|

市場調査レポート

商品コード

1432960

データ収集:市場シェア分析、産業動向と統計、成長予測(2024年~2029年)Data Acquisition - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| データ収集:市場シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

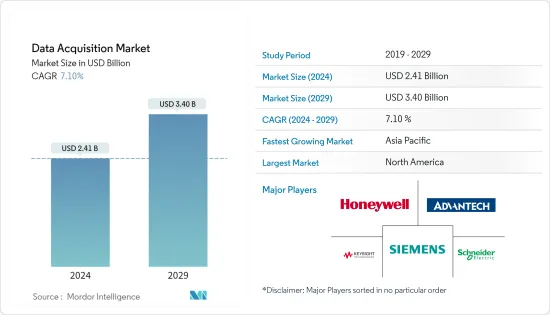

データ収集市場規模は2024年に24億1,000万米ドルと推定され、2029年までに34億米ドルに達すると予測されており、予測期間(2024年から2029年)中に7.10%のCAGRで成長します。

データ収集システムは、産業部門におけるリアルタイムの意思決定において重要な役割を果たします。企業が生産と運用におけるデータ中心のアプローチに向けて発展し、ユーザーが場所に関係なくいつでもデータにアクセスできるようにしながら競争力を維持するにつれて、データ収集システムは単なる処理システムから、自動化のメリットを最大限に活用できます。

主なハイライト

- データ収集市場の主な推進力の1つは、イーサネットの有望な成長です。産業用イーサネットは、ここ数年で従来のフィールドバスよりも急速に成長し、フィールドバスを追い越しました。

- この需要は、より高速なインターネット速度、工場設備のシームレスな統合、IoTの導入、および産業用制御に対するニーズの高まりによって増大しています。このような動向は、データ収集システムの需要を促進するのに役立ってきました。

- さらに、世界中でのファクトリーオートメーションとスマートマニュファクチャリングの導入は、データ収集市場の主要な成長原動力となっています。これには、複数のシステムパラメータの追跡や、PLC、データベース、メンテナンスアプリケーション、既存のデータ収集システムなどのデータをリアルタイムで交換しながら多くのデータソースを監視して、機械やフロアの動作の可視性を高めることが含まれます。

- データ収集システムの市場は北米が独占していましたが、政府の優れた改革、産業オートメーションの強力な導入、スマート製造の初期化により、欧州地域の市場が押し上げられ、予測期間中にさらに重要な市場シェアを獲得すると予想されます。この発展は、次世代の産業ソリューションを導入しているドイツと英国の経済によって支えられると予想されます。

- さらに、電子技術の進歩により、安価なセンシングおよび監視機能が実現しました。 Arduinoと呼ばれるオープンソースハードウェアプロジェクトは、低コストのセンサーとともに、調査目的でいくつかの安価な自動センシングおよびデータロギングシステムを開発するために使用されています。これは、将来、高度なシステムを開発するためのオープンソース DAQソフトウェアへの投資が増加する可能性があることを示唆しています。

- パンデミックにより、いくつかの業界や企業は移行を余儀なくされ、市場では完全に監視された業務への切り替えと、適切に設計されたシステムを通じて得られる先見性の向上が促されました。最も重要なシステムは、効率を向上させるためにデータ収集システムの実装を開始しました。

データ収集市場の動向

航空宇宙および防衛が市場で大きなシェアを占める

- 効率的な宇宙探査デバイスの開発により、より安全で適切に管理された旅を可能にするデータ収集システムの需要が高まっています。 SpaceXやBlueOriginなどのこの分野の新興企業は、一貫して効率的な相互接続システムの構築に取り組んできました。 2021年8月、SpaceXは衛星データのスタートアップであるSwarm Technologiesを買収し、120基のSpaceBee衛星を軌道上に統合し、データ収集の取り組みを推進し、スターリンクインフラを拡張しました。

- DDSは、P&Vシステム、32台のIPカメラ、8台のマイク、および進行中のテストを観察するDASからのデータを表示するために使用されました。 GUIは、リアルタイムの進行状況を表示したり、過去のテストデータを取得したりするために補完的に使用されます。 3つのシステムのタンデム操作により、エンジニアは現実世界のシナリオを再現し、初期段階の構造テストを完了するために必要な機能のより詳細なシミュレーションを促進できます。

- 航空宇宙分野のすべてのコラボレーションが宇宙探査に特化しているわけではありません。センサーとデータ分析システムの感度の向上により、宇宙観測の取り組みの成長が予測されています。 2021年7月、スパイア・世界はNASAの商用小型衛星データ収集(CSDA)プログラムへの参加継続を600万米ドルの契約延長で発表しました。この契約には、電波掩蔽(RO)データ、土壌水分、精密軌道決定(POD)データ、斜角 GNSS-RO、総電子量(TEC)データ、海洋を提供するサブスクリプションデータソリューションであるタスクオーダー6(TO6)が含まれています。表面風速GNSS反射率測定データ、および磁力計データの取得。データは、すべての連邦政府機関、NASAの資金提供を受けた研究者、および米国政府の資金提供を受けたすべての研究者が科学目的で利用できるようになります。

- NASAは、Spireデータによって可能になった利点、特に宇宙ベースのデータを利用して地球の大気を分析し、地球観測システムに統合するGEOS大気データ同化システムについて述べました。さらに、NASAは、極域の水と海氷のレベル、惑星境界層の高度(PBL)の高さ、飛行レベルでの熱圏密度の日次変動に関する調査にスパイアのデータを使用しています。

北米が現在最大の市場シェアを保持

- 北米のデータ収集市場は大幅に成長しており、National Instruments、Keysight、Tektronix、Siemensなどの企業が市場の35%以上を占めています。ただし、産業用モノのインターネット(IIoT)アーキテクチャを通じたインテリジェント製造に対する需要の増加は、適切なハードウェアとソフトウェアを選択することで実現可能になっています。この地域では、エラーのない結果をもたらす、より高速な生産手段の導入が顕著に見られます。

- 平均して、メーカーは時間の80%近くをアーキテクチャとデータ収集の処理に費やしました。残りの20%はデータ分析に使用できるため、IIoTを導入することでデータ収集にかかる時間を短縮できます。これには、この地域でIIoTを主流に採用する必要があります。 IIoTエコシステムを構築するために、ベンダーはいくつかの対策を講じています。たとえば、National InstrumentsはCisco、Intelなどと協力してIIoT Labを設立しました。さらに、IoTはサプライチェーン全体にわたって重要です。

- さらに、米国は世界有数の自動車市場であり、13社以上の主要自動車メーカーが拠点を置いています。自動車製造業は、この国の製造部門において最大の収益源の1つです。

- 産業オートメーションは、DAQシステムの需要を促進すると予想される主な促進要因です。人間の介入を伴わない制御プロセスの採用が増加しており、指示を提供するデータに大きく依存しています。したがって、ちょっとした方向性の誤りが業界に甚大な損失をもたらす可能性があります。

- 効率的なデータ収集は、あらゆる規制への準拠を確保し、あらゆる運行に対する監視意識を維持するために、車両の動作に関する正確なデータを提供するための、あらゆる車両の中核的なコンポーネントとなっています。フォルクスワーゲンの排ガスに関するスキャンダル以来、信頼性の観点からユーザーのニーズが浮上しており、DCSや運用監視機能など、他のシステムやシステム機能とのコンプライアンスが優先事項となっています。

データ収集業界の概要

データ収集市場は細分化されています。市場で活動している大手企業は、買収や戦略的合併を利用して競合を排除し、自社の能力を向上させようとしています。市場の主要企業には、ABB Ltd、Advantech、Agilent Technologies、Campbell Scientific Inc.、Data Translation Inc.、Schneider Electric SE、Honeywell International、Siemens AG、Rockwell Automation Inc.、MathWorks Corporation、General Electric Ltd、Omron Corporation、横河電機株式会社、エマソン電機株式会社

市場における主な発展には次のようなものがあります。

- 2021年 4月- 世界なカスタマーエクスペリエンスプラットフォームであるPianoは、ID5、InfoSum、LiveRamp、Usercentricsと提携して、ファーストパーティデータ収集ソリューションを拡張しました。これは、データ管理、アイデンティティ、カスタマージャーニーオーケストレーション機能を統合し、1つのシステムとデジタルエコシステム全体でユーザーデータを収集、統合、有効化する1つのビューで、データ漏洩や広告パフォーマンスの低下を防ぎながら、顧客エクスペリエンスを向上させます。

- 2021年 4月- 自動化された外部データプラットフォームであるExploriumは、高度な分析と機械学習のためのデータ収集製品であるSignal Studioの発売を発表しました。これにより、データアナリストチームとビジネスアナリストチームは、最も関連性の高い外部データシグナルを迅速に見つけて統合できるようになります。分析パイプライン。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因と市場抑制要因のイントロダクション

- 市場促進要因

- 産業用イーサネットソリューションの採用拡大

- 製造現場の複雑化により、設計検証とテストにDAQの導入が進む

- エッジコンピューティングやTSNなどの技術的進歩

- 市場抑制要因

- 主要市場におけるコスト問題と飽和が、予測期間中の成長を妨げる可能性

- バリューチェーン分析

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- 流通チャネル分析(ディストリビューター、システムインテグレーター、直販)

- 技術スナップショット

- DAQ接続技術の進化

- TSNとエッジコンピューティングの採用による影響予測

- 統合プラットフォームへのシフトの分析

第5章 市場セグメンテーション

- チャネル

- 32未満

- 32-128

- 128以上

- タイプ

- ハードウェア

- ソフトウェア

- エンドユーザー業界別

- 水処理・廃棄物処理

- 電力・エネルギー

- 自動車

- 教育・研究

- 航空宇宙・防衛

- 製紙・パルプ

- 化学

- その他のエンドユーザー業界

- 地域

- 北米

- 欧州

- アジア太平洋

- 世界のその他の地域

第6章 競合情勢

- ベンダー市場シェア分析- 世界および地域別

- 企業プロファイル

- Advantech Co. Ltd

- Spectris PLC(HBM and Bruel & Kjaer and Omega)

- National Instruments Corporation

- Schneider Electric SE

- ABB Ltd

- Honeywell International

- Siemens AG

- Rockwell Automation Inc.

- Keysight Technologies

- General Electric Ltd

- Omron Corporation

- Yokogawa Electric Co.

- Tektronix

- AMETEK(VTI Instruments)

- Bustec

- Emerson Electric Co.

- Curtiss-Wright Corporation

- DAQ Systems Co, Limited

- Imc Dataworks, LLC

- ADLINK Technology, Inc.

- Beijing GEMOTECH Intelligent Technology

- DATAQ Instruments

第7章 投資分析

- DAQハードウェアおよびソフトウェアセグメントにおける主要ベンダーの競合要因と戦略

- 主要なM&A

第8章 市場機会と今後の動向

The Data Acquisition Market size is estimated at USD 2.41 billion in 2024, and is expected to reach USD 3.40 billion by 2029, growing at a CAGR of 7.10% during the forecast period (2024-2029).

Data acquisition systems play an essential role in real-time decision-making in the industrial sector. As companies develop toward a data-centric approach in production and operations to maintain a competitive edge while promoting the users to access the data at any time, irrespective of the location, data acquisition systems have evolved from mere processing systems to the key to achieving the full benefits of automation.

Key Highlights

- One of the primary drivers of the data acquisition market is the promising growth of Ethernet. Industrial Ethernet has grown faster than traditional field buses during the last few years and has overtaken field buses.

- This demand has been augmented by the growing need for faster internet speeds, seamless integration of factory installations, the adoption of IoT, and industrial controls. Such trends have been instrumental in driving the demand for data acquisition systems.

- Moreover, the adoption of factory automation and smart manufacturing across the world is a major growth driver of the data acquisition market. These include tracking multiple system parameters and monitoring many data sources while exchanging data in real-time, including PLCs, databases, maintenance applications, and existing data acquisition systems, to gain greater visibility of the machine and floor operations.

- Although North America dominated the market for data acquisition systems, good government reforms, strong industrial automation adoption, and smart manufacturing initializes are expected to boost the market in the European region to attain a more significant market share over the forecast period. This development is anticipated to be backed by the economies of Germany and the United Kingdom, which are adopting the next generation of industrial solutions.

- Additionally, advances in electronic technologies led to inexpensive sensing and monitoring capabilities. An Open-Source Hardware project called Arduino has been used, along with low-cost sensors, to develop several inexpensive, automated sensing and data logging systems for research purposes. This is suggestive of potential yet increased open-source DAQ software investment for developing the advanced system in the future.

- The pandemic forced a transition for several industries and enterprises and primed the market for a switch into fully monitored operations and the increased prescience obtained through well-designed systems. Most critical systems began implementing data acquisition systems to improve their efficacies.

Data Acquisition Market Trends

Aerospace and Defense Accounts for Significant Share in the Market

- The development of efficient space exploration devices elevates the demand for data acquisition systems that enable safer and better-managed journeys. Startups in the sector, such as SpaceX and BlueOrigin, have been consistent with work in the establishment of efficient, interconnected systems. In August 2021, SpaceX acquired the satellite data startup Swarm Technologies to consolidate their 120 SpaceBee satellites in orbit, furthering their data acquisition initiatives and expanding their star-link infrastructure.

- The DDS was employed to present data from the P&V system, 32 IP cameras, eight microphones, and the DAS to observe the test in progress. GUIs are used complementarily to view real-time progress or retrieve past test data. The tandem operations of the three systems allow engineers to replicate real-world scenarios and encourage more detailed simulation of capabilities needed to complete early-stage structural tests.

- Not all collaborations in aerospace have been dedicated to space exploration. Increasing sensitivity of sensors and data analysis systems have projected the growth of Space Observation initiatives. In July 2021, Spire Global announced the continuation of its participation in NASA's Commercial Small-sat Data Acquisition (CSDA) program with a USD 6 million contract extension. The contract includes Task Order 6 (TO6), a subscription data solution that provides for radio occultation (RO) data, soil moisture, precise orbit determination (POD) data, grazing angle GNSS-RO, total electron content (TEC) data, ocean surface wind speed GNSS-Reflectometry data, and magnetometer data acquisition. The data is made available to all federal agencies, NASA-funded researchers, and all US government-funded researchers for scientific purposes.

- NASA stated the positives that the Spire data has enabled, primarily its GEOS Atmospheric Data Assimilation System, which utilizes space-based data to analyze the earth's atmosphere and integrate it into its earth observation systems. Furthermore, NASA has employed Spire data in research on water and sea ice levels in the polar regions, the Planetary Boundary Layer's height (PBL) height, and the day-to-day variability of thermospheric density at flight level.

North America Presently Holds the Largest Market Share

- The North American market for data acquisition has been growing significantly, with players such as National Instruments, Keysight, Tektronix, and Siemens, accounting for over 35% of the market. However, increasing demand for intelligent manufacturing through Industrial Internet of Things (IIoT) architectures has been made achievable by selecting the appropriate hardware and software. The region is highly depictive of adopting faster means of production with errorless outcomes.

- On average, the manufacturers spent nearly 80% of their time handling the architecture and data acquisition. With the remaining 20% left for data analysis, adopting IIoT can help lower the time spent on data acquisition. This requires a mainstream adoption of IIoT in the region. To build an IIoT ecosystem, the vendors have taken several measures. For instance, National Instruments with Cisco, Intel, and others created an IIoT Lab. Additionally, IoT is significant throughout supply chains.

- Moreover, the United States has been one of the leading automotive markets in the world and is home to over 13 major automobile manufacturers. The automotive manufacturing industry has been one of the largest revenue generators for the country in the manufacturing sector.

- Industrial automation is the primary driving factor expected to drive the demand for DAQ systems. The increasing adoption of controlling processes without human interference relies heavily on data to provide instructions. Hence, any minor misdirection may lead to drastic losses to the industry.

- Efficient data acquisition has become a core component of any vehicle to provide accurate data regarding its working to ensure compliance with any regulation and maintain a sense of oversight over any operations. Since the Volkswagen scandal regarding its emissions, user needs have emerged from a reliability standpoint, and compliance with other systems and system functions, such as DCSs and operation and monitoring functions, has become a priority.

Data Acquisition Industry Overview

The Data Acquisition Market is fragmented. The major companies operating in the market try to eliminate the competition and improve their capabilities utilizing either acquisition or strategic mergers. Some key players in the market include ABB Ltd, Advantech Co. Ltd, Agilent Technologies, Campbell Scientific Inc., Data Translation Inc., Schneider Electric SE, Honeywell International, Siemens AG, Rockwell Automation Inc., MathWorks Corporation, General Electric Ltd, Omron Corporation, Yokogawa Electric Co., and Emerson Electric Co.

Some key developments in the market include:

- April 2021- The global customer experience platform Piano entered into a partnership with ID5, InfoSum, LiveRamp, and Usercentrics to extend its First-Party Data Acquisition solution, that integrates its data management, identity, and customer journey orchestration capabilities and provides one system and one view that collects, unifies and activates user data across the entire digital ecosystem, preventing data leakage and poor ad performance while improving customer experience.

- April 2021 - An automated external data platform, Explorium, announced the launch of its data acquisition product, Signal Studio, for advanced analytics and machine learning that allows the data and business analyst teams to quickly find and integrate the most relevant external data signals into their analytics pipeline.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Introduction to Market Drivers and Restraints

- 4.3 Market Drivers

- 4.3.1 Growing Adoption of Industrial Ethernet Solutions

- 4.3.2 Increasing Complexity in Manufacturing Establishments is Driving Operators Towards Adoption of DAQ for Design Validation and Testing

- 4.3.3 Technological Advancements Such as Edge Computing and TSN

- 4.4 Market Restraints

- 4.4.1 Cost Implications and Saturation in Key Markets Could Hinder Growth Over the Forecast Period

- 4.5 Value Chain Analysis

- 4.6 Industry Attractiveness - Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Distribution Channel Analysis (Distributors, System Integrators and Direct Sales)

- 4.8 Technology Snapshot

- 4.8.1 Evolution of DAQ Connectivity Technologies

- 4.8.2 Anticipated Impact of the Adoption of TSN and Edge Computing

- 4.8.3 Analysis of the Growing Shift Towards Integrated Platforms

5 MARKET SEGMENTATION

- 5.1 Channel

- 5.1.1 Less than 32

- 5.1.2 32-128

- 5.1.3 Greater than 128

- 5.2 Type

- 5.2.1 Hardware

- 5.2.2 Software

- 5.3 End-User Vertical

- 5.3.1 Water and Waste Treatment

- 5.3.2 Power & Energy

- 5.3.3 Automotive

- 5.3.4 Education and Research

- 5.3.5 Aerospace & Defense

- 5.3.6 Paper and Pulp

- 5.3.7 Chemicals

- 5.3.8 Other End-Users

- 5.4 Geography

- 5.4.1 North America

- 5.4.2 Europe

- 5.4.3 Asia Pacific

- 5.4.4 Rest of the World

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share Analysis - Global and Regional

- 6.2 Company Profiles

- 6.2.1 Advantech Co. Ltd

- 6.2.2 Spectris PLC (HBM and Bruel & Kjaer and Omega)

- 6.2.3 National Instruments Corporation

- 6.2.4 Schneider Electric SE

- 6.2.5 ABB Ltd

- 6.2.6 Honeywell International

- 6.2.7 Siemens AG

- 6.2.8 Rockwell Automation Inc.

- 6.2.9 Keysight Technologies

- 6.2.10 General Electric Ltd

- 6.2.11 Omron Corporation

- 6.2.12 Yokogawa Electric Co.

- 6.2.13 Tektronix

- 6.2.14 AMETEK (VTI Instruments)

- 6.2.15 Bustec

- 6.2.16 Emerson Electric Co.

- 6.2.17 Curtiss-Wright Corporation

- 6.2.18 DAQ Systems Co, Limited

- 6.2.19 Imc Dataworks, LLC

- 6.2.20 ADLINK Technology, Inc.

- 6.2.21 Beijing GEMOTECH Intelligent Technology

- 6.2.22 DATAQ Instruments

7 INVESTMENT ANALYSIS

- 7.1 Key Competitive Factors and Strategies of Major Vendors in DAQ Hardware and Software Segments

- 7.2 Major Mergers and Acquisitions