|

市場調査レポート

商品コード

1444620

通信クラウド:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Telecom Cloud - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| 通信クラウド:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

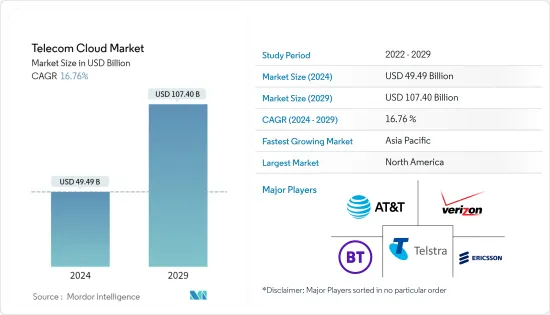

通信クラウド市場規模は2024年に494億9,000万米ドルと推定され、2029年までに1,074億米ドルに達すると予想されており、予測期間(2024年から2029年)中に16.76%のCAGRで成長します。

クラウドテクノロジーの最新動向により、通信組織はインターネットへの移行が可能になり、企業が世界のその他の地域との接続を維持するために高価なハードウェアを用意する必要がなくなりました。

主なハイライト

- クラウドネイティブテクノロジ、ネットワーク機能の仮想化、およびソフトウェアデファインドネットワークを組み合わせた分散コンピューティングネットワークは、「通信クラウド」として知られています。ネットワークとコンピューティングリソースは複数の場所とクラウドに分散しているため、自動化とオーケストレーションが重要です。この開発は、仮想化され、プログラム可能な、人工知能を備えたネットワークアーキテクチャの導入です。ネットワークアーキテクチャを変更する最先端のクラウドビジネス戦略を採用することももう1つの側面です。世界の通信クラウドの動向には、インターネットやモバイルデバイスの普及の増加、さまざまなビジネスの急速なデジタル変革などが含まれます。

- 情報通信技術の進歩は、世界のビジネス運営に著しい変化をもたらしています。さまざまな政府および公共企業は、重要な情報インフラストラクチャサービスに依存しています。また、企業は現在、ビジネス運営からの需要の高まりに応えるために、クラウドサービスにますます関心を示しています。

- オーバーザトップクラウドサービスに対する需要の増加、運用管理コストの削減、企業間の通信クラウドに対する意識の高まりにより、市場の成長が促進されると予想されます。

- 費用対効果が高く、ユーザーフレンドリーなブラウザベースの通信ソリューションに対する需要が高まる中、多くの著名なベンダーが北米での垂直特化型WebRTCソリューションやサービスの導入を検討しており、これにより市場の成長が促進されると予想されています。しかし、通信事業者に対するサイバー攻撃は、電話やインターネットの消費者へのサービスを妨害し、企業を麻痺させ、政府の業務を停止させる可能性があるため、サイバー脅威のリスクは市場の成長にとって大きな課題となっています。

- COVID-19感染症のパンデミックにより、通信業界は新しいテクノロジーとクラウドパターンに適応するための進歩の変革期を経験しています。在宅勤務する人が増えるにつれ、ホームスクーリングやビデオエンターテインメントのストリーミング用の教育リソースの入手が増加しています。これを踏まえると、通信業界では当然、音声、データ、ブロードバンドサービスの急増が見られます。

通信クラウド市場の動向

通信クラウド市場を独占すると予想されるソリューション

- ソリューション領域には、ネットワーク機能の仮想化、ユニファイドコミュニケーションとコラボレーション、コンテンツ配信ネットワークのオプションが含まれます。インターネットとモバイルデバイスの使用の増加により、ソリューションの受け入れが促進されています。その結果、組織は新しいテクノロジーをますます活用して、業務効率と組織の機敏性を向上させる必要があります。ビジネスで使用されるアプリケーションには、ボイスメール、電子メール、IM(インスタントメッセージング)、ユニファイドメッセージング、音声、Web、およびビデオ会議、ファイル共有、ホワイトボード、ソーシャルネットワーキングなどが含まれます。

- 市場で提供されるソリューションには、ユニファイドコミュニケーションとコラボレーション、コンテンツ配信ネットワーク、その他のソリューションが含まれます。これは主に、インターネットとモバイルデバイスの普及の増加によるものです。これに伴い、企業はビジネスの機敏性を向上させ、業務効率を高めるために高度なテクノロジーを活用する必要性をますます認識しています。

- 電話、電子メール、ボイスメール、ユニファイド・メッセージング、インスタント・メッセージング(IM)、プレゼンス、オーディオ、ウェブ、ビデオ会議、ファイル共有、ホワイトボード、モビリティ、ソーシャル・ネットワーキングなど、幅広いコミュニケーションおよびコラボレーション・アプリケーションを導入しています。

- さらに、メディアコンテンツが急激に増加し、オンラインユーザーの増加によるリッチビデオコンテンツへの需要が、エンドユーザーの業種全体にわたる組織間のデジタル化の傾向とともに、コンテンツ配信ネットワークソリューションの必要性を高めています。

北米が通信クラウド市場で主要シェアを握る

- 北米では、技術的熟練した従業員を抱える大企業が大幅に浸透し、継続的に革新的なテクノロジーを提供しています。米国とカナダでは、ハイブリッド通信クラウド設備の使用が増加しています。これにより、パブリッククラウド分野で利用可能なクラス最高のデータ分析と人工知能の統合が可能になり、消費者のニーズと好みを予測して満たすことができます。また、企業はクラウドを利用してサイロ化されたデータベースを排除し、顧客データを結合し、魅力的なオムニチャネルの顧客エクスペリエンスを提供し、顧客の360度のビューを開発します。

- ITの消費者化もこの地域の優位性の原因となっており、現在のモビリティブームとインテリジェントモバイルガジェットの開発に関連している可能性があります。さらに、いくつかの有名メーカーは、ユーザーフレンドリーで経済的なブラウザベースの通信ソリューションに対するニーズの高まりに応えて、業界固有のWebRTCソリューションとサービスを北米で提供する可能性を検討しています。これにより間接的に市場の成長が加速すると予想されます。

- さらに、この地域の優位性は、ITの消費者化による最近のモビリティの増加とスマートモバイルデバイスの爆発的な増加に起因していると考えられます。さらに、費用対効果が高く、ユーザーフレンドリーなブラウザベースの通信ソリューションに対する需要が高まっているため、多くの著名なベンダーが北米での垂直特化型WebRTCソリューションやサービスの導入を検討しており、間接的に市場の成長を促進すると期待されています。

- 最近、今年のMWCラスベガスでは、企業、クラウドおよびサービスプロバイダー、さらには家庭を対象とした幅広い最新の通信ソリューションが展示されました。ここでは、北米で最も重要な接続イベントで展示された5つの新鮮な商品とサービスを厳選して紹介します。

- COVID-19は新たな変曲点を生み出しており、各地域の通信プロバイダーは、継続的な健康、経済、社会の回復力、新しいエクスペリエンスと製品、構造的なコスト削減を構築するデジタル変革の基盤としてクラウドへの移行を劇的に加速する必要があります。そして社会的危機の要請。

通信クラウド業界の概要

主要なプレーヤーには、AT&T Inc.、BT Group PLC、Verizon Communications Inc.、Level 3 Communications Inc.、Telefonaktiebolaget LM Ericsson、Deutsche Telekom、およびNTT Communications Corporationが含まれます。これらの企業は、新しい技術や製品を開発して市場に導入するために、ますます合併・買収や製品の発売を行っています。したがって、市場の集中度は高くなります。

- 2022年 9月- ウインドリバーとデルテクノロジーズは、通信クラウドのインストールに革命を起こすために協力しました。市場初のウインドリバーと共同設計されたデルのソリューションは、オープンなクラウドネイティブネットワークテクノロジーの導入を加速するのに役立ちます。

- 2022年 5月-Nokiaがリリースを発表したクラウドネイティブのIMS Voice Core製品は、CSP(通信サービスプロバイダー)の運用の俊敏性の向上、ネットワーク運用の合理化、ネットワーク管理コストの削減を支援します。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 市場の定義と範囲

- 調査の前提条件

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界関係者の分析

- 業界の魅力- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場力学

- 市場促進要因

- 通信業界におけるハイブリッドクラウドの採用の増加

- 運用コストと管理コストの削減

- 市場の課題

- セキュリティ侵害のリスク

- 世界の通信クラウド市場におけるCOVID-19の影響

第6章 主要テクノロジーへの投資

- クラウドテクノロジー

- 人工知能

- サイバーセキュリティ

- デジタルサービス

第7章 市場セグメンテーション

- タイプ

- ソリューション

- ユニファイドコミュニケーションとコラボレーション

- コンテンツ配信ネットワーク

- その他のソリューション

- サービス

- コロケーションサービス

- ネットワークサービス

- プロフェッショナルサービス

- マネージドサービス

- その他のタイプ

- ソリューション

- 用途

- 請求とプロビジョニング

- 交通管理

- その他の用途

- クラウドプラットフォーム

- Software-as-a-Service

- Infrastructure-as-a-Service

- Platform-as-a-Service

- エンドユーザー

- BFSI

- 小売り

- 製造業

- 輸送と流通

- ヘルスケア

- 政府

- メディアとエンターテイメント

- その他のエンドユーザー

- 地域

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他欧州

- アジア太平洋地域

- インド

- 中国

- 日本

- その他アジア太平洋地域

- 世界のその他の地域

- 北米

第8章 競合情勢

- 企業プロファイル

- AT&T Inc.

- BT Group PLC

- Verizon Communications Inc.

- Telstra Corporation Ltd

- Telefonaktiebolaget LM Ericsson

- Deutsche Telekom

- NTT Communications Corporation

- CenturyLink Inc

- Singapore Telecommunications Limited

- China Telecommunications Corporation

- Telus Corporation

- Swisscom AG

第9章 投資分析

第10章 市場機会と将来の動向

The Telecom Cloud Market size is estimated at USD 49.49 billion in 2024, and is expected to reach USD 107.40 billion by 2029, growing at a CAGR of 16.76% during the forecast period (2024-2029).

The latest trend of cloud technology has enabled telecommunication organizations to migrate to the internet, where there is no longer the need to have costly hardware for businesses to stay connected to the rest of the world.

Key Highlights

- A distributed computing network that combines cloud-native technologies, network function virtualization and software-defined networking is known as the "telecommunication cloud." Since network and computing resources are dispersed across several locations and clouds, automation and orchestration are crucial. This development is the deployment of a virtualized, programmable, and artificially intelligent network architecture. Adopting cutting-edge cloud business tactics that modify network architecture is another aspect. Some global telecom cloud trends include rising internet and mobile device adoption and the quick digital transformation of various businesses.

- The advancements in information and communications technology have brought remarkable changes in global business operations. Various government and public enterprises are dependent on critical information infrastructure services. Also, organizations are now showing more interest in cloud services to meet the growing demand from business operations.

- The increasing demand for over-the-top cloud services, lower operational and administrative costs, and growing awareness about telecom cloud among enterprises are expected to boost the market's growth.

- With the rising demand for cost-effective and user-friendly browser-based communication solutions, many notable vendors are looking to introduce vertical-specific WebRTC solutions and services in North America, which is expected to boost the market's growth. However, the risk of cyber threats poses a significant challenge to market growth, as cyber attacks on telecommunication operators can disrupt services for phone and internet consumers, cripple businesses, and shut down government operations.

- Due to the Covid-19 pandemic, the telecom industry is experiencing a transformational period of advancement to adjust to new technologies and cloud patterns. With an increasing number of people working from home, obtaining educational resources for homeschooling and streaming video entertainment is rising. Given this, the telco industry is naturally seeing spikes in voice, data, and broadband services.

Telecom Cloud Market Trends

Solution Expected To Dominate the Telecom Cloud Market

- The solution area includes options for network function virtualization, unified communication and collaboration, and content delivery networks. The growing use of the internet and mobile devices is driving the acceptance of solutions. As a result, organizations need to leverage new technology more and more to improve operational efficiency and organizational agility. Applications used by businesses include voicemail, email, IM (instant messaging), unified messaging, audio, web, and video conferencing, file sharing, whiteboarding, social networking, and more.

- The solution offerings in the market include unified communication and collaboration, a content delivery network, and other solutions. This is majorly owing to the increasing internet and mobile device penetration. With this, businesses increasingly acknowledge the need to leverage advanced technologies to improve business agility and gain operational efficiencies.

- They are deploying a broad array of communications and collaboration applications, including telephone, email, voice mail, unified messaging, instant messaging (IM) and presence, audio, web, and video conferencing, file sharing and whiteboarding, mobility, social networking, and more.

- Additionally, the exponentially rising media content and demand for rich video content among the increasing online users, along with the trend of digitization among organizations across end-user verticals, spurs the need for content delivery network solutions.

North America Holds the Major Share in the Telecom Cloud Market

- North America witnessed a huge penetration from large enterprises with technically-skilled employees, providing continuous innovative technologies. In the U.S. and Canada, there is an increase in the use of hybrid telco cloud installations, which enables the integration of best-in-class data analytics and artificial intelligence available in the public cloud sector to anticipate and meet the needs and preferences of consumers. The businesses also use the cloud to get rid of silo databases, combine customer data, offer an engaging Omni channel customer experience, and develop a 360-degree view of the customer.

- The consumerization of IT, which is also to blame for this region's dominance, may be linked to the current boom in mobility and the development of intelligent mobile gadgets. In addition, several well-known manufacturers are looking into the possibilities of providing industry-specific WebRTC solutions and services in North America in response to the growing need for browser-based communication solutions that are user-friendly and economical. Indirectly, this is anticipated to accelerate market growth.

- Further, the dominance of this region can be attributed to the recent increase in mobility and the explosion of smart mobile devices due to the consumerization of IT. Moreover, with the rising demand for cost-effective and user-friendly browser-based communication solutions, many notable vendors are looking to introduce vertical-specific WebRTC solutions and services in North America, which is indirectly expected to boost the market's growth.

- Recently, A wide range of brand-new telecommunications solutions aimed at businesses, cloud and service providers, and even homes were displayed at MWC Las Vegas this year. Here is a selection of five fresh goods and services displayed at North America's most important connectivity event.

- COVID-19 has created a new inflection point that requires every regional telecom provider to dramatically accelerate the move to the cloud as a foundation for digital transformation to build the resilience, new experiences and products, and structural cost reduction that the ongoing health, economic, and societal crisis demands.

Telecom Cloud Industry Overview

The major players include AT&T Inc., BT Group PLC, Verizon Communications Inc., Level 3 Communications Inc., Telefonaktiebolaget L.M. Ericsson, Deutsche Telekom, and NTT Communications Corporation. These players are increasingly undertaking mergers and acquisitions and product launches to develop and introduce new technologies and products in the market. Hence, the market concentration will be high.

- September 2022 - Wind River and Dell Technologies have cooperated to revolutionize telecom cloud installations. The market-first co-engineered Dell solution with Wind River will aid in accelerating the adoption of open, cloud-native network technologies.

- May 2022 - The cloud-native IMS Voice Core product, which Nokia announced the release, will aid CSPs (Communication Service Providers) in enhancing operational agility, streamlining network operations, and lowering the cost of managing their networks.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Market Definition and Scope

- 1.2 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Stakeholder Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Adoption of Hybrid Cloud in Telecom

- 5.1.2 Lower Operational and Administration Costs

- 5.2 Market Challenges

- 5.2.1 Risk of Security Breaches

- 5.3 Impact of Covid-19 in Global Telecom Cloud Market

6 KEY TECHNOLOGY INVESTMENTS

- 6.1 Cloud Technology

- 6.2 Artificial Intelligence

- 6.3 Cyber Security

- 6.4 Digital Services

7 MARKET SEGMENTATION

- 7.1 Type

- 7.1.1 Solution

- 7.1.1.1 Unified Communication and Collaboration

- 7.1.1.2 Content Delivery Network

- 7.1.1.3 Other Solutions

- 7.1.2 Service

- 7.1.2.1 Colocation Services

- 7.1.2.2 Network Services

- 7.1.2.3 Professional Services

- 7.1.2.4 Managed Services

- 7.1.3 Other Types

- 7.1.1 Solution

- 7.2 Application

- 7.2.1 Billing and Provisioning

- 7.2.2 Traffic Management

- 7.2.3 Other Applications

- 7.3 Cloud Platform

- 7.3.1 Software-as-a-Service

- 7.3.2 Infrastructure-as-a-Service

- 7.3.3 Platform-as-a-Service

- 7.4 End User

- 7.4.1 BFSI

- 7.4.2 Retail

- 7.4.3 Manufacturing

- 7.4.4 Transportation and Distribution

- 7.4.5 Healthcare

- 7.4.6 Government

- 7.4.7 Media and Entertainment

- 7.4.8 Other End Users

- 7.5 Geography

- 7.5.1 North America

- 7.5.1.1 US

- 7.5.1.2 Canada

- 7.5.2 Europe

- 7.5.2.1 Germany

- 7.5.2.2 UK

- 7.5.2.3 France

- 7.5.2.4 Italy

- 7.5.2.5 Rest of Europe

- 7.5.3 Asia Pacific

- 7.5.3.1 India

- 7.5.3.2 China

- 7.5.3.3 Japan

- 7.5.3.4 Rest of Asia-Pacific

- 7.5.4 Rest of the World

- 7.5.1 North America

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 AT&T Inc.

- 8.1.2 BT Group PLC

- 8.1.3 Verizon Communications Inc.

- 8.1.4 Telstra Corporation Ltd

- 8.1.5 Telefonaktiebolaget LM Ericsson

- 8.1.6 Deutsche Telekom

- 8.1.7 NTT Communications Corporation

- 8.1.8 CenturyLink Inc

- 8.1.9 Singapore Telecommunications Limited

- 8.1.10 China Telecommunications Corporation

- 8.1.11 Telus Corporation

- 8.1.12 Swisscom AG