|

市場調査レポート

商品コード

1432589

クラウドストレージ:市場シェア分析、産業動向と統計、成長予測(2024年~2029年)Cloud Storage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| クラウドストレージ:市場シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

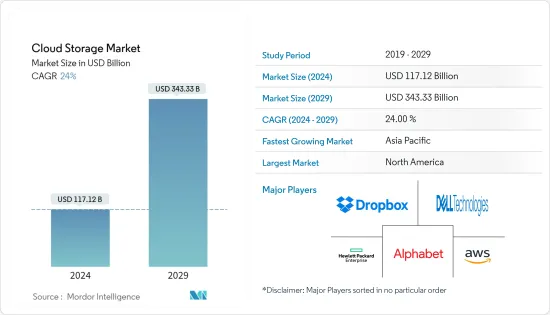

クラウドストレージ市場規模は2024年に1,171億2,000万米ドルと推計され、2029年には3,433億3,000万米ドルに達すると予測され、予測期間(2024~2029年)のCAGRは24%で成長する見込みです。

あらゆる企業において、低コストのデータバックアップ、ストレージ、保護に対する需要が高まっており、モバイル技術の利用拡大によって生成されたデータを処理する必要性も相まって、クラウドストレージの採用率が高まっています。

主なハイライト

- クラウド・ストレージ市場は、企業全体でデータ量が増加し、リモート・ワーカーにデータやファイルへのユビキタス・アクセスを提供する必要性が高まっていることから、成長が見込まれています。例えば、シーゲイト・テクノロジーズ・ホールディングスPLCによると、2020年から2022年にかけて、企業の総データ量は約1ペタバイト(PB)から2.02ペタバイトに増加する見込みです。これは2年間のCAGR42.2%に相当します。

- さらに、あらゆる企業で低コストのデータバックアップとデータ保護に対する需要が高まっていることに加え、モバイル技術の利用が増加することで発生するデータを処理する必要性が高まっていることも、クラウド・ストレージの採用に拍車をかけています。企業は定期的に運用コストを削減し、利益率を高める方法を見出しているが、これはサードパーティー・ベンダーによるマネージド・クラウド・サービスのアウトソーシングや採用によって実現できます。

- 戦略的パートナーシップ、M&A、研究開発を通じて、市場の有力企業の一部はクラウドストレージ技術をさらに発展させることができました。このことが、予測期間中のクラウドストレージ需要を促進する可能性があります。

- COVID-19が大流行する中、公衆衛生上の懸念から多くの国で在宅勤務が義務付けられ、リモートワーク・インフラの必要性が高まった。そのため、政府機関を含むあらゆるレベルの組織は、仮想サービスへの需要の増加と、これらのサービスの提供に関する市民の期待の高まり、政府労働力の再形成の長期的な可能性、適応的かつ動的な規制モデルの提供の必要性など、幅広い潜在的影響を予想しました。

クラウドストレージ市場の動向

BFSIが大きなシェアを占める見込み

- 収益創出を向上させるため、銀行は顧客インサイトを高め、コストを抑制し、市場に関連した商品を迅速かつ効率的に提供し、企業データ資産の収益化を支援します。銀行は、オンライン・ポータルを導入することで業務のデジタル化を開始し、ユーザーは銀行職員の介入を必要とせずに直接業務に取り組むことができます。その結果、データ生成量が大幅に増加し、こうした機関はクラウドストレージを採用するようになった。

- クラウド・ストレージ・ソリューションは、銀行が企業を同期化し、リスク、財務、規制、顧客サポートにまたがる業務とデータのサイロ化を解消し、膨大なデータセットを一箇所に集めて高度な分析と統合された洞察を可能にするため、世界中の銀行サービス・プロバイダーが採用しています。

- BFSIプレーヤーがクラウドに移行するのを支援するテクノロジー・ベンダーのイニシアティブも、このセグメントの成長を後押ししています。ファインダーによると、2021年には、デジタル専用銀行の英国からの顧客数は1,400万人を超え、今後数年間で1,000万人増加すると予想されています。これは、このような増加に対応するためにクラウドストレージのようなソリューションが必要になることを示しており、予測期間におけるクラウドストレージの成長を後押しします。

- 銀行セクターにおけるデータ漏えいの増加は、銀行がクラウドストレージを採用する原動力となっています。クラウドストレージは、銀行またはサードパーティが管理・所有するスペースにデータを保存することを可能にし、エンドユーザーに強化されたセキュリティを提供します。このため、予測期間中にクラウドストレージの導入が進むと予想されます。例えば、Identity Theft Resource Centerのデータによると、米国の金融サービスセクターにおけるデータ漏洩件数は、2020年の138件から2022年には268件に達しました。

北米が最大のシェアを占める見込み

- 北米は、新技術の早期導入、クラウドベースのソリューションの研究開発への莫大な投資、ITインフラの強化により、大きなシェアを占めると予測されています。さらに、安価で安全なストレージ・オプションが産業の急速な発展をもたらしています。

- 北米地域は、同市場におけるベンダーの足場が強固です。その中には、Google LLC、IBM Corporation、Microsoft Corporation、Oracle Corporation、Amazon Web Services Inc.などが含まれます。研究開発を通じて、同地域のこれらの有力企業は技術をさらに発展させることができました。これにより、予測期間を通じてクラウドストレージの導入が促進され、クラウドストレージのコストが削減されると期待されています。

- Stormforgeが2021年4月に発表したレポートによると、北米の回答者の18%は、自社の組織で毎月のクラウド支出が10万米ドルから25万米ドルの間であると回答しています。さらに、44%は今後1年間にクラウド支出が増加すると予想しており、さらに32%は今後1年間に組織のクラウド支出が大幅に増加すると予想しています。

- さらに、カナダ政府は「クラウドファースト」戦略を採用しており、情報技術への投資、イニシアティブ、戦略、プロジェクトを開始する際には、クラウドサービスが主要なデリバリーオプションとして特定され、見積もられます。また、クラウドを利用することで、政府は民間プロバイダーのイノベーションを活用し、情報技術をより俊敏なものにすることができます。このモデルはプライベート・クラウドのセキュリティとパブリック・クラウドの柔軟性を可能にするため、このような取り組みはハイブリッド・クラウド市場に多くの機会を提供すると予想されます。

クラウドストレージ業界の概要

クラウドストレージ市場は、マイクロソフト、IBM、オラクルなどの大手企業が大きなシェアを占めているため、適度に集中しています。各社の継続的なイノベーション能力により、他社に対する競争優位性を獲得しています。戦略的パートナーシップ、研究開発、M&Aを通じて、これらのプレーヤーは市場により大きな足跡を残しています。

- 2022年11月:Dell APEXポートフォリオの継続的な勢いの一環として、Dell Technologies Inc.は、Dell PowerFlexがAWSマーケットプレースで利用可能になったことを発表しました。この提供により、顧客はPowerFlexのミッションクリティカルなパフォーマンス、回復力、拡張性、管理を既存のクラウドクレジットを使用しながら利用できるようになります。Dell PowerFlexは、Project Alpineを通じてパブリック・クラウドで利用可能になるデルの主要なストレージ・ソフトウェア製品の最初の製品であり、AWSの幅広いデータ保護ポートフォリオを補完するものです。

- 2022年5月:レッドハットとアクセンチュアは、世界中の企業向けにパワーオープンなハイブリッドクラウド・イノベーションを推進するため、約12年にわたる戦略的パートナーシップを拡大しました。両社は、マルチクラウドとハイブリッドクラウドの世界におけるシームレスなナビゲーションを支援する新しいソリューションの共同開発に投資し、戦略を定義し、イノベーションのペースを加速して、より早く価値を実現するために提携します。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の市場への影響評価

- 過去数年間のコスト/価格動向分析

第5章 市場力学

- 市場促進要因

- 組織全体におけるクラウド導入の増加

- 低コストストレージとデータアクセスの高速化に対する需要の高まり

- 市場の課題

- プライバシーとセキュリティへの懸念

- 技術スナップショット

- クラウド・ストレージ・ゲートウェイ

- プライマリストレージ

- バックアップ・ストレージ

- データアーカイブ

第6章 市場セグメンテーション

- モード別

- プライベートクラウド

- パブリッククラウド

- ハイブリッドクラウド

- 業界別

- BFSI

- 小売・消費財

- ヘルスケア

- メディア・エンターテイメント

- IT・通信

- 製造業

- 政府機関

- その他エンドユーザー業界別

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Google LLC(Alphabet Inc.)

- Amazon Web Services Inc.

- Dropbox Inc

- Dell EMC(Dell Technologies Inc.)

- Hewlett Packard Enterprise Company

- IBM Corporation

- Microsoft Corporation

- Oracle Corporation

- Rackspace Inc.

- NetApp Inc.

- Alibaba Cloud(Alibaba Group)

第8章 投資分析

第9章 市場の将来展望

The Cloud Storage Market size is estimated at USD 117.12 billion in 2024, and is expected to reach USD 343.33 billion by 2029, growing at a CAGR of 24% during the forecast period (2024-2029).

The increasing demand for low-cost data backup, storage, and protection across all enterprises, coupled with the need to handle data generated by augmented usage of mobile technologies, favors the adoption rate of cloud storage.

Key Highlights

- The cloud storage market is expected to grow due to rising data volumes across enterprises and the growing need to provide remote workers with ubiquitous access to data and files. For instance, according to Seagate Technologies Holdings PLC, from 2020 to 2022, total enterprise data volume is expected to go from approximately one petabyte (PB) to 2.02 petabytes. This is a 42.2% average annual growth over two years.

- Further, the total volume of data/information created, captured, copied, and consumed worldwide is expected to reach 181 zettabytes in 2025 from 79 zettabytes in 2021. Further, the World Economic Forum estimates that, by 2025, 463 exabytes of data will be created globally, equivalent to 212,765 thousand DVDs per day.

- Moreover, the increasing demand for low-cost data backup and protection across all enterprises, coupled with the necessity of handling the data generated by augmented usage of mobile technologies, favors cloud storage adoption. Companies regularly find ways to mitigate their operating costs and increase profit margins, which can be done by outsourcing or adopting managed cloud services from third-party vendors.

- Through strategic partnerships, mergers and acquisitions, and R&D, some of the prominent players in the market have been able to further develop the cloud storage technology. This may fuel the demand for cloud storage over the forecast period.

- Amid the COVID-19 pandemic, many countries mandated work from home due to public health safety concerns that drove the need for remote working infrastructure. Thus, organizations at all levels, including government bodies, expected a wide range of potential impacts, such as increased demand for virtual services, coupled with rising citizen expectations around the delivery of these services, the long-term potential for reshaping the government workforce, and the need to provide adaptive and dynamic regulatory models.

Cloud Storage Market Trends

BFSI Expected to Hold a Significant Share

- To improve revenue generation, banks increase customer insights, contain costs, deliver market-relevant products quickly and efficiently, and help monetize enterprise data assets; they have started digitizing their work by introducing online portals through which a user can directly meet his work without any requirement for a bank official's intervention. This further results in a substantial increase in data generation, propelling such institutions to adopt cloud storage.

- Banking service providers worldwide are adopting cloud storage solutions as it enables banks to synchronize the enterprise, break down operational and data silos across risk, finance, regulatory, and customer support, and allow institutions to combine massive data sets in one place for advanced analytics and integrated insights.

- Increasing initiatives from technology vendors to help the BFSI players transition into the cloud also fuel this segment's growth. According to Finder, in 2021, digital-only banks had more than 14 million customers from Britain, which is expected to grow by 10 million in the next few years. This indicates that such an increase would require solutions like cloud storage to handle the surge, thereby boosting the growth of cloud storage over the forecast period.

- The rising data breaches in the banking sector are driving the banks to adopt cloud storage that enables them to store data in a space managed and owned by the bank or a third party, providing enhanced security to the end-user. This is expected to increase cloud storage adoption over the forecast period. For instance, according to the data from the Identity Theft Resource Center, the number of data compromises in the financial services sector in the United States reached 268 in 2022, up from 138 such incidents in 2020.

North America Expected to Hold the Largest Share

- North America is predicted to hold a major share owing to the early adoption of new technologies, huge investments in R&D for cloud-based solutions, and enhanced IT infrastructure. Moreover, cheap and secure storage options result in rapid industrial development.

- The North American region has a strong foothold of vendors in the market. Some of them include Google LLC, IBM Corporation, Microsoft Corporation, Oracle Corporation, and Amazon Web Services Inc. Through research and development, these prominent players in the region have been able to develop the technology further. This is expected to boost the adoption of cloud storage and reduce the cost of cloud storage throughout the forecast period.

- According to a report published by Stormforge in April 2021, 18% of respondents from North America stated that their organization has a monthly cloud spend that ranges between USD 100,000 and USD 250,000. Further, 44% expect cloud spending to increase over the next 12 months, while another 32% indicate that they expect their organization's cloud spending to increase significantly over the next 12 months.

- Moreover, the government of Canada has adopted a "cloud-first" strategy, whereby cloud services are identified and estimated as the principal delivery option when initiating information technology investments, initiatives, strategies, and projects. The cloud will also let the government harness the innovation of private-sector providers and thus make its information technology more agile. Such initiatives are expected to offer plenty of opportunities to the hybrid cloud market, as this model enables private cloud security and public cloud flexibility.

Cloud Storage Industry Overview

The cloud storage market is moderately concentrated owing to some major players, such as Microsoft, IBM, and Oracle, holding significant market share. Their ability to continually innovate their offerings has allowed them to gain a competitive advantage over others. Through strategic partnerships, research and developments, and mergers & acquisitions, these players have gained a more significant footprint in the market.

- November 2022: As part of continuing Dell APEX portfolio momentum, Dell Technologies Inc. announced that Dell PowerFlex is available in the AWS Marketplace. This offer provides customers with the mission-critical performance, resilience, scale, and management of PowerFlex with the ability to use existing cloud credits. Dell PowerFlex is the first of Dell's leading storage software offerings to be available in the public cloud via Project Alpine and compliments its broad AWS data protection portfolio.

- May 2022: Red Hat and Accenture expanded their nearly 12-year strategic partnership to advance power-open hybrid cloud innovation for enterprises worldwide. The companies are partnering to invest in the co-development of new solutions to help in the seamless navigation of a multi- and hybrid cloud world, define their strategy, and accelerate their pace of innovation to get to value faster.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Force Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of COVID-19 on the Market

- 4.5 Cost/Price Trend Analysis for the Past Few Years

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increase in Cloud Adoption Across Organizations

- 5.1.2 Growing Demand for Low-cost Storage and .Faster Data Accessibility

- 5.2 Market Challenges

- 5.2.1 Privacy and Security Concerns

- 5.3 TECHNOLOGY SNAPSHOT

- 5.3.1 Cloud Storage Gateway

- 5.3.2 Primary Storage

- 5.3.3 Backup Storage

- 5.3.4 Data Archiving

6 MARKET SEGMENTATION

- 6.1 By Mode

- 6.1.1 Private Cloud

- 6.1.2 Public Cloud

- 6.1.3 Hybrid Cloud

- 6.2 By End-user Vertical

- 6.2.1 BFSI

- 6.2.2 Retail and Consumer Goods

- 6.2.3 Healthcare

- 6.2.4 Media and Entertainment

- 6.2.5 IT and Telecom

- 6.2.6 Manufacturing

- 6.2.7 Government

- 6.2.8 Other End-user Verticals

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia-Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Google LLC (Alphabet Inc.)

- 7.1.2 Amazon Web Services Inc.

- 7.1.3 Dropbox Inc

- 7.1.4 Dell EMC (Dell Technologies Inc.

- 7.1.5 Hewlett Packard Enterprise Company

- 7.1.6 IBM Corporation

- 7.1.7 Microsoft Corporation

- 7.1.8 Oracle Corporation

- 7.1.9 Rackspace Inc.

- 7.1.10 NetApp Inc.

- 7.1.11 Alibaba Cloud (Alibaba Group)