|

市場調査レポート

商品コード

1444361

民間航空飛行訓練およびシミュレーション:市場シェア分析、業界動向と統計、成長予測(2024~2031年)Civil Aviation Flight Training And Simulation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2031) |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| 民間航空飛行訓練およびシミュレーション:市場シェア分析、業界動向と統計、成長予測(2024~2031年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 230 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

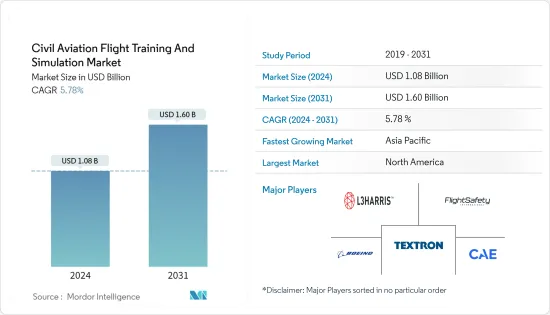

民間航空飛行訓練およびシミュレーション市場規模は、2024年に10億8,000万米ドルと推定され、2031年までに16億米ドルに達すると予測されており、予測期間(2024年から2031年)中に5.78%のCAGRで成長します。

主なハイライト

- COVID-19のパンデミック中、世界中で渡航制限が課され、収益源が減少し、航空機の大部分が運航停止になったため、民間航空業界は前例のない低迷を経験しました。この状況は、パンデミック下で航空会社が事業を存続させるのに苦労する中、航空業界全体で注文の延期と広範囲にわたる一時解雇をもたらしました。しかし、民間航空部門の回復に伴い、パイロットの需要も急速に増加しました。

- 深刻なパイロット不足があるという事実により、予測期間中に新しいパイロットの需要が市場を牽引すると予想されます。民間航空シミュレーション市場はパイロット訓練プログラムに不可欠な部分であり、航空業界で重要な役割を果たしています。フライトシミュレーターは、パイロットに現実的な訓練環境を提供し、航空機を安全に操作するために必要なスキルを習得し、維持できるようにします。

- これらのシミュレーターは、さまざまなシナリオ、気象条件、緊急事態を含む、実際の航空機の操縦体験を再現します。世界の航空交通量の増加とそれに伴う熟練したパイロットの必要性により、航空シミュレーターの需要が高まっています。航空会社と飛行訓練アカデミーは、パイロットを効率的、コスト効率よく、安全に訓練するためにシミュレーターを利用しています。

フライトシミュレータ市場動向

固定翼航空機セグメントが予測期間中に市場を独占すると予測される

- 航空機のタイプ別では、固定翼セグメントが最大の市場シェアを保持し、予測期間中もその支配を継続しました。民間航空と一般航空の両方で新しい航空機を調達したため、長年にわたってパイロット不足が生じていました。パンデミックの影響でパイロットの需要は減少しましたが、民間航空機パイロットの長期的な需要は依然として強いです。

- ボーイングの2022年版パイロット&技術者の見通しによると、世界のパイロット需要は今後数十年間で約60万2,000人と予測されています。パイロットの需要により、世界中でいくつかの飛行訓練機関の設立が促進され、飛行シミュレーションと訓練機器を調達して、航空志望者に認定訓練サービスを提供しています。

- COVID-19のパンデミックにより、2020年と2021年にパイロットの一時帰休が発生したが、航空会社は現在、長期的な成長戦略に注力しており、パイロット向けの航空会社特有の訓練を受けるためにパイロット訓練学校との協力を再開しています。

- たとえば、2022年7月、エアカリン(ニューカレドニア)は、A320およびA330のパイロットに運航乗務員の訓練を提供するエアバス・アジア・トレーニング・センター(AATC)との契約を締結しました。このような開発は、予測期間中に焦点を当てている市場の固定翼航空機セグメントの成長見通しを強化すると想定されています。

予測期間中に北米が市場を独占すると予想される

北米地域は、主に米国の大規模な航空市場により最大の市場シェアを保持しました。この国の航空旅客数は過去10年間で急速に増加しており、航空会社は機材の規模や新しい路線の拡大の必要性も生じています。アメリカン航空、デルタ航空、ユナイテッド航空は、米国の3大国内航空会社です。 2023年1月現在、アメリカン航空はエアバスとボーイングの933機の航空機を擁する世界最大の商用フリートを運航しており、さらに161機が発注されています。さらに、労働統計局によると、2021年に航空会社および民間パイロットの雇用者数は135,300人でした。また、その数は今後10年間で6%増加すると予測されており、これは年間18,000人以上の新規雇用に相当します。

COVID-19のパンデミックにより、過去2年間でこの地域ではパイロットの一時帰休が発生したが、予測期間の後半にはこの地域でのパイロットに対する大きな需要が予想されます。自主的な出発、機材の変更、国内旅行需要の急増により、今後数年間でパイロット訓練の需要が大幅に増加しました。そのため、いくつかの航空会社はパイロットの訓練能力を高めるための措置を講じています。アメリカン航空、ユナイテッド航空、デルタ航空などの航空会社は、パイロットができるだけ早く運航に復帰できるよう、パイロットの訓練を強化していると報告しました。このような発展は、民間航空飛行訓練およびシミュレーション市場の成長を促進すると予想されます。

フライトシミュレータ業界の概要

民間航空飛行訓練およびシミュレーション市場は、適度に細分化されています。 CAE Inc.は、主にその巨大な地理的存在とブランドイメージにより市場リーダーです。 L3Harris Technologies Inc.、TRU Simulation+Training Inc.、FlightSafety International Inc.、およびThe Boing Companyも、市場の著名なプレーヤーの一部です。シミュレーションおよびトレーニングのプロバイダーと機器メーカーは、ブランドの評判を確立し、より多くの顧客を引き付けるために地理的に極端な地域に手を伸ばすことに常に努力しています。

航空学校は、長期間にわたって持続可能な収益を得るのに役立つ可能性のあるパイロット訓練プログラムについて、航空会社や航空機運航者との長期的な協力関係を模索しています。新しい航空機モデルをサポートするために再構成またはアップグレードできるシミュレーターの需要が高まっており、そのようなシミュレーターの製造に重点が置かれることで、予測期間中のプレーヤーの成長が促進されるでしょう。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 バリューチェーン分析- 定性的分析

第6章 市場セグメンテーション

- シミュレータタイプ別

- フルフライトシミュレーター(FFS)

- 飛行訓練装置(FDS)

- その他のトレーニングタイプ

- 航空機タイプ別

- 固定翼

- 回転翼

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- その他ラテンアメリカ

- 中東とアフリカ

- アラブ首長国連邦

- サウジアラビア

- その他中東およびアフリカ

- 北米

第7章 競合情勢

- ベンダーの市場シェア

- 企業プロファイル

- CAE Inc.

- FlightSafety International Inc.

- L3Harris Technologies, Inc.

- TRU Simulation+Training Inc.(Textron Inc.)

- The Boeing Company

- Frasca International, Inc.

- ALSIM EMEA

- Raytheon Technologies Corporation

- Airbus SE

- Simcom Aviation Training

- Pureflight Aviation Training

- FAAC Inc.

- Avion Group

第8章 市場機会と将来の動向

The Civil Aviation Flight Training And Simulation Market size is estimated at USD 1.08 billion in 2024, and is expected to reach USD 1.60 billion by 2031, growing at a CAGR of 5.78% during the forecast period (2024-2031).

Key Highlights

- The commercial aviation industry witnessed an unprecedented downturn during the COVID-19 pandemic as travel restrictions were imposed globally, causing revenue streams to decline and leading to the grounding of a significant portion of the fleet. This situation resulted in the deferral of orders and widespread layoffs throughout the aviation sector as airlines struggled to stay afloat during the pandemic. However, with the recovery of the commercial aviation sector, the demand for pilots also experienced rapid growth.

- Due to the fact that there is a severe pilot shortage, the demand for new pilots is expected to drive the market during the forecast period. The civil aviation simulation market is an integral part of pilot training programs and plays a crucial role in the aviation industry. Flight simulators provide a realistic training environment for pilots, allowing them to acquire and maintain the necessary skills to safely operate aircraft.

- These simulators replicate the experience of flying an actual aircraft, including various scenarios, weather conditions, and emergency situations. The growing global air traffic and the subsequent need for skilled pilots are driving the demand for aviation simulators. Airlines and flight training academies rely on simulators to train their pilots efficiently, cost-effectively, and safely.

Flight Simulator Market Trends

Fixed-wing Aircraft Segment is Projected to Dominate the Market During the Forecast Period

- By aircraft type, the fixed-wing segment held the largest market share and continued its domination during the forecast period. The procurement of new aircraft for both commercial and general aviation created a pilot shortage over the years. Although the pandemic has resulted in a drop in pilot demand, the long-term demand for commercial aircraft pilots remains strong.

- As per Boeing's 2022 edition of the Pilot & Technician Outlook, the global demand for pilots is projected to be around 602,000 during the next couple of decades. The demand for pilots fostered the establishment of several flight training institutes across the world, which procure flight simulation and training equipment to provide certified training services to aviation aspirants.

- Though the COVID-19 pandemic resulted in pilot furloughing in 2020 and 2021, airlines are now focusing on long-term growth strategies and have re-started collaborating with pilot training schools to obtain airline-specific training for pilots.

- For instance, in July 2022, Aircalin (New Caledonia) secured a contract with Airbus Asia Training Centre (AATC) to provide flight crew training for its A320 and A330 pilots. Such developments are envisioned to bolster the growth prospects of the fixed-wing aircraft segment of the market in focus during the forecast period.

North America is Expected to Dominate the Market During the Forecast Period

The North American region held the largest market share mainly due to a large aviation market in the US. Air passenger traffic in the country increased at a rapid pace in the past decade, which has also generated the need for airlines to expand in terms of fleet size and new routes. American Airlines, Delta Airlines, and United Airlines are the three largest domestic airlines in the US. As of January 2023, American Airlines operates the largest commercial fleet in the world with 933 aircraft from both Airbus and Boeing, with an additional 161 on order. Furthermore, according to the Bureau of Labor Statistics, there were 135,300 airline and commercial pilots employed in 2021. Also, it projects that the number is expected to grow by 6% over the next decade, translating to more than 18,000 new hires annually.

Though the COVID-19 pandemic has resulted in furloughing of pilots in the region in the last two years, a great demand for pilots in the region is anticipated in the latter half of the forecast period. Voluntary departures, fleet modifications, and the rapid rise in domestic travel demand created a significant demand upsurge for pilot training in the upcoming years. Hence, several airlines have taken measures to increase their pilot training capabilities. Airlines like American Airlines, United Airlines, and Delta Air Lines have reported that they have ramped up the pilot training to help pilots return to service as quickly as possible. Such developments are anticipated to drive the growth of the civil aviation flight training and simulation market.

Flight Simulator Industry Overview

The civil aviation flight training and simulation market is moderately fragmented. CAE Inc. is the market leader mainly due to its huge geographical presence and brand image. L3Harris Technologies Inc., TRU Simulation + Training Inc., FlightSafety International Inc., and The Boeing Company are also some of the other prominent players in the market. Simulation and training providers and equipment manufacturers constantly strive to build brand reputation and reach out to geographic extremes to attract more customers.

Flight schools are looking for long-term collaborations with airlines and aircraft operators for pilot training programs, which may help them make sustainable revenues for longer durations. There is a growing demand for simulators that can be re-configured or possibly upgraded to support newer aircraft models, and the focus on manufacturing such simulators will drive the growth of the players during the forecast period.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 Value Chain Analysis- A Qualitative Analysis

6 MARKET SEGMENTATION

- 6.1 By Simulator Type

- 6.1.1 Full Flight Simulator (FFS)

- 6.1.2 Flight Training Devices (FDS)

- 6.1.3 Other Training Types

- 6.2 By Aircraft Type

- 6.2.1 Fixed-wing

- 6.2.2 Rotory-wing

- 6.3 Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Italy

- 6.3.2.5 Rest of Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 China

- 6.3.3.2 India

- 6.3.3.3 Japan

- 6.3.3.4 South Korea

- 6.3.3.5 Rest of Asia-Pacific

- 6.3.4 Latin America

- 6.3.4.1 Brazil

- 6.3.4.2 Rest of Latin America

- 6.3.5 Middle-East and Africa

- 6.3.5.1 United Arab Emirates

- 6.3.5.2 Saudi Arabia

- 6.3.5.3 Rest of Middle-East and Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Vendor Market Share

- 7.2 Company Profiles

- 7.2.1 CAE Inc.

- 7.2.2 FlightSafety International Inc.

- 7.2.3 L3Harris Technologies, Inc.

- 7.2.4 TRU Simulation + Training Inc. (Textron Inc.)

- 7.2.5 The Boeing Company

- 7.2.6 Frasca International, Inc.

- 7.2.7 ALSIM EMEA

- 7.2.8 Raytheon Technologies Corporation

- 7.2.9 Airbus SE

- 7.2.10 Simcom Aviation Training

- 7.2.11 Pureflight Aviation Training

- 7.2.12 FAAC Inc.

- 7.2.13 Avion Group