|

市場調査レポート

商品コード

1432783

金属包装:市場シェア分析、産業動向と統計、成長予測(2024~2029年)Metal Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| 金属包装:市場シェア分析、産業動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

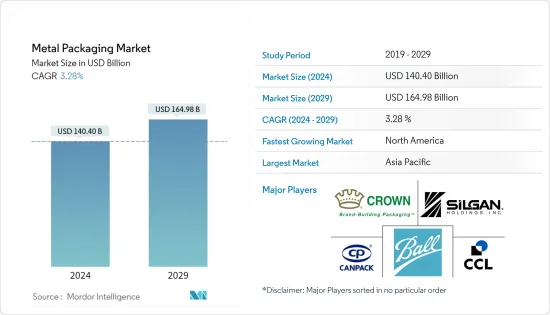

金属包装市場規模は2024年に1,404億米ドルと推定され、2029年には1,649億8,000万米ドルに達すると予測され、予測期間中(2024-2029年)のCAGRは3.28%で成長します。

主なハイライト

- 金属包装は主にスチール、アルミニウム、金属でできています。金属包装の主な利点には、耐衝撃性、厳しい温度に耐える能力、長距離輸送の利便性などがあります。缶詰食品は、特に忙しい都市部で高い需要があるため、この用途での製品の魅力が高まっており、消費を促進しています。製品の耐久性と高圧に耐える能力は、フレグランス業界で人気のある選択肢となっています。また、クッキー、コーヒー、紅茶などの嗜好品が金属包装でますます普及するにつれて、金属ベースの包装も成長しています。

- 消費者製品、化粧品、ヘルスケア、飲食品、その他の最終用途産業は金属包装に依存しています。予想される期間中、これらの最終用途産業の驚異的な成長により、市場は大幅に増加すると予想されます。金属包装の需要は、利便性の高い包装に対する消費者の需要の高まり、健康志向の高まり、「オン・ザ・ゴー」ライフスタイルの傾向の高まり、競合が激化する環境下でのブランド強化と差別化のニーズの高まり、環境意識の高まりなど、その他の幅広い要因にも影響されています。このため、企業は新しいパッケージリサイクル規制を採用しています。金属包装の需要は主に、顧客の健康志向の高まりによってもたらされています。

- 金属包装は、食品内容物の保護に適しており、他のほとんどの包装ソリューションよりも長い賞味期限を保証するため、飲食品業界においても広範な用途を見出しています。これとは対照的に、ドラム缶やIBC(中間バルクコンテナ)のような、石油、化学薬品、液体を輸送する頑丈な金属容器もあります。国連によると、世界は急速に都市化しており、都市部に住む人の割合は2050年までに66%に増加すると予想されています。都市化が進み、豊かさが増すにつれて食生活も変化し、包装食品への需要が高まっています。さらに、様々な金属製品タイプの優れた防腐特性と構造的完全性により、より高い保存期間が得られるため、食品包装業界では金属包装の使用量が増加しています。

- さらに、金属包装のリサイクル可能性は、図期間にわたって世界の金属包装市場を促進すると予想される重要な要素の1つです。再利用の基盤が普及しているため、アルミニウムとスチール包装材料は、包装のための2つの最も活発な未精製コンポーネントです。欧州と北米のほとんどの企業は、自社製品が環境に優しい材料で梱包されていることを宣伝することを好みます。

- さらに、惣菜やオン・ザ・ゴー食も、特に多忙なライフスタイルを送る消費者の間で、利便性に対する安定した需要を目の当たりにしてきました。そのため、組織化された大手小売業者は、膨大な缶詰食品や飲食品を積み重ねるようになった。現在、オフラインおよびオンラインの小売業者は、幅広いブランドのパッケージ食品を店舗にストックしています。金属包装は冷却しやすく、内容物の鮮度を保つのに最適であり、素材の強度により外出先での破損を防ぐことができるため、飲料の容器として適しています。

- 金属包装は、代替包装ソリューションとの高い競合に直面しています。プラスチックとガラスのパッケージング・ソリューションは、業界で利用可能な代替パッケージング・オプションです。また、欧州におけるeコマースの重要性の高まりは、パッケージング業界全体に影響を与えると予想されます。

- 化粧品・パーソナルケア業界では、消費者の交渉力が高いです。これは競争の激化と、さまざまなメーカーから化粧品が提供されているためです。これらの製品は代替性が高いため、競合他社の製品を購入する消費者はメーカーに製品価格を下げさせることができ、これはエアゾール缶市場にとって大きな制約となります。エネルギー価格の上昇に伴い、COVID-19期間中のサプライチェーンの混乱はアルミニウム産業の成長に影響を与えました。

- ロシアとウクライナの戦争は、いくつかの国に対する経済制裁、商品価格の高騰、サプライチェーンの混乱、世界の多くの市場への影響をもたらし、業界の貿易の混乱を引き起こしました。戦争は欧州のアルミ会社を減産に追い込み、金属不足を招いた。ウクライナでの戦争がロシアの供給に依存する欧州メーカーに深刻な供給不足をもたらしたため、商品取引業者は中国からのアルミニウム出荷による乏しい利益をめぐって競争しています。欧州はエネルギーコストの高騰に見舞われています。

金属包装市場の動向

缶が大きなシェアを占める見込み

- 金属缶は、剛性、安定性、高いバリア性など多くの利点を備えているため、賞味期限が長く、長距離輸送が可能な商品の保存に使用されています。欧州では、スズ、スチール、アルミの金属缶が好まれます。これらの素材は、柔らかく軽量であるなどの重要な特性を持っているため、メーカーは物流コストを節約することができます。

- この国の食品包装は、金属パッケージの台頭以来、多くの技術革新を目の当たりにしてきました。工業化は、金属が食品の大量商品化のための材料として最初に選ばれる原動力のひとつであることを証明しています。食品包装業界では、過去100年にわたり様々な素材が使用されてきたが、アルミニウムのような金属は、信頼できる強度と持続可能性により、最も広く支持されています。食品の長期保存には金属缶が最も理にかなっています。

- 若い顧客は、クラフトビールの代名詞となった、大胆で鮮やかな360度デザインに特に惹かれています。アルコール飲料の缶が、おいしい飲料のための高級品であるという消費者の認識の変化が、成長に影響を与えています。メタル缶のアルコール飲料は、缶がより便利で持ち運びができ、旅行にも適していることから、顧客の間で人気が拡大しました。さらに、ガラス瓶に比べて金属缶は安価で、リサイクル率も高いです。

- 近年、パーソナル・ケア用品や製造用品の消費が増加しており、その実用的なパッケージング・ソリューションにより、より広く利用されるようになった。エアゾール缶は、最も効果的な包装の選択肢のひとつであり、保管、輸送、消費者の利便性において優れた性能を発揮します。パーソナルケア&化粧品業界の世界の拡大に伴い、環境に優しい包装缶の需要が急増しています。パーソナルケア製品や化粧品には、日光や空気に反応する敏感な化学成分が含まれているため、エアゾール缶に特別に梱包されています。

- アルミ缶は、競合するパッケージ・タイプよりもリサイクル率が高く、リサイクル含有量も多いです。アルミニウム協会によると、市場で最もリサイクルされている素材のひとつです。2022年4月、ボール社はRecycle Aerosol LLCと提携し、米国におけるアルミ製エアゾール缶のリサイクル率を向上させました。この提携は、エアゾール缶のリサイクル率を向上させるだけでなく、使用済み缶を新しいエアゾール缶にリサイクルするクローズド・ループ・システムを確立しました。リサイクル・アルミニウムからアルミニウム製品を製造することは、エネルギー効率と炭素効率に優れています。アルミエアゾールの製造に使用される合金は非常に純度が高いため、主にリサイクルされたアルミエアゾール・ボトルや缶から得られる場合、バージン・アルミの需要を減らす効率向上もあります。

- 印刷面積が大きく、さまざまなサイズ、スタイル、装飾の選択肢がある円筒形アルミ飲料缶は、重要な場所、つまり棚の上や消費者の手元で強いブランドの存在感を示すのに、理想的なパッケージ・ソリューションです。オーストラリアを拠点とするエナジードリンク・ブランドのレッドブルによると、2022年の世界全体での販売缶数は115億8,000万缶を超え、前年比18.1%増となった。

アジア太平洋が大きなシェアを占めると予想される

- 世界最大のアルミニウム生産国である中国は、2060年までに炭素排出量を正味ゼロにするために生産量を削減しました。そのため、国内生産量の減少を補うためにアルミニウムの輸入が急増しました。この方程式は、ウクライナ・ロシア戦争によって変化しました。天然ガスやその他のエネルギーコストが上昇したため、欧州のアルミニウム生産者は生産を削減し、金属不足を招き、中国と欧州の価格差はほとんどなくなった。

- さらに、中国はロシアに制裁を課していないため、欧州に比べて安価なエネルギーを利用でき、生産コストも削減できました。したがって、予測期間中、アルミニウムを主原料とするエアゾール缶の生産では、中国がコスト面で優位に立つ可能性があります。特筆すべきは、中国では世界の他の地域よりもライバルが少ないため、市場のメーカーにとって大きな成長機会があるということです。

- パーソナルケアおよび化粧品業界の需要の高まりにより、製造業者は環境に優しい包装オプションを提供する必要に迫られています。そのため、研究開発(R&D)努力の高まりとグリーン技術への投資がエアゾール缶市場を後押ししています。中国で最も急成長が期待される経済セクターのひとつが美容・化粧品セクターです。中国国家統計局によると、国内では卸売・小売業による化粧品の小売販売動向が拡大しています。この成長により、シャンプーボトル、クリーム、デオドラント、ヘアスプレー、保湿クリームなどの包装用缶の需要が高まると思われます。

- 環境・森林・気候変動省の報告によると、インド政府は2022年7月、こうした製品による汚染への懸念に対応するため、使い捨てプラスチック製品の禁止を実施しました。使い捨てプラスチックの利用が減少するにつれて、パーソナルケア、ヘルスケア、医薬品、自動車を含むさまざまな事業において、アルミニウムやスチールをベースとした完全にリサイクル可能な金属パッケージング利用への関心が差し迫った時期に高まると思われます。

- ウクライナとロシアの戦争はインドの金属産業を強化し、同国は北米、欧州、MEAの主要国への鉄鋼・鉄の輸出機会を強化しているが、ベースメタルの価格は上昇傾向にあり、製品価格に影響を及ぼしています。

- 食品セクターは、金属缶や容器を使用するインドの主要セクターのひとつです。スチール缶は主に硬い缶に使われ、アルミ缶は薄くて軽い缶に使われます。缶に使用されるほぼすべての鋼鉄は、食品からの腐食を防ぐために錫の薄い層でコーティングされており、錫缶と呼ばれています。インド市場では、食品業界向けの新たな動向が顕著になっています。例えば、インドは主要な農産物・加工食品の輸出国です。商工省によると、特にパンデミックの第二波に起因するCOVID-19規制にもかかわらず、農産物および加工食品の輸出は2021-22年(4-6月)に、2020-21年の対応期間と比較して44.3%の堅調な伸びを達成しました。

- ウクライナ・ロシア戦争が始まって以来、日本経済は新たな局面を迎えています。戦争によって世界経済の先行きに対する懸念が高まっただけでなく、日本などが宣言した一連の経済制裁によって、ロシア経済と(ほぼ)世界の他の地域との格差が拡大しました。日本経済研究センターによると、日本の輸入物価指数は2022年2月に前年比34%増を記録しました。アルミニウムの主要輸入国である日本は、急激な価格上昇に直面しました。そのため、アルミベースのエアゾール缶を製造する企業は、原材料の不足と製品コストに影響する価格高騰に関連した混乱に直面しています。

金属包装業界の概要

金属包装市場は断片化されており、Ball Corporation、Crown Holdings, Inc.、Silgan Holdings, Inc.などの重要なプレーヤーで構成されています。多くの企業が新製品の投入、事業の拡大、戦略的なM&Aを行うことで、市場での存在感を高めています。

2023年1月、持続可能なパッケージング・ソリューションのメーカーであるカンパックは、エミレーツ・世界・アルミニウム(EGA)がドバイで設立したアルミニウム・リサイクル連合に参加しました。カンパックはアラブ首長国連邦(UAE)に重要なアルミ缶製造施設を有しています。アラブ首長国連邦の飲料、廃棄物、アルミニウム分野の主要企業が集まったこの同盟は、アルミニウムのリサイクル率を高めるために、使用済みの飲料用ジャーを最も効果的に再利用する方法を教えています。

2022年12月、クラウン・ホールディングスは、コカ・コーラが製造する爽やかな飲料ブランド「アクエリアス」とその印刷・複写専門スタジオとのコラボレーションによる、スペインでの知的で魅力的な販促キャンペーンを発表しました。対照的に、アクエリアスは標準的な330mlのアルミ缶で販売されていました。この持続可能なパッケージングは、サーキュラー・エコノミー(循環型経済)を先進させ、その無限のリサイクル可能性により、地球から調達する原材料を最小限に抑えることができます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の業界への影響評価

第5章 市場力学

- 市場促進要因

- 金属包装の高いリサイクル率

- 缶詰が提供する利便性と低価格

- 市場の課題

- 代替包装ソリューションの存在

第6章 市場セグメンテーション

- 材料タイプ別

- アルミニウム

- スチール

- 製品タイプ別

- 缶

- 食品缶

- 飲料缶

- エアゾール

- バルク容器

- 輸送用バレルとドラム

- キャップと栓

- その他の製品タイプ

- 缶

- 業界別

- 化粧品・パーソナルケア

- 塗料・ワニス

- その他業界別

- 地域別

- 北米

- 米国

- 英国

- ドイツ

- フランス

- スペイン

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- タイ

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- その他ラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- その他中東とアフリカ

- 北米

第7章 競合情勢

- 企業プロファイル

- Ball Corporation

- Crown Holdings Inc.

- Can-Pack SA

- Silgan Holdings Incorporated

- Tubex GmbH

- Greif Incorporated

- Mauser Packaging Solutions

- Ardagh Group

- DS Containers Inc.

- CCL Container Inc.

- Toyo Seikan Group Holdings Ltd.

第8章 投資分析

第9章 市場の将来

The Metal Packaging Market size is estimated at USD 140.40 billion in 2024, and is expected to reach USD 164.98 billion by 2029, growing at a CAGR of 3.28% during the forecast period (2024-2029).

Key Highlights

- Metal packaging is made mainly of steel, aluminum, and metal. Key benefits of metal packaging include impact resistance, the capacity to withstand severe temperatures, convenience for long-distance shipping, and others. There is a high demand for canned food, particularly in busy urban areas; therefore, the product's rising appeal for this usage encourages consumption. The product's durability and ability to withstand high pressure make it a popular choice in the fragrance industry. Metal-based packaging is also growing as luxury goods like cookies, coffee, tea, and other commodities become increasingly popular in metal packaging.

- Consumer products, cosmetics, healthcare, food & beverage, and other end-use industries rely on metal packaging. Over the anticipated period, the market is expected to increase significantly due to these end-use industries' phenomenal growth. The demand for metal packaging is also influenced by a wide range of other factors, including rising consumer demand for convenience packaging, rising health consciousness, rising "on-the-go" lifestyle trend, rising need for brand enhancement and differentiation in an environment of greater competition, and increasing environmental awareness. Due to this, businesses have adopted new package recycling regulations. The demand for metal packaging is primarily driven by customers' increasing health consciousness.

- Metal packaging is also finding extensive application in the food and beverage industry, as it is suitable for protecting food content, ensuring a longer shelf life than most other packaging solutions. In contrast, heavy-duty metal containers transport oil, chemicals, and liquids, such as drums and IBCs (Intermediate bulk containers). According to the United Nations, the world is urbanizing rapidly; the proportion of people living in urban areas is expected to increase to 66% by 2050. As urbanization is picking up and rising affluence, diet is changing, characterized by a high demand for packaged food. Additionally, excellent preservative properties and structural integrity of the various metal product types, offering higher shelf life, have increased the usage of metal packaging in the food packaging industry.

- In addition, the recyclability of metal packaging is one of the critical elements expected to drive the worldwide metal packaging market over the figure period. Because of the prevalent reusing foundation, aluminum and steel packaging materials are the two most active unrefined components for packaging. Most businesses in Europe and North America prefer to advertise that their products are packed with environmentally friendly materials.

- Moreover, ready or on-the-go meals have also witnessed a steady demand for convenience, especially among consumers with busy lifestyles. Therefore, large organized retailers have started to stack vast canned food and beverages. Nowadays, offline and online retailers stock a wide range of brands of packaged food items in their stores. Metal packaging is suited as containers for beverages as they are easy to cool, great for keeping the contents fresh, and prevent breakages when on the go due to the material's strength.

- Metal packaging faces high competition from alternative packaging solutions. Plastic and glass packaging solutions are the alternative packaging options available in the industry. Also, the increasing importance of e-commerce in Europe is expected to influence the overall packaging industry.

- Consumers have high bargaining leverage in the cosmetics and personal care industry. This is owing to increased competition and the availability of cosmetics from different manufacturers. Because these products are highly substitutable, consumers buying competitors' products can force manufacturers to lower their product prices which is a significant limitation for the aerosol cans market. With increased energy prices, supply chain disruptions during COVID-19 affected the growth of the aluminum industry.

- The war between Russia and Ukraine has resulted in economic sanctions against several countries, high commodity prices, supply chain disruptions, and impacts on many markets worldwide, and caused trade disruptions in the industry. War pushed European aluminum companies to cut production, leading to metal shortages. Commodity traders are competing for scarce profits from shipping aluminum from China as the war in Ukraine has created severe shortages for European manufacturers who rely on Russian supplies. Europe has experienced a surge in energy costs.

Metal Packaging Market Trends

Cans are Expected to Hold a Significant Share

- Metal cans provide many benefits, such as rigidity, stability, and high barrier properties, due to which they are used to store goods that have a longer shelf life and can be transported for longer distances. In Europe, metal cans of tin, steel, and aluminum are preferred. These materials have significant properties, such as being softer and lightweight, so manufacturers can save logistics costs.

- Food packaging in the country has witnessed many innovations since the rise of metal packages. Industrialization has proved to be one of the driving forces behind metal being the first choice of material for the mass commercialization of food products. The food packaging industry has used various materials over the past century, but metals like aluminum have gained the most widespread favor owing to reliable strength and sustainability. Metal cans make the most sense for long-term food storage.

- Young customers are particularly drawn to the bold, vibrant 360-degree designs that have become synonymous with craft beer. The change in consumer perception around the alcoholic can as a premium product for great tasting drinks has impacted growth; also, its overall experience fits in with today's lifestyle. Metal Can alcoholic beverages expanded in popularity among customers since cans are more convenient, portable, and travel-friendly. Furthermore, as compared to glass bottles, metal cans are less expensive and have a much greater recycling rate.

- Consumption of personal care and manufacturing items has increased in recent years, and it is now more widely available due to its practical packaging solution. Aerosol cans are one of the most effective packaging alternatives, offering excellent performance during storage, transportation, and consumer convenience. With the expansion of the personal care & cosmetics industry globally, the demand for eco-friendly packaging cans has surged. As personal care and cosmetic products have sensitive chemical ingredients that are reactive to sun exposure and air, they are packed in aerosol cans specifically.

- Aluminum cans have a higher recycling rate and more recycled content than competing package types. According to the Aluminum Association, it's one of the most recycled materials on the market. In April 2022, Ball Corporation partnered with Recycle Aerosol LLC to boost the recycling rates of aluminum aerosol cans in the United States; the collaboration not only increases aerosol can recycling but also establishes a closed-loop system in which used cans are recycled into new aerosol cans. The production of aluminum goods from recycled aluminum is energy- and carbon-efficient. Because the alloys used to make aluminum aerosols are of such high purity, there are efficiency improvements that also lessen the demand for virgin aluminum when they are mainly derived from recycled aluminum aerosol bottles and cans.

- With a huge printing surface area and various sizes, styles, and decoration choices, cylindrical aluminum beverage cans are the ideal package solution for creating a strong brand presence where it matters - on the shelf and in the hands of consumers. According to Red Bull, an energy drink brand based out of Australia, it sold more than 11.58 billion cans globally in 2022, 18.1% up from the previous year.

Asia-Pacific is Expected to Hold Major Share

- China, the largest aluminum producer in the world, reduced its output to reach net-zero carbon emissions by 2060. Therefore, the country's aluminum imports sharply increased to compensate for the decline in domestic production. The equation has changed due to the Ukraine-Russia war. European aluminum producers cut back on production as natural gas and other energy costs increased, leading to a shortage of metal and a pricing difference of almost between China and Europe.

- Additionally, China has had access to cheaper energy and reduced production costs compared to Europe because it has not imposed sanctions on Russia. Hence, for the forecast period, the country could have the cost advantage for producing aerosol cans, which use aluminum as the primary raw material. Notable, because there is less rivalry in China than in other parts of the world, there is a huge growth opportunity for the manufacturers in the market.

- The personal care and cosmetics industries' growing demand has compelled producers to provide eco-friendly packaging options. Therefore, rising research and development (R&D) efforts and investments in green technologies propel the aerosol cans market. One of the economic sectors in China that are expected to grow the fastest and most soon is the beauty and cosmetics sector. According to the National Bureau of Statistics of China, there is a growing trend of retail sales of cosmetics by wholesale and retail businesses in the country. This growth would consequently bolster the demand for cans for packaging shampoo bottles, creams, deodorants, hair sprays, hydrating creams, and many others.

- The Indian government, as reported by the Ministry of Environment, Forest, and Climate Change, implemented a ban on single-use plastic items in response to concerns about pollution caused by such products in July 2022. With the decrease in the utilization of single-utilized plastic, the interest in aluminum or steel-based, completely recyclable metal packaging use would increment in the impending time frame across different ventures, including personal care, healthcare, pharmaceutical, and automotive.

- Although Ukraine- Russia war has bolstered India's metal industry, and the country has strengthened its export opportunity of steel and Iron to major North American, Europe, and MEA countries, the prices of base metals are gravitating on the higher side, thereby affecting the price of products.

- The food sector is one of India's major sectors using metal cans and containers. Steel is primarily used to make rigid cans, whereas aluminum makes thin, lightweight cans. Nearly all steel used for cans is coated with a thin layer of tin to inhibit corrosion from the food and is called tin cans. The Indian market is witnessing significant emerging trends catering to the food industry. For instance, India is a major agricultural and processed food product exporter. According to the Ministry of Commerce & Industry, despite COVID-19 restrictions, particularly owing to the second wave of the pandemic, agricultural and processed food product exports achieved a robust increase of 44.3% in 2021-22 (April-June) compared to the corresponding period in 2020-21.

- Japan's economy has entered a new phase since the beginning of the Ukraine-Russia war. Not only did the war heighten concerns about the future of the global economy, but also a series of economic sanctions declared by Japan and others have widened the gap between the Russian economy and (nearly) the rest of the globe. According to the Japan Center for Economic Research, the country's import price index recorded a year-over-year increase of 34% in February 2022. Japan, a major importer of aluminum, faced a sudden price rise. Thereby the companies manufacturing aluminum-based aerosol cans face disruption related to the shortage of raw materials and escalated prices impacting the cost of the product.

Metal Packaging Industry Overview

The metal packaging market is fragmented, consisting of significant individual players such as Ball Corporation, Crown Holdings, Inc., Silgan Holdings, Inc., etc. Many companies are increasing their market presence by introducing new products, expanding their operations, or entering into strategic mergers and acquisitions.

In January 2023, CANPACK, a manufacturer of sustainable packaging solutions, joined the Aluminium Recycling Coalition, which was established in Dubai by Emirates Global Aluminium (EGA). CAN PACK has a significant aluminum can manufacturing facility in the United Arab Emirates (UAE). This Alliance, which brought together key players in the UAE's beverage, waste, and aluminum sectors, teaches people how to reuse used beverage jars most effectively to increase aluminum recycling rates.

In December 2022, Crown Holdings, Inc. announced a collaboration with Aquarius, a refreshing beverage brand produced by Coca-Cola and its dedicated print and reprographics studio, on an intelligent and engaging promotional campaign in Spain. In contrast, Aquarius was available in standard 330ml aluminum cans. This sustainable packaging format advanced a Circular Economy and helps minimize the raw materials required to be sourced from the Earth via its infinite recyclability.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of COVID-19 on the industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 High Recyclability Rates of Metal Packaging

- 5.1.2 Convenience and Lower Price Offered by Canned Food

- 5.2 Market Challenges

- 5.2.1 Presence of Alternate Packaging Solutions

6 MARKET SEGMENTATION

- 6.1 By Material Type

- 6.1.1 Aluminum

- 6.1.2 Steel

- 6.2 By Product Type

- 6.2.1 Cans

- 6.2.1.1 Food Cans

- 6.2.1.2 Beverage Can

- 6.2.1.3 Aerosols

- 6.2.2 Bulk Containers

- 6.2.3 Shipping Barrels and Drums

- 6.2.4 Caps and Closures

- 6.2.5 Other Product Types

- 6.2.1 Cans

- 6.3 By End-user Vertical

- 6.3.1 Beverage

- 6.3.2 Food

- 6.3.3 Industrial

- 6.3.4 Cosmetic and Personal Care

- 6.3.5 Paints and Varnishes

- 6.3.6 Automotive

- 6.3.7 Household

- 6.3.8 Other End-user Verticals

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 United Kingdom

- 6.4.2.2 Germany

- 6.4.2.3 France

- 6.4.2.4 Spain

- 6.4.2.5 Rest of Europe

- 6.4.3 Asia-Pacific

- 6.4.3.1 China

- 6.4.3.2 India

- 6.4.3.3 Japan

- 6.4.3.4 South Korea

- 6.4.3.5 Thailand

- 6.4.3.6 Rest of Asia-Pacific

- 6.4.4 Latin America

- 6.4.4.1 Brazil

- 6.4.4.2 Mexico

- 6.4.4.3 Rest of Latin America

- 6.4.5 Middle East and Africa

- 6.4.5.1 United Arab Emirates

- 6.4.5.2 Saudi Arabia

- 6.4.5.3 South Africa

- 6.4.5.4 Rest of Middle East & Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Ball Corporation

- 7.1.2 Crown Holdings Inc.

- 7.1.3 Can-Pack SA

- 7.1.4 Silgan Holdings Incorporated

- 7.1.5 Tubex GmbH

- 7.1.6 Greif Incorporated

- 7.1.7 Mauser Packaging Solutions

- 7.1.8 Ardagh Group

- 7.1.9 DS Containers Inc.

- 7.1.10 CCL Container Inc.

- 7.1.11 Toyo Seikan Group Holdings Ltd.