|

市場調査レポート

商品コード

1441700

睡眠時無呼吸用デバイス:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Sleep Apnea Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| 睡眠時無呼吸用デバイス:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 116 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

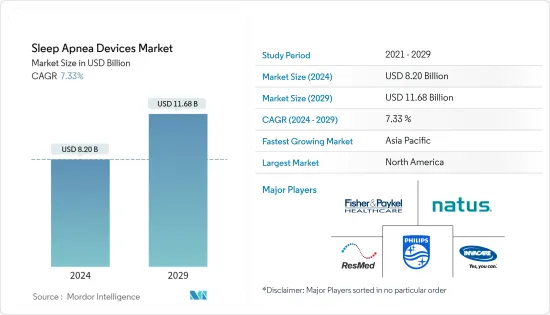

睡眠時無呼吸用デバイスの市場規模は、2024年に82億米ドルと推定され、2029年までに116億8,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に7.33%のCAGRで成長します。

COVID-19のパンデミックは、睡眠時無呼吸用デバイス市場に大きな影響を与えると予想されています。 2021年1月にBMJ Open Respiratory調査に発表された研究によると、閉塞性睡眠時無呼吸症候群(OSA)の患者は、OSAではない人に比べて、COVID-19の影響を受けた場合に入院するリスクが2.93倍高かったです。この研究はまた、COVID-19が疑われる、または感染が確認された患者の評価において、閉塞性睡眠時無呼吸症候群が重篤な疾患を発症する併存疾患の危険因子の1つとして認識されるべきであることを示唆しました。 2022年 3月に睡眠財団組織が発表した記事によると、COVID-19はさまざまな方法で睡眠パターンを変化させ、中断させました。記事はさらに、成人、子供、青少年の間で不眠症の症状が顕著に増加しており、ほぼ40%の人が睡眠に問題があると報告していることが研究で判明したと述べました。パンデミック後であってもこの睡眠障害の増加は、今後数年間で睡眠時無呼吸症候群市場に影響を与えると予想されます。

市場を牽引する主な要因には、睡眠時無呼吸症候群の発生率の増加、高齢者人口の増加、肥満と高血圧の有病率の増加、新興諸国の患者人口の意識の高まりなどが含まれます。高齢化は睡眠時無呼吸用デバイス市場の成長を促進する主な要因です。この障害を発症するリスクが最も高いのは高齢者です。 2022年の世界人口見通しによると、世界人口に占める65歳以上の人口の割合は2022年の10%から2050年には16%に上昇すると予測されています。2050年までに、世界中の65歳以上の人の数は5歳未満の子供の数の2倍以上、12歳未満の子供の数とほぼ同じです。

また、革新的な製品に対する需要の高まりに応えるためのメーカーによる発売の増加も、市場の成長を促進すると予想されます。たとえば、2021年8月、フィリップスのCPAPリコールによって空いた穴を埋めるべく争奪戦が繰り広げられる中、レスメドは新しい睡眠時無呼吸治療器を発表しました。同様に、閉塞性睡眠時無呼吸症候群に対する口腔器具療法のホームケアプロバイダーであるGoPAPfreeは、2021年 2月に、CPAP療法に代わる非常に効果的でより便利な新製品 O2Vent Optimaを発売しました。

さらに、睡眠障害は最も困難な病状の一部であり、3人に1人が人生のある段階で影響を受けていることも報告しました。睡眠時無呼吸症候群は、生命を脅かす重篤な睡眠疾患ですが、通常は診断も治療も受けられません。しかし、さまざまな政府の取り組みがOSAに苦しむ患者を助けています。たとえば、米国では、睡眠時無呼吸症候群に関する意識を高め、治療の継続的な改善に取り組み、睡眠時無呼吸症候群患者の利益を擁護する非営利団体である米国睡眠時無呼吸症候群協会(ASAA)が活動しています。

したがって、上記の要因が市場の成長を促進しています。ただし、CPAPマシンのコストが高いため、市場の成長が妨げられると予想されます。

睡眠時無呼吸用デバイスの市場動向

パルスオキシメーターは、診断用デバイスカテゴリーで最高のCAGRで推移すると予想されます

パルスオキシメーターは、血中ヘモグロビン酸素飽和度の測定に広く使用されています。これらは、比較的非侵襲的な方法で血中ヘモグロビン酸素飽和度を長期間にわたって継続的に測定するために使用されます。その利便性により、病院やヘルスケア機関ではほぼ遍在する機器となっています。大人と子供の閉塞性睡眠時無呼吸症候群を調査および診断するためのパルスオキシメトリーの応用は、さまざまな実践から構成されます。パルスオキシメーターを夜間睡眠ポリグラム(PSG)の一部として使用すると、酸素濃度測定データのパターンを他の生理学的チャネルのイベントと照らし合わせて解釈でき、病態生理の詳細な特徴付けが可能になる可能性があります。

さらに、睡眠時無呼吸症候群の世界の有病率の増加により、予測期間中にこのセグメントが押し上げられると予想されます。 American Journal of Respiratory and Critical Care Medicineに2021年7月に発表された研究によると、OSAの世界の有病率は22.6%(95%信頼区間、20.9~24.3%)でした。一晩に基づいたOSA患者の誤診の可能性は、約20%~50%の範囲でした。したがって、睡眠時無呼吸症候群の有病率の増加がセグメントの成長を促進すると予想されます。

メドトロニックは、NellcorポータブルSpO2患者モニタリングシステムPM10Nと呼ばれるパルスオキシメーターを製造しています。このデバイスは、さまざまなヘルスケアや家庭での使用環境での即時チェックと継続的なモニタリングに最適です。人間工学に基づいた形状とシンプルなデザインにより、直感的に使用でき、操作も簡単です。このようなタイプのデバイスが入手可能になると、市場の成長に役立ちます。

さらに、このセグメントを後押しできる製品の発売と承認、パートナーシップ、コラボレーション、合併、買収などの多くの開発が行われています。たとえば、2021年 1月、遠隔医療会社Tyto Careは、血中酸素飽和度レベルと心拍数を遠隔でチェックするための、米国食品医薬品局(FDA)の認可を受けた指先パルスオキシメーター(SpO2)医療機器を発売しました。

したがって、睡眠時無呼吸症候群の有病率の増加やデバイスの可用性などの前述のすべての要因が、予測期間中のセグメントの成長を押し上げます。

北米が市場を独占しており、予測期間中もその優位性が続くと予想

現在、睡眠時無呼吸用デバイス市場は北米が独占しており、予測期間中もその傾向が続くと予想されます。この市場は、うつ病や不安などのいくつかの基礎疾患による睡眠時無呼吸症候群の有病率の上昇、技術の進歩、および地域のアメリカ人に対するCOVID-19のロックダウンの深刻な影響による研究の増加による製品発売によって牽引されると予測されています。たとえば、2021年5月のCOVID-19と精神的健康に関する調査(SCMH)によると、18歳以上のカナダ人の4人に1人(25%)が、うつ病、不安、心的外傷後ストレス障害(PTSD)の症状の検査で陽性反応を示しました。

2022年 1月にUpToDateに掲載された研究によると、北米における推定有病率は男性で15~30%、女性で10~15%です。さらに、同じ研究によると、体重の10%増加はOSAのリスクの6倍の増加と関連していました。さらに、Clocks and Sleepが2022年2月に発表した研究によると、中等度から重度のOSAカテゴリーに属する男性の割合(16.3%)が女性と比べて高かったです。もう1つの興味深い観察結果は、中等度から重度のOSA参加者の12.9%が18~39歳の年齢層であったことです。肥満の有病率は49.4%でした。この研究では、男性の38%、女性の58%が肥満であると定義されました。したがって、肥満の有病率の増加により、睡眠時無呼吸症候群の需要が増加し、それによって予測期間中に市場を牽引すると予想されます。

したがって、上記の要因により、市場は分析期間中に北米地域で成長すると予想されます。

睡眠時無呼吸用デバイス業界の概要

睡眠時無呼吸用デバイス市場は競争が激しく、世界中に大手企業が数社あります。技術の進歩と製品の革新が進む中、中小規模の企業は、新しいデバイスを競争力のある価格で市場に導入することで、市場での存在感を高めています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 途上諸国の患者の間での意識の向上

- 肥満と高血圧の有病率の増加

- 今後の技術の進歩

- 市場抑制要因

- CPAPマシンの高コスト

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 診断用デバイス別

- 睡眠ポリグラフィ(PSG)デバイス

- パルスオキシメーター

- アクティグラフィデバイス

- 治療用デバイス別

- 陽圧呼吸(PAP)デバイス

- 持続陽圧呼吸(CPAP)デバイス

- 二相性陽圧呼吸(BiPAP)デバイス

- 酸素デバイス

- 酸素濃縮器

- ポータブル酸素濃縮器

- ポータブル液体酸素

- 口腔器具

- 順応性サーボ換気(ASV)デバイス

- マスク・付属品

- 陽圧呼吸(PAP)デバイス

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東とアフリカ

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Fisher &Paykel Healthcare Limited

- Koninklijke Philips NV

- Invacare Corporation

- Natus Medical Incorporated

- Resmed

- Cadwell Laboratories Inc.

- Vyaire Medical Inc.

- GE Healthcare

- Nihon Kohden Corporation

- Teleflex Incorporated

- Somnomed

- Oventus Medical

第7章 市場機会と将来の動向

The Sleep Apnea Devices Market size is estimated at USD 8.20 billion in 2024, and is expected to reach USD 11.68 billion by 2029, growing at a CAGR of 7.33% during the forecast period (2024-2029).

The COVID-19 pandemic is expected to have a significant impact on the sleep apnea devices market. According to a study published in January 2021 in the BMJ Open Respiratory Research, patients with obstructive sleep apnea (OSA) had a 2.93 times higher risk to be hospitalized when affected by COVID-19 than non-OSA individuals. The study also suggested that in the assessment of patients who were suspected or confirmed with COVID-19 infection, obstructive sleep apnea should be recognized as one of the comorbidity risk factors for developing a severe form of the disease. As per the article published by the Sleep Foundation Organization in March 2022, COVID-19 altered and interrupted sleep patterns in a variety of ways. The article further stated that studies have found that the prevalence of insomnia symptoms among adults, children, and adolescents had increased noticeably, and almost 40% of people report having trouble sleeping. This increase in sleep disorders even post-pandemic is expected to have an impact on the sleep apnea market in the years to come.

The major factors driving the market include the increasing incidences of sleep apnea, an increase in the geriatric population, an increase in the prevalence of obesity and hypertension, and increasing awareness among the patient population in developing countries. Aging is a major factor driving the market growth for sleep apnea devices. The elderly are the most at risk for developing this disorder. According to the World Population Prospects 2022, the share of the global population aged 65 years or above is projected to rise from 10% in 2022 to 16% in 2050. By 2050, the number of persons aged 65 years or over worldwide is projected to be more than twice the number of children under age 5 and about the same as the number of children under age 12.

Also, the increasing launches by manufacturers to meet the growing demand for innovative products are expected to drive market growth. For instance, in August 2021, ResMed unveiled a new sleep apnea machine amid a scramble to fill the void left by Philips' CPAP recall. Similarly, in February 2021, GoPAPfree, a homecare provider of oral appliance therapy for obstructive sleep apnea launched its new product O2Vent Optima, a highly effective and more convenient alternative to CPAP therapy.

Furthermore, it also reported that sleep disorders represent some of the most challenging medical conditions and affect 1 out of 3 people at some stage of their lives. Sleep apnea is a serious and life-threatening sleep illness that usually goes undiagnosed and untreated. However, various government initiatives are helping patients who suffer from OSA. For instance, in the United States, the American Sleep Apnea Association (ASAA) which is a non-profit organization that promotes awareness regarding sleep apnea, works for continuing improvements in treatments, and advocates for the interests of sleep apnea patients.

Thus, the above-mentioned factors are boosting the market's growth. However, the high cost of CPAP Machines is expected to hinder the growth of the market.

Sleep Apnea Devices Market Trends

Pulse Oximeters are Expected to Register the Highest CAGR in the Diagnostic Devices Category

Pulse oximeters are used extensively in the measurement of blood hemoglobin oxygen saturation. They are used to measure blood hemoglobin oxygen saturation continuously over time in a relatively noninvasive way. Due to their convenience, they have become an almost ubiquitous instrument in hospitals and healthcare institutions. The application of pulse oximetry to investigate and diagnose obstructive sleep apnoea in adults and children consists of different practices. When pulse oximeters are used as a part of an overnight polysomnogram (PSG), the patterns in the oximetry data can be interpreted in the context of events in other physiological channels, potentially allowing detailed characterization of the pathophysiology.

Additionally, the increasing global prevalence of sleep apnea is expected to boost the segment over the forecast period. According to the study published in July 2021, published in the American Journal of Respiratory and Critical Care Medicine, The OSA global prevalence was 22.6% (95% confidence interval, 20.9-24.3%). The likelihood of misdiagnosis in people with OSA based on a single night ranged between approximately 20% and 50%. Thus, the growing prevalence of sleep apnea is expected to drive segment growth.

Medtronic manufactures a pulse oximeter called Nellcor portable SpO2 patient monitoring system, PM10N. This device is ideal for instant checks and continuous monitoring in various healthcare and also home use settings. Its ergonomic shape and simple design make it intuitive to use and simple to operate. The availability of these types of devices will help with the market growth.

Additionally, many developments are taking place that includes product launches and approvals, partnerships, collaborations, mergers, and acquisitions that can boost the segment. For instance, in January 2021, Telehealth company Tyto Care launched its United States Food and Drug Administration (FDA)-cleared fingertip Pulse Oximeter (SpO2) medical device for checking blood oxygen saturation levels and heart rate remotely.

Thus, all aforementioned factors such as the increasing prevalence of sleep apnea and the availability of devices boost the segment growth over the forecast period.

North America Dominates the Market, and it is Expected to Continue its Dominance through the Forecast Period

North America currently dominates the market for sleep apnea devices, and it is expected to continue during the forecast period. The market is predicted to be driven by the rising prevalence of sleep apnea due to several underlying conditions such as depression and anxiety, technical advancements, and research-increasing product launches with the profound impact of COVID-19 lockdowns on Americans in the region. For instance, according to the Survey on COVID-19 and Mental Health (SCMH) in May 2021, 1 in 4 (25%) Canadians of age 18 and older screened positive for symptoms of depression, anxiety, or posttraumatic stress disorder (PTSD).

According to a study published in UpToDate in January 2022, the estimated prevalence in North America is 15 to 30% in males and 10 to 15% in females. Furthermore, according to the same study, a 10% increase in weight was linked to a six-fold increase in the risk of OSA. Moreover, as per the study published by Clocks and Sleep in February 2022, there was a higher proportion of males (16.3%) in the moderate to severe OSA category compared to females. Another interesting observation was that 12.9% of moderate to severe OSA participants were in the 18-39 years age group. The prevalence of obesity was 49.4%. In this study, 38% of males and 58% of females were defined as being obese. Thus, the growing prevalence of obesity is expected to rise the demand for sleep apnea, thereby driving the market over the forecast period.

Therefore, owing to the abovementioned factors, the market is expected to grow in the North American region over the analysis period.

Sleep Apnea Devices Industry Overview

The sleep apnea devices market is highly competitive, with several major players across the world. With the rising technological advancements and product innovations, mid-size and small-scale companies are increasing their market presence by introducing new devices into the market at competitive prices. Companies, like Resmed, Fisher & Paykel Healthcare Limited, and Invacare Corporation, hold substantial shares in the market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Awareness Among the Patient Population in the Developing Countries

- 4.2.2 Increase in Prevalence of Obesity and Hypertension

- 4.2.3 Upcoming Technological Advancements

- 4.3 Market Restraints

- 4.3.1 High Cost of Cpap Machines

- 4.4 Industry Attractiveness- Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Diagnostic Devices

- 5.1.1 Polysomnography Devices (PSG)

- 5.1.2 Pulse Oximeters

- 5.1.3 Actigraphy Devices

- 5.2 By Therapeutic Devices

- 5.2.1 Positive Airway Pressure (PAP) Devices

- 5.2.1.1 Continuous Positive Airway Pressure (CPAP) Devices

- 5.2.1.2 Bi-level Positive Airway Pressure (BiPAP) Devices

- 5.2.2 Oxygen Devices

- 5.2.2.1 Oxygen Concentrators

- 5.2.2.2 Portable Oxygen Concentrators

- 5.2.2.3 Liquid Portable Oxygen

- 5.2.3 Oral Appliances

- 5.2.4 Adaptive Servo Ventilation (ASV) Devices

- 5.2.5 Masks and Accessories

- 5.2.1 Positive Airway Pressure (PAP) Devices

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle-East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle-East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Fisher & Paykel Healthcare Limited

- 6.1.2 Koninklijke Philips NV

- 6.1.3 Invacare Corporation

- 6.1.4 Natus Medical Incorporated

- 6.1.5 Resmed

- 6.1.6 Cadwell Laboratories Inc.

- 6.1.7 Vyaire Medical Inc.

- 6.1.8 GE Healthcare

- 6.1.9 Nihon Kohden Corporation

- 6.1.10 Teleflex Incorporated

- 6.1.11 Somnomed

- 6.1.12 Oventus Medical