|

|

市場調査レポート

商品コード

1237850

茶の市場- 成長、動向、および予測(2023年-2028年)Tea Market - Growth, Trends, And Forecasts (2023 - 2028) |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| 茶の市場- 成長、動向、および予測(2023年-2028年) |

|

出版日: 2023年03月03日

発行: Mordor Intelligence

ページ情報: 英文 90 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

茶の市場は、予測期間中に4.5%のCAGRで推移すると予測されています。

COVID-19のパンデミックは、世界の茶の市場に直接的かつ不利な影響を及ぼしました。パンデミックの抑制と封じ込めのための世界の閉鎖は、流通チャネルに悪影響を及ぼしました。流通経路が寸断されたことにより、付加価値創造活動にも影響が及び、最終製品の市場での入手性が低下しました。茶業は、茶葉の栽培や加工に多くの労力を必要とする労働集約型産業です。品質の良い茶葉の収穫のピーク時期に合わせた積極的な封じ込めの発表が、品質の良い茶葉の生産に影響を及ぼしていました。

茶の市場は、紅茶部門が大きなシェアを占めているのが特徴です。しかし、緑茶やハーブ・フレーバーティーが健康に良いという認識から、最大の成長が見込まれています。中国が世界最大の茶生産国であり、インド、ケニア、スリランカなどがそれに続く。茶の生産は気候条件の変化に非常に敏感であり、茶は狭く定義された農業生態学的条件下でしか生産することができないからです。中国は世界の茶輸出の約31.8%を占め、第1位にランクされています。また、中国は緑茶の主要輸出国です。

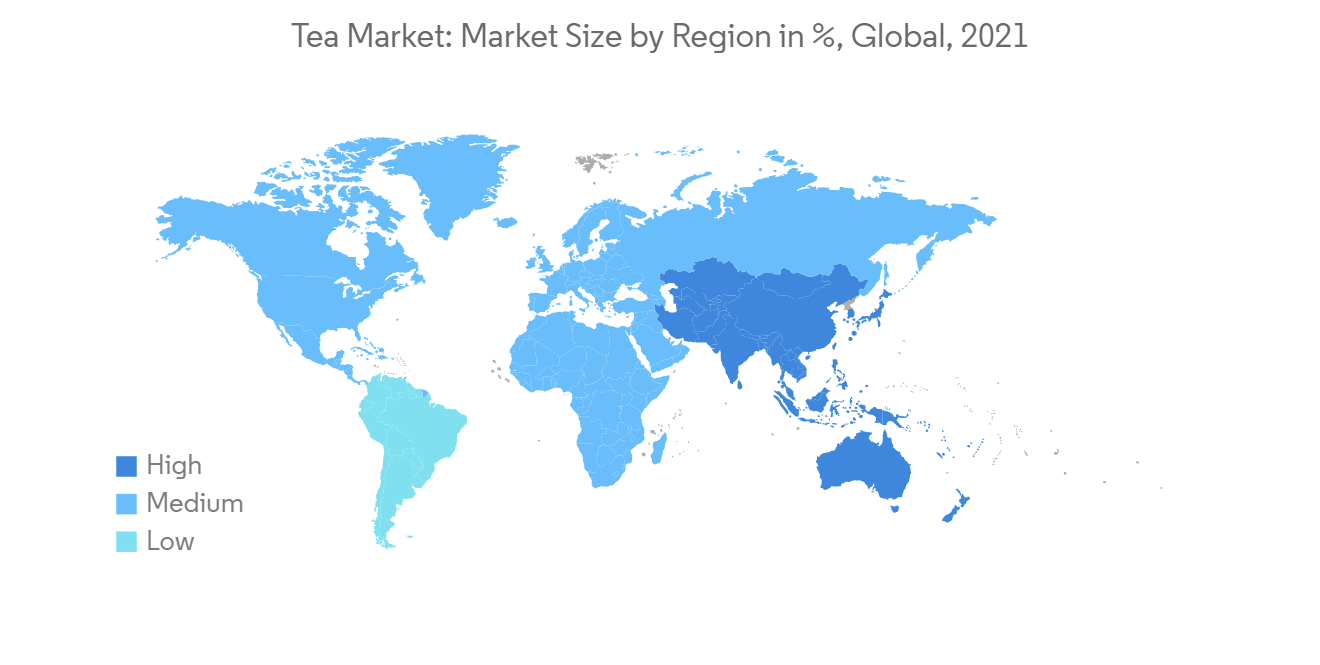

アジア太平洋は、今回の調査で最も大きな地域セグメントとなりました。各国の堅調な経済成長により、プレミアムブレンドティーを好む中産階級の消費者層が多くなっています。消費者は、包装されていない茶葉から、包装され袋詰めされた特殊な茶葉へと、購入の幅を広げています。さらに、炭酸飲料の消費は茶業界の新しい動向であり、これが茶の市場の成長をさらに後押ししています。また、ビゲロー社などの茶メーカー各社は、フルーティーなものからハーブの香りまで、さまざまなフレーバーの茶を発売しており、顧客向けに多様な茶製品のラインナップを用意しています。

茶の市場の動向

ハーブティーや緑茶への傾倒が進む

ハーブティーや緑茶の健康効果に関する消費者の意識は、茶の市場の成長をさらに促進する可能性があります。消費者の可処分所得の増加、味覚や嗜好の変化、さまざまな市場関係者による茶の健康成分の追加導入は、市場成長を促進するその他の要因です。茶の入手が容易であることは、アジア太平洋地域の緑茶の市場の成長を促すと予想されます。世界の緑茶生産量は、中国の成長を反映して、紅茶よりも速い速度で成長すると予想されます。また、ミレニアル世代は茶の消費量を増やしており、茶の学校やティーアートのトレーニングの推進、茶の博覧会や茶のイベントの開催が各地で行われ、ミレニアル世代の主力商品となっていることに牽引されています。このような世界の消費拡大に伴い、中国の緑茶の輸出は堅調な伸びを記録しています。ITCトレードによると、中国の3kg以下のパッケージの緑茶の輸出額は、2017年の6億4,850万米ドルに対し、2020年には約7億3,410万米ドルと評価されています。したがって、世界中で需要が増加していることが、長年にわたって市場を牽引する可能性があります。

アジア太平洋が茶の市場をリードする

現在、茶の消費量の増加は、特にアジア太平洋の新興諸国における一人当たりの所得の急速な増加によってもたらされています。中間層に入る、ますます都市化する若い人口層は、より多くの消費と高級茶製品への支払いの準備が整っています。したがって、これらの変化は、より強く、より長い動向に発展する可能性を持っています。現在、アジア太平洋地域は、中国やインドなど多くの新興国が堅調な経済成長を遂げており、茶の消費量では最大の市場となっています。このため、高級茶のブレンドやブランドを好む中間層が多く、無包装茶からパック入りや袋入りの特殊な茶葉へと購入のグレードを上げることが多くなっています。

茶の市場の競合他社分析

その他の特典です。

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件条件と市場の定義

- 調査対象範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- バリューチェーン分析

- バリューチェーンの概要

- バリューチェーンにおける価格マークアップ

- バリューチェーンの課題・問題点

第5章 市場セグメンテーション

- タイプ

- ブラックティー

- グリーンティー

- スペシャルティー

- 発酵茶

- その他のタイプ

- 地域(生産量分析:数量、消費量分析:数量・金額、輸入量分析:数量・金額、輸出量分析:数量・金額、価格動向)

- 北米

- 米国

- カナダ

- 欧州

- ロシア

- ポーランド

- 英国

- ドイツ

- アイルランド

- アジア太平洋地域

- 中国

- インド

- カザフスタン

- スリランカ

- ベトナム

- 日本

- インドネシア

- 南米

- ブラジル

- アルゼンチン

- チリ

- 中東・アフリカ地域

- サウジアラビア

- アラブ首長国連邦

- ナイジェリア

- 南アフリカ

- ケニア

- トルコ

- 北米

第6章 市場機会と将来動向

第7章 COVID-19が市場に与える影響についての評価

The tea market is projected to register a CAGR of 4.5% during the forecast period.

The COVID-19 pandemic had a direct and unfavorable impact on the tea market globally. Global lockdowns to curb and contain the pandemic adversely affected the distribution channels. Value addition activities were affected due to disrupted distribution channels, which lowered the availability of end products in the market. The tea industry is a labor-intensive industry that has more labor involved in the process of growing and processing tea. The announcement of aggressive containments that coincided with the peak harvesting periods for quality tea leaves had affected the production of quality tea.

The tea market is characterized by the black tea segment holding a prominent share. However, the maximum growth is estimated for green and herbal/flavored tea due to the awareness of the health benefits associated with them. China is the largest producer of tea in the world, followed by India, Kenya, Sri Lanka, and others. Tea production is highly sensitive to changes in climatic conditions, as tea can only be produced in narrowly defined agro-ecological conditions. China ranks first in the global tea exports, representing approximately 31.8% of the global export of tea. China is also the leading green tea exporter.

Asia-Pacific was the largest geographic segment of the market studied. The robust economic growth in the countries has also created a large consumer base among middle-class groups with a preference for premium tea blends. Consumers are frequently enhancing their purchases from unpackaged tea to packed and bagged specialty varieties. Furthermore, the consumption of carbonated tea drinks is a new trend in the tea industry, which is further fuelling the growth of the tea market. Various tea manufacturing companies, such as Bigelow, have introduced several flavors of tea, ranging from fruity to herbal flavors, creating a diversified portfolio of tea products for customers.

Tea Market Trends

Increasing Inclination Toward Herbal and Green Tea

Consumer awareness about the health benefits of herbal and green tea may further drive the growth of the tea market. The rise in disposable income of consumers, changes in taste and preferences, and the introduction of additional healthy ingredients in tea by different market players are the other factors that fuel the market growth. The easy availability of tea is expected to encourage the growth of the Asia-Pacific green tea market. World green tea production is expected to grow at a faster rate than black tea, reflecting the growth in China. The millennials are also increasing their tea consumption, led by the promotion of tea schools and tea art training and the staging of tea expos and tea events all over the country, making it a flagship product among millennials. Owing to the increased consumption across the world, China's export of green tea has been recording steady growth. According to the ITC Trade, China's green tea export of packages lesser than or equal to 3 kg packing was valued at around USD 734.1 million in 2020 compared to USD 648.5 million in 2017. Hence, the increasing demand around the world may drive the market over the years.

Asia-Pacific is Leading the Tea Market

Currently, the growth in tea consumption is being driven by rapid growth in per capita incomes, particularly in the developing countries of Asia-Pacific. A growing, increasingly urban young population segment entering the middle class is prepared to consume more and pay for premium tea products. Therefore, these changes have the potential to develop into stronger and longer trends. At present, Asia-Pacific has the largest market for tea consumption, with robust economic growth in a number of developing countries, such as China and India. This has created a large middle-class group, with a preference for premium tea blends and brands, often upgrading their purchases from unpackaged tea to packed and bagged specialty varieties.

Tea Market Competitor Analysis

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Value Chain Analysis

- 4.4.1 Value Chain Overview

- 4.4.2 Price Markups in the Value Chain

- 4.4.3 Value Chain Issues and Challenges

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Black Tea

- 5.1.2 Green Tea

- 5.1.3 Specialty Teas

- 5.1.4 Fermented Tea

- 5.1.5 Other Types

- 5.2 Geography (Production Analysis in Volume, Consumption Analysis by Volume and Value, Import Analysis by Value and Volume, Export Analysis by Value and Volume, and Price Trend Analysis)

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.2 Europe

- 5.2.2.1 Russia

- 5.2.2.2 Poland

- 5.2.2.3 United Kingdom

- 5.2.2.4 Germany

- 5.2.2.5 Ireland

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Kazakhstan

- 5.2.3.4 Srilanka

- 5.2.3.5 Vietnam

- 5.2.3.6 Japan

- 5.2.3.7 Indonesia

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Chile

- 5.2.5 Middle-East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 United Arab Emirates

- 5.2.5.3 Nigeria

- 5.2.5.4 South Africa

- 5.2.5.5 Kenya

- 5.2.5.6 Turkey

- 5.2.1 North America