|

市場調査レポート

商品コード

1272669

アクリルエマルジョン市場- 成長、動向、予測(2023年-2028年)Acrylic Emulsions Market - Growth, Trends, and Forecasts (2023 - 2028) |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| アクリルエマルジョン市場- 成長、動向、予測(2023年-2028年) |

|

出版日: 2023年04月14日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

アクリルエマルジョン市場は、予測期間中に5%以上のCAGRで推移すると予想されています。

COVID-19は、すべての産業が製造プロセスを停止したため、市場にマイナスの影響を与えました。ロックダウン、社会的距離、貿易制裁により、世界のサプライチェーンネットワークに大規模な混乱が生じた。建設業界は、活動の停止により衰退を目の当たりにしました。しかし、2021年には状態が回復し、予測期間中に市場に利益をもたらすと期待されています。

主なハイライト

- 市場を牽引する主な要因は、水性塗料に対する需要の高まりです。これは、溶剤系塗料の投入コストが上昇していることに起因しています。

- しかし、コーティング用途におけるポリウレタンへの嗜好の高まりは、市場の成長を抑制すると予想されます。

- 建築・建設産業の成長と拡大、アクリルエマルジョン技術の利点に関する認識の高まりは、市場成長の機会として作用します。

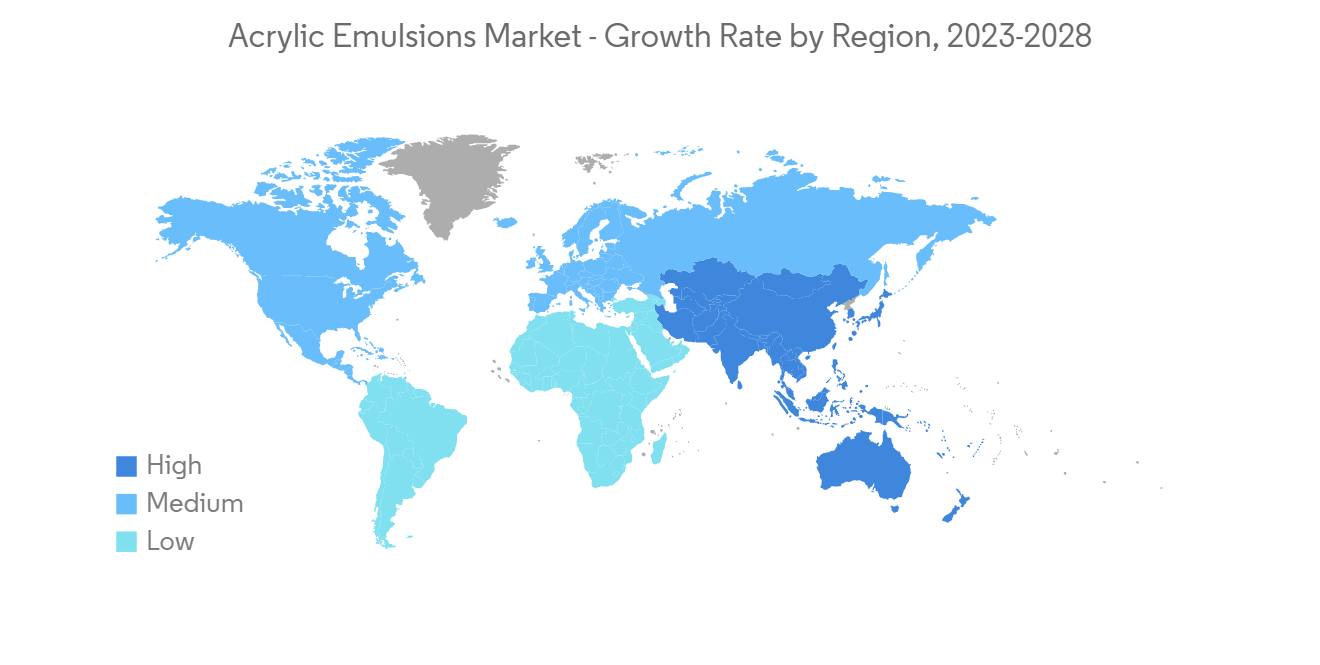

- アジア太平洋は、急速な都市化と工業化により、中国、日本、インドなどの国々からアクリルエマルジョンの大規模な需要につながるため、世界市場を独占すると予想されます。

アクリルエマルジョンの市場動向

塗料とコーティングの用途が市場を独占する

- アクリルポリマーエマルションは、耐紫外線性、伸びのバランス、耐水性、良好な粘着性など、さまざまな利点のために使用されています。

- アクリルエマルジョンの重要な用途の1つは、VOC排出量の少なさ、取り扱いの容易さ、水性層での高い性能などの要因から、建築用および工業用塗料の製造に使用されています。

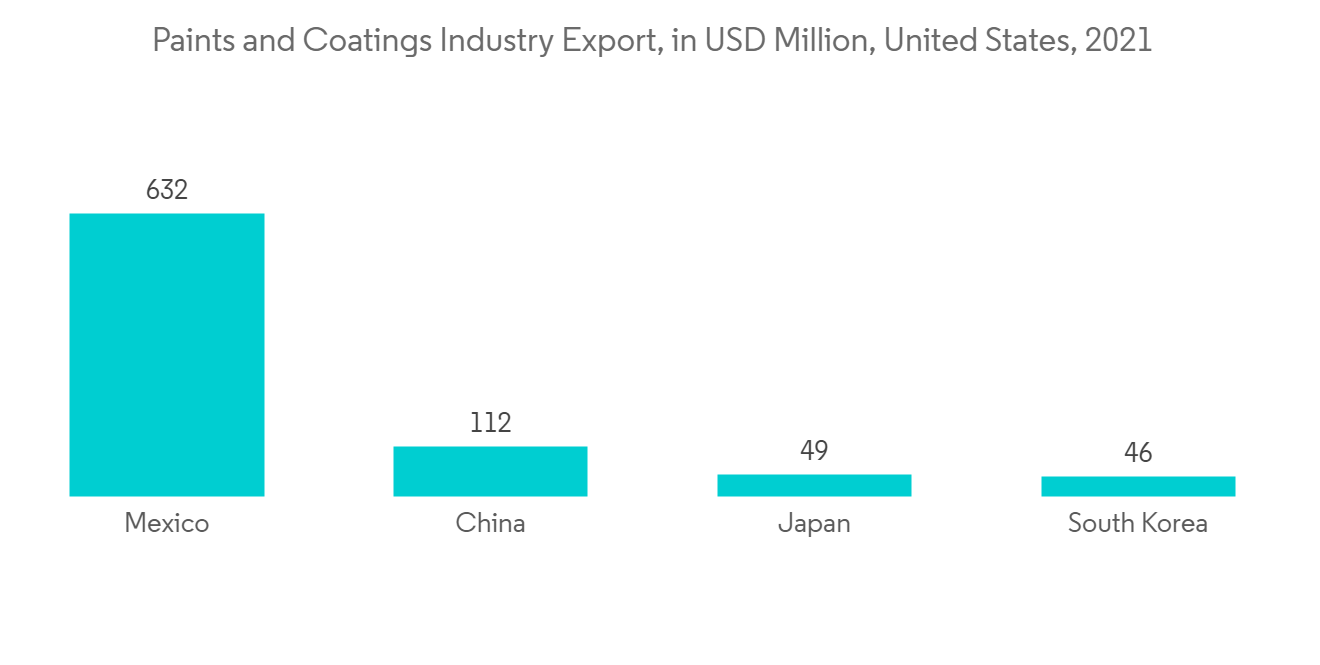

- American Coatings Associationによると、塗料とコーティングはポリマーエマルションの世界の需要をリードしており、2021年には150億米ドルを占めています。さらに、2027年には226億米ドルに達すると予測されています。2021年、米国は塗料・コーティング製品を25億米ドル輸出しています。

- アクリルエマルジョンは優れた粘着性と防水性を有しているため、建設業界において様々な用途に広く使用されています。米国国勢調査局によると、2021年12月、同国の建設支出は季節調整済み年率1兆6,399億米ドルと推定されました。2022年、米国では完成した公認民営住宅が1,664万7,000戸に達しました。

- 世界人口の増加により、住宅の消費が増え、塗料やコーティングに使用されるポリマーエマルジョンの需要が高まります。国連経済社会局によると、世界人口は2022年11月に80億人に達し、2030年には約85億人、2050年には約97億人、2100年には約104億人に増加すると推定されています。

- 水性塗料・コーティングは、高い耐久性、臭いの少なさ、VOC排出量の少なさなどから、近年採用が進んでいる塗料・コーティングです。住宅用塗料分野では、水性塗料が販売色数の約80%を占めています。

- したがって、予測期間中、塗料とコーティングの用途が引き続き市場を独占すると予想されます。

アジア太平洋地域が大きな伸びを示す

- 中国とインドにおける建築・建設需要の増加により、アジア太平洋地域が世界のアクリルエマルジョン市場を独占することになりました。

- インド、日本、シンガポール、マレーシアなどの国々では、急速な工業化が進み、建設や建築活動が活発化しているため、アジア太平洋地域は予測期間中、最も魅力的な市場になると予想されます。

- 例えば、インド政府は今後7年間で約1兆3,000億米ドルを住宅に投資する見込みです。同政府は6,000万戸の住宅を新たに建設し、アクリルエマルジョン市場を押し上げると思われます。

- 中国は、建設部門で大きな成長を遂げています。中国国家統計局によると、2021年、中国の建設生産高は約4兆2,900億米ドルと評価されました。

- 世界の建設活動の増加は、塗料やコーティングにおけるアクリルエマルジョンの需要に影響を与えます。中国は、2025年までに1兆4,300億米ドルを重要な建設プロジェクトに投資することを計画しています。国家発展改革委員会(NDRC)によると、上海の計画には今後3年間で387億米ドルの投資が含まれており、広州は80億9,000万米ドルを投資する16の新しいインフラプロジェクトに署名しました。

- 2022年、インドは、Housing to Allやスマートシティ計画など、インフラ整備や手頃な価格の住宅に関する政府の取り組みにより、建設業界に約6,400億米ドルを貢献しました。同国における建設活動の活発化は、塗料やコーティングの需要を促進し、それが予測期間中のアクリルエマルジョン市場を牽引する可能性があります。

- ASEAN諸国では、政府機関や民間企業による投資の増加により、商業および住宅建設産業が成長を遂げています。

- これらの要因から、アジア太平洋地域は予測期間中に大きな成長率を記録すると思われます。

アクリルエマルジョン産業の概要

アクリルエマルジョン市場は、少数の企業が大きな市場シェアを占めており、緩やかに統合されています。主なプレーヤーには、BASF SE、Dow.、Arkema Group、Celanese Corporation、DIC CORPORATIONが含まれます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 本調査の前提条件

- 本調査の対象範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 水性塗料への需要拡大

- アジア太平洋地域の建設業界への投資拡大

- 抑制要因

- コーティング用途におけるポリウレタン分散液の選好の高まり

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の度合い

第5章 市場セグメンテーション

- タイプ

- 純アクリルエマルジョン

- スチレンアクリルエマルジョン

- ビニルアクリルエマルジョン

- 用途

- 塗料・コーティング剤

- 建材用添加剤

- 紙用コーティング剤

- 粘着剤

- その他の用途

- 地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- ロシア

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米地域

- 中東・アフリカ地域

- サウジアラビア

- 南アフリカ

- その他中東とアフリカ

- アジア太平洋地域

第6章 競合情勢

- M&A、ジョイントベンチャー、コラボレーション、契約など

- 市場シェア(%)分析**/ランキング分析

- 主要企業が採用した戦略

- 企業プロファイル

- 3M

- Arkema Group

- BASF SE

- Celanese Corporation

- DIC Corporation

- Dow

- Gellner Industrial LLC

- Mallard Creek Polymers

- Pexi Chem Private Limited

- Royal DSM NV

- Synthomer plc

- The Cary Company

- The Lubrizol Corporation

第7章 市場機会および今後の動向

- アクリルエマルジョンの自己架橋技術の高度化

The market for acrylic emulsions is expected to register at a CAGR of over 5% during the forecast period.

COVID-19 negatively impacted the market as all the industries halted their manufacturing processes. Lockdowns, social distances, and trade sanctions triggered massive disruptions to global supply chain networks. The construction industry witnessed a decline due to the halt in activities. However, the condition recovered in 2021 is expected to benefit the market during the forecast period.

Key Highlights

- The major factors driving the market studied are the growing demand for water-based paints. It is due to the rising input costs for solvent-based paints.

- However, the growing preference for polyurethane in coating applications is expected to restrain the market growth.

- Growth and expansion of buildings and construction industry and increasing awareness about the benefits of acrylic emulsions technique act as opportunities for market growth.

- Asia-Pacific is expected to dominate the global market due to rapid urbanization and industrialization, leading to a massive demand for acrylic emulsions from countries such as China, Japan, and India.

Acrylic Emulsions Market Trends

Paints and Coatings Application to Dominate the Market

- Acrylic polymer emulsions are used for various benefits such as UV resistance, elongation balance, water resistance, good adhesion, and many others.

- One of the significant applications of acrylic emulsions is in making architectural and industrial coatings owing to factors like low VOC emissions, easy handling, and high performance in water-borne layers.

- According to the American Coatings Association, paints and coatings lead the worldwide demand for Polymer Emulsions, which accounted for USD 15 billion in 2021. It is further projected to reach USD 22.6 billion by 2027. In 2021, the United States exported USD 2.5 billion in paint and coatings products.

- Acrylic emulsion possesses excellent adhesive and waterproofing properties, so it is extensively used in the construction industry for various purposes. According to the US Census Bureau, in December 2021, construction spending in the country was estimated at a seasonally adjusted annual rate of USD 1,639.9 billion. In 2022, the completed authorized privately-owned housing units reached 16,647 thousand in the United States.

- The increasing global population increases the consumption of residential buildings, enhancing the demand for polymer emulsions to be used in paints and coatings. According to the United Nations Department of Economic and Social Affairs, the global population reached 8 billion in November 2022 and is estimated to grow to around 8.5 billion by 2030, 9.7 billion in 2050, and 10.4 billion in 2100.

- Water-based paints and coatings are recently adopted due to their high durability, less odor, and low VOC emissions. Water-based paints and coatings account for around 80% of total colors sold in the residential coatings sector.

- Hence, paints and coatings application is expected to continue dominating the market during the forecast period.

Asia-Pacific Region to Witness a Major Growth Rate

- Increasing demand for building and construction in China and India resulted in Asia-Pacific's domination over the global acrylic emulsions market.

- Due to fast industrialization and rising construction and building activities in nations including India, Japan, Singapore, & Malaysia, Asia-Pacific is expected to be the most appealing market over the projected timeframe.

- For instance, the Indian government will likely invest around USD 1.3 trillion in housing over the next seven years. The government will likely construct 60 million new homes, boosting the acrylic emulsions market.

- China is experiencing massive growth in its construction sector. According to the National Bureau of Statistics of China, in 2021, the construction output in China was valued at approximately USD 4.29 trillion.

- Increasing construction activities worldwide impact the demand for acrylic emulsions in paints and coatings. China planned to invest USD 1.43 trillion by 2025 in significant construction projects. According to National Development and Reform Commission (NDRC), the Shanghai plan includes an investment of USD 38.7 billion in the next three years, whereas Guangzhou signed 16 new infrastructure projects with an investment of USD 8.09 billion.

- In 2022, India contributed about USD 640 billion to the construction industry due to government initiatives in infrastructure development and affordable housing, such as housing to all, smart city plans, and others. The growing construction activities in the country are driving the demand for paint and coatings, which, in turn, may drive the acrylic emulsions market over the forecast period.

- The commercial and residential construction industries are witnessing growth in the ASEAN countries owing to the increasing investment by government and private organizations.

- Due to these factors, Asia-Pacific will likely witness a significant growth rate during the forecast period.

Acrylic Emulsions Industry Overview

The acrylic emulsions market is moderately consolidated, with a few players occupying a significant market share. Some key players include BASF SE, Dow., Arkema Group, Celanese Corporation, and DIC CORPORATION.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for Water-Based Paints

- 4.1.2 Growing Investment in Asia-Pacific Construction Industry

- 4.2 Restraints

- 4.2.1 Growing Preference for Polyurethane Dispersions in Coating Applications

- 4.3 Industry Value-Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Pure Acrylic Emulsions

- 5.1.2 Styrene Acrylic Emulsions

- 5.1.3 Vinyl Acrylic Emulsions

- 5.2 Application

- 5.2.1 Paints and Coatings

- 5.2.2 Construction Material Additives

- 5.2.3 Paper Coating

- 5.2.4 Adhesives

- 5.2.5 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Australia & New Zealand

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Russia

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East & Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East & Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Arkema Group

- 6.4.3 BASF SE

- 6.4.4 Celanese Corporation

- 6.4.5 DIC Corporation

- 6.4.6 Dow

- 6.4.7 Gellner Industrial LLC

- 6.4.8 Mallard Creek Polymers

- 6.4.9 Pexi Chem Private Limited

- 6.4.10 Royal DSM NV

- 6.4.11 Synthomer plc

- 6.4.12 The Cary Company

- 6.4.13 The Lubrizol Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Advancements in Self-crosslinking Technology of Acrylic Emulsion