|

市場調査レポート

商品コード

1443890

マネージドセキュリティサービス:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Managed Security Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| マネージドセキュリティサービス:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 117 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

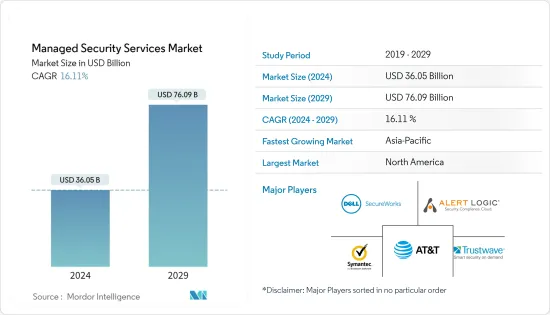

マネージドセキュリティサービス市場規模は、2024年に360億5,000万米ドルと推定され、2029年までに760億9,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に16.11%のCAGRで成長します。

COVID-19の発生は、マネージドセキュリティサービスの市場シェアの成長にプラスの影響を与えると予想されます。これは、COVID-19の到来により、マネージドセキュリティサービスを使用することで、企業がセキュリティの問題に対処し、リモート勤務中の安全な情報アクセスを促進できると考えられているためです。パンデミック後、恒久的な在宅勤務やデジタル化の進展により市場は急速に成長しています。

主なハイライト

- コンピューティングにおけるマネージドセキュリティサービスは、サービスプロバイダーにアウトソーシングされたネットワークセキュリティサービスです。多くの組織は、社内に必要な専門知識やスタッフを持たないため、マネージドセキュリティサービスプロバイダー(MSSP)を雇用してセキュリティ監視を行っています。セキュリティ監視インフラストラクチャの維持は複雑であり、資格のあるスタッフが継続的に評価して対応する必要があります。

- さらに、過度に複雑または拡張的なアーキテクチャ、または異種システムでの特定の実装ニーズのためにカスタムセキュリティの展開を必要とする組織は、このようなサービスから大きなメリットを得ることができます。さらに、動的なリソース割り当てに依存している組織は、一般に、効果的に動作する動的な環境を監視するためのより優れた自動化を必要とします。このような複雑な自動化のニーズは、AT&T、Verizon、IBM、SecureWorksなどの企業が提供するサービスによって管理できます。

- HIPAAによると、米国のヘルスケア分野における上位3つのデータ侵害により、AccudocSolutions、UnityPoint Health、テキサス州従業員退職制度などの組織を含む、合わせて520万件以上の患者記録が失われています。

- 今日、世界はこれまで以上にデジタルでつながっています。サイバー犯罪者は、このオンライン変革を利用して、オンラインシステム、ネットワーク、インフラストラクチャの弱点を狙います。世界中の政府、企業、個人に多大な経済的および社会的影響があります。フィッシング、ランサムウェア、データ侵害は現在のサイバー脅威のほんの一例にすぎませんが、新しい種類のサイバー犯罪も常に出現しています。サイバー犯罪者はますます機敏かつ組織化されており、新しいテクノロジーを悪用し、攻撃を調整し、新しい方法で協力しています。 FBIのインターネット犯罪報告書2021によると、2021年に一般からFBIに報告されたサイバー犯罪の苦情は847,376件で、2020年から7%増加しました。

- サイバー脅威の複雑化により、組織のセキュリティ運用の1つまたは複数をアウトソーシングする傾向が強まっています。社内のセキュリティオペレーションセンター(SOC)と外部委託のセキュリティオペレーションセンター(SOC)のどちらを選択するかを決定する場合、多くの要素を考慮する必要があります。ビジネスシステムに侵入した悪意のあるコードがビジネス全体を破壊する可能性があるため、正しい選択は重大な結果をもたらす可能性があります。

マネージドセキュリティサービス市場動向

市場を独占するためのクラウド展開

- デジタル変革の渦中にある企業が、オンプレミスのITインフラストラクチャをアップグレードし、業務の一部をクラウドに移行するという避けられない、しかし困難な作業に取り組む中、IT意思決定者は通常、規制遵守、セキュリティ、リスク軽減に関する問題に直面しています。熟練したITプロフェッショナルの人材が不足していることと、最新のツール、テクノロジー、実践方法を常に最新の状態に保つことができないことが、こうした企業の懸念をさらに悪化させています。ネットワークとデータのセキュリティの脅威が増大している場合、マネージドセキュリティサービスプロバイダー(MSSP)は、クラウド構成、リスク軽減、規制順守に立ち向かう企業を支援する可能性があります。

- クラウドに導入されたマネージドセキュリティサービスは、柔軟性と拡張性に優れています。さらに、サービスプロバイダーは、クラウド環境内の問題にアクセスし、監視し、リモートで修復することもできます。継続的な監視により、問題を迅速かつ効率的に解決できます。クラウドベースのマネージドセキュリティサービスへの移行は、AI/ML、ビッグデータ分析、脅威インテリジェンス、高度な自動化プラットフォームなどの新興テクノロジーの普及拡大によっても促進されています。いくつかの市場関係者は、業界の進化する要件に応えるため、イノベーションとコラボレーションを通じて包括的なサービスを開始しています。

- 2021年 8月、Amazon Web Servicesはマネージドセキュリティサービスプロバイダー(MSSP)向けの新しいパートナーコンピテンシーを開始し、そのクラウドソフトウェアソリューションとサービスをAWSマーケットプレースで利用できるようにしました。 AWSが1年間試験的に実施してきたAWSレベル1 MSSPコンピテンシーは、重要なAWSリソースのセキュリティイベントを保護、監視、対応するマネージドセキュリティサービスの新しいベースライン標準を作成し、フルマネージドサービスとして顧客に提供します。同社によれば、この新しいコンピテンシーは、パートナーが混雑したセキュリティ市場で差別化できるようにし、顧客がサービスを調達しやすくすることを目的としているといいます。

- さらに2021年7月、Tech Mahindraはサイバーセキュリティ企業Palo Alto Networksとのマネージドセキュリティサービスプロバイダー(MSSP)提携を発表しました。この合意により、Tech Mahindraと米国に本拠を置く多国籍企業との世界パートナーシップが拡大し、マネージドセキュリティサービスの完全なスイートを提供することになりました。 MSSPとして、Tech Mahindraは、リスク評価、体制管理、ワークロード保護、オーケストレーションなどの付加価値サービスを含む、ネットワーク、エンドポイント、クラウドセキュリティの完全な可視化と制御を同社の顧客に提供します。

- さらに、2021年 7月にTelusは、Palo Alto NetworksのPrisma Accessテクノロジーに基づく新しいマネージドクラウドセキュリティソリューションを発表し、カナダの企業がどこからでもデータやアプリに安全にアクセスできるようにしました。さらに、ネットワークのセキュリティと保護を確保するために、新しいマネージドクラウドセキュリティソリューションは、ファイアウォールサービス、脅威防御、マルウェア防御、URLフィルタリング、SSL復号化、およびアプリケーションベースのポリシーを提供します。また、消費者はTelus SD-WANサービスに接続してSASEを使用できるようになります。

アジア太平洋が最も急速な成長を遂げる

- デジタル変革はこの地域における最優先事項となっています。より多くの企業が自社の取り組みをサポートする正式な戦略を導入し、市場の需要を促進するにつれて、この技術は急速に普及しています。

- 企業のITリソースに対してアウトソーシングされたマネージドサービスを活用することは、大幅な予算の節約、より回復力のあるコンピューティング能力、より安全なネットワークの稼働時間とパフォーマンスを確保する方法となります。 China Telecom Americas Corporationは、ジュニパー、マイクロソフト、シスコ、FSNetworks、IBM、VMware、ファーウェイなどの主要ベンダーと提携して、完全なターンキーのプロフェッショナルICTサービスを世界 72か国で提供しています。

- ITランサムウェア攻撃、DDoS攻撃、データ漏洩など、この地域におけるサイバーセキュリティへの脅威の増大や、注目を集めるサイバー攻撃のメディア報道の増加により、国内の組織はマネージドセキュリティサービスの導入を余儀なくされています。さらに、従来の産業は、デジタル変革を受け入れ、ITテクノロジーの導入を強化する政策によってサポートされています。したがって、インターネットデータセンターサービスに対する需要も高まっており、市場の成長をさらに推進しています。

- AI、5G、IoT、仮想現実の急速な発展、およびこれらの新技術の商用利用に伴い、データ処理と情報対話の需要が増大しており、これにより、この地域でのデータセンターの建設が加速し、業界の爆発的な成長が見込まれています。

- インドでは、組織情報の完全性、機密性、入手可能性に対する脅威が急激に増加しているため、ビジネスリスクアプローチに基づいて、情報セキュリティの確立、実装、運用、監視、レビュー、保守、およびセキュリティの標準化されたモデルを提供することに重点が置かれています。顧客の全体的な情報セキュリティを向上させます。

- 2022年 2月、IBMは、アジア太平洋(APAC)地域の企業がサイバー攻撃の増大する危険に備え、管理できるよう支援するためのリソースへの投資を発表しました。この地域初となる新しいIBM Security Command Centerでは、経営幹部から技術担当者に至るまでの全員が準備できるよう、非常に現実的なシミュレートされたサイバー攻撃を使用してサイバーセキュリティ対応戦略を教育することが期待されています。この投資には、新しいセキュリティオペレーションセンター(SOC)も含まれています。これは、IBMの現在の世界SOCネットワークの一部となる可能性があり、24時間年中無休で世界中の顧客にセキュリティ対応サービスを提供します。

マネージドセキュリティサービス業界の概要

マネージドセキュリティサービス市場は、ネットワーク攻撃、サービス妨害、さらにはリスク評価の実行などの攻撃から企業を防ぐためのセキュリティサービスを提供する既存の大手企業と多くの今後のベンダーによって細分化されています。組織が戦略的に投資を続けるにつれて、この市場では多くの提携、合併、サービスの立ち上げ、買収が行われることが予想されます。

- 2022年 4月- アプリケーションホスティングと仮想デスクトップの世界クラウドサービスプロバイダーであるAce Cloud Hosting(ACE)は、マネージドセキュリティサービス(MSS)の開始を発表しました。さらに、アクセンチュアはセキュリティサービスに柔軟性を組み込むためにシマンテックのサイバーセキュリティサービス事業を買収しました。さらに、VerizonはBlackberry CylanceのAIベースのウイルス対策ソリューションをセキュリティサービスポートフォリオに統合しました。この統合は、AIベースのサイバーセキュリティソリューションに対する需要の高まりを示しています。これらの発展はどちらも、市場がもたらす成長の可能性を強調しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 消費者の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場力学

- 市場促進要因

- サイバー犯罪の増加、デジタル破壊、コンプライアンス要求の増大

- 市場の成長を促進する早期段階での脅威の検出とインテリジェンスの必要性

- 市場抑制要因

- セキュリティサービスに対する認知度の欠如が市場拡大を抑制

- MSSP分野の進化と主要な動向

- COVID-19の市場への影響の評価

第6章 市場セグメンテーション

- 展開タイプ別

- オンプレミス

- クラウド

- ソリューションの種類別

- 侵入の検出と防止

- 脅威の防止

- 分散型サービス妨害

- ファイアウォール管理

- エンドポイントセキュリティ

- リスクアセスメント

- マネージドセキュリティサービスプロバイダー別

- ITサービスプロバイダー

- マネージドセキュリティスペシャリスト

- テレコムサービスプロバイダー

- エンドユーザー別業種別

- BFSI

- 政府と防衛

- 小売り

- 製造業

- ヘルスケアとライフサイエンス

- ITとテレコム

- その他のエンドユーザー分野

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東とアフリカ

第7章 競合情勢

- 企業プロファイル

- AT&T Inc.

- Secureworks Inc.(Dell Technologies Inc.)

- Symantec(Broadcom Inc.)

- Trustwave Holdings Inc.

- Alert Logic

- IBM Corporation.

- Verizon

- CenturyLink

- BAE Systems

- AtoS

- Capgemini

- Wipro

- Fujitsu

第8章 ベンダーのポジショニング分析

第9章 投資分析と市場展望

The Managed Security Services Market size is estimated at USD 36.05 billion in 2024, and is expected to reach USD 76.09 billion by 2029, growing at a CAGR of 16.11% during the forecast period (2024-2029).

The COVID-19 outbreak is expected to impact the growth of managed security services market share positively. This is because, with the arrival of COVID-19, the use of managed security services is believed to enable enterprises to address security issues and facilitate secure information access while remote working. After the pandemic, the market is growing rapidly due to permanent work-from-home jobs and increased digitalization.

Key Highlights

- Managed security services in computing are network security services outsourced to any service provider. Many organizations hire managed security service providers (MSSPs) to undertake security monitoring, as they do not have the necessary expertise or staff in-house. Maintaining any security monitoring infrastructure is complex and requires qualified staff to assess and respond continually.

- Moreover, organizations requiring custom security deployments due to overly complex or expansive architecture or specific implementation needs with disparate systems can significantly benefit from such services. Additionally, organizations relying on dynamic resource allocation generally require better automation to monitor the dynamic environments in which they operate effectively. Such complex automation needs can be managed by the services offered by players like AT&T, Verizon, IBM, and SecureWorks.

- According to HIPAA, the top three data breaches in the healthcare sector in the United States witnessed a combined loss of more than 5.2 million patient records, including organizations like AccudocSolutions, UnityPoint Health, and the Employees' Retirement System of Texas.

- Today, the world is more digitally connected than ever before. Cybercriminals use this online transformation to target online systems, networks, and infrastructure weaknesses. There is a massive economic and social impact on governments, businesses, and individuals worldwide. Phishing, ransomware, and data breaches are just a few examples of current cyber threats, while new types of cybercrime are always emerging. Cybercriminals are increasingly agile and organized - exploiting new technologies, tailoring their attacks, and cooperating in new ways. According to the FBI's Internet Crime Report 2021, 847,376 complaints of cybercrime were reported to the FBI by the public in 2021, a 7% increase from 2020.

- The increasing complexity of cyber threats has driven the trend toward outsourcing one or more of an organization's security operations. When deciding between an internal and an outsourced Security Operations Center (SOC), many factors must be considered. The right choice may have critical consequences, as malicious code infiltrating a business system can now destroy an entire business.

Managed Security Services Market Trends

Cloud Deployment to Dominate the Market

- IT decision-makers are typically confronted with issues surrounding regulatory compliance, security, and risk reduction as businesses in the throes of digital transformation undertake the inevitable yet daunting task of upgrading their on-premises IT infrastructure and moving some of their operations to the cloud. The shortage of skilled IT professionals on staff and the inability to stay updated with the recent tools, technologies, and practices exacerbates these corporate concerns. When network and data security threats are rising, managed security service providers (MSSPs) may help overwhelmed enterprises confront cloud configuration, risk reduction, and regulatory compliance.

- The cloud-deployed managed security services are flexible and scalable. Furthermore, it enables the service provider to access, monitor, and even remotely repair any issues within the cloud environment. Continual monitoring ensures the quick and efficient resolution of problems. The shift to cloud-based managed security services is also aided by the increasing penetration of emerging technologies such as AI/ML, big data analytics, threat intelligence, and advanced automation platforms. Several market players are launching comprehensive services through innovation and collaboration to cater to the industry's evolving requirements.

- In August 2021, Amazon Web Services launched a new partner competency for managed security service providers (MSSPs) and made their cloud software solutions and services available in the AWS Marketplace. The AWS Level 1 MSSP Competency, which AWS has been piloting for a year, creates a new baseline standard for managed security services that protect, monitor, and respond to security events of essential AWS resources and are delivered to customers as a fully managed service. According to the company, the new competency is designed to help partners differentiate themselves in a crowded security market and make it easier for customers to procure their services.

- Furthermore, in July 2021, Tech Mahindra announced a managed security services provider (MSSP) partnership with cybersecurity company Palo Alto Networks. The agreement led to the expansion of Tech Mahindra's global partnership with the US-based multinational to provide a full suite of managed security services. As an MSSP, Tech Mahindra would offer complete visibility and control of the network, endpoint, and cloud security, including value-added services like risk assessment, posture management, workload protection, and orchestration to the company's customers.

- Furthermore, in July 2021, Telus launched a new managed cloud security solution based on Palo Alto Networks' Prisma Access technology, allowing Canadian businesses to access data and apps from anywhere securely. Additionally, to assure network security and protection, the new managed cloud security solution offers firewall services, threat prevention, malware prevention, URL filtering, SSL decryption, and application-based policies. It also allows consumers to use SASE by connecting to Telus SD-WAN services.

Asia-Pacific to Witness the Fastest Growth

- Digital transformation has become a top priority in the region. It is spreading rapidly as more companies implement formal strategies to support their efforts, driving the market demand.

- Engaging outsourced managed services for a company's IT resources can be a way to ensure substantial budget savings, more resilient computing capacity, and more secure network uptime and performance. China Telecom Americas Corporation gives complete turnkey professional ICT services in 72 countries globally in partnership with major vendors, such as Juniper, Microsoft, Cisco, FSNetworks, IBM, VMware, and Huawei, among many more.

- The increasing threats to cybersecurity in the region, including IT ransomware attacks, DDoS attacks, data exfiltration, and the increasing media coverage of high-profile cyberattacks, are compelling organizations in the country to adopt managed security services. Moreover, conventional industries are supported by policies to embrace digital transformation and enhance their adoption of IT technologies. Hence, their demand for internet data center services is also rising, further driving the market growth.

- With the rapid development of AI, 5G, IoT, virtual reality, and the commercial application of these new technologies, the demand for data processing and information interaction is increasing, which may speed up the construction of data centers in the region and lead to the explosive growth of the industry.

- Threats to the integrity, confidentiality, and obtainability of organization information are increasing exponentially in India, hence emphasizing the focus on providing a standardized model for information security based on a business risk approach to establish, implement, operate, monitor, review, maintain, and improve overall information security for customers.

- In February 2022, IBM announced an investment in its resources to help businesses in the Asian-Pacific (APAC) region prepare for and manage the growing danger of cyberattacks. The new IBM Security Command Center, the first in the region, is expected to educate cybersecurity response strategies using extremely realistic, simulated cyberattacks to prepare everyone from the C-suite to technical personnel. The investment also includes a new Security Operation Center (SOC), which may be part of IBM's current global SOC network, providing security response services to clients globally 24/7.

Managed Security Services Industry Overview

The managed security services market is fragmented due to existing giants and many upcoming vendors who provide security services to prevent companies from attacks like network attacks, Denial of services, or even performing a risk assessment. This market is anticipated to encounter many partnerships, mergers, service launches, and acquisitions as organizations continue to invest strategically.

- April 2022 - Ace Cloud Hosting (ACE), the global cloud services provider of application hosting and virtual desktops, announced the launch of Managed Security Services (MSS). Furthermore, Accenture acquired Symantec's cybersecurity services business to incorporate flexibility into security services. Additionally, Verizon integrated Blackberry Cylance's AI-based anti-virus solution into its security services portfolio. This integration is indicative of the increasing demand for AI-based cybersecurity solutions. Both these developments underscore the growth potential that the market offers.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Cyber Crime, Digital Disruption, and Increased Compliance Demands

- 5.1.2 Need for Threat Detection and Intelligence at an Early Stage Driving the Market Growth

- 5.2 Market Restraints

- 5.2.1 Lack of Awareness of Security Services is Discouraging the Market Expansion

- 5.3 Evolution and Key Trends in the MSSP Space

- 5.4 Assessment of the Impact of COVID-19 on the Market

6 MARKET SEGMENTATION

- 6.1 By Deployment Type

- 6.1.1 On-Premise

- 6.1.2 Cloud

- 6.2 By Solution Type

- 6.2.1 Intrusion Detection and Prevention

- 6.2.2 Threat Prevention

- 6.2.3 Distributed Denial of Services

- 6.2.4 Firewall Management

- 6.2.5 End-Point Security

- 6.2.6 Risk Assesment

- 6.3 By Managed Security Service Provider

- 6.3.1 IT Service Providers

- 6.3.2 Managed Security Specialist

- 6.3.3 Telecom Service Provider

- 6.4 By End-user Vertical

- 6.4.1 BFSI

- 6.4.2 Government and Defense

- 6.4.3 Retail

- 6.4.4 Manufacturing

- 6.4.5 Healthcare and Life Sciences

- 6.4.6 IT and Telecom

- 6.4.7 Other End-user Verticals

- 6.5 By Geography

- 6.5.1 North America

- 6.5.2 Europe

- 6.5.3 Asia-Pacific

- 6.5.4 Latin America

- 6.5.5 Middle East & Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 AT&T Inc.

- 7.1.2 Secureworks Inc. (Dell Technologies Inc.)

- 7.1.3 Symantec (Broadcom Inc.)

- 7.1.4 Trustwave Holdings Inc.

- 7.1.5 Alert Logic

- 7.1.6 IBM Corporation.

- 7.1.7 Verizon

- 7.1.8 CenturyLink

- 7.1.9 BAE Systems

- 7.1.10 AtoS

- 7.1.11 Capgemini

- 7.1.12 Wipro

- 7.1.13 Fujitsu