|

市場調査レポート

商品コード

1441674

血行動態モニタリング:世界市場シェア分析、業界動向と統計、成長予測(2024~2029年)Global Hemodynamic Monitoring - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| 血行動態モニタリング:世界市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 118 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

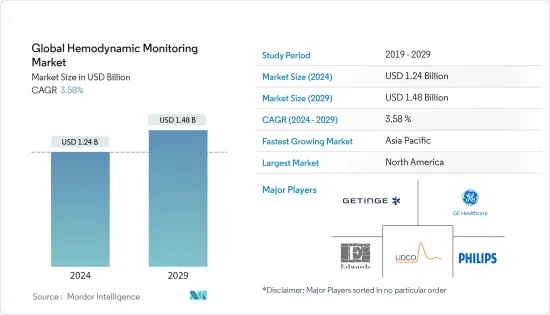

世界の血行動態モニタリング市場規模は、2024年に12億4,000万米ドルと推定され、2029年までに14億8,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に3.58%のCAGRで成長します。

COVID-19は市場に大きな影響を与えています。 LiDCO Group PLCの2020年の年次報告書によると、血行動態モニタリング機器の需要は多くの既存顧客から増加しており、英国の病院からの需要が短期的に大幅に高まり、武漢で販売された少数のモニターを含む他のいくつかの国でも需要が増加しています。さらに、一部のCOVID-19患者は敗血症などの合併症を発症し、集中治療が必要となりますが、高度な血行動態モニタリングを使用することで患者の転帰が改善されるという強力な臨床証拠があります。したがって、パンデミックが終息するまで、この製品に対する需要もさらに高まる可能性があります。

この市場の成長を推進する主な要因は、重篤な高齢者の症例数の増加、心疾患と糖尿病の有病率の増加、在宅ベースの非侵襲的モニタリングシステムに対する需要の増加、および医療機器の増加です。高血圧に苦しむ人の数。世界保健機関の2021年の事実によると、世界中の30~79歳の成人 12億8,000万人が高血圧であると推定されています。同情報源によると、心血管疾患(CVD)は世界の主な死因であり、毎年推定1,790万人の命を奪い、全世界の死亡者数の推定32%に相当します。したがって、心疾患と高血圧の有病率は市場の成長を促進する可能性があります。

血行動態モニタリングの新しい技術は、血行動態的変化とその原因を検出し、組織への酸素供給などの血行動態的状態を最適化するために使用できる正確で再現性のある測定を提供するため、術後のケアと麻酔中の心臓血管患者の管理を進歩させる可能性があります。治療介入の適切性についてフィードバックを提供します。心臓の前負荷や体液反応性などの要件を評価するための静的変数から動的変数への移行、および低侵襲的または非侵襲的モニタリング技術への変化も市場の成長を推進しています。

したがって、市場は予測期間中に成長を示すと予想されます。ただし、侵襲的モニタリングシステムに関連する合併症の発生率の増加と、新しいシステムの承認に関する厳格なFDAガイドラインが市場の成長を妨げる可能性があります。

血行動態モニタリングデバイスの市場動向

低侵襲的モニタリングシステムは、予測期間中に高い市場シェアを維持すると予想される

市場のシステムセグメントでは、低侵襲的モニタリングシステムが最大の市場規模を持つと考えられており、予測期間中に大幅な成長が見込まれると予想されます。

低侵襲的システムは、ストローク量を継続的に追跡し、流体の反応性に関する動的な情報を提供するのに役立ちます。一部のシステムは容積の事前負荷変数を評価しますが、他のシステムは独自のカテーテルを使用した中心静脈飽和度の連続測定に重点を置いています。低侵襲的処置と心拍出量のこれらの変数により、血行動態モニタリングが改善されます。

最近、小型プローブを備えた経食道心エコー装置として知られる心エコー装置が進歩しており、現在では継続的な血行動態的評価に使用されています。これらのモニタリングシステムにより血行動態の計算が容易になり、医療従事者の注目を集め、その結果市場が成長しました。

したがって、上記の要因により、市場セグメントは予測期間中に成長を示すと予想されます。

北米が市場を独占しており、予測期間中も同様に推移すると予想される

現在、北米は血行動態モニタリング市場を独占しており、今後数年間はその牙城を維持すると予想されています。米国は世界の血行動態モニタリング市場で最大のシェアを占めています。米国の血行動態モニタリング市場の成長は、主要な市場プレーヤー、技術的に先進的な病院、および地域の病院で治療を受ける重症患者の増加により、最も注目に値します。

Edwards Lifesciences Corporationの年次報告書によると、2020年に米国で同社の圧力監視製品の需要が増加し、この傾向は第4四半期まで続きました。 2021年には、病院の設備投資が引き続き改善し、米国でのCOVID-19による入院が増加したため、圧力モニタリングの需要が増加しました。

さらに、米国食品医薬品局(FDA)によるモニタリング装置の承認の増加と米国の血行動態モニタリング市場での新製品の発売により、予測期間中に成長すると予想されます。たとえば、2021年 9月に、Caretaker Medicalは、血圧および血行動態患者モニタリングシステムVitalStreamのFDA認可を取得しました。また、2021年 3月、ミシガン州に本拠を置くリアルタイム臨床分析会社Fifth Eyeは、食品医薬品局が同社の血行動態不安定性分析(AHI)ツールに対してDE Novo分類を付与したと発表しました。

したがって、上記の要因により、北米地域の市場は予測期間中に成長を示すと予想されます。

血行動態モニタリングデバイス業界の概要

血行動態モニタリング市場は競争が激しく、複数の主要企業で構成されています。市場シェアの観点から見ると、現在市場を独占している有力な企業はほとんどありません。しかし、技術の進歩と製品の革新に伴い、中規模から中小企業はより低価格の新しいデバイスを導入することで市場での存在感を高めています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 重症高齢者人口の増加

- 心疾患と糖尿病の有病率の増加

- 技術の進歩

- 市場抑制要因

- 侵襲的モニタリングシステムに関連した合併症の発生率の増加

- 新しいシステムの承認に関する厳格なFDAガイドライン

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- システム別

- 低侵襲的

- 侵襲的

- 非侵襲的

- 用途別

- 研究室ベース

- 在宅ベース

- 病院ベース

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東とアフリカ

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- LiDCO Group PLC

- Baxter(Cheetah Medical Inc.)

- ICU Medical Inc.

- Tensys Medical Inc.

- Schwarzer Cardiotek GmbH

- Koninklijke Philips NV

- Edwards Lifesciences Corporation

- Getinge Group

- GE Healthcare

- Draeger Medical

- Masimo

- Smiths Medical

- Change Healthcare

- Deltex Medical, SC

第7章 市場機会と将来の動向

The Global Hemodynamic Monitoring Market size is estimated at USD 1.24 billion in 2024, and is expected to reach USD 1.48 billion by 2029, growing at a CAGR of 3.58% during the forecast period (2024-2029).

COVID-19 has a substantial market impact. According to the LiDCO Group PLC's annual report for 2020, demand for hemodynamic monitoring equipment has increased from many existing customers, with significant short-term heightened demand from UK hospitals and increased demand in several other countries, including a small number of monitors sold in Wuhan, China. Furthermore, some COVID-19 patients develop complications such as sepsis and require intensive care, and there is strong clinical evidence that using advanced hemodynamic monitoring improves patient outcomes. Hence, this is also likely to create more demand for the products till the pandemic ends.

The key factors propelling the growth of this market are an increase in the number of critically ill geriatric cases, a rise in the prevalence of cardiac disorders and diabetes, increasing demand for home-based and non-invasive monitoring systems, and an increase in the number of people suffering from hypertension. As per the World Health Organization's Fact of 2021, an estimated 1.28 billion adults aged 30-79 years worldwide have hypertension. As per the same source, Cardiovascular diseases (CVDs) are the leading cause of death globally, taking an estimated 17.9 million lives each year, an estimated 32% of all the deaths worldwide. Hence the prevalence of cardiac disorders and hypertension will likely boost the market growth.

New techniques of hemodynamic monitoring have the potential to advance the management of the cardiovascular patient during postoperative care and anesthesia as they provide accurate and repeatable measurements that can be used to detect hemodynamic alterations and their causes, optimize hemodynamic conditions such as oxygen delivery to the tissues, and provide feedback on the adequacy of therapeutic interventions. The transition from static to dynamic variables to assess requirements such as cardiac preload and fluid responsiveness, as well as the change to less invasive or noninvasive monitoring techniques, are also driving the market growth.

Thus, the market is expected to show growth over the forecast period. However, Increasing incidences of complications associated with an invasive monitoring system and stringent FDA guidelines for approval of new systems may hinder the growth of the market.

Hemodynamic Monitoring Devices Market Trends

Minimally Invasive Monitoring Systems is Expected to Hold High Market Share Over the Forecast Period

In the system segment of the market, minimally invasive monitoring systems are believed to have the largest market size and are expected to witness significant growth during the forecast period.

The minimally invasive systems help track stroke volume continuously and offer dynamic information on fluid responsiveness. Some systems assess volumetric preload variables, while others highlight the continuous measurement of central venous saturation with proprietary catheters. These variables of minimally invasive procedures and cardiac output deliver improved hemodynamic monitoring.

There is a recent advancement in echocardiography devices known as a transesophageal echocardiography device with a miniaturized probe, which is now used for continuous hemodynamic assessment. These monitoring systems have made hemodynamic calculations easier, gaining healthcare providers' attention, thus, resulting in the market's growth. Additionally, the market players for reaching out large population base are timely participating in various health conferences. For Instance, in January 2022, At Arab Health 2022, Masimo demonstrated how different solutions from the company can work together across the patient journey - from the hospital to the home and anywhere care is provided - to help care teams enhance care consistency and improve patient outcomes. The company shoed its non-invasive monitoring solutions.

Thus, owing to the abovementioned factors, the market segment is expected to show growth over the forecast period.

North America Dominates the Market and Expected to do the Same Over the Forecast Period

North America currently dominates the market for hemodynamic monitoring and is expected to continue its stronghold for a few more years. The United States holds the largest share of the global hemodynamic monitoring market. The growth of the United States hemodynamic monitoring market is the most notable, owing to significant market players, technologically advanced hospitals, and an increasing number of critically ill patients being treated in the region's hospitals.

According to Edwards Lifesciences Corporation's annual report, demand for its pressure monitoring products increased in the United States in 2020, and this trend continued through the fourth quarter. In 2021, as hospital capital spending continued to improve and COVID hospitalizations in the United States increased, there was an increase in demand for pressure monitoring.

Moreover, with increasing United States Food and Drug Administration (FDA) approvals for monitoring devices and new product launches in the United States hemodynamic monitoring market is expected to grow during the forecast period. For instance, in September 2021, Caretaker Medical landed FDA clearance for its blood pressure and hemodynamic patient monitoring system VitalStream. Also, in March 2021, Fifth Eye, a Michigan-based real-time clinical analytics company, announced that the Food and Drug Administration had granted DE Novo classification for its Analytic for Hemodynamic Instability (AHI) tool.

Thus, owing to the abovementioned factors, the market in the North American region is expected to show growth over the forecast period.

Hemodynamic Monitoring Devices Industry Overview

The hemodynamic monitoring market is highly competitive and consists of several major players. In terms of market share, few significant players currently dominate the market. However, with technological advancements and product innovations, mid-size to smaller companies are increasing their market presence by introducing new devices with fewer prices. Companies like Getinge Group, Koninklijke Philips NV, Edwards Life Sciences Corporation, GE Healthcare, and LiDCO Group hold substantial shares in the market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Critically Ill Geriatric Population

- 4.2.2 Rise in the Prevalence of Cardiac Disorders and Diabetes

- 4.2.3 Technological Advanements

- 4.3 Market Restraints

- 4.3.1 Increasing Incidences of Complications Associated with Invasive Monitoring Systems

- 4.3.2 Stringent FDA Guidelines for Approval of New Systems

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By System

- 5.1.1 Minimally Invasive Monitoring Systems

- 5.1.2 Invasive Monitoring Systems

- 5.1.3 Non-invasive Monitoring Systems

- 5.2 By Application

- 5.2.1 Laboratory-based Monitoring Systems

- 5.2.2 Home-based Monitoring Systems

- 5.2.3 Hospital-based Monitoring Systems

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle-East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 LiDCO Group PLC

- 6.1.2 Baxter (Cheetah Medical Inc.)

- 6.1.3 ICU Medical Inc.

- 6.1.4 Tensys Medical Inc.

- 6.1.5 Schwarzer Cardiotek GmbH

- 6.1.6 Koninklijke Philips NV

- 6.1.7 Edwards Lifesciences Corporation

- 6.1.8 Getinge Group

- 6.1.9 GE Healthcare

- 6.1.10 Draeger Medical

- 6.1.11 Masimo

- 6.1.12 Smiths Medical

- 6.1.13 Change Healthcare

- 6.1.14 Deltex Medical, SC