|

市場調査レポート

商品コード

1403030

核医学イメージング:市場シェア分析、産業動向と統計、2024~2029年の成長予測Nuclear Imaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| 核医学イメージング:市場シェア分析、産業動向と統計、2024~2029年の成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 168 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

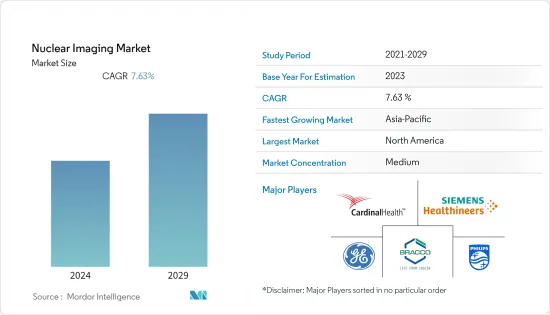

世界の核医学イメージング市場は、基準年に71億3,557万米ドルと評価され、予測期間終了時には109億7,618万米ドルに達すると予測され、CAGRは7.63%を記録します。

核医学イメージング市場は、パンデミックにより中程度の影響を受けました。原子炉の運転は、その重要性から、大部分が必須サービスに分類されています。そのため、原子炉は封鎖中も停止しなかった。例えば、南アフリカでは1995年労働法第66条第71項に基づき、2020年3月以降に同国で実施されたロックダウンの間、SAFARI-1原子炉は稼働し続けた。

しかし、2021年6月にSeminar in Nuclear Medicineに掲載された論文によると、米国疾病予防管理センター(CDC)が報告したCOVID-19感染者と死亡者の増加により、2020年3月と4月に核医学検査、心臓核医学イメージング、腫瘍学陽電子放射断層撮影/コンピュータ断層撮影の件数が減少しました。この研究ではさらに、COVID-19症例が減少したため、2020年6月から2021年2月にかけて手技が増加したと述べています。このように、COVID-19は、臨床研究の遅れ、様々な手術や画像処置の延期、遠隔画像診断の増加、スタッフに関するいくつかの制限など、核画像診断市場に若干の影響を与えています。しかし、ロックダウン規制が解除されて以来、業界は順調に回復しています。

過去2年間、慢性疾患の高い流行が市場の回復を牽引してきました。規制が緩和されたことで、画像診断のために病院を訪れる患者が増加したため、業界では診断と治療が大きく伸びた。これが今後数年間の市場成長を促進すると予想されます。

市場の成長を促進する要因としては、技術の進歩、がんや心血管疾患など様々な疾患における診断用途の増加、政府の支援、スタンドアロン型からハイブリッド型への移行などが挙げられます。例えば、Breast Cancer Factsheet Now 2021によると、英国では毎年約5万5,000人の女性と370人の男性が乳がんと診断されています。乳がんは英国で推定60万人の命を奪っています。この数字は、2030年までに120万人に達すると予想されています。さらに、心臓病の有病率の増加が市場の成長を促進すると予想されています。米国心臓協会(American Heart Association)の2021年ジャーナルによると、2035年までに米国では1億3,000万人以上の成人が何らかの心臓病を患うと推定されています。このように、がんや心疾患などの慢性疾患の有病率の増加は、早期かつ効果的な診断に対する需要を増加させ、予測期間中の核医学イメージング市場の成長を後押しすると予想されます。

画像診断分野における技術の進歩は、患者ケアにいかに最適化するかという点で、開業医にとって常に課題でした。過去数年の間に、科学者、研究者、技術者は、2つまたはそれ以上の独立した画像診断モダリティを組み合わせたシステムを臨床に持ち込むことができるようになった。こうしたマルチモダリティ画像診断システムには、PET/CT、SPECT/CT、PET/MRI、PET/SPECT/CTなどがあります。例えば、2022年10月、スペクトラム・力学社は、3600-CZTベースのワイドボアSPECT/CT構成で、固体検出器技術を使用して高エネルギー同位元素を画像化するデジタル核医学イメージング機能の最新開発を発表しました。この機能は新しいVERITON-CT 400シリーズデジタルSPECT/CTスキャナーで利用可能で、全身、脳、心臓、その他のイメージングアプリケーションを可能にします。核医学イメージングにおけるこのような進歩により、調査された市場は予測期間中に大きく成長すると予想されます。

主要企業は、合併、買収、提携、パートナーシップ、製品発売など、多くの戦略的取り組みを行っています。例えば、2021年1月、Koninklijke Philips NVとレンヌ大学病院は、PET診断、インターベンショナルイメージング、患者モニタリング、管理などをサポートする5年間のイノベーションと技術パートナーシップを締結しました。さらに、GE医療は2021年3月、英国でStarGuideを発売しました。この次世代SPECT/CTシステムは、最新のデジタル技術を駆使し、骨処置、心臓病学、神経学、腫瘍学、その他の専門分野において、臨床医が患者の予後を改善できるよう支援します。

慢性疾患の蔓延や核医学イメージング技術の進歩など、上記の要因から、予測期間中に同市場は成長すると予想されます。しかし、規制上の問題や償還不足が市場の成長を抑制する可能性があります。

核医学イメージング市場動向

予測期間中、PET用途ではがん領域が大きな市場シェアを占める見込み

放射性医薬品は近年、がんのイメージングに多用されています。2022年11月に発表されたREDECANレポートによると、乳がんはスペインの女性において最も頻度の高いがんであり、がんに関連した死亡の主要原因であり、2022年には3万4,750人の女性がこの病気と診断されると推定されています。さらに、同出典によると、2022年にスペインで新たに診断される肺がん患者は3万948人と推定されます。2022年には、男性2万2,316人、女性8,632人が肺がんと診断されると推定されています。このように、がんの有病率の増加と早期診断の必要性の増加が予測され、予測期間中の同分野の拡大を支えています。

腫瘍学では、PET(陽電子放射断層撮影法)は放射性医薬品としてFDG(18フッ素-2-フルオロ-2-デオキシ-d-グルコース)を使用し、正常細胞と比較して悪性細胞による代謝の増加を示します。この技術は、肺がん、リンパ腫、頭頸部腫瘍、乳がん、食道がん、大腸がん、尿路腫瘍などの画像診断に使用できます。さらに、核医学分野における研究開発の増加が市場の成長を後押しすると予想されています。例えば、Society of Nuclear Medicine and Molecular Imagingが2022年に発表したプレスリリースによると、Society of Nuclear Medicine and Molecular Imaging 2022 Annual Meetingで発表された新たな研究によると、新たに開発された低分子放射性医薬品ペアが前臨床試験でメラノーマの可視化と治療に成功しました。

さらに、新製品の上市が予測期間中の同分野の成長を後押しすると期待されています。2022年3月、米国食品医薬品局(FDA)はノバルティスの補完的画像診断薬Locametzを承認しました。Locametzは、ガリウム-68で放射性標識した後、前立腺特異的膜抗原(PSMA)陽性病変の同定に使用されます。FDAはまた、2022年3月にノバルティスのPluvictoを、前立腺特異的膜抗原陽性転移性去勢抵抗性前立腺がん(PSMA陽性mCRPC)と呼ばれる、体の他の部分に転移する特定のタイプの進行がんの成人患者の画像診断用に承認しました。さらに2022年2月、Monrol社はオランダのキュリウム社と、同社のGMP(Good Manufacturing Practice)グレードの医療用放射性同位元素であるキャリア無添加177Luと最先端の製造技術LuMagicのライセンス契約を締結しました。したがって、がん負担の増加や製品上市などの上記の要因により、この市場セグメントは予測期間中に成長を示すと予想されます。

北米が市場で大きなシェアを占めると予想され、予測期間中も同様と予想される

北米は、ハイブリッドイメージング、診断用の新しい放射性医薬品の導入、分子イメージングの開発などの技術の進歩により、市場で最大のシェアを占めると予測されます。

米国における医療セクターの堅調な成長、がん罹患率の増加、高齢者人口の増加、製品上市の増加が市場成長の要因となっています。カナダ政府が2021年11月に発表した統計によると、2021年には推定22万9,200人のカナダ人ががんと診断され、8万4,600人ががんで死亡しました。肺がん、乳がん、大腸がん、前立腺がんは引き続き最も多く診断されるがんで、2021年の診断全体の46%を占めると予想されています。調査によると、乳がんは女性の8人に1人が生涯のどこかで罹患します。がんの罹患数が増加するにつれて、早期発見への欲求も高まり、予測期間中、核医学イメージングに対する需要を促進します。同様に、CDCは2021年9月、米国の40歳以上の約650万人が2021年に末梢動脈疾患に罹患すると報告しました。このように、心血管疾患の負担が大きいことから、核医学画像診断のような効果的な診断に対する需要が高まり、予測期間にわたって同国の市場成長に拍車がかかると予想されます。

競合他社の存在、共同研究、研究イニシアチブは市場の成長を後押しします。例えば、カナダ原子力安全委員会(CNSC)は2021年、オンタリオ州クラリントン近郊にあるOntario Power Generation(OPG)のダーリントン原子力発電所の運転免許を改正し、同社がダーリントンのCANDU原子炉2号機を使用して医療用放射性同位元素モリブデン-99を生産することを許可しました。テクネチウム-99mの前駆体であるモリブデン-99(Mo-99)は、がんの検出や様々な病状を診断するために、年間4,000万件以上の手術に使用されています。放射性医薬品にTc-99mが使用されるようになったことで、カナダでは市場の飛躍的な成長が見込まれています。

北米地域では市場参入企業による発売が相次いでおり、核医学イメージングに対する需要の増加が見込まれています。例えば、Spectrum Dynamicsは2022年10月、CZTベースのワイドボアSPECT/CT構成で固体検出器技術を用いた高エネルギー同位元素の画像化機能という最新開発品を発表しました。この機能は新しいVERITRON-CT 400シリーズデジタルSPECT/CTスキャナーで利用可能であり、フルボディイメージング用途を可能にします。このように、がんや心疾患の有病率の増加や製品の発売といった上述の要因により、北米は予測期間中に調査した市場において大きな成長率を記録すると予想されます。

核医学イメージング産業概要

世界の核医学イメージング市場は競争が激しく、複数の大手企業で構成されています。市場シェアでは、現在数社の大手企業が市場を独占しています。Bracco Imaging SpA、Curium、Cardinal Health Inc.、Koninklijke Philips NV、General Electric Company(GE Healthcare)、Siemens Healthineersなどの企業がかなりのシェアを占めています。主要な市場参入企業は、新興地域や経済的に有利な地域でのM&Aを通じた地理的拡大、戦略的提携、パートナーシップを選択しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- がんと心疾患の有病率の上昇

- 技術進歩の増加

- 核医学と画像診断の用途拡大

- 市場抑制要因

- 規制上の問題

- 償還不足

- 業界の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(市場規模:金額)

- 製品別

- 装置

- ラジオアイソトープ

- SPECT放射性同位元素

- テクネチウム-99m(TC-99m)

- タリウム~201(TI~201)

- ガリウム(Ga-67)

- ヨウ素(I-123)

- その他のSPECT放射性同位元素

- PET放射性同位元素

- フッ素-18(F-18)

- ルビジウム-82(RB-82)

- その他のPET放射性同位元素

- 用途別

- SPECT用途

- 心臓病学

- 神経学

- 甲状腺

- その他のSPECT用途

- PET用途

- 腫瘍学

- 循環器内科

- 神経学

- その他のPET用途

- SPECT用途

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC諸国

- 南アフリカ

- その他の中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Bracco Imaging SpA

- Cardinal Health Inc.

- General Electric Company(GE Healthcare)

- Koninklijke Philips NV

- Siemens Healthineers

- Curium

- CMR Naviscan(Gamma Medica Inc.)

- Nordion(Canada)Inc.

- NTP Radioisotopes SOC

- Canon Medical Systems Corporation

第7章 市場機会と今後の動向

The global nuclear imaging market was valued at USD 7,135.57 million in the base year, and it is expected to reach USD 10,976.18 million by the end of the forecast period, registering a CAGR of 7.63%.

The nuclear imaging market was moderately impacted due to the pandemic. The operation of reactors has been largely classified as an essential service, given its criticality. Therefore, nuclear reactors were not shut down during the lockdown. For instance, under Section 71 of the Labour Act 66 of 1995 in South Africa, its SAFARI-1 reactor remained operational during the lockdown enforced in the country post-March 2020.

However, according to an article published in Seminar in Nuclear Medicine in June 2021, the number of nuclear studies, nuclear cardiac imaging, and oncology positron emission tomography/computed tomography decreased in March and April 2020 due to the rise of COVID-19 cases and deaths as reported by the Centers for Disease Control and Prevention (CDC). The study further stated that procedures increased from June 2020 to February 2021 as COVID-19 cases declined. Thus, COVID-19 has slightly impacted the nuclear imaging market with delays in clinical studies, postponement of various surgeries and imaging procedures, an increase in teleradiology, and several staff-related limitations. However, since the lockdown restrictions were lifted, the industry has been recovering well.

Over the last two years, the market recovery has been led by the high prevalence of chronic diseases. Patients' hospital visits for imaging diagnosis increased as the restrictions were relaxed, and so the industry saw a major surge in diagnostics and treatment. This is expected to promote the market's growth in the next few years.

Certain factors that are propelling the growth of the market include technological advancements, increasing diagnostic applications in various diseases, such as cancer and cardiovascular diseases, government support, and a shift from standalone to hybrid modalities. For instance, according to the Breast Cancer Factsheet Now 2021, around 55,000 women and 370 men in the United Kingdom are diagnosed with breast cancer every year. Breast cancer has claimed the lives of an estimated 600,000 people in the United Kingdom. This figure is expected to climb to 1.2 million by 2030. Moreover, the growing prevalence of heart diseases is expected to propel the growth of the market. As stated by the American Heart Association 2021 Journal, it is estimated that by 2035, more than 130 million adults in the United States will have some type of heart disease. Thus, the growing prevalence of chronic diseases such as cancer and cardiac diseases is expected to increase demand for early and effective diagnosis, thereby boosting the growth of the nuclear imaging market over the forecast period.

The technological advancements in the field of imaging have always been challenging to practitioners in terms of how best to optimize them in patient care. Over the past few years, scientists, researchers, and technologists have been able to bring systems into clinical practice in which two or even more standalone diagnostic imaging modalities are combined. Some of those multimodality imaging systems include PET/CT, SPECT/CT, PET/MRI, and PET/SPECT/CT. For instance, in October 2022, Spectrum Dynamics announced its newest development in digital nuclear medicine imaging capability to image high-energy isotopes using solid-state detector technology in a 3600-CZT-based, wide-bore SPECT/CT configuration. This functionality is available in the new VERITON-CT 400 Series Digital SPECT/CT scanners, enabling total body, brain, heart, and other imaging applications. With such advances in nuclear imaging, the market studied is expected to grow significantly over the forecast period.

The key players are working on many strategic initiatives such as mergers, acquisitions, collaborations, partnerships, and product launches. For instance, in January 2021, Koninklijke Philips NV and Rennes University Hospital signed a five-year innovation and technology partnership to support PET diagnostics, interventional imaging, patient monitoring, and management, among other things. Additionally, in March 2021, GE Healthcare launched StarGuide in the United Kingdom, a next-generation SPECT/CT system that uses the latest digital technologies to help clinicians improve patient outcomes in bone procedures, cardiology, neurology, oncology, and other specialties.

According to the factors mentioned above, such as the growing prevalence of chronic diseases and technological advances in nuclear imaging, the market studied is anticipated to witness growth over the forecast period. However, regulatory issues and a lack of reimbursement may restrain the market's growth.

Nuclear Imaging Market Trends

Oncology is Expected to Hold the Significant Market Share in PET Applications over the Forecast Period

Radiopharmaceuticals have been heavily used in the imaging of cancer in recent times. According to the REDECAN Report published in November 2022, breast cancer is the most frequent cancer and the primary cause of cancer-related death in women in Spain, with an estimated 34,750 women diagnosed with the disease in 2022. Additionally, as per the same source, there were estimated to be 30,948 new cases of lung cancer diagnosed in Spain in 2022. In 2022, 22,316 men and 8,632 women were estimated to be diagnosed with lung cancer. Thus, the growing prevalence of cancer and the need for early diagnostics are expected to increase, supporting the segment's expansion over the forecast period.

In oncology, PET (positron emission tomography) uses FDG (18 fluorine-2-fluoro-2-deoxy-d-glucose) as the radiopharmaceutical, as it demonstrates the increased metabolism by malignant cells when compared to that of normal cells. This technique can be used for the imaging of lung cancer, lymphoma, head and neck tumors, breast cancer, esophageal cancer, colorectal cancer, and urinary tract tumors. Furthermore, increased research and development in the field of nuclear medicine are anticipated to boost the market's growth. For instance, as per the press release published in 2022 by the Society of Nuclear Medicine and Molecular Imaging, according to new research presented at the Society of Nuclear Medicine and Molecular Imaging 2022 Annual Meeting, a newly developed small-molecular radiopharmaceutical pair has successfully visualized and treated melanoma in a preclinical study.

Furthermore, new product launches are expected to aid the growth of the segment during the forecast period. In March 2022, the United States Food and Drug Administration (FDA) approved Novartis' complementary diagnostic imaging agent, Locametz. Locametz, after radiolabeling with gallium-68, is used for the identification of prostate-specific membrane antigen (PSMA)-positive lesions. The FDA also approved Novartis's Pluvicto in March 2022 for the imaging of adult patients with a specific type of advanced cancer called prostate-specific membrane antigen-positive metastatic castration-resistant prostate cancer (PSMA-positive mCRPC) that will spread to other parts of the body. Additionally, in February 2022, Monrol signed an agreement with Curium Netherlands to license its good manufacturing practice (GMP)-grade medical radioisotope, no-carrier-added 177Lu, and cutting-edge production technology LuMagic. Hence, due to the factors mentioned above, such as the growing burden of cancer and product launches, this market segment is expected to witness growth over the forecast period.

North America is Expected to Hold a Significant Share in the Market and Expected to do the Same in the Forecast Period

North America is projected to account for the largest share of the market due to the advancements in technology, including hybrid imaging, the introduction of new radiopharmaceuticals for diagnosis, and the development of molecular imaging.

The robust growth of the healthcare sector in the United States, the increasing incidences of cancer, the growing geriatric population, and the increase in product launches account for the growth of the market. According to statistics published in November 2021 by the Government of Canada, an estimated 229,200 Canadians were diagnosed with cancer in 2021, and 84,600 died from it. Lung, breast, colorectal, and prostate cancers are expected to remain the most commonly diagnosed cancers, accounting for 46% of all diagnoses in 2021. According to the survey, breast cancer affects one out of every eight women at some point in their lives. As the number of incidences of cancer increases, the urge for early detection also rises, propelling demand for nuclear imaging over the forecast period. Similarly, the CDC reported in September 2021 that approximately 6.5 million people in the United States aged 40 and older had peripheral arterial disease in 2021. Thus, the high burden of cardiovascular diseases is expected to drive the demand for effective diagnoses such as nuclear imaging and fuel the growth of the market in the country over the forecast period.

The presence of competitors, collaborations, and research initiatives boost the market's growth. For instance, in 2021, the Canadian Nuclear Safety Commission (CNSC) amended Ontario Power Generation's (OPG) operating license for its Darlington nuclear power station near Clarington, Ontario, allowing the company to produce the medical radioisotope molybdenum-99 using Darlington's Unit 2 CANDU reactor. A precursor to technetium-99m, molybdenum-99 (Mo-99) is used in more than 40 million procedures a year to detect cancer and diagnose various medical conditions. With the use of Tc-99m in radiopharmaceuticals, the market is expected to grow at a tremendous rate in Canada.

The number of launches in the North American region by market players is expected to increase the demand for nuclear imaging. For instance, in October 2022, Spectrum Dynamics introduced its newest development, the capability to image high-energy isotopes using solid-state detector technology in a CZT-based, wide-bore SPECT/CT configuration. This functionality is available in the new VERITRON-CT 400 series digital SPECT/CT scanners, enabling full-body imaging applications. Thus, owing to the factors mentioned above, such as the growing prevalence of cancer and cardiac diseases coupled with product launches, North America is expected to register a significant growth rate for the market studied over the forecast period.

Nuclear Imaging Industry Overview

The global nuclear imaging market is highly competitive and consists of several major players. In terms of market share, a few of the major players currently dominate the market. Companies like Bracco Imaging SpA, Curium, Cardinal Health Inc., Koninklijke Philips NV, General Electric Company (GE Healthcare), and Siemens Healthineers hold a substantial share of the market. Leading market players are opting for geographic expansion, strategic collaborations, and partnerships through mergers and acquisitions in emerging and economically favorable regions.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise in Prevalence of Cancer and Cardiac Disorders

- 4.2.2 Increase in Technological Advancements

- 4.2.3 Growth in Applications of Nuclear Medicine and Imaging

- 4.3 Market Restraints

- 4.3.1 Regulatory Issues

- 4.3.2 Lack of Reimbursement

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD Million)

- 5.1 By Product

- 5.1.1 Equipment

- 5.1.2 Radioisotope

- 5.1.2.1 SPECT Radioisotopes

- 5.1.2.1.1 Technetium-99m (TC-99m)

- 5.1.2.1.2 Thallium-201 (TI-201)

- 5.1.2.1.3 Gallium (Ga-67)

- 5.1.2.1.4 Iodine (I-123)

- 5.1.2.1.5 Other SPECT Radioisotopes

- 5.1.2.2 PET Radioisotopes

- 5.1.2.2.1 Fluorine-18 (F-18)

- 5.1.2.2.2 Rubidium-82 (RB-82)

- 5.1.2.2.3 Other PET Radioisotopes

- 5.2 By Application

- 5.2.1 SPECT Applications

- 5.2.1.1 Cardiology

- 5.2.1.2 Neurology

- 5.2.1.3 Thyroid

- 5.2.1.4 Other SPECT Applications

- 5.2.2 PET Applications

- 5.2.2.1 Oncology

- 5.2.2.2 Cardiology

- 5.2.2.3 Neurology

- 5.2.2.4 Other PET Applications

- 5.2.1 SPECT Applications

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Bracco Imaging SpA

- 6.1.2 Cardinal Health Inc.

- 6.1.3 General Electric Company (GE Healthcare)

- 6.1.4 Koninklijke Philips NV

- 6.1.5 Siemens Healthineers

- 6.1.6 Curium

- 6.1.7 CMR Naviscan (Gamma Medica Inc.)

- 6.1.8 Nordion (Canada) Inc.

- 6.1.9 NTP Radioisotopes SOC

- 6.1.10 Canon Medical Systems Corporation