|

市場調査レポート

商品コード

1404090

ガラス瓶と容器:市場シェア分析、産業動向と統計、2024~2029年の成長予測Glass Bottles and Containers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| ガラス瓶と容器:市場シェア分析、産業動向と統計、2024~2029年の成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 227 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

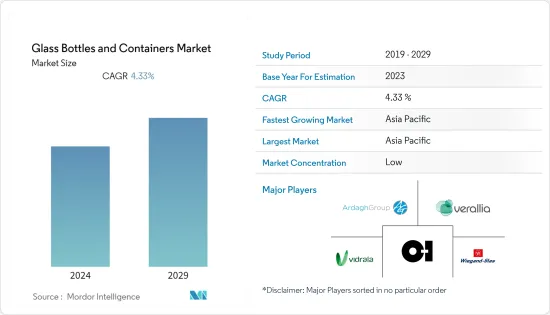

ガラス瓶と容器の市場規模は、2024年の8,306億2,000万個から2029年には1兆300億個に拡大し、予測期間(2024~2029年)のCAGRは4.33%と予測されます。

主要ハイライト

- 安全で健康的な包装に対する消費者の需要の高まりが、様々なカテゴリーにおけるガラス包装の成長を後押ししています。また、ガラスにエンボス加工を施し、成形し、芸術的な仕上げを加える革新的な技術が、ガラス包装をエンドユーザーの間でより望ましいものにしています。さらに、環境に優しい製品に対する需要の増加や飲食品市場の需要の高まりといった要因も、市場の成長を促しています。

- ここ数年、食品包装の透明化傾向が強まっています。消費者は、表示された原材料だけでなく、購入前に現物を確認することを望んでいます。多くの企業、特に乳製品は、この動向をとらえるため、透明なガラス容器で提供し始めています。

- ガラス瓶や透明容器は、時代を超越したエレガントなデザインで、消費者にアピールします。また、ガラスの透明性は製品に高級感と洗練された印象を与え、棚や陳列棚でより魅力的に見せる。こうした要因が、予測期間中の同分野の成長を促進すると思われます。

- 市場の成長を促進するもう1つの要因は、医療産業からのガラス瓶需要の増加です。また、消費者がより効果的で審美的なパッケージデザインを求める傾向にあるため、人々の可処分所得の増加も市場開拓を推進する大きな要因となっています。

- さらに、糖尿病患者の増加が注射用ガラス瓶の成長を大きく後押ししています。世界保健機関(WHO)によると、近年、世界中で約4億2,200万人が糖尿病を患っています。この数の増加がインスリン需要の原動力となり、市場の成長に寄与しています。

- しかし、ガラス瓶や容器は壊れやすく、適切な取り扱いと作業・物流上の注意が必要です。これは、ガラス包装ソリューションを展開する企業にとって重要な課題となっています。ガラス包装はその重量と嵩のため、長距離輸送には不向きです。伝統的な業界の制約として、これがガラス包装業界が主に地元志向である主要理由です。加えて、ガラス製造による二酸化炭素排出量も市場成長の妨げになると予想されます。

- 消費者や産業界における持続可能な包装に対する意識の高まりに伴い、特にパンデミックを目の当たりにした後は、持続可能な包装の成長には大きな余地があると思われます。鎖国後、消費者はより健康的なライフスタイルを採用することに重点を置き、特に飲食品部門に関連する製品について持続可能なソリューションを探し始めています。

- 需要の急増は、購買力の増加、近代的な小売、都市化、消費者の健康と衛生に対する意識の高まりに負うところが大きく、COVID後の世界ではガラス包装業界に大きな成長機会が生まれると予想されます。

ガラス瓶・容器の市場動向

ワイン・スピリッツがノンアルコール飲料セグメントをリード

- ワインの包装ではガラス瓶が最も好まれ、特に色付きガラスが好まれます。そうしないと腐敗してしまうからです。ワインの消費量の増加は、予測される期間中、ガラス包装の需要を先導すると予想されます。ワインメーカーは、パッケージで顧客を引き付けるためにますます革新的になっており、新しいコンセプトやデザインを開発しています。例えば、Vinebox社は、円筒形の100mlガラス容器に詰められた9種類のシングルサーブ・ワインのボックスを年4回顧客に発送しています。

- ガラス瓶に詰められたワインは、デザイン、エレガントな感触、伝統を通じてプレミアムな体験を提供します。ユニークなデザインは、他の包装材では味わえない高級感を提供します。先進国では、ワインは贈答用にも使われます。そのため、ユニークなガラス瓶に詰められたワインは、他のパッケージング・ソリューションよりも優位に立つ。

- ブランドや包装メーカーは、カーボンフットプリントを削減するため、軽量ガラス瓶の開発に注力しています。さらに、ブランドや企業は、シャンパンと呼ばれるスパークリングワイン用の軽量ボトルを開発するための実験や研究も行っています。フランスのガラスメーカー、ヴェラリア・グループとシャンパーニュ・テルモンは、2023年に800グラムのシャンパン用ガラス瓶を使用するという最新の実験に成功したと発表しました。新しい軽量ガラス瓶は、ボトル1本あたりの二酸化炭素発生量を約4%削減します。

- 米国、フランス、イタリア、ドイツ、英国はワイン消費量の上位5カ国です。国際ブドウ・ワイン機構によると、米国のワイン消費量は2022年に2021年比で2.8%増加しました。さらに、ボトルワインは世界貿易量の大部分を占め、2022年の貿易量では53%、貿易額では68%を占めました。2022年のボトルワインの貿易額は、2021年と比較して7%増加しました。ボトル入りワインの輸出は、他の包装タイプに比べてほとんどの国で多かった。例えば、イタリアは57%、フランスは72%、チリは58%、ドイツは73%、ポルトガルは76%、米国は52%、アルゼンチンは76%、オーストラリアは35%、スペインは34%です。

- 世界の蒸留酒の消費と取引の増加が、蒸留酒用ガラス瓶の需要を牽引しています。米国蒸留酒協会によれば、米国は世界第2位の蒸留酒市場です。米国の蒸留酒輸出は過去20年間でほぼ4倍になり、2022年には5億5,100万米ドルから約21億米ドルに達します。米国における2023年1月から6月までのウイスキー輸出量は約2,330万ガロンでした。ウイスキー輸出全体のうち、ボトル入りウイスキーが約55.44%を占めています。これは市場にかなりのインパクトを与えていることを示しています。

アジア太平洋が最大の市場シェアを占める

- 中国の包装業界は、同国の経済拡大と購買力のある中間層の増加により、急速かつ安定したペースで成長しています。中国の飲料市場は近年著しく成長しているため、飲料用パッケージのニーズは高まっています。

- 各飲料カテゴリーには課題と機会があるが、中国の消費者ライフスタイルの新しい動向がガラス包装の需要を形成しています。中国は大都市中心部において、あらゆる産業でアルコール飲料とノンアルコール飲料の消費が増加しています。中国の大富豪が最も好む飲料には、赤ワイン、ウイスキー、シャンパンなどがあります。

- インドにおけるアルコール飲料消費の増加は、ガラス瓶と容器の成長を支えるものと予想されます。ガラス瓶はアルコール飲料で最も好まれており、ワインは日光に当たると腐敗するため、ワイン用のワイルドな色ガラスが使われています。また、ワインの消費の増加は、予測期間中にガラス包装需要の先鋒を務めると予想されます。例えば、Agriculture and Agri-Food Canadaによると、インド全体のワイン消費量は2025年に5,220万リットルに達すると予測されています。

- さらに、市場の需要はノンアルコール飲料の成長によっても影響を受ける。ソフトドリンクは、ノンアルコール飲料のビジネスを支える最も重要な柱です。インドにおけるコーラの売上シェアは、ガラス瓶が35%を維持しています。2022年5月、Coca-Cola India Pvt. Ltdは、コカ・コーラ、サムズアップ、スプライトといった同社の売れ筋ブランドにおいて、一部の州で再びリターナブルのガラス瓶の販促を開始しました。市場によっては、2022年にはガラス瓶が飲料売上の30%を占める。

- 過去数年間における国産ビールの成長が、ガラス製パッケージの成長を支えていると予想されます。韓国におけるビールの小売売上高は、2018年の159億8,000万米ドルから2022年には192億7,000万米ドルに達しました。同市場は過去数年間成長を経験しており、今後数年間も同様の変化の兆しを見せると予想される(カナダ農業・農業食品省)。

- 本調査でアジア太平洋としてすでに取り上げた国々以外に、オーストラリア、台湾、タイ、マレーシア、シンガポール、ベトナムなどの国々も、調査対象市場でかなりのシェアを獲得する可能性が高いです。アルコール飲料の販売増加、買収、合併がこの地域のガラス包装市場を牽引しています。

ガラス瓶・容器産業概要

ガラス瓶・容器市場は、主にGerresheimer AG、Owens-Illinois(O-I)、Ardagh Packaging Group PLC、Piramal Glass Ltd.など一握りの大手企業によって支配されています。これらの業界大手は、様々な地域で事業を展開し、多様な製品ポートフォリオを維持しています。とはいえ、数多くの他社も同様の製品を製造しているため、業界は激しい競合に直面しています。

強力で評判の高いブランドは、市場での存在感を確立し、高度な製品を提供できるため、競合を維持できると予想されます。さらに、大規模な資本投資の注入は、既存企業の撤退障壁を高め、業界内の競争をさらに激化させる。

2023年9月、Ardagh Glass Packagingは、温室効果ガスの排出削減を目的として、オーベルンキルヘンの施設に環境的に持続可能な炉を建設する構想を発表しました。ネクストジェン炉は2023年末までに商業用ガラス容器の生産を開始する予定で、1日最大350トン(t)のガラス瓶の製造能力を誇る。

2023年7月、飲料業界ではガラス製パッケージの技術革新が急増し、飲みやすさを追求した広口製品「ドリンクテナー」がイントロダクション登場しました。FX Matt Beverage Co.とO-I Glassは、このイノベーションを市場に送り出すために協力しました。Drinktainerは、両社の新たなパートナーシップの成功の成果です。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 業界バリューチェーン分析

- COVID後のガラス瓶と容器市場への影響

- ウクライナ・ロシア紛争のガラス瓶と容器市場への影響

- キードライバーを用いたコスト分析(構成要素とエネルギー消費量)-ガラス容器の構成要素

第5章 市場力学

- 市場促進要因

- 飲食品産業からの需要拡大

- 持続可能性とリサイクルへの取り組みが包装業者と消費者ブランドをガラス包装に移行させる

- 市場抑制要因

- ガラス製造による高いカーボンフットプリント

- 操業と物流に関する懸念

第6章 市場セグメンテーション

- エンドユーザー業界別

- 飲料

- アルコール飲料

- ビールとサイダー

- ワイン・スピリッツ

- その他のアルコール飲料

- ノンアルコール

- 炭酸飲料

- 牛乳

- 水、その他ノンアルコール飲料

- 食品

- 化粧品

- 医薬品

- その他業界別

- 飲料

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ポーランド

- ロシア

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- その他の中東とアフリカ

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他のラテンアメリカ

- 北米

第7章 競合情勢

- 企業プロファイル

- O-I Glass, Inc.

- Vidrala SA

- Ardagh Group S.A.

- Wiegand-glas GmbH

- Verallia Packaging

- Vetropack Holding Ltd

- Stoelzle Oberglas GmbH(CAG-holding GmbH)

- Gaasch Packaging

- Beatson Clark

- Vitro SAB de CV

- Schott AG

- Glassworks International Limited

- Gerresheimer AG

- Middle East Glass Manufacturing Co SAE

- Berlin Packaging LLC

- BA VIDRO SA(BA Glass BV)

- PGP Glass Private Limited

- VERESCENCE FRANCE

- SGD SA(SGD Pharma)

- Saver Glass SAS(The Carlyle Group Inc.)

第8章 投資分析

第9章 市場の将来

The glass bottles and containers market size is expected to grow from 830.62 billion units in 2024 to 1.03 trillion units by 2029, at a CAGR of 4.33% during the forecast period (2024-2029).

Key Highlights

- Increasing consumer demand for safe and healthier packaging is helping glass packaging grow in different categories. Also, innovative technologies for embossing, shaping, and adding artistic finishes to glass make glass packaging more desirable among end users. Furthermore, factors such as the increasing demand for eco-friendly products and the rising demand from the food and beverage market are stimulating the market's growth.

- There has been an increasing transparency trend in food packaging over the past few years. Beyond the labeled listed ingredients, consumers also want to see the physical product before purchasing. Many companies, especially dairy products, have started offering them in transparent glass containers to capture this trend.

- Glass bottles and transparent containers have a timeless, elegant design that appeals to consumers. The transparency of glass also adds a premium and refined look to products, making them more appealing on shelves or displays. These factors would drive segment growth over the forecast period.

- Another factor driving the market's growth is the increasing demand for glass bottles from the healthcare industry. The rise in the disposable income of people is also a significant factor propelling the development of the market, as consumers tend to demand more effective and aesthetic packaging design.

- Moreover, the increasing number of people with diabetes significantly supports the growth of glass bottles for injectable pharmaceuticals. According to the World Health Organization (WHO), around 422 million people worldwide have had diabetes in recent years. The increase in this number drives the demand for insulin, thereby contributing to the market's growth.

- However, glass bottles and containers are fragile and need proper handling and care of operation and logistics. This stands as a significant challenge for companies deploying glass packaging solutions. Due to its weight and bulkiness, glass packaging is unsuitable for long-distance transportation. As a traditional industry constraint, this is the main reason that the glass packaging industry is primarily locally oriented. In addition, the carbon footprint due to glass manufacturing is also expected to hinder the market's growth.

- With the increase in the awareness of sustainable packaging among consumers and industries, especially after witnessing the pandemic, there will be huge scope for growth in sustainable packaging. After the lockdown, consumers are more focused on adopting a healthier lifestyle and have started looking for sustainable solutions, especially for products related to the food and beverage sector.

- The surge in demand, owing largely to the growing purchasing power, modern retail, urbanization, and increasing awareness about health and hygiene among consumers, is expected to create significant growth opportunities for the glass packaging industry in the post-COVID world.

Glass Bottle and Container Market Trends

Wine and Spirits to Lead the Non-alcoholic Beverages Segment

- The glass bottle is most favored in wine packaging, especially colored glass, the reason being that wine should not be exposed to sunlight. Otherwise, it gets spoiled. The increasing consumption of wine is expected to spearhead the glass packaging demand during the forecasted period. Wine manufacturers are becoming increasingly innovative to attract customers with the packaging and are developing new concepts and designs. For example, Vinebox ships customers a box of nine single-serve wines packaged in cylindrical 100 ml glass containers four times a year.

- The wine packed in glass bottles offers a premium experience through the design, elegant feel, and heritage. The unique design provides the feeling of luxury that other packaging materials could not offer. Wine is also used for gifting purposes on occasions in the developed country. Therefore, the wine packed in unique glass bottles gains an advantage over the other packaging solutions.

- The brands and packaging manufacturers focus on developing lightweight glass bottles to reduce carbon footprints. In addition, the brands and companies are also carrying out experiments and studies to develop lightweight bottles for sparkling wine called champagne. French glassmaker Verallia Group and Champagne Telmont announced the success of their most recent experiment of using an 800-gram champagne glass bottle in 2023. The new lighter glass bottles will generate around 4% less carbon dioxide per bottle produced.

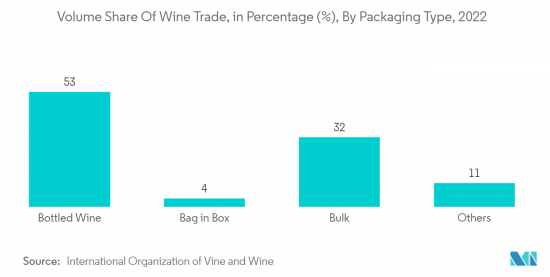

- The United States, France, Italy, Germany, and the United Kingdom are the top five countries in terms of wine consumption. According to the International Organization of Vine and Wine, wine consumption in the United States increased by 2.8% in 2022 compared to 2021. Furthermore, bottled wine represented the major portion of the trade volume globally, accounting for 53% in terms of trade volume and 68% in terms of trade value for the year 2022. The bottled wine trade value increased by 7% in 2022 compared to 2021. Bottled wine exports were high in most countries compared to other packaging types. For instance, Italy exported 57% of wine in bottles, France 72%, Chile 58%, Germany 73%, Portugal 76%, the United States 52%, Argentina 76%, Australia 35%, and Spain 34%.

- The increasing consumption and trade of spirits worldwide are driving the demand for glass bottles for spirits. The United States is the second-largest market for spirits in the world, according to the Distilled Spirits Council of the United States. The spirits export in the United States nearly quadrupled over the past two decades, reaching around USD 2.1 billion in 2022 from USD 551 million in 2022. The export of whiskey in the United States stood at around 23.3 million gallons from January to June 2023. Out of the total whiskey exports, bottled whiskey accounts for around 55.44% of the total. This showcases a fair impact on the market.

Asia-Pacific to Hold the Largest Market Share

- The packaging industry in China is growing at a fast and steady rate due to the country's expanding economy and growing middle class with more purchasing power. The need for beverage packaging is increasing because China's beverage market has grown significantly recently.

- Each beverage category will have challenges and opportunities, but new trends in the Chinese consumer lifestyle are shaping the demand for glass packaging. China has seen a rise in the consumption of alcoholic and non-alcoholic drinks across all industries in its large urban centers. Some of the most preferred beverages by millionaires in China are Red Wine, Whiskey, and Champagne.

- The increase in the consumption of alcoholic beverages in India is expected to support the growth of glass bottles and containers. The glass bottle is most favored in alcoholic beverages, wildly colored glass for wine because wine gets spoiled if exposed to the sunlight. Also, the increasing consumption of wine is expected to spearhead the glass packaging demand during the forecasted period. For Example, according to Agriculture and Agri-Food Canada, the volume of wine consumption across India is projected to reach 52.2 million liters in 2025.

- Moreover, the demand for the market will also be impacted by the growth in non-alcoholic beverages. Soft drinks are the most significant pillar on which the business of non-alcoholic drinks rests. Glass bottles retain a 35% share of sales for Coke in India. In May 2022, Coca-Cola India Pvt. Ltd started promoting returnable glass bottles again in select states across the company's top-selling brands, such as Coca-Cola, Thums Up, and Sprite. In some markets, glass bottles comprise 30% of beverage sales in 2022.

- The growth in domestic beer during the past years is expected to support growth in glass packaging. The retail sales of beer in South Korea reached USD 19.27 billion in 2022 from USD 15.98 billion in 2018. The market has experienced growth in the past years and is anticipated to show similar signs of change in the years ahead (Agriculture and Agri-Food Canada).

- Apart from the countries already discussed in the study under the Asia-Pacific region, other countries like Australia, Taiwan, Thailand, Malaysia, Singapore, Vietnam, etc., also have a high potential scope for gaining a considerable share in the market studied. The growth in the sale of alcoholic beverages, acquisitions, and mergers drives the market for glass packaging in the region.

Glass Bottle and Container Industry Overview

The glass bottles and containers market is primarily dominated by a handful of major companies, including Gerresheimer AG, Owens-Illinois (O-I), Ardagh Packaging Group PLC, and Piramal Glass Ltd. These industry leaders operate across various regions and maintain diversified product portfolios. Nevertheless, the industry faces fierce competition, as numerous other companies also manufacture similar products.

Strong and reputable brands are expected to maintain a competitive edge due to their established market presence and ability to offer advanced product offerings. Additionally, the infusion of significant capital investments raises the barriers to exit for existing players, further intensifying competition within the sector.

In September 2023, Ardagh Glass Packaging unveiled its initiative to construct an environmentally sustainable furnace at its Obernkirchen facility with the aim of reducing greenhouse gas emissions. The NextGen furnace is anticipated to commence the production of commercial glass containers by the end of 2023, boasting the capacity to manufacture up to 350 tonnes (t) of glass bottles daily.

In July 2023, the beverage industry witnessed a surge in glass packaging innovation, resulting in the introduction of the Drinktainer, a wide-mouth product designed to enhance the drinking experience. FX Matt Beverage Co. and O-I Glass collaborated to bring this innovation to market. The Drinktainer represents the successful outcome of a new partnership between the two companies.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Post-COVID Impact on Glass Bottles and Containers Market

- 4.5 Impact of Ukraine-Russia Conflict on Glass Bottles and Containers Market

- 4.6 Cost Analysis With Key Drivers (Components and Energy Consumption) - Components of Glass Container

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Demand from Food and Beverage Industry

- 5.1.2 Sustainability and Recyclability Initiatives Moving Packagers and Consumer Brands to Glass Packaging

- 5.2 Market Restraints

- 5.2.1 High Carbon Footprint due to Glass Manufacturing

- 5.2.2 Operation and Logistical Concerns

6 MARKET SEGMENTATION

- 6.1 By End-user Vertical

- 6.1.1 Bevarages

- 6.1.1.1 Alcoholic

- 6.1.1.1.1 Beer and Cider

- 6.1.1.1.2 Wine and Spirits

- 6.1.1.1.3 Other Alcoholic Beverages

- 6.1.1.2 Non-alcoholic

- 6.1.1.2.1 Carbonated Soft Drinks

- 6.1.1.2.2 Milk

- 6.1.1.2.3 Water and Other Non-alcoholic Beverages

- 6.1.2 Food

- 6.1.3 Cosmetics

- 6.1.4 Pharmaceutical

- 6.1.5 Other End-user Verticals

- 6.1.1 Bevarages

- 6.2 By Geography

- 6.2.1 North America

- 6.2.1.1 United States

- 6.2.1.2 Canada

- 6.2.2 Europe

- 6.2.2.1 United Kingdom

- 6.2.2.2 Germany

- 6.2.2.3 France

- 6.2.2.4 Italy

- 6.2.2.5 Spain

- 6.2.2.6 Poland

- 6.2.2.7 Russia

- 6.2.2.8 Rest of Europe

- 6.2.3 Asia-Pacific

- 6.2.3.1 China

- 6.2.3.2 India

- 6.2.3.3 Japan

- 6.2.3.4 South Korea

- 6.2.3.5 Rest of Asia-Pacific

- 6.2.4 Middle East and Africa

- 6.2.4.1 United Arab Emirates

- 6.2.4.2 Saudi Arabia

- 6.2.4.3 South Africa

- 6.2.4.4 Rest of Middle East and Africa

- 6.2.5 Latin America

- 6.2.5.1 Brazil

- 6.2.5.2 Mexico

- 6.2.5.3 Argentina

- 6.2.5.4 Rest of Latin America

- 6.2.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 O-I Glass, Inc.

- 7.1.2 Vidrala SA

- 7.1.3 Ardagh Group S.A.

- 7.1.4 Wiegand-glas GmbH

- 7.1.5 Verallia Packaging

- 7.1.6 Vetropack Holding Ltd

- 7.1.7 Stoelzle Oberglas GmbH (CAG-holding GmbH)

- 7.1.8 Gaasch Packaging

- 7.1.9 Beatson Clark

- 7.1.10 Vitro SAB de CV

- 7.1.11 Schott AG

- 7.1.12 Glassworks International Limited

- 7.1.13 Gerresheimer AG

- 7.1.14 Middle East Glass Manufacturing Co SAE

- 7.1.15 Berlin Packaging LLC

- 7.1.16 BA VIDRO SA (BA Glass BV)

- 7.1.17 PGP Glass Private Limited

- 7.1.18 VERESCENCE FRANCE

- 7.1.19 SGD SA (SGD Pharma)

- 7.1.20 Saver Glass SAS (The Carlyle Group Inc.)