|

市場調査レポート

商品コード

1432812

スマートウェアラブル:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)Smart Wearable - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| スマートウェアラブル:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

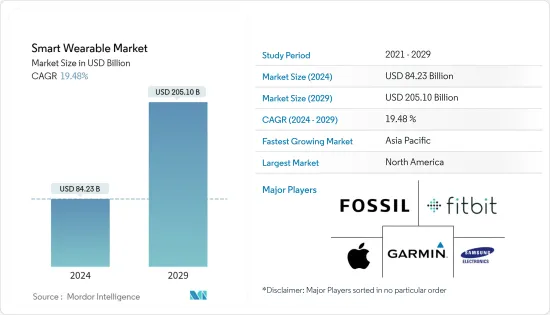

スマートウェアラブル市場規模は2024年に842億3,000万米ドルと推定され、2029年には2,051億米ドルに達すると予測され、予測期間中(2024-2029年)のCAGRは19.48%で成長する見込みです。

調査の進歩は近年の技術革新の増加につながり、ウェアラブル市場の需要を牽引しています。また、スマートファブリックやヒアラブルなど、日常生活にハイエンドの技術とデザインを取り入れた新しい製品カテゴリーも生まれています。最近では、顧客を惹きつけるためにデバイスに美しいデザインを提供することに焦点が当てられています。

主なハイライト

- 新たな動向であるウェアラブルテクノロジーは、エレクトロニクスを日常活動に統合し、体のどの部分にも装着できる機能でライフスタイルの変化に対応します。インターネットへの接続機能や、ネットワークとデバイス間のデータ交換オプションといった動向が、ウェアラブル技術の動向を牽引しています。

- ウェアラブルは、消費者全体のフィットネス傾向のブームにより、大きな支持を得ています。シスコシステムズによると、接続されたウェアラブルデバイスは2018年の5億9,300万台から今年は11億500万台に増加すると予想されています。スマートウォッチ・カテゴリーは、日常的なライフスタイルに合ったブランドのような追加機能により、上昇を経験しています。アップルやフォッシルのような強力なブランドは、収益を維持するために従来の腕時計の価格帯と一貫した価格設定を維持しています。グーグルのWearOSにより、TAGやアルマーニなど多くの高級時計メーカーがこのセグメントに参入しています。

- 世界各地で都市化の浸透率が上昇しているため、1つのデバイスに複数の機能を搭載したり、タイムスケジュールを表示したりするなど、消費者の要求に応えるため、先進的で審美的に魅力的な製品への需要が高まっています。さらに、世界中の膨大なミレニアル世代は、彼らの通常の勤務時間の追跡と贅沢な基準で増加した支出能力のために、スマートウォッチを採用するのが早かった。

- ヒアラブルは、スマートアシスタントの受け入れが進むにつれて人気を集めています。Bragi、Google、Apple、Jabra、Samsung、Sonyなどの企業がこの分野の成長に積極的に貢献しています。

- COVID-19の発生と世界各地の封鎖規制は、世界中の産業活動に影響を及ぼしています。エレクトロニクス産業は、サプライチェーンや生産設備に大きな影響を受け、深刻な打撃を受けました。中国と台湾では2月から3月にかけて生産が停止し、世界中のさまざまなOEMに影響を与えました。

スマートウェアラブル市場動向

ヘッドマウントディスプレイが市場需要を牽引する見込み

- ヘッドマウントディスプレイは、単眼HMDまたは両眼HMDの前に小型のディスプレイ光学系を備えた装置で、頭部に装着するかヘルメットの一部として着用します。これらは主に、ゲーム、航空、エンジニアリング、医療など、さまざまな目的で使用されています。ヘッドアップディスプレイは、ユーザーの視界を遮るのではなく、現実世界を見るユーザーの視界に画像を重ね合わせる。ヘッドアップディスプレイの新たな形態として、網膜の敏感な部分に直接画像を投影する網膜ディスプレイがあります。しかし、画像はユーザーの理想的な視聴距離にあるスクリーン上に表示されます。それでも、ユーザーの目の前に実際のスクリーンがあるわけではないです。ヘッドマウントディスプレイには、画像をユーザーの目に反射させる改造メガネのような特殊な光学部品が含まれています。ヘッドマウント・ディスプレイの中には、方向や動きを判断するためのモーション・センサーや、没入型バーチャル・リアリティ・アプリケーションのインターフェースとして搭載されているものもあります。

- ディスプレイはHMDの不可欠な部分であり、一般的に仮想現実(VR)機器と拡張現実(AR)機器に分類されます。ARデバイスは透明なディスプレイを持ち、現実の物体にデジタル情報を重ね合わせる。これらのHMDはOptical head-mounted displaysまたはOHMDとして知られています。VRデバイスでは、ディスプレイは透明ではなく、仮想的な情報と画像のみが装着者の目の前に存在します。

- 機能性に基づいて、処理HMDはさらにスライドオンHMD、ディスクリートHMD、統合HMDに分類されます。スライド式HMDは最も費用対効果が高く、利用しやすいVRの形態で、スマートフォンホルダー、レンズ、いくつかの一次入力で構成されます。スマートフォンをスライド式HMDに装着し、デバイス全体をユーザーの目の上で再生することでVR体験を実現します。このように、表示、処理、回転トラッキングにスマートフォンを利用します。しかし、スマートフォンに頼るのではなく、独自のIMUを使用するものもあります。例えば、サムスンのGear VRは内蔵IMUを利用しています。

- ディスクリートHMDは、処理以外にディスプレイ、レンズ、回転トラッキング、位置トラッキング、音声、高度な入力を備えています。そのため、処理のためにパソコンとの接続が必要となります。最高のVR体験を提供するが、スライド式や一体型のHMDに比べると機動性に劣る。テザー型HMDとも呼ばれ、Oculus Rift、HTC Vive、PlayStation VRなどがあります。

- 一体型HMDは最も先進的で高価なHMDであり、OHMDでもあります。PCやスマートフォンなどの外部ハードウェアなしでVRやAR体験を提供する独立したコンピューティングデバイスです。ディスプレイ、プロセッサ、カメラを内蔵し、立体3D画像の表示、複雑なトラッキングの実行、高度な入力方法の利用が可能です。現在、ほとんどの統合型HMDは高価格帯のAR OHMDであり、ビジネスプロフェッショナルのみをターゲットとしています。最も人気のある一体型HMDは、Microsoft HoloLens、Google Glass、Magic Leapなどです。

アジア太平洋地域が最も速い成長率を示す

- アジア太平洋地域は、予測期間中にスマートウェアラブル市場で最も高い成長を示すと予想されています。同地域ではエレクトロニクス産業の成長と可処分所得の急増がスマートウェアラブル市場を牽引しています。

- 中国では、裕福な消費者の購買意欲が高まっていることもあり、ウェアラブル市場はこれまでとは異なる様相を呈しています。例えば、中国の政府系シンクタンクによる最近の報告書によると、世界のスマート・ウェアラブルデバイスの約80%が、中国南東部の港湾都市であり製造拠点である中国で製造されているといいます。中国情報産業開発センターの報告書によると、多くの中国ハイテク大手のベースキャンプである深センは、スマート・ウェアラブルの最も広範なR&D(研究開発)および生産拠点です。

- 今年3月、インド携帯電話電子協会(ICEA)によると、PMPはスマート・ウェアラブルを生産するための逆義務構造を合理化しました。インド政府は、携帯電話やラップトップ/タブレット型コンピュータの現地生産を促進した後、手首に装着するウェアラブルガジェット、聴覚デバイス、電子スマート・メーターを製造するための新たな段階的製造プログラム(PMP)を開始しました。

- さらに、フィットネスに関する意識の高まり、技術の進歩、高速インターネット接続の利用可能性が、同国のスマート・ウェアラブル市場の成長を促進する主な要因となっています。

スマートウェアラブル産業の概要

スマートウェアラブル市場は競争が激しく、近年は競争力を獲得しています。さらに、プレーヤーは、主にミレニアル世代の人口の需要に応えることで、この急成長市場で競争優位性を獲得しています。

- 2022年9月-U&iは、アクティブなライフスタイルのための3つのプレミアムウェアラブルの発売を発表しました。スマートウォッチはリアルタイムで、ウォーキング、ランニング、ジョギングなど複数の身体活動を感知できるスポーツモードも搭載し、ユーザーの健康維持と活動をサポートします。

- 2022年5月-Vuzix Corporationはフランスに拠点を置くmLED(micro-Light Emitting Diode)ディスプレイソリューション企業であるAtomistic SAS(アトミスティック)と契約を締結したと発表しました。この契約はカスタムバックプレーンの設計、主要なmLED技術の独占ライセンス、そして様々な技術段階の達成次第で企業を買収する能力を提供するものです。Atomistic社は、先進ノード300mmウェハー上にバックプレーンを提供し、ウエハーからのシステムレベルのサポートとともに、同社の革新的な材料科学に基づく今後のmLEDと、潜在的なサードパーティサプライヤーの代替LEDをサポートする予定です。mLEDはARグラスに提供される予定です。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場の概要

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- バリューチェーン分析

- COVID-19の業界への影響評価

第5章 市場力学

- 市場促進要因

- 市場成長を助ける技術的進歩の増加

- 市場抑制要因

- 高コストとデータセキュリティへの懸念

第6章 市場セグメンテーション

- 製品別

- スマートウォッチ

- ヘッドマウントディスプレイ

- スマートウェア

- 耳掛け型

- フィットネス・トラッカー

- 身体装着型カメラ

- 外骨格

- 医療機器

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 北米

第7章 競合情勢

- 企業プロファイル

- Ekso Bionics Holdings Inc.

- Cyberdyne Inc.

- Transcend Information Inc.

- GoPro Inc.

- Sensoria Inc.

- AIQ Smart Clothing Inc.

- Medtronic PLC

- Withings

- Huami Corporation

- Omron Healthcare Inc.

- Nuheara Limited

- Bragi GmbH

- Microsoft Corporation

- Sony Corporation

- Huawei Technologies Co. Ltd

- Fitbit Inc.

- Fossil Group Inc.

- Garmin Ltd

- Samsung Electronics Co. Ltd

- Apple Inc.

第8章 投資分析

第9章 市場の将来

The Smart Wearable Market size is estimated at USD 84.23 billion in 2024, and is expected to reach USD 205.10 billion by 2029, growing at a CAGR of 19.48% during the forecast period (2024-2029).

Research advancements have led to increased innovation in recent years and are instrumental in driving the demand for the wearable market. It also led to new product categories like smart fabrics and hearables, which incorporate high-end technology and design in daily living. Lately, the focus is to provide an aesthetic design to devices to attract customers.

Key Highlights

- Wearable technology, an emerging trend, integrates electronics into daily activities and addresses the changing lifestyles with the ability to wear on any body part. Factors such as the ability to connect to the internet and data exchange options between a network and a device are leading to the wearable technology trend.

- Wearables have gained significant traction owing to the boom in the fitness trend across consumers. According to Cisco Systems, connected wearable devices are expected to increase from 593 million in 2018 to 1,105 million this year. The smartwatch category is experiencing a rise, owing to additional features, like the brand that suits the everyday lifestyle. Strong brands, such as Apple and Fossil, are keeping the pricing consistent with the price bands of traditional watches to maintain their revenues. With Google's WearOS, many other premium watchmakers, such as TAG and Armani, have entered the segment.

- The rising penetration rates of urbanization in various parts of the world have driven the demand for advanced, aesthetically appealing products to better serve consumers' requirements, such as multiple features in one device and time schedules. Moreover, the vast millennial population across the globe was quick to adopt smartwatches, owing to the increased spending ability on their regular work hours tracking and luxury standards.

- Hearables are gaining traction with the increasing acceptance of smart assistants. Companies like Bragi, Google, Apple, Jabra, Samsung, and Sony have been actively contributing to the growth of this segment.

- The COVID-19 outbreak and the lockdown restrictions across the world have affected industrial activities around the globe. The electronics industry is hit severely with a significant influence on its supply chain and production facilities. Production reached a standstill in China and Taiwan during February and March, influencing various OEMs worldwide.

Smart Wearables Market Trends

Head-Mounted Displays is Expected to Drive the Market Demand

- A head-mounted display is a device with a small display optic in front of one (monocular HMD) or each eye (binocular HMD) and worn on the head or as part of a helmet. These are primarily used for various purposes, including gaming, aviation, engineering, and medicine. Heads-up displays do not block the user's vision but superimpose the image on the user's view of the real world. An emerging form of a heads-up display is a retinal display that projects a picture directly on the sensitive part of the retina. However, the image appears on a screen at the user's ideal viewing distance. Still, there is no actual screen in front of the user. It includes special optics, such as modified eyeglasses that reflect the image into the user's eye. Some Head-mounted displays have motion sensors to determine direction and movement or as the interface to an immersive virtual reality application.

- The display is an integral part of the HMDs and generally is categorized into Virtual Reality (VR) and Augmented Reality (AR) devices. AR devices have a transparent display and digital information superimposed onto real-life objects. These HMDs are known as Optical head-mounted displays or OHMDs. In a VR device, the display is not transparent, and only virtual information and images are present in front of the wearer's eyes.

- Based on the functionality, processing HMDs are further categorized into Slide-on HMD, Discrete HMD, and Integrated HMD. The Slide-on HMD is the most cost-effective and accessible form of VR and consists of a smartphone holder, lenses, and some primary input. A smartphone is placed into the slide-on HMD, and the entire device is played upon the user's eyes to create the VR experience. Thus, it utilizes the smartphone for display, processing, and rotational tracking. However, some use their own IMUs instead of relying on smartphones. For instance, Samsung Gear VR utilizes its built-in IMUs.

- Discrete HMDs have a display, lenses, rotational tracking, positional tracking, audio, and advanced input, aside from processing. Thus, it requires connections to personal computers for processing. It delivers the best VR experience but is less mobile than slide-on and integrated HMD. It is also known as Tethered HMD, and some of them are Oculus Rift, HTC Vive, PlayStation VR, etc.

- Integrated HMD is the most advanced and expensive HMD and OHMD. It is an independent computing device that delivers VR or AR experiences without external hardware, such as a PC or smartphone. It contains a display, processors, and a camera and can display stereoscopic 3D images, perform complex tracking, and utilize advanced input methods. Currently, most integrated HMDs are AR OHMDs with high price points and target only business professionals. The most popular integrated HMD are Microsoft HoloLens, Google Glass, Magic Leap, etc.

Asia-Pacific to Witness the Fastest Growth Rate

- The Asia-Pacific region is expected to witness the highest growth in the smart wearable market during the forecast period. The growing electronics industry and a rapid rise in disposable income in the region are driving the smart wearable market.

- In China, the wearables market had taken a different shape, fuelled partly by the purchases of growing affluent consumers. For instance, a recent report by a government think tank in China stated approximately 80% of the smart wearable devices in the world are manufactured in the southeastern Chinese port city and manufacturing hub. According to the China Center for Information Industry Development report, Shenzhen, the base camp of many Chinese tech giants, is the most extensive R&D (research and development) and production center for smart wearables.

- In March this year, According to the Indian Cellular and Electronics Association (ICEA), the PMP rationalized the inverted duty structure to produce smart wearables. After boosting local manufacturing of mobile phones and laptop/tablet computers, the Indian government launched a new Phased Manufacturing Programme(PMP) to create wrist wearable gadgets, hearable devices, and electronic smart meters.

- Moreover, increasing awareness regarding fitness, technological advancements, and the availability of high-speed Internet connectivity are the major factors propelling smart wearable market growth in the country.

Smart Wearables Industry Overview

The smart wearable market is highly competitive and gained a competitive edge in recent years. Additionally, the players have gained a competitive advantage in this fast-growing market, mainly catering to the demand of the millennial generation population.

- September 2022 - U&i announced the launch of three premium wearables for an active lifestyle. In real-time, the smartwatch also features Sports Modes that can sense multiple body activities, such as walking, running, jogging, etc., to help users stay fit and active.

- May 2022 - Vuzix Corporation announced signing an agreement with Atomistic SAS (Atomistic), an mLED(micro-Light Emitting Diode) display solutions enterprise based in France. The agreement provides for the custom backplane design, an exclusive license of key mLEDtechnology, and the ability to acquire the enterprise, which depends upon achieving various technical phases. The Atomistic company will deliver a backplane on advanced node 300mm wafers, along with system-level support from Vuzix, intended to support upcoming mLEDs based upon its innovative material science and alternative LEDs from potential third-party suppliers. The mLEDswill be provided for AR glasses.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGTHS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Value Chain Analysis

- 4.4 Assessment of Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Incremental Technological Advancements Aiding the Market Growth

- 5.2 Market Restraints

- 5.2.1 High Cost and Data Security Concerns

6 MARKET SEGMENTATION

- 6.1 By Product

- 6.1.1 Smartwatches

- 6.1.2 Head-mounted Displays

- 6.1.3 Smart Clothing

- 6.1.4 Ear Worn

- 6.1.5 Fitness Trackers

- 6.1.6 Body-worn Camera

- 6.1.7 Exoskeleton

- 6.1.8 Medical Devices

- 6.2 By Geography

- 6.2.1 North America

- 6.2.1.1 United States

- 6.2.1.2 Canada

- 6.2.2 Europe

- 6.2.2.1 United Kingdom

- 6.2.2.2 Germany

- 6.2.2.3 France

- 6.2.2.4 Rest of Europe

- 6.2.3 Asia Pacific

- 6.2.3.1 China

- 6.2.3.2 Japan

- 6.2.3.3 India

- 6.2.3.4 South Korea

- 6.2.3.5 Rest of Asia Pacific

- 6.2.4 Latin America

- 6.2.5 Middle East and Africa

- 6.2.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Ekso Bionics Holdings Inc.

- 7.1.2 Cyberdyne Inc.

- 7.1.3 Transcend Information Inc.

- 7.1.4 GoPro Inc.

- 7.1.5 Sensoria Inc.

- 7.1.6 AIQ Smart Clothing Inc.

- 7.1.7 Medtronic PLC

- 7.1.8 Withings

- 7.1.9 Huami Corporation

- 7.1.10 Omron Healthcare Inc.

- 7.1.11 Nuheara Limited

- 7.1.12 Bragi GmbH

- 7.1.13 Microsoft Corporation

- 7.1.14 Sony Corporation

- 7.1.15 Huawei Technologies Co. Ltd

- 7.1.16 Fitbit Inc.

- 7.1.17 Fossil Group Inc.

- 7.1.18 Garmin Ltd

- 7.1.19 Samsung Electronics Co. Ltd

- 7.1.20 Apple Inc.