|

市場調査レポート

商品コード

1432784

アダプティブセキュリティ:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)Adaptive Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| アダプティブセキュリティ:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

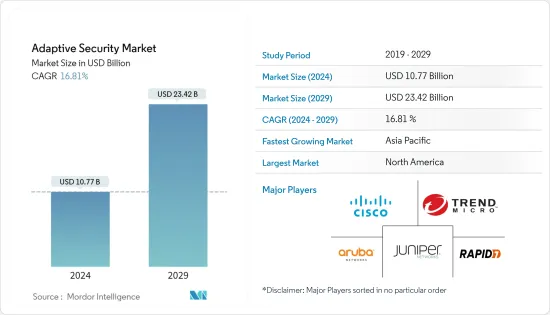

アダプティブセキュリティ市場規模は、2024年に107億7,000万米ドルと推定され、2029年には234億2,000万米ドルに達すると予測され、予測期間(2024-2029年)のCAGRは16.81%で成長すると予測されます。

企業のデータ、ネットワーク、アプリケーションを安全に保護するため、企業は未検出のリスクを追跡する予防措置をますます利用するようになっています。

主なハイライト

- アダプティブセキュリティ市場の拡大を促す主な要因は、企業が高度持続的脅威(APT)、ゼロデイ・マルウェア、その他の標的型攻撃などの高度な脅威から継続的に攻撃を受けていることです。現在の攻撃は、組織の従来の防御の欠陥を突こうとするダイナミックかつ協調的なものです。サイバー犯罪者は、企業の情報技術(IT)インフラを侵害し、ビジネスクリティカルな情報にアクセスすることで、損害を与え、莫大な財務的損失とデータ損失をもたらします。ますます巧妙化するサイバー攻撃から身を守るには、従来の防御を超えた備えが必要です。

- 多層的なセキュリティやスマート・ソリューションに対する需要の高まり、規制遵守に対する緊急の要求は、予測期間中の市場成長を促進すると予測されるいくつかの要因です。アダプティブセキュリティ市場は、特に組織におけるクラウドベースのセキュリティ・システムの利用拡大によって牽引されています。しかし、技術的スキルの不足や膨大なデータの処理に問題があるなどの要因により、世界のアダプティブセキュリティのニーズは限られています。

- さらに、クラウドベースのセキュリティ・ソリューションが受け入れられるようになれば、魅力的な市場開拓の可能性が生まれると思われます。アダプティブセキュリティ戦略は、組織の現在のセキュリティ・インフラを利用して強力なセキュリティ体制を構築しようとするものです。悪意のある攻撃からネットワーク、エンドポイント、データ、ユーザーを守るため、大企業や中小企業は、新たな脅威に適応できるセキュリティ・ソリューションの導入を試みています。企業は、必要のないセキュリティ・サービスにコストをかけたくありません。

- ビジネスにとって最も重要なリスクに優先順位をつけることで、将来そのような攻撃を防ぐ方法を学ぶことができます。アダプティブセキュリティの業界は、データの拡大や、より多くの有能な従業員に対する需要から、大きな障害に直面しています。こうした障害により、企業がアダプティブセキュリティ・ソリューションを導入することは難しくなっています。予測期間中、より熟練したサイバーセキュリティ専門家の必要性がアダプティブセキュリティ市場の成長を抑制すると予想されます。

- COVID-19の発生に伴い、ロックダウンや社会的距離を置く対策により、組織のほぼ大半が在宅勤務モデルに移行し、アプリケーションの管理やアプリケーションの側面からの遠隔監視に対する大きな需要が生まれました。アプリケーション・サービスのニーズに対する適応型セキュリティに対する組織の需要が高まった結果、適応型アプリケーション・セキュリティ・サービスを提供する企業の中には、サービス・パッケージの提供に戦略的に進出しているところもあります。

- 例えば、OpsRampは最近、ハイブリッドおよびマルチクラウドのIT環境を顧客が管理し、クラウドアプリケーション、ユニファイドコミュニケーション(UC)およびコラボレーションツール、ビデオ会議、その他のITリソースに対する需要が大幅に増加したため、ソリューションプロバイダーが在宅勤務従業員のニーズに対応できるように、OpsRampプラットフォームに新機能を追加して、WFHの世界に向けたネットワーク、UCモニタリングの幅を広げました。

- さらに、この流行を通じてサイバー攻撃やデータ漏えいが増加しました。VMwareのCybersecurity Threat Survey Reportによると、COVID-19が攻撃状況に与えた影響に関する調査を補足したもので、米国のサイバーセキュリティ専門家の88%が、在宅勤務者が増えるにつれて攻撃量が増加したと回答しています。さらに、89%が自社でCOVID-19マルウェアに関連したサイバー攻撃を受けたと報告しています。また、約89%がCOVID-19関連のマルウェアに狙われていると報告しています。

アダプティブセキュリティ市場の動向

クラウドが大きなシェアを占める

- クラウドセキュリティは、従来のプレミスベースのシステムよりも導入コストが低く、企業はコストと人員を節約できます。また、プロバイダーはデータを保護するための帯域幅、IT専門家、インフラを提供します。

- 俊敏性の向上、安価な資本コスト、合理化された運用(ソフトウェアからinfrastructure-as-a-serviceまで)により、企業によるクラウド・ソリューションとサービスの急速な採用は、同様にダイナミックなクラウド・プロテクションを必要としています。この新しい環境には、クラウドベースの適応型セキュリティが必要です。

- サイバー攻撃が複雑化するにつれて、クラウドプロバイダーから機密データを実行する際の遅延、遅延、危険性が危険にさらされています。

- その結果、企業は、オンプレミス・ソリューションがネットワーク保護を定期的に自動更新して保護し、クラウドを活用してさまざまな攻撃に対する第二の防御層を提供するハイブリッド・ソリューションの導入を検討しています。

北米が大きなシェアを占める

- 北米は、サイバーセキュリティ活動に関して最も積極的で熱心な地域です。主要国のGCI(世界・サイバーセキュリティ指数)のスコア(米国-100、カナダ-97.67)は、強力なサイバーセキュリティの枠組み構築へのコミットメントを再確認しています。

- しかし、重要な企業やデータセンターが存在するため、北米は最も影響を受けやすいと評価されています。米国国土安全保障省は、米国の重要インフラに属する60以上の組織が、500億米ドル以上の被害を受けたことを確認しました。

- この地域の中小企業(企業全体の約97%)は、セキュリティ・ソリューションの総所有コストを削減するために、クラウドの導入を好んでいます。その結果、セキュリティ・ソリューション・プロバイダーは、顧客のニーズを満たすソリューションを設計するチャンスを得ることになります。また、これらの企業の大半は、テクノロジーを活用し、効果的なエンドポイントセキュリティ対策を導入して、顧客体験を向上させるだろうと予測されています。

アダプティブセキュリティ業界の概要

アダプティブセキュリティ市場の競争は中程度です。同市場のプレーヤーは、市場でのプレゼンスと顧客基盤を拡大するために、戦略的ソリューションを提供する革新を進めています。これにより、新たな契約を獲得し、新たな市場を開拓することができます。

2023年3月、クラウドのリスクと脅威の検知企業であるRapid7は、侵入防止とランサムウェア保護技術のプロバイダーであるMinerva Labs, Ltd.の買収を発表しました。Rapid7のMDR(Managed Detection and Response)サービスは、クラウド、オンプレミス、拡張された攻撃サーフェスにおいて、より強化された検知・対応能力を顧客に提供します。今回の買収により、Rapid7の優れたマネージド脅威検知能力は、洗練されたランサムウェア保護を組織化する能力とともに拡張されます。これらの新機能により、企業はクラウドリソース、レガシーインフラ、現行のエンドポイントプロテクションアーキテクチャにMDRをシームレスに拡張することで、セキュリティ支出をさらに統合することができます。

2022年6月、ビジネス・ネットワーキングとセキュリティの企業であるシスコは、あらゆる規模や形態の企業を保護し接続する、クラウド配信の世界の統合プラットフォームの計画を発表しました。パブリッククラウドにロックインされることのないCisco Security Cloudは、ITエコシステム全体の整合性を維持し、市場で最もオープンなプラットフォームとなることを意図しています。

セキュリティクラウドは、あらゆる場所で人とデバイスをアプリケーションとデータに安全に接続するための統一されたエクスペリエンスを提供します。このオープンなプラットフォームは、統一された管理を通じて、脅威の予防、検知、対応、修復の機能を大規模に提供します。シスコは以前からセキュリティ・クラウドへの道を歩んでおり、現在、そのポートフォリオ全体で新たなセキュリティの進歩によるさらなる進展を共有しています。

2021年7月、セキュリティ分析と自動化のプロバイダーであるRapid7, Inc.は、完全に統合されたCloud-Native Security Platform(CNSP)であるInsightCloudSecのリリースを発表しました。複雑なクラウド環境に対する継続的なセキュリティとコンプライアンスにより、InsightCloudSecは企業のクラウドセキュリティプログラムの改善を可能にしました。Rapid7のInsight Platformの最新コンポーネントであるInsightCloudSecは、DivvyCloud(2020年5月に買収)、KubernetesセキュリティプロバイダーのAlcide(2021年1月に買収)、およびその他のクラウドセキュリティプロバイダーのクラウドセキュリティ態勢管理、インフラストラクチャエンタイトルメント管理、およびコードとしてのインフラストラクチャ機能を単一のシームレスなクラウドセキュリティソリューションに統合しました。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因と市場抑制要因のイントロダクション

- 市場促進要因

- 高度なサイバー攻撃からITリソースを保護する必要性

- セキュリティコンプライアンスと規制の必要性

- 市場抑制要因

- 熟練したサイバーセキュリティ専門家の不足

- 業界の魅力- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- アプリケーション

- アプリケーション・セキュリティ

- ネットワーク・セキュリティ

- エンドポイントセキュリティ

- クラウドセキュリティ

- サービス

- サービス

- ソリューション

- 導入モデル

- オンプレミス

- クラウド

- エンドユーザー

- BFSI

- 政府・防衛

- 製造業

- ヘルスケア

- エネルギー&公益事業

- IT &テレコム

- その他のエンドユーザー

- 地域

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第6章 競合情勢

- 企業プロファイル

- Cisco Systems Inc.

- Trend Micro Incorporated.

- Rapid7

- RSA Security LLC

- Juniper Networks, Inc.

- Fireeye Inc.(Trellix)

- Panda Security Inc.

- Illumio Inc.

- Cloudwick

- Aruba Networks Inc.(Hewlett Packard Enterprise Development LP)

第7章 投資分析

第8章 市場機会と今後の動向

The Adaptive Security Market size is estimated at USD 10.77 billion in 2024, and is expected to reach USD 23.42 billion by 2029, growing at a CAGR of 16.81% during the forecast period (2024-2029).

To secure businesses' data, networks, and applications, enterprises have increasingly used preventative measures to keep track of undetected risks.

Key Highlights

- The primary factor driving adaptive security market expansion is that enterprises are continually being attacked by sophisticated threats such as advanced persistent threats (APTs), zero-day malware, and other targeted assaults. These current assaults are dynamic and coordinated, intending to exploit flaws in an organization's traditional defenses. Cybercriminals can breach a company's information technology (IT) infrastructure and access business-critical information to inflict harm and enormous financial and data loss. Protecting against increasingly sophisticated cyberattacks, then, necessitates preparation that goes beyond traditional defenses.

- Growing demand for multilayer security and smart solutions, as well as the urgent requirement for regulatory compliance, are some factors predicted to fuel market growth during the forecast period. The adaptive security market is driven by the growing usage of cloud-based security systems, particularly in organizations. However, factors such as a lack of technical skills and problems processing vast volumes of data limit the need for global adaptive security.

- Furthermore, the rising acceptance of cloud-based security solutions will likely generate attractive market development possibilities. Adaptive security strategies attempt to use an organization's present security infrastructure to develop a strong security posture. To safeguard their networks, endpoints, data, and users from malicious assaults, large and small companies (SMBs) try to deploy security solutions that can adapt to emerging threats. Businesses do not want to spend money on security services that are not necessary.

- Prioritizing the risks most important to their business can help them learn how to prevent such assaults in the future. The industry of adaptive security faces substantial obstacles from the expanding data and the demand for more qualified employees. These barriers make it difficult for enterprises to implement adaptive security solutions. During the forecast period, the need for more seasoned cybersecurity experts is anticipated to restrain the growth of the Adaptive Security Market.

- With the outbreak of COVID-19, almost the majority of the organization shifted to the work-from-home model due to the lockdown ad social distancing measures that created a significant demand for managing the application and monitoring the application aspect remotely. As a result of the rising demand from organizations for adaptive security for their application services needs, some companies providing adaptive application security services are making strategic inroads into delivering a package of services.

- For example, OpsRamp recently expanded its network, UC monitoring for the WFH world with new functionality in the OpsRamp platform that allows solution providers to help customers manage hybrid and multi-cloud IT environments and meet the needs of work-from-home employees as demand for cloud applications, unified communications (UC) and collaboration tools, video conferencing, and other IT resources increased significantly.

- Furthermore, there was an increase in cyber-attacks and data breaches throughout the epidemic. According to VMware's Cybersecurity Threat Survey Report, supplemented with a survey on the impact COVID-19 had on the attack landscape, 88% of US cybersecurity professionals stated that as more workers work from home, attack volumes rose. Moreover, 89% reported cyberattacks tied to COVID-19 malware in their companies. Approximately 89% reported being targeted by COVID-19-related malware.

Adaptive Security Market Trends

Cloud to Hold Significant Share

- Cloud security is less expensive to install than traditional premise-based systems, and firms may save money and staff. The provider also supplies the bandwidth, IT professionals, and infrastructure to safeguard the data.

- Due to enhanced agility, cheaper capital costs, and streamlined operation (from software to infrastructure-as-a-service), businesses' rapid adoption of cloud solutions and services by enterprises need equally dynamic cloud protection. This new environment necessitates cloud-based adaptive security.

- The latency, delays, and hazards of running confidential data from a cloud provider are at risk as cyber assaults get more complicated.

- As a result, enterprises are looking to install a hybrid solution in which on-premise solutions automatically update and secure network protection regularly and utilize the cloud to give a second layer of defense against various assaults.

North America to Hold Major Share

- North America is the most active and committed area regarding cybersecurity activities. The main nations' GCI (global cybersecurity index) scores (United States of America - 100 and Canada - 97.67) reaffirm their commitment to constructing a strong cybersecurity framework.

- However, due to the existence of vital corporations and data centers, North America is rated the most susceptible. The US Department of Homeland Security identified more than 60 organizations in critical infrastructure in the United States that were damaged by a single event that cost over USD 50 billion.

- The region's SMEs (about 97% of total firms) favor cloud deployment to reduce the total cost of ownership of security solutions. As a consequence, security solution providers have a chance to design solutions that meet customer needs. It is also predicted that most of these players would use technology and deploy effective end-point security measures to improve the client experience.

Adaptive Security Industry Overview

The adaptive security market is moderately competitive. The players in the market are innovating in providing strategic solutions to increase their market presence and customer base. This enables them to secure new contracts and tap new markets.

In March 2023, Rapid7, a cloud risk and threat detection company, announced the acquisition of Minerva Labs, Ltd., a provider of anti-evasion and ransomware protection technologies. Rapid7's Managed Detection and Response (MDR) services now give clients enhanced detection and response capabilities across cloud, on-premise, and extended attack surfaces. Rapid7's superior managed threat detection capabilities will be expanded with the ability to organize sophisticated ransomware protection due to this purchase. These new capabilities will allow companies to further consolidate their security expenditures by seamlessly extending MDR across cloud resources, legacy infrastructure, and current endpoint protection architecture.

In June 2022, Cisco, the business networking and security company, announced plans for a worldwide, cloud-delivered, integrated platform that secures and connects enterprises of any size and shape. With no public cloud lock-in, the Cisco Security Cloud was intended to be the most open platform in the market, preserving the integrity of the whole IT ecosystem.

The Security Cloud offers a unified experience for securely connecting people and devices to apps and data everywhere. The open platform delivers threat prevention, detection, response, and remediation capabilities at scale through a unified administration. Cisco has been on the path to the Security Cloud for some time and is now sharing further progress with new security advancements throughout its portfolio.

In July 2021, Rapid7, Inc., a provider of security analytics and automation, announced the release of InsightCloudSec, the fully integrated Cloud-Native Security Platform (CNSP). With continuous security and compliance for complex cloud environments, InsightCloudSec enabled organizations to improve their cloud security programs. InsightCloudSec, the newest component of Rapid7's Insight Platform, combined the cloud security posture management, infrastructure entitlements management, and infrastructure as code capabilities of DivvyCloud (acquired in May 2020), Kubernetes security provider Alcide (acquired in January 2021), and other cloud security providers into a single seamless cloud security solution.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Introduction to Market Drivers and Restraints

- 4.3 Market Drivers

- 4.3.1 Need to Secure IT Resources from Advanced Cyberattacks

- 4.3.2 Need for Security Compliances and Regulations

- 4.4 Market Restraints

- 4.4.1 Lack of Skilled Cyber Security Professionals

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Application Security

- 5.1.2 Network Security

- 5.1.3 End Point Security

- 5.1.4 Cloud Security

- 5.2 Offering

- 5.2.1 Service

- 5.2.2 Solution

- 5.3 Deployment Model

- 5.3.1 On-premise

- 5.3.2 Cloud

- 5.4 End-User

- 5.4.1 BFSI

- 5.4.2 Government & Defense

- 5.4.3 Manufacturing

- 5.4.4 Healthcare

- 5.4.5 Energy & Utilities

- 5.4.6 IT & Telecom

- 5.4.7 Other End-Users

- 5.5 Geography

- 5.5.1 North America

- 5.5.2 Europe

- 5.5.3 Asia-Pacific

- 5.5.4 Latin America

- 5.5.5 Middle East & Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Cisco Systems Inc.

- 6.1.2 Trend Micro Incorporated.

- 6.1.3 Rapid7

- 6.1.4 RSA Security LLC

- 6.1.5 Juniper Networks, Inc.

- 6.1.6 Fireeye Inc. (Trellix)

- 6.1.7 Panda Security Inc.

- 6.1.8 Illumio Inc.

- 6.1.9 Cloudwick

- 6.1.10 Aruba Networks Inc.(Hewlett Packard Enterprise Development LP)