|

|

市場調査レポート

商品コード

1432671

ファクトリーオートメーション・産業制御:市場シェア分析、産業動向と統計、成長予測(2024年~2029年)Factory Automation and Industrial Controls - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| ファクトリーオートメーション・産業制御:市場シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

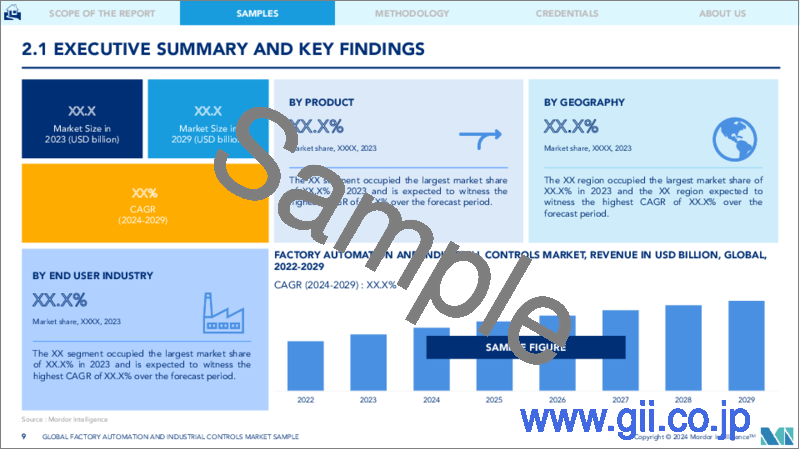

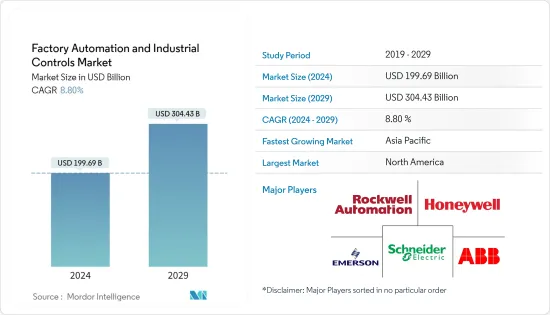

ファクトリーオートメーション・産業制御市場規模は、2024年に1,996億9,000万米ドルと推定され、2029年には3,044億3,000万米ドルに達すると予測され、予測期間中(2024-2029年)のCAGRは8.80%で成長する見込みです。

自動化と制御システムは製造ミスを減らし、時間とコストを節約し、顧客満足度を高めます。計画、製品開発、サプライチェーン・ロジスティクスのためのスマート工場の構築は、自動化と自己最適化によるプロセス改善のためのスマートシステム、コンポーネント、機械、設備の採用が増加した結果です。これは市場に影響を与える重要な側面です。

主なハイライト

- オートメーション産業は、最適なパフォーマンスを提供することを目的とした製造のデジタルと物理的側面の組み合わせによって革命を起こしています。さらに、廃棄物ゼロ生産の達成と市場投入までの時間短縮に注力することで、市場の成長が加速しています。

- 産業モノのインターネット(IIoT)とインダストリアル4.0は、スマートファクトリーオートメーションとして知られる物流チェーン全体の開発、生産、管理のための新しい技術的アプローチの中心であり、機械やデバイスがインターネットを介して接続され、産業分野の動向を支配しています。

- さらに、インダストリー4.0とIoTの受容による製造業の大規模なシフトにより、企業は、自動化によって人間労働を補完・拡張し、プロセスの失敗による産業事故を削減する技術で生産を進めるために、機敏でスマートな革新的方法を採用する必要があります。

- さらに、世界中の自動車メーカーは、次世代のロボットとオートメーション技術が、生産性、品質、安全性、コストパラメーターにおいて自動車産業を変革する革命的な可能性を持っていることを認識しています。ロボット自動化システムのニーズも、年々増加するロボット自動化支出から恩恵を受けると予想されます。

- 人件費は様々な分野で急激に上昇しています。さらに、品質に対する基準も厳しくなっています。このことを考慮すると、工場の自動化は生産費、運営費、人件費の削減につながる可能性があります。

- COVID-19の流行により世界中の企業や製造施設が閉鎖を余儀なくされ、市場は混乱しました。製造業における産業用オートメーション・システムの需要減退の結果、特に年初の2四半期に大きな損失が発生しました。幸いなことに、2021年の最初の数カ月は、工場の再開と産業運営の再開により、復活の明るい兆しが見えています。インダストリー4.0技術の進歩により、幅広い産業分野でロボットのような自動化ソリューションへの需要が高まっています。

ファクトリーオートメーション・産業制御市場の動向

自動車産業が大幅な成長を記録する見込み

- 自動車産業は、世界の自動化製造設備で大きなシェアを占める著名なセクターの1つです。様々な自動車メーカーの生産設備は、精度と効率を維持するために自動化されていることが確認されています。さらに、従来の自動車をEVに置き換える動向の高まりは、自動車産業の需要を増大させると予想されます。

- 多くの産業分野では、インダストリー4.0技術の発展により、ロボットのような自動化ソリューションの需要が増加しています。技術のおかげで、工場は365日24時間、人間の監視なしに操業できます。例えば、組み立てロボットは専用の設備よりも使い方が簡単で、人間よりも素早く正確に動くことができます。ロボットアームは、自動車製造施設において、ネジの打ち込み、フロントガラスの取り付け、ホイールの取り付けなどの作業を行うことができます。ロボットアームは、生産性と効率を高めると同時に、人間の作業員の経費と危険性を下げるという評判を得ています。

- さらにAIは、設計や生産のような製造業務から、保険や予知保全のような支援活動まで、自動車のバリューチェーンで活用されています。しかし、今日のAIの魅力的な用途のひとつは輸送であり、そこでは 促進要因レス車や運転支援システムの創造を後押ししています。

- さらに、ヒュンダイのようなブランドは、競合他社をリードするためにスマート・モビリティ・ソリューションに多額の投資を行っています。自動車がよりスマートでコネクテッドになる中、ロボット工学とAIに特化した企業を持つことは、長期的には大きな資産となります。2021年6月、現代自動車はソフトバンクからボストン・ダイナミクスの経営権を取得したことを明らかにしました。この取引によると、アメリカのロボット開発会社の評価額は11億米ドルで、現代自動車が80%の株式を保有し、ソフトバンクはまだ20%を保有しています。

- 自動車産業は、スマート工場のおかげで、生産量を増やし、製造のダウンタイムを減らし、サプライチェーンの効率を改善し、市場の需要により迅速に対応するチャンスがあります。プロジェクト期間は、自動車業界が直面する最重要課題のひとつです。プロジェクトの迅速な回収は、手頃な価格の自動化とコスト革新とともに、生産性向上によるメーカーの競争力強化を支援します。

北米が大きな市場シェアを占める

- 主要な自動車メーカーが北米に拠点を置いており、充実したインフラと政府による電気自動車支援の恩恵を受けています。さらに、高級車やプレミアム車に対する若者の志向の高まりが、有利な機会をもたらすと予測されます。

- 自動車業界の関心が電気自動車に移っているのは、自動車の排出ガス低減が重視されるようになっているためです。各国政府や環境機関は、環境問題の高まりに対処するため、厳しい排出規制や法律を制定しており、電気ドライブトレインや低燃費ディーゼルエンジンの生産コストが上昇する可能性があります。その結果、過去5年間で、北米におけるバッテリー式電気自動車の需要は過去最高を記録しました。

- さらに、自動車業界も同様に、デジタル化、自動化の進展、新たなビジネスモデルによって変化を遂げると思われます。モビリティの多様化、自律走行、電動化、コネクティビティという4つの破壊的な技術主導の動向が、こうした要因の結果として自動車業界に生まれつつあります。しかし、レンタカーや中古車市場の人気の高まりにより、市場参入企業は困難に直面する可能性があります。アマゾンのような大手eコマース企業による車両保有台数の拡大とともに、物流・配送サービスの成長は、商用車の需要に大きな影響を与えます。

- 工場自動化ソリューションの採用は、これらのメーカーのコスト削減、生産性向上、品質向上に役立ちます。最近、カナダロイヤル銀行(RBC)はマイクロソフトと協力し、カナダ企業のスマートオートメーション技術とクラウドソリューションへの投資を支援するGo Digitalプログラムを開始しました。このプログラムはカナダの食品メーカーが対象で、今後も他の業界にも拡大していく予定です。

- さらに北米では、2022年第1四半期に自動車メーカーや部品メーカーからのロボット受注が全体の47%を占めました。複数の自動車メーカーが、将来の電気自動車モデルに対応するため、あるいはバッテリーの生産能力を増強するために、工場の設備投資を強化すると発表しています。このような重要な取り組みにより、産業用ロボットの需要は今後数年間で増加すると思われます。

ファクトリーオートメーション・産業制御産業の概要

ファクトリーオートメーション・産業制御の世界市場は競争が激しく、複数の大手企業で構成されています。市場は適度に断片化されているようです。同市場で圧倒的なシェアを誇る大手企業は、海外における顧客基盤の拡大に注力しています。これらの企業は、市場シェアと収益性を高めるために、戦略的な共同イニシアティブを活用しています。また、ァクトリーオートメーション・産業制御に取り組む新興企業を買収し、製品力の強化を図っています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 業界バリューチェーン分析

- COVID-19の業界への影響評価

第5章 市場力学

- 市場促進要因

- エネルギー効率とコスト削減の重視の高まり

- 自動化への動向の高まり

- 市場の課題

- 貿易摩擦と導入課題

第6章 市場セグメンテーション

- 製品別

- 産業用制御システム別

- 分散型制御システム(DCS)

- プログラマブル・ロジック・コントローラー(PLC)

- 監視制御・データ収集(SCADA)

- 製品ライフサイクル管理(PLM)

- ヒューマン・マシン・インターフェース(HMI)

- 製造実行システム(MES)

- 企業資源計画(ERP)

- その他の産業用制御システム

- フィールド機器

- マシンビジョンシステム

- ロボット工学(産業用)

- センサーとトランスミッター

- モーター&ドライブ

- その他のフィールド・デバイス

- 産業用制御システム別

- エンドユーザー産業別

- 自動車

- 化学・石油化学

- ユーティリティ

- 製薬

- 飲食品

- 石油・ガス

- その他エンドユーザー産業

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- その他アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 北米

第7章 競合情勢

- 企業プロファイル

- Schneider Electric SE

- Rockwell Automation Inc.

- Honeywell International Inc.

- Emerson Electric Company

- ABB Limited

- Mitsubishi Electric Corporation

- Siemens AG

- Omron Corporation

- Yokogawa Electric Corporation

- General Electric Co.

- Texas Instruments Inc.

- Robert Bosch GmbH

第8章 投資分析

第9章 将来展望

The Factory Automation and Industrial Controls Market size is estimated at USD 199.69 billion in 2024, and is expected to reach USD 304.43 billion by 2029, growing at a CAGR of 8.80% during the forecast period (2024-2029).

Automation and control systems decrease manufacturing errors, which saves time and money and increases customer satisfaction. The creation of smart factories for planning, product development, and supply chain logistics is a result of the increased adoption of smart systems, components, machinery, and equipment for the improvement of processes through automation and self-optimization. This is a key aspect influencing the market.

Key Highlights

- The automation industry has been revolutionized by the combination of digital and physical aspects of manufacturing aimed at delivering optimum performance. Further, the focus on achieving zero waste production and a shorter time to reach the market has augmented the growth of the market.

- The Industrial Internet of Things (IIoT) and the Industrial 4.0 are at the center of the new technological approaches for the development, production, and management of the entire logistics chain, otherwise known as smart factory automation, and are dominating the trends in the industrial sector, with machinery and devices being connected via internet.

- Moreover, massive shifts in manufacturing due to Industry 4.0 and the acceptance of IoT require enterprises to adopt agile, smarter, and innovative ways to advance production with technologies that complement and augment human labor with automation and reduce industrial accidents caused by process failure.

- Additionally, automakers worldwide are aware of the revolutionary potential of the next generation of robots and automation technologies to transform the automotive industry in terms of productivity, quality, safety, and cost parameters. The need for robot automation systems is also anticipated to benefit from rising robotic automation spending year over year.

- The cost of labor has risen exponentially in many different areas. Additionally, the standards for quality are becoming stricter. In light of this, factory automation may result in lower production, operating, and labor expenses.

- The market was disrupted when the COVID-19 epidemic forced the closure of enterprises and manufacturing facilities worldwide. Significant losses were incurred, particularly in the first two quarters of the year, as a result of the drop in demand for industrial automation systems in the manufacturing sectors. Fortunately, there have been encouraging signs of a resurgence in the first few months of 2021, owing to the reopening of the plants and the restart of industrial operations. Industry 4.0 technology advancements have increased demand for automated solutions like robots across a wide range of industrial industries.

Factory Automation and Industrial Controls Market Trends

Automotive is Expected to Register a Significant Growth

- The automotive industry is one of the prominent sectors that hold a significant share in worldwide automated manufacturing facilities. It is observed that the production facilities of various automakers are automated to maintain accuracy and efficiency. Further, the growing trend of replacing conventional vehicles with EVs is expected to augment the automotive industry's demand.

- In many industrial areas, the demand for automated solutions like robots has increased due to developments in Industry 4.0 technology. Because of technology, factories can operate without human supervision for 24 hours daily, 365 days per year. For instance, assembly robots are simpler to use than specialized equipment and can move more quickly and precisely than people. Robotic arms can do activities like screw driving, windshield installation, and wheel mounting in auto manufacturing facilities. They have a reputation for boosting productivity and efficiency while lowering expenses and dangers for human workers.

- Additionally, AI is used in the automotive value chain, from manufacturing duties like design and production to supporting activities like insurance and predictive maintenance. However, one of AI's fascinating uses today is transportation, where it powers the creation of driverless vehicles and driver assistance systems.

- Further, brands such as Hyundai have invested heavily in smart mobility solutions to stay ahead of their competitors. With cars becoming smarter and more connected, having a company specializing in robotics and AI can be a great asset in the long run. In June 2021, Hyundai Motor Company recently confirmed that they had bought a controlling interest in Boston Dynamics from SoftBank. According to the deal, the American robotics developer has been valued at USD 1.1 billion, and Hyundai has 80% shares while SoftBank still owns 20%.

- The automotive industry has chances to increase production, decrease manufacturing downtime, improve supply chain efficiency, and respond more quickly to market demands thanks to smart factories. The length of a project is one of the top issues facing the automotive sector. Rapidly paying off projects, together with affordable automation and cost innovation, aid manufacturers in becoming more competitive by enhancing productivity.

North America to Hold a Significant Market Share

- Major automotive OEMs are based in the nation, benefiting from a substantial infrastructure and the government's support for electric vehicles. In addition, the increasing inclination of young people for luxury and premium vehicles is predicted to present lucrative opportunities.

- The automotive industry's attention has switched to electric vehicles due to the growing emphasis on decreasing vehicle emissions. Governments and environmental agencies are rolling out stringent emission rules and laws to address growing environmental concerns, which could increase the cost of producing electric drive trains and fuel-efficient diesel engines. As a result, over the past five years, battery electric car demand in North America has reached an all-time high.

- Additionally, the automotive industry will similarly undergo a change fueled by digitization, rising automation, and new business models. Four disruptive technology-driven trends are emerging in the automobile industry as a result of these factors: diversified mobility, autonomous driving, electrification, and connection. However, market participants may face difficulties due to the growing popularity of rental and used car markets. Growing logistics and delivery services, along with the expansion of vehicle fleets by major e-commerce players like Amazon, etc., significantly impact the demand for commercial cars.

- The adoption of factory automation solutions can help these manufacturers in cost savings, enhance productivity, and improve quality. Recently, the Royal Bank of Canada (RBC) collaborated with Microsoft and launched the Go Digital program to help Canadian businesses invest in smart automation technologies and cloud solutions. The program is available to Canadian food manufacturers and will continue expanding to other industries.

- In addition, in North America, orders for robots from automakers and component manufacturers accounted for 47% of all orders in the first quarter of 2022. Several automakers have announced investments better to outfit their plants for future electric drive car models or to boost battery production capacity. These significant initiatives will increase the demand for industrial robots in the coming years.

Factory Automation and Industrial Controls Industry Overview

The Global Factory Automation and Industrial Controls Market is highly competitive and consists of several major players. The market appears to be moderately fragmented. The major players with prominent shares in the market are focusing on expanding their customer base across foreign countries. These companies are leveraging on strategic collaborative initiatives to increase their market shares and profitability. The companies operating in the market are also acquiring start-ups working on factory automation and industrial control systems to strengthen their product capabilities.

- July 2022 - Rockwell Automation, Inc., the world's largest company dedicated to industrial automation and digital transformation, announced the launch of the PowerFlex AC variable frequency drive portfolio in the Asia Pacific to support an array of motor control applications. This will provide customers more flexibility, performance, and intelligence in their next generation drive through TotalFORCE Technology.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 An Assessment of Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Emphasis on Energy Efficiency and Cost Reduction

- 5.1.2 Growing Trend Towards Automation

- 5.2 Market Challenges

- 5.2.1 Trade Tensions and Implementation Challenges

6 MARKET SEGMENTATION

- 6.1 By Product

- 6.1.1 By Industrial Control Systems

- 6.1.1.1 Distributed Control System (DCS)

- 6.1.1.2 Programmable Logic Controller (PLC)

- 6.1.1.3 Supervisory Control and Data Acquisition (SCADA)

- 6.1.1.4 Product Lifecycle Management (PLM)

- 6.1.1.5 Human Machine Interface (HMI)

- 6.1.1.6 Manufacturing Execution System (MES)

- 6.1.1.7 Enterprise Resource Planning (ERP)

- 6.1.1.8 Other Industrial Control Systems

- 6.1.2 Field Devices

- 6.1.2.1 Machine Vision Systems

- 6.1.2.2 Robotics (Industrial)

- 6.1.2.3 Sensors and Transmitters

- 6.1.2.4 Motors and Drives

- 6.1.2.5 Other Field Devices

- 6.1.1 By Industrial Control Systems

- 6.2 By End-User Industry

- 6.2.1 Automotive

- 6.2.2 Chemical and Petrochemical

- 6.2.3 Utility

- 6.2.4 Pharmaceutical

- 6.2.5 Food and Beverage

- 6.2.6 Oil and Gas

- 6.2.7 Other End-user Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Rest of Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 China

- 6.3.3.2 India

- 6.3.3.3 Japan

- 6.3.3.4 Rest of Asia Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East & Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Schneider Electric SE

- 7.1.2 Rockwell Automation Inc.

- 7.1.3 Honeywell International Inc.

- 7.1.4 Emerson Electric Company

- 7.1.5 ABB Limited

- 7.1.6 Mitsubishi Electric Corporation

- 7.1.7 Siemens AG

- 7.1.8 Omron Corporation

- 7.1.9 Yokogawa Electric Corporation

- 7.1.10 General Electric Co.

- 7.1.11 Texas Instruments Inc.

- 7.1.12 Robert Bosch GmbH