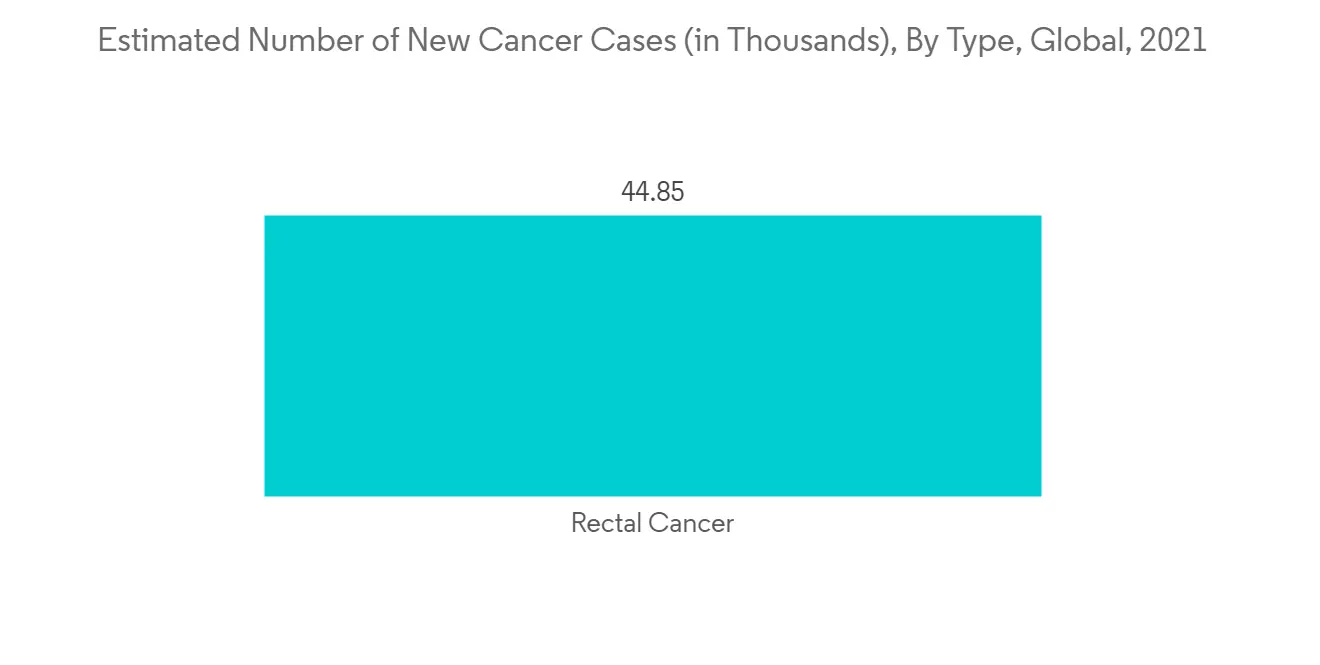

調査した市場の成長に寄与する主な要因は、炎症性腸疾患(IBD)の高い有病率、潰瘍性大腸炎やクローン病などの尿失禁(UI)の有病率の上昇、大腸がんによるオストミー手術例の増加です。2021年7月のWHOの更新情報によると、2030年までに全世界で大腸がん患者が約70%増加することが予想されています。さらに、GLOBOCANが発表した統計によると、大腸がん(CRC)はドイツの人口の中で4番目に多いがん種であり、2021年にはドイツで約57,528人のCRCの新規症例が報告されました。さらに、GLOBOCANが提供する統計によると、2020年に英国で約33,815人の結腸がんの新規症例と11,951人の新規死亡が報告され、オストメイト手術およびデバイスの需要が増加し、予測期間中の市場成長を後押ししています。さらに、2022年4月にFemale Pelvic Medicine &Reconstructive Surgeryが発表した研究によると、女性の61.8%が尿失禁(UI)を抱えており、米国の成人女性7829万7094人に相当し、2021年には全体の32.4%が少なくとも毎月症状を報告しています。UIを持つ人のうち、37.5%がストレス性尿失禁、22.0%が切迫性尿失禁、31.3%が混合症状、9.2%が特定不能の失禁であることがわかりました。このように、女性におけるUIの高い負担は、失禁製品の需要を増加させると予想され、予測期間中の市場の成長を後押しすると考えられています。

オストメイト患者の生活の質の向上に役立つ、効率的で適切なパウチングシステムと関連アクセサリーの開拓は、予測期間中、調査対象市場の成長の地平を開くと期待されています。例えば、トリオヘルスケアは、シリコンベースのオストミー用シール「トリオシルタック」を発売しました。この製品は、漏れを防ぎ、ストーマ周囲の皮膚を保護するのに役立ちます。このような技術的進歩は、予測期間中、市場の成長を促進すると予想されます。

さらに、個人のオストメイトに対する意識を高めるための取り組みが増加していることも、市場の成長をさらに後押ししています。例えば、United Ostomy Association of America Inc.(UOAA)は、オストミー・ヘルスケアの質を向上させ、すべての医療環境におけるより高い水準のケアを促進するために活動しています。同団体は、毎年10月の第1土曜日に「世界オストミー・デー」を開催し、ストーマケアに関する意識を高めています。このような取り組みにより、一般住民のストーマケアに対する意識が高まり、市場の成長を後押しすると考えられます。

しかし、適切な償還が行われていないこと、オストミーや失禁製品の使用に伴う合併症が、市場の成長を抑制する可能性があります。

失禁器具とオストミーの市場動向

人工肛門バッグは用途別セグメントで有利な成長が期待される

人工肛門バッグは、ストーマバッグやオストミーバッグとも呼ばれ、体内の排泄物を回収するために使用される小型の防水ポーチです。人工肛門と呼ばれる外科手術では、大腸と腹壁の間にストーマまたはオストミーと呼ばれる開口部が形成されます。これにより、老廃物は大腸から直腸、肛門を経由するのではなく、腹壁の開口部から排泄されるようになります。便やその他の老廃物は、袋状の人工肛門バッグに排出され、定期的に空っぽにすることができます。

炎症性腸疾患(IBD)の増加により、このバッグの需要は年々増加しています。例えば、2021年8月にBMC Journalに掲載された調査研究によると、英国では、2021年の炎症性腸疾患(IBD)、クローン病(CD)、潰瘍性大腸炎(UC)の発症率は、人口10万人あたりそれぞれ28.6、10.2、15.7と判明しています。こうした疾患の発症率の高さが、市場成長の原動力となることが期待されます。

さらに、製品の発売数の増加も、今後数年間におけるセグメントの成長をさらに促進すると予想されます。オストメイト患者の生活の質の向上に役立つ効率的で適切なオストメイトバッグのイントロダクションは、このセグメントの成長に十分な成長機会を提供すると期待されています。例えば、2021年6月、カーディフにあるペリカンヘルスケア社は、ModaViostomyバッグシリーズの導入により、英国およびアイルランドのヘルスケア分野における使い捨てストーマデバイスの主要メーカーの1つとしての地位を強化しました。

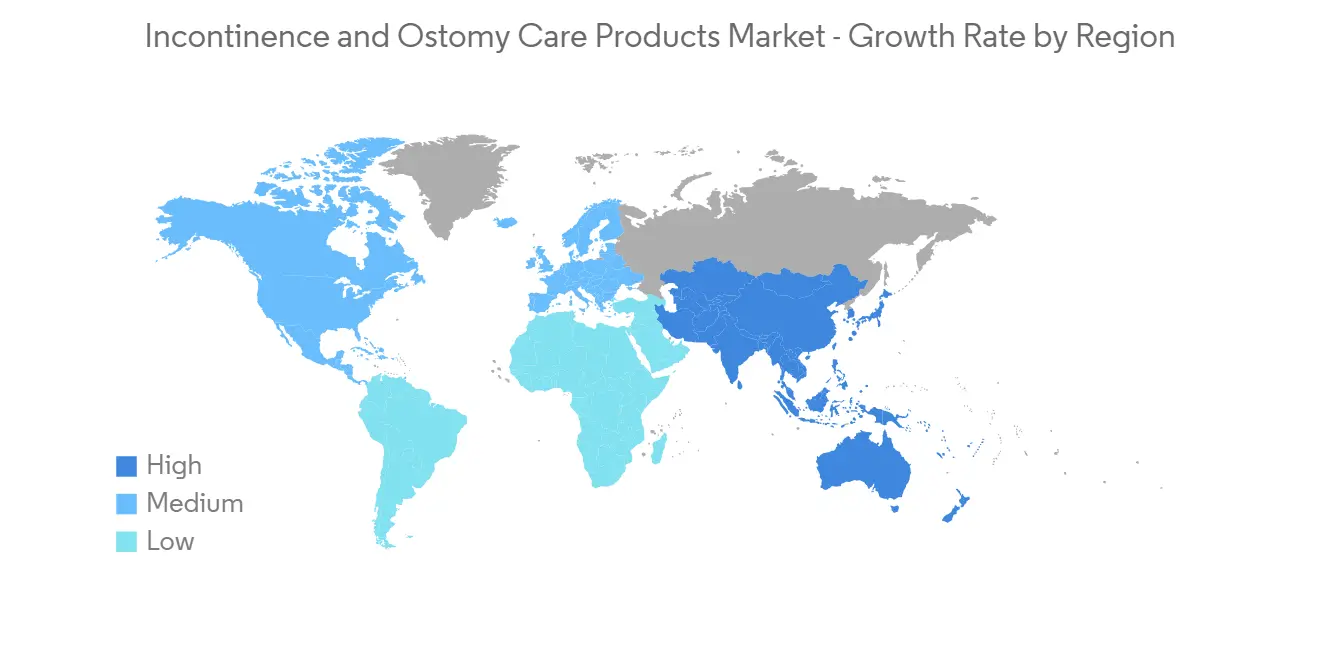

北米が市場を独占し、予測期間中も同様と予想される

北米は、クローン病や潰瘍性大腸炎による患者数の増加、ストーマケアやストーマ手術に関する意識の高まりなどの要因から、失禁・ストーマケア製品市場を独占し、最大の収益シェアを占めています。

2023年のジョンズ・ホプキンス大学の論文によると、2,500万人以上の成人アメリカ人が一時的または慢性の尿失禁を経験しています。さらに、米国だけでもUIの治療費は163億米ドルで、その75%は女性の治療に費やされています。このように米国では尿失禁の有病率が高まっており、市場の成長を促進すると予想されます。

さらに、複数の市場関係者が、市場の成長を支える様々な戦略的イニシアチブを実施しています。例えば、2021年4月、ウェランド・メディカルは、販売代理店であるプレミア・オストミー・センターを通じて、カナダでの事業を拡大しました。カナダに住む人々が直接利用することができます。このような新興国市場の開拓は、予測期間中、同国での市場成長を後押しすると考えられます。さらに、2022年1月には、Owens &Minor Inc.とApria Inc.が、Owens &MinorがApriaを買収する正式契約を締結しました。この買収により、同社のオストミー製品のポートフォリオが拡大すると予想されます。

失禁器具とオストミー産業の概要

失禁器具とオストミー介護用品市場は競争が激しく、多くの主要企業で構成されています。Abena AS、B. Braun Melsungen AG、Coloplast Corporation、ConvaTec、Hollister Inc.、Kimberly-Clark Corporationなどの企業が、市場でかなりのシェアを占めています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 本調査の対象範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 世界の失禁の増加

- 腎臓疾患および腎臓損傷の有病率の増加

- オストミー(人工肛門)ケア製品に関する認識と受容の高まり

- 市場抑制要因

- 適切な保険償還の欠如

- オストミーと失禁用品の使用に関連する合併症

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- 製品タイプ別

- 失禁ケア製品

- 吸収体

- 失禁バッグ

- その他の製品タイプ(クランプ、消臭剤、クリーナー、尿器など)

- オストミー用ケア用品

- オストミー用バッグ

- 人工肛門用バッグ

- イレオストミーバッグ

- ウロストミーバッグ

- スキンバリア

- イリゲーション製品

- その他の人工肛門用製品

- 失禁ケア製品

- 用途別

- 膀胱がん

- 大腸がん

- クローン病

- 腎臓結石

- 慢性腎不全

- その他の用途

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ地域

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米地域

- 北米

第6章 競合情勢

- 企業プロファイル

- Abena AS

- B. Braun Melsungen AG

- Coloplast Corporation

- ConvaTec

- Hollister Inc.

- Kimberly-Clark Corporation

- Salts Healthcare

- Unicharm Corporation

- Welland Medical

- Pelican Healthcare Ltd.

- Flexicare(Group)Limited

- Torbot Group, Inc.

第7章 市場機会および将来動向

The incontinence and ostomy care product market is expected to register a CAGR of nearly 10.1% during the forecast period.

The outbreak of the COVID-19 pandemic significantly impacted the incontinence devices and ostomy business, as only the most acute ostomy surgeries were performed following the outbreak. Stoma care is a potentially overlooked aspect of the outbreak, and no specific stoma care recommendations were published during the pandemic. According to the study published by the National Library of Medicine in March 2022, ostomies decreased by 19.5% during the time between March 2020 and February 2021. Thus, the decline in surgeries related to ostomies hampered the growth of the market during the pandemic. However, the demand for ostomy care products for home care considerably increased during the same period as most patients opted for home treatments. Hence, COVID-19 had a significant impact on market growth. However, as COVID-19 cases have subsided, the market has been recovering very well and is likely to maintain the same trend over the forecast period.

The major factor contributing to the growth of the market studied is the high prevalence of inflammatory bowel diseases (IBD), rising prevalence of urinary incontinence (UI), including ulcerative colitis or Crohn's disease, and colorectal cancer, resulting in increased ostomy surgery cases. According to the WHO updates from July 2021, an increase of around 70% is expected in colorectal cancer cases across the world by 2030. Furthermore, according to statistics published by GLOBOCAN, colorectal cancer (CRC) is the fourth most common type of cancer among the German population, and approximately 57,528 new cases of CRC were reported in Germany in 2021. Additionally, according to statistics provided by GLOBOCAN in 2020, approximately 33,815 new cases of colon cancer and 11,951 new deaths were reported in the United Kingdom in 2020 increasing the demand for ostomy surgeries and devices, thereby boosting the market growth over the forecast period. Moreover, as per a study published in April 2022 by Female Pelvic Medicine & Reconstructive Surgery, 61.8% of women had urinary incontinence (UI), corresponding to 78,297,094 adult United States women, with 32.4% of all women reporting symptoms at least monthly in 2021. Of those with UI, 37.5% had stress urinary incontinence, 22.0% had urgency urinary incontinence, 31.3% had mixed symptoms, and 9.2% had unspecified incontinence. Thus, a high burden of UI in women is expected to increase the demand for incontinence products which is expected to boost the growth of the market over the forecast period.

The development of efficient and suitable pouching systems and associated accessories which help to improve the quality of life of ostomy patients, is expected to open up the growth horizons for the studied market over the forecast period. For instance, the company Trio Healthcare launched a silicone-based ostomy seal, Trio Siltac. This product aids in preventing leakage and protecting the skin around the stoma. Such technological advancements are anticipated to propel the market growth over the forecast period.

Furthermore, an increase in initiatives to raise awareness about ostomy in individuals further propels the growth of the market. For instance, the United Ostomy Association of America Inc. (UOAA) works to improve the quality of ostomy healthcare and promote higher standards of care in all healthcare settings. The organization commemorates World Ostomy Day on the first Saturday of October every year to raise awareness about ostomy care. Such initiatives is likely to create awareness among the general population about stoma care, thereby aiding market growth.

However, lack of proper reimbursement and complications associated with ostomy and usage of incontinence products are likely to restrain the market growth.

Incontinence Devices and Ostomy Market Trends

Colostomy Bags are Expected to Observe Lucrative Growth in the Application Segment

A colostomy bag also called a stoma bag, or ostomy bag, is a small, waterproof pouch used to collect waste from the body. During a surgical procedure known as a colostomy, an opening, called a stoma or ostomy, is formed between the large intestine (colon) and the abdominal wall. This allows waste products to be excreted through the opening in the abdominal wall rather than via the colon through the rectum and anus. Stools and other waste products are drainable into the pouch-like colostomy bag, which can then be emptied at regular intervals.

The demand for these bags has increased over the years due to the increasing incidence of inflammatory bowel diseases (IBD). For instance, according to the research study published in BMC Journal in August 2021, in the United Kingdom, the incidence of inflammatory bowel disease (IBD), Crohn's disease (CD), and ulcerative colitis (UC) were found to be 28.6, 10.2, and 15.7 per 100,000 population, respectively in 2021. Such a high incidence of these diseases is expected to drive market growth.

Furthermore, the rising number of product launches is also expected to further drive segmental growth in the coming years. The introduction of efficient and suitable ostomy bags which help to improve the quality of life of ostomy patients is expected to provide ample growth opportunities for the segment's growth. For instance, in June 2021, Pelican Healthcare Ltd., located in Cardiff, strengthened its position as one of the leading manufacturers of disposable stoma devices in the United Kingdom and Ireland healthcare sectors with the introduction of the ModaViostomy bag range.

North America Dominates the Market and is Expected to do the Same in the Forecast Period

North America dominated the incontinence and ostomy care products market and accounted for the largest revenue share owing to factors such as an increase in the number of patients due to Crohn's disease, ulcerative colitis, and rising awareness initiatives related to ostomy care or stoma surgical procedures.

As per a Johns Hopkins University article of 2023, more than 25 million adult Americans experience temporary or chronic urinary incontinence. Additionally, the cost of treatment of UI in the United States alone is USD 16.3 billion, 75% of which is spent on the treatment of women. This increasing prevalence of UI in the United States is expected to propel the market's growth.

Moreover, several market players are implementing various strategic initiatives that support the market's growth. For instance, in April 2021, Welland Medical expanded its business in Canada through its distributor, Premier Ostomy Centre. It is directly available to people living in Canada. Such developments are likely to boost the market growth in the nation over the forecast period. Additionally, in January 2022, Owens & Minor Inc. and Apria Inc. entered into a definitive agreement under which Owens & Minor will acquire Apria. The acquisition is anticipated to broaden the company's ostomy portfolio.

Incontinence Devices and Ostomy Industry Overview

The incontinence devices and ostomy care products market is highly competitive and consists of a number of major players. Companies like Abena AS, B. Braun Melsungen AG, Coloplast Corporation, ConvaTec, Hollister Inc., and Kimberly-Clark Corporation, among others, hold substantial shares in the market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Incontinence Around the World

- 4.2.2 Increasing Prevalence of Renal Diseases and Nephrological Injuries

- 4.2.3 Growing Awareness and Acceptance regarding Ostomy Care Products

- 4.3 Market Restraints

- 4.3.1 Lack of Proper Reimbursement

- 4.3.2 Complications Associated with Ostomy and Usage of Incontinence Products

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Product Type

- 5.1.1 Incontinence Care Products

- 5.1.1.1 Absorbents

- 5.1.1.2 Incontinence Bags

- 5.1.1.3 Other Product Types (Clamps, Deodorizers, Cleaners, Urinals, etc.)

- 5.1.2 Ostomy Care Products

- 5.1.2.1 Ostomy Bags

- 5.1.2.1.1 Colostomy Bags

- 5.1.2.1.2 Ileostomy Bags

- 5.1.2.1.3 Urostomy Bags

- 5.1.2.2 Skin Barriers

- 5.1.2.3 Irrigation Products

- 5.1.2.4 Other Ostomy Products

- 5.1.1 Incontinence Care Products

- 5.2 By Application

- 5.2.1 Bladder Cancer

- 5.2.2 Colorectal Cancer

- 5.2.3 Crohn's Disease

- 5.2.4 Kidney Stone

- 5.2.5 Chronic Kidney Failure

- 5.2.6 Other Applications

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Abena AS

- 6.1.2 B. Braun Melsungen AG

- 6.1.3 Coloplast Corporation

- 6.1.4 ConvaTec

- 6.1.5 Hollister Inc.

- 6.1.6 Kimberly-Clark Corporation

- 6.1.7 Salts Healthcare

- 6.1.8 Unicharm Corporation

- 6.1.9 Welland Medical

- 6.1.10 Pelican Healthcare Ltd.

- 6.1.11 Flexicare (Group) Limited

- 6.1.12 Torbot Group, Inc.