|

市場調査レポート

商品コード

1403981

胃がん治療:市場シェア分析、産業動向と統計、2024年~2029年の成長予測Gastric Cancer Therapy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| 胃がん治療:市場シェア分析、産業動向と統計、2024年~2029年の成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 112 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

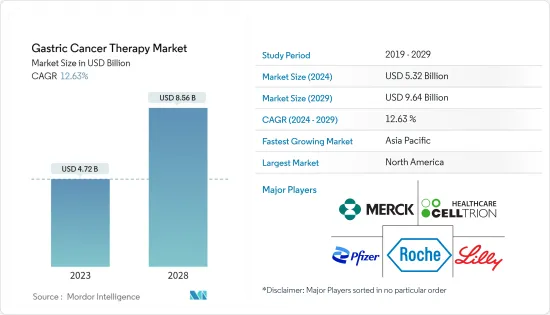

胃がん治療市場規模は2024年に53億2,000万米ドルと推定され、2029年には96億4,000万米ドルに達すると予測され、予測期間中(2024年~2029年)のCAGRは12.63%で成長すると予測されます。

主なハイライト

- COVID-19パンデミックは世界のヘルスケアシステムに影響を与え、胃がん治療市場に大きな影響を与えました。世界の封鎖により、胃がんの診断や治療が遅れたり中止されたりしました。例えば、2023年3月にPubMedに掲載された論文によると、パンデミックの最初の1年間、集学的チーム会議の頻度や選択的胃切除術の件数が減少し、胃がん患者の管理は世界的に影響を受けました。

- COVID-19パンデミックの間、診断と治療の遅れのために、がん患者は有害な転帰のリスクにさらされました。治療と診断の遅れの結果、パンデミックは市場の成長に大きな影響を与えました。しかし、胃がん治療の需要に関しては、現在、市場はパンデミック以前の状態に戻っています。

- この背景には、胃がん罹患率の上昇といくつかの技術的進歩があります。市場の成長を後押ししている要因としては、胃がん患者の増加、転移性がんに対する新規治療法のイントロダクション、主要企業による研究開発活動の活発化などが挙げられます。

- 例えば、Cancer Australia 2022の統計によると、2022年にはオーストラリアで新たに2,572例(男性1,661例、女性911例)の胃がんが診断されました。このように、胃がんの有病率が高いことから、胃がん治療薬に対する需要が増加し、市場成長に寄与すると期待されています。このように、人口の間で胃がんの負担が増加していることから、効果的な治療や療法に対する需要が高まり、市場成長に拍車がかかると予想されます。

- さらに、胃がん治療のための新薬や治療法の開発に注力する企業が増加していることや、製品上市が増加していることも、予測期間中の市場成長を後押しすると予想されます。例えば、2021年11月、ナトコファーマは、進行大腸がんおよび胃がんの治療に使用されるトリフルリジンとティピラシルの新規合剤を発売しました。

- 同様に、2022年2月、小野薬品工業とブリストル・マイヤーズスクイブ社は、オプジーボと化学療法を併用した胃がん患者を対象とした、業界主導の大規模多施設共同臨床研究について、プライムリサーチ・インスティテュート・フォー・メディカルRWD社と業務委託契約を締結しました。

- 本試験は、PRiME-R社が開発した、がん臨床における実データを標準化・構造化・管理・統合化するデータ入力支援システム「CyberOncology」を活用して実施されました。さらに、2022年4月には、BDRファーマシューティカルズが進行胃がん治療薬のジェネリック経口剤「フルメシル」を発売しました。このように、胃がんを治療するさまざまな薬剤の出現は、予測期間中の市場の成長に寄与すると予想されます。

- さらに、アステラス製薬は2023年6月、クローディン18.2(CLDN18.2)標的モノクローナル抗体ゾルベツキシマブについて、局所進行性切除不能または転移性のHER2陰性胃がんまたは胃食道接合部(GEJ)腺がんを適応症とする新薬承認申請を厚生労働省に行った。

- このように、胃疾患の増加や研究開発と結びついた戦略的活動により、調査市場は予測期間中に大きな成長を遂げると予想されます。しかし、がん治療の高額な費用と薬剤の副作用が、予測期間中の市場成長を抑制する可能性が高いです。

胃がん治療市場の動向

予測期間中、標的療法セグメントが市場で大きなシェアを占める見込み

- 標的療法は、がん細胞内に存在する特定の遺伝子やタンパク質を標的として薬剤が作用する、がんに用いられる治療法です。がんの標的治療には、ホルモン療法、遺伝子発現調節薬、アポトーシス誘導薬、血管新生阻害薬、シグナル伝達阻害薬など、いくつかの種類があります。胃がんの治療に使用される標的治療薬には、ラムシルマブ、ベバシズマブ、アパチニブ、スニチニブ、トラスツズマブ、ペルツズマブ、ラパチニブ、セツキシマブなどがあります。

- 胃がん有病率の増加、標的治療薬開発における企業活動の活発化、標的治療薬や治療法に関連する研究開発の活発化などの要因により、標的治療薬セグメントは予測期間中に大きな成長が見込まれています。

- 例えば、2022年7月にPubMedに掲載された論文によると、精密医療の開発は、胃がんにおける分子標的治療に関する国内外の研究において近年行われた目覚ましい進歩によって一貫して助けられてきました。したがって、胃がんにおける分子標的治療研究開発の増加は、予測期間中の市場成長を後押しすると予想されます。さらに、製品の上市や承認の増加は、セグメントの成長を増加させると予想されます。

- 例えば、2021年11月、独立行政法人医薬品医療機器総合機構(PMDA)は、メルク社のKEYTRUDAを、化学療法(5-フルオロウラシル[5-FU]+シスプラチン)との併用による根治切除不能な進行・再発食道がん患者に対する第一選択薬として承認しました。

- また、2021年4月、FDA(米国食品医薬品局)は、線維芽細胞増殖因子受容体2b(FGFR2b)過剰発現およびヒト上皮増殖因子受容体2(HER2)陰性の転移性および局所進行胃・胃食道(GEJ)腺がん患者に対する一次治療として、改良型FOLFOX6(フルオロピリミジン、ロイコボリン、オキサリプラチン)との併用療法です。

- したがって、胃がん症例の増加と主要企業による製品上市の増加が、予測期間中の同分野の市場成長を後押しすると予想されます。

予測期間中、北米が市場の主要シェアを占める見込み

北米は、胃がん有病率の増加、標的がん治療の採用増加、がん研究・治療センターにおける先端技術の利用可能性などの要因により、予測期間にわたって胃がん治療市場で大きなシェアを占めると予想されます。例えば、カナダがん協会による2021年5月の更新によると、2022年には4,100人のカナダ人が胃がんと診断されました。

また、米国がん協会の2023年の統計によると、米国では2023年に26,500例が胃がんと診断されると推定されています。このように、同地域における胃がん患者数の増加は、胃がん患者を治療するための効果的な治療法に対する需要を高め、ひいては予測期間中の市場成長を促進すると予想されます。

さらに、胃がん患者のための効果的な薬剤を開発するための臨床試験を実施する企業活動の高まりや、同地域における製品の上市と承認の増加は、市場の成長を促進すると予想されます。例えば、2021年4月、FDAはブリストル・マイヤーズスクイブ社のオプジーボをフルオロピリミジンおよびプラチナ含有化学療法との併用で、進行性または転移性の胃がん、胃食道接合部がん、食道腺がん患者の治療薬として承認しました。

同様に2021年1月、FDAはEnhertuを局所進行性または転移性のHER2陽性の胃または胃食道接合部(GEJ)腺がんの成人患者の治療薬として承認しました。同様に、オルガノン・カナダは2022年11月、基準生物学的製剤ハーセプチンのバイオシミラーであるオントルーサントを上市し、カナダの特定の乳がんおよび胃がん患者に、より低コストで追加の治療選択肢を提供しています。

したがって、胃がん患者の増加と主要企業による製品上市の増加は、北米地域の市場成長を後押しすると予想されます。

胃がん治療産業の概要

胃がん治療市場は適度な競争があり、少数の主要企業で構成されています。シェアの面では、現在数社の大手企業が市場を独占しています。市場の主要企業には、F. Hoffmann-La Roche Ltd、Bristol-Myers Squibb、Pfizer、Merck &Co.Inc.、Celltrion Inc.などです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 胃がん罹患率の増加

- 新規治療法の研究開発と政府のイニシアチブの増加

- 市場抑制要因

- がん治療の高コストと抗がん剤の副作用

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(市場規模)

- 治療タイプ別

- 化学療法

- 標的療法

- 免疫療法

- 放射線療法

- 外科療法

- エンドユーザー別

- 外来手術センター

- 病院・専門クリニック

- その他のエンドユーザー

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Bristol-Myers Squibb Company

- Celltrion Healthcare Co.,Ltd

- Eli Lilly and Company

- F. Hoffmann-La Roche Ltd

- GSK plc

- Imugene Limited

- Novartis AG

- Merck & Co. Inc.

- Otsuka Holdings Co. Ltd

- Pfizer Inc.

- Sanofi S.A

- Astrazeneca

- Amgen

第7章 市場機会と今後の動向

The Gastric Cancer Therapy Market size is estimated at USD 5.32 billion in 2024, and is expected to reach USD 9.64 billion by 2029, growing at a CAGR of 12.63% during the forecast period (2024-2029).

Key Highlights

- The COVID-19 pandemic affected healthcare systems globally and had a significant impact on the gastric cancer therapy market. Diagnosis and therapies for gastric cancer were delayed or canceled due to the global lockdown. For instance, as per the article published in March 2023 in PubMed, during the first year of the pandemic, the management of gastric cancer patients was globally affected by decreasing the frequency of multidisciplinary team meetings and the number of elective gastrectomies.

- During the COVID-19 pandemic, cancer patients were put at risk of adverse outcomes because of delays in diagnosis and treatment. As a result of the treatment and diagnosis delays, the pandemic had a substantial impact on market growth. However, the market has currently returned to its pre-pandemic state in relation to the demand for gastric cancer treatments.

- This is attributed to the elevated incidence of gastric cancer cases and several technological advancements. It is anticipated that the market will experience robust growth in the upcoming years.Certain factors that are propelling the market growth are the growing burden of gastric cancer and the introduction of novel therapies for metastatic cancer coupled with an increase in research and development activities by the key players.

- For instance, according to the Cancer Australia 2022 statistics, 2,572 new cases of stomach cancer were diagnosed in Australia (1,661 males and 911 females) in 2022. Thus, the high prevalence of stomach cancer is expected to increase the demand for gastric cancer therapies, thereby contributing to market growth. Thus, the rising burden of stomach cancer among the population is expected to raise the demand for effective treatment and therapies, which in turn is anticipated to fuel market growth.

- Furthermore, the rising company's focus on developing novel drugs and therapies for treating gastric cancer, coupled with increasing product launches, are all expected to boost the market growth over the forecast period. For instance, in November 2021, Natco Pharma launched a novel fixed-dose combination of Trifluridine and Tipiracil used to treat advanced colorectal and gastric cancer.

- Similarly, in February 2022, Ono Pharmaceutical Co., Ltd. and Bristol-Myers Squibb signed an outsourcing agreement with Prime Research Institute for Medical RWD, Inc. on an industry-sponsored, large-scale, multi-institutional clinical research in patients with gastric cancer treated with Opdivo in combination with chemotherapy.

- The study was conducted utilizing the PRiME-R's data input support system 'CyberOncology' which standardizes, structures, manages, and integrates real-world data in daily cancer clinical practice. Furthermore, in April 2022, BDR Pharmaceuticals launched Furmecil, a generic oral drug for the treatment of advanced gastric cancer. Thus, the emergence of various drugs to treat gastric cancer is expected to contribute to the growth of the market over the forecast period.

- Furthermore, in June 2023, Astellas Pharma submitted a New Drug Application (NDA) to Japan's Ministry of Health, Labour and Welfare (MHLW) for zolbetuximab, an investigational Claudin 18.2 (CLDN18.2)-targeted monoclonal antibody, indicated for the treatment of patients with locally advanced unresectable or metastatic HER2-negative gastric or gastroesophageal junction (GEJ) adenocarcinoma.

- Thus, due to the rise in gastric diseases and strategic activities coupled with research and development, the studied market is expected to witness significant growth over the forecast period. However, the high cost of cancer therapy and the side effects of drugs are likely to restrain the market growth over the forecast period.

Gastric Cancer Therapy Market Trends

Targeted Segment is Expected to Hold a Significant Share of the Market Over the Forecast Period

- Targeted therapy is a treatment used for cancer in which the drugs work by targeting the specific genes or proteins that are present in the cancer cells. There are several types of targeted therapies for cancers, such as hormone therapies, gene expression modulators, apoptosis inducers, angiogenesis inhibitors, signal transduction inhibitors, and many other therapies. Some of the targeted therapy drugs that are used to treat gastric cancer are ramucirumab, Bevacizumab, apatinib, sunitinib, trastuzumab, pertuzumab, lapatinib, and cetuximab.

- The targeted segment is expected to witness significant growth over the forecast period owing to factors such as the rising prevalence of gastric cancer among the population, increasing company activities in developing targeted therapies, and growing research studies related to targeted drugs and therapies.

- For instance, according to the article published in July 2022 in PubMed, the development of precision medicine has been consistently aided by the impressive advancements made in recent years in both domestic and international research on molecular targeted therapy in gastric cancer. Thus, an increase in targeted therapy research and development in gastric cancer is expected to bolster market growth over the forecast period. Moreover, the rising product launches and approvals are expected to increase segment growth.

- For instance, in November 2021, the Japan Pharmaceuticals and Medical Devices Agency (PMDA) approved Merck's KEYTRUDA as the first-line treatment for patients with radically unresectable, advanced, or recurrent esophageal carcinoma in combination with chemotherapy (5-fluorouracil [5-FU] plus cisplatin).

- Also, in April 2021, the Food Drug Administration (FDA) granted breakthrough therapy designation for investigational bemarituzumab as first-line treatment for patients with fibroblast growth factor receptor 2b (FGFR2b) overexpressing and human epidermal growth factor receptor 2 (HER2)-negative metastatic and locally advanced gastric and gastroesophageal (GEJ) adenocarcinoma in combination with modified FOLFOX6 (fluoropyrimidine, leucovorin, and oxaliplatin).

- Hence, the increase in cases of gastric cancer and the rise in product launches by the key players are expected to bolster the segment market growth over the forecast period.

North America is Expected to Occupy a Major Share of the Market Over the Forecast Period

North America is expected to hold a significant share in the gastric cancer therapy market over the forecast period owing to the factors such as the increasing prevalence of gastric cancer, rising adoption of targeted cancer therapy, and the availability of advanced technology in cancer research and treatment centers. For instance, according to the May 2021 update by the Canadian Cancer Society, 4,100 Canadians were diagnosed with gastric cancer in 2022.

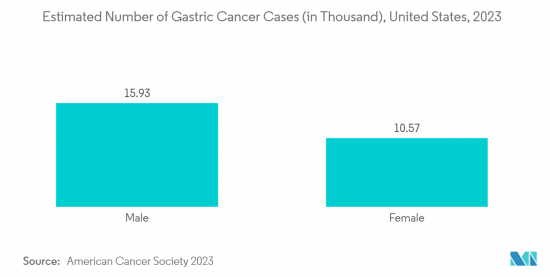

Also, according to the American Cancer Society 2023 statistics, 26,500 cases are estimated to be diagnosed with stomach cancer in 2023 in the United States. Thus, the increasing number of gastric cancer cases in the region is expected to rise the demand for effective therapies for treating patients with gastric cancer which in turn is anticipated to fuel the market growth over the forecast period.

Furthermore, the rising company activities in conducting clinical trials for developing effective drugs for patients suffering from gastric cancer and increasing product launches and approvals in the region, are expected to fuel the market growth. For instance, in April 2021, the FDA approved Bristol Myers Squibb's Opdivo in combination with fluoropyrimidine and platinum-containing chemotherapy, for the treatment of patients with advanced or metastatic gastric cancer, gastroesophageal junction cancer, and esophageal adenocarcinoma.

Similarly, in January 2021, the FDA approved Enhertu for the treatment of adult patients with locally advanced or metastatic HER2-positive gastric or gastroesophageal junction (GEJ) adenocarcinoma. Similarly, in November 2022, Organon Canada launched Ontruzant, a biosimilar of the reference biologic Herceptin, providing patients in Canada with certain breast and gastric cancers with an additional therapeutic option at a lower cost.

Therefore, the increase in cases of gastric cancer and the rise in product launches by the key players are expected to bolster the market growth in the North American region.

Gastric Cancer Therapy Industry Overview

The gastric cancer therapy market is moderately competitive and consists of a few major players. In terms of shares, a few of the major players are currently dominating the market. Some of the major players in the market are F. Hoffmann-La Roche Ltd, Bristol-Myers Squibb, Pfizer, Merck & Co. Inc., and Celltrion Inc., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Burden of Gastric Cancer

- 4.2.2 Increase in Research and Development for Novel Therapies Coupled with Government Initiatives

- 4.3 Market Restraints

- 4.3.1 High Cost of Cancer Therapy and Side Effects of Cancer Drugs

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value in USD)

- 5.1 By Therapy Type

- 5.1.1 Chemotherapy

- 5.1.2 Targeted Therapy

- 5.1.3 Immunotherapy

- 5.1.4 Radiation Therapy

- 5.1.5 Surgery

- 5.2 By End-User

- 5.2.1 Ambulatory Surgery Centers

- 5.2.2 Hospitals and Specialty Clinics

- 5.2.3 Other End-users

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Bristol-Myers Squibb Company

- 6.1.2 Celltrion Healthcare Co.,Ltd

- 6.1.3 Eli Lilly and Company

- 6.1.4 F. Hoffmann-La Roche Ltd

- 6.1.5 GSK plc

- 6.1.6 Imugene Limited

- 6.1.7 Novartis AG

- 6.1.8 Merck & Co. Inc.

- 6.1.9 Otsuka Holdings Co. Ltd

- 6.1.10 Pfizer Inc.

- 6.1.11 Sanofi S.A

- 6.1.12 Astrazeneca

- 6.1.13 Amgen