|

市場調査レポート

商品コード

1406088

ポリフェニレン:市場シェア分析、産業動向と統計、2024年~2029年の成長予測Polyphenylene - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| ポリフェニレン:市場シェア分析、産業動向と統計、2024年~2029年の成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

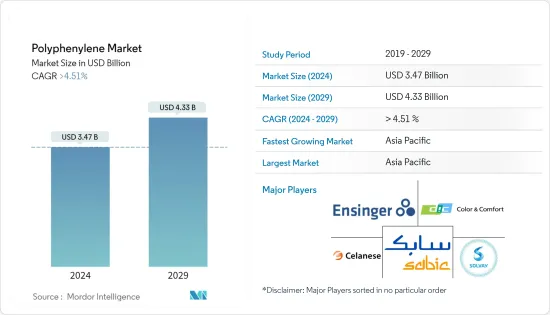

ポリフェニレン市場規模は2024年に34億7,000万米ドルと推定・予測され、2029年には43億3,000万米ドルに達し、予測期間中(2024年~2029年)のCAGRは4.51%以上で成長すると予測されます。

ポリフェニレン市場は、COVID-19の大流行によって生産と移動が停滞し、電気・電子、運輸などの業界が封じ込め対策と経済的混乱によって生産の遅れを余儀なくされるなど、マイナスの影響を受けました。現在、市場はパンデミックから回復しています。市場は2022年にパンデミック以前の水準に達し、今後も安定した成長が見込まれます。

電気・電子産業におけるポリフェニレンの使用量の増加とハイブリッド電気自動車の需要の増加が、調査対象市場の成長を促進する要因となっています。

その反面、ポリフェニレンは他の従来材料に比べて代替品が入手しやすく、コストが高いことが市場の成長を制限する主な要因となっています。

さらに、5G回路基板におけるポリフェニレンの新たな用途は、調査市場にとって有利な機会として作用すると予想される主要因です。

アジア太平洋が市場を独占し、中国、日本、韓国、インドの消費が最大となる見込みです。

ポリフェニレン市場の動向

自動車・輸送分野からの需要増加

- ポリフェニレンは、ポリフェニレンスルフィド(PPS)、ポリフェニレンオキシド(PPO)、ポリフェニレンエーテル(PPE)などの誘導体に加工されます。ポリフェニレン誘導体は、より高い温度安定性が要求される電気自動車部品に好まれます。

- 近年、PPSは、金属、芳香族ナイロン、フェノールポリマー、およびバルク成形化合物に代わって、さまざまなエンジニアリング自動車部品に採用されるようになった。

- ポリフェニレン誘導体は、高温にさらされる自動車部品にとって理想的な選択肢となっています。これらは軽量でありながら高い強度を提供することができます。これらは、電気コネクター、点火システム、照明システム、燃料システム、ハイブリッド車用インバーター部品、ピストンなどの自動車部品に使用されています。

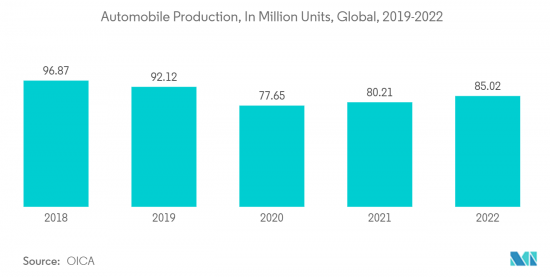

- OICA(Organisation Internationale des Constructeurs d'Automobiles)によると、2022年には世界中で8,502万台の自動車が生産され、2021年比で6%の成長率を記録しました。

- 中国は世界最大の自動車メーカーです。同国の自動車部門は製品の進化を図っており、環境問題への関心の高まりから、排ガスを最小限に抑えながら燃費を確保する製品の製造に注力しています。

- OICAによると、2022年の同国の自動車生産台数は2,702万1,000台、自動車販売台数は2,686万4,000台に達し、前年比3.4%増、2.1%増となった。

- さらに、世界の電気自動車市場は大幅に拡大しており、これが調査対象市場に利益をもたらしています。例えば、2022年には、バッテリー電気自動車(BEV)とプラグインハイブリッド電気自動車(PHEV)が全世界で約1,050万台販売され、前年の677万台に比べて55%の成長率を示しています。

- 以上のような要因によって、自動車・輸送分野におけるポリフェニレンの需要が大幅に増加し、市場セグメンテーションの成長が促進されるものと思われます。

アジア太平洋が市場を独占する

- ポリフェニレンの最大市場はアジア太平洋です。中国、日本、韓国、インドなどの国々では、自動車・輸送、電気・電子などの産業が成長しているため、ポリフェニレンの需要が増加しています。

- アジア太平洋地域では、各国政府が電気自動車の導入や電気自動車製造インフラの拡大に向けて好意的な政策を採用しています。このことは、予測期間中、同地域の電気自動車市場に大きな刺激を与えると予想されます。

- 中国政府の政策展開には、新たな内燃機関車製造工場への投資制限や、2025年までに小型乗用車の平均燃費を引き締めるという提案が含まれます。

- アジア諸国の生活水準が向上していることも、電気自動車やハイブリッド車の利用に対する人々の意識の高まりにつながっています。

- アジア太平洋地域は、中国、日本、韓国、マレーシアといった国々が貢献する電気・電子機器の世界の生産地でもあります。インドもまた、アジアにおける電子製品の製造拠点として台頭してきています。このように確立された産業は、この地域のポリフェニレンとその誘導体の需要を引きつけると予想されます。

- このように、電気・電子産業における使用量の増加と応用範囲の拡大は、市場の成長を促進すると予想されます。エレクトロニクス分野では、中国メーカーが国際市場進出のために海外生産拠点を設立しています。

- 例えば、2023年3月、TCLは海外に工場を設立し、ベトナム、マレーシア、メキシコ、インドでテレビ、モジュール、太陽電池を生産することで、国際市場でのプレゼンスを拡大しました。さらに、ブラジルの現地企業とパートナーシップを結び、生産施設、サプライチェーン、研究開発インフラを共同で開発しています。

- さらに、電子情報技術省によると、インド全土の消費者向け電子機器(テレビ、アクセサリー、オーディオ)の生産額は、2022年度に7,450億インドルピー(94億6,000万米ドル)を超えます。このことが市場の成長を支えています。

- さらに、日本電子情報技術産業協会(JEITA)によると、日本のエレクトロニクス産業による2022年の国内生産額は11兆1,243億円(851億9,000万米ドル)と推定され、前年比2%の成長率を示しています。

- このように、上記のエンドユーザーからの需要増加がアジア太平洋地域の成長を牽引すると予想されます。

ポリフェニレン産業の概要

ポリフェニレン市場は部分的に細分化されています。調査対象市場の主要企業(順不同)には、SABIC、Ensinger、Celanese Corporation、DIC CORPORATION、Solvayなどが含まれます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 電気・電子産業における用途の拡大

- ハイブリッド電気自動車からの需要増加

- その他の促進要因

- 抑制要因

- 代替品の入手可能性

- その他の阻害要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(市場規模)

- タイプ

- ポリフェニレンスルフィド

- ポリフェニレンオキシド

- ポリフェニレンエーテル

- エンドユーザー産業

- 電気・電子

- 自動車・輸送

- その他のエンドユーザー産業(コーティングなど)

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 北米

- 米国

- メキシコ

- カナダ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業が採用した戦略

- 企業プロファイル

- Biesterfeld AG

- Celanese Corporation

- Chevron Phillips Chemical Company LLC

- DIC Corporation

- Emco Industrial Plastics

- Ensinger

- KUREHA CORPORATION

- LG Chem

- Mitsubishi Chemical Group of companies

- Nagase America LLC

- RTP Company

- SABIC

- Solvay

- Sumitomo Bakelite Co., Ltd.

- TORAY INDUSTRIES, INC.

- Tosoh Europe B.V.

第7章 市場機会と今後の動向

- 5G回路基板におけるアプリケーション

- その他の機会

The Polyphenylene Market size is estimated at USD 3.47 billion in 2024, and is expected to reach USD 4.33 billion by 2029, growing at a CAGR of greater than 4.51% during the forecast period (2024-2029).

The polyphenylene market was negatively impacted by the COVID-19 pandemic as there was a slowdown in production and mobility, wherein industries such as electrical and electronics, transportation, and others were forced to delay their production due to containment measures and economic disruptions. Currently, the market has recovered from the pandemic. The market reached pre-pandemic levels in 2022 and is expected to grow steadily in the future.

The growing usage of polyphenylene in the electrical and electronics industry and increasing demand for hybrid electric vehicles are the factors driving the growth of the studied market.

On the flip side, the availability of substitutes and the high cost associated with polyphenylene over other conventional materials are key factors limiting the growth of the market studied.

Moreover, the emerging applications of polyphenylene in 5G circuit board is a key factor expected to act as a lucrative opportunity for the studied market.

Asia-Pacific is expected to dominate the market, with the largest consumption from China, Japan, South Korea, and India.

Polyphenylene Market Trends

Increasing Demand from Automotive and Transportation Segment

- Polyphenylene is processed into its derivatives, like polyphenylene sulfide (PPS), polyphenylene oxide (PPO), and polyphenylene ether (PPE). Polyphenylene derivatives are preferred in electric auto parts that require higher temperature stability.

- In recent years, PPS successfully replaced metal, aromatic nylons, phenolic polymers, and bulk molding compounds in various engineered vehicle components.

- Polyphenylene derivatives become the ideal choice for automotive parts exposed to high temperatures. These can provide high strength while being light in weight. These are used in vehicle components, like electrical connectors, ignition systems, lighting systems, fuel systems, hybrid vehicle inverter components, and pistons.

- According to the Organisation Internationale des Constructeurs d'Automobiles(OICA), 85.02 million vehicles were produced across the globe in 2022, witnessing a growth rate of 6% compared to 2021, thereby enhancing the demand for polyphenylene derivatives, which are employed for various automotive parts.

- China is the largest manufacturer of automobiles in the world. The country's automotive sector has been shaping up for product evolution, with the country focusing on manufacturing products to ensure fuel economy while minimizing emissions, owing to the growing environmental concerns.

- According to OICA, automobile production and sales in the country reached 27.021 million and 26.864 million, respectively, in 2022, up 3.4% and 2.1% from the previous year.

- Further, the global electric vehicle market is expanding significantly which is benefitting the market studied. For instance, in 2022, around 10.5 million units of battery electric vehicles (BEVs) and plug-in hybrid electric vehicles (PHEVs) were sold across the globe, witnessing a growth rate of 55% compared to 6.77 million units sold in the previous year.

- All factors above are likely to significantly enhance the demand for polyphenylene in the automotive and transportation segment, and thus will propel the growth of the market studied.

Asia-Pacific to Dominate the Market

- Asia-Pacific represents the largest market for polyphenylene. In countries like China, Japan, South Korea, and India, the demand for polyphenylene has been increasing due to growing industries like automotive and transportation and electrical and electronics.

- In the Asia-Pacific region, the governments have adopted favorable policies toward the adoption of electric vehicles and the expansion of manufacturing infrastructure for electric vehicles. This, in turn, is anticipated to provide a huge impetus to the electric vehicle market in the region during the forecast period.

- The Chinese government policy developments include the restriction of investments in new ICE-vehicle manufacturing plants and a proposal to tighten the average fuel economy of its light-duty passenger vehicle fleet by 2025.

- Increasing standards of living in Asian countries have also led to increased awareness among the people of the use of electric and hybrid vehicles.

- The Asia-Pacific region is also the dominant producer of electrical and electronics across the world, with countries such as China, Japan, South Korea, and Malaysia contributing toward it. India is also emerging as a manufacturing hub for electronic products in Asia. This established industry is expected to attract demand for polyphenylene and its derivatives from the region.

- Thus, the increasing usage and widening arena of application in the electrical and electronics industry is expected to drive market growth. In the electronics segment, Chinese manufacturers are setting up overseas production bases in order to expand in the international markets.

- For instance, In March 2023, TCL broadened its presence in international markets by establishing factories abroad, producing televisions, modules, and photovoltaic cells in Vietnam, Malaysia, Mexico, and India. In addition, it has formed partnerships with local companies in Brazil to collaboratively develop production facilities, supply chains, and an R&D infrastructure.

- Further, according to the Ministry of Electronics and Information Technology, the production value of consumer electronics (TV, accessories, and audio) across India was above INR 745 billion (USD 9.46 billion) in fiscal year 2022. Thus supporting the growth of the market.

- Moreover, as per the Japan Electronics and Information Technology Industries Association (JEITA), the domestic production by the Japanese electronics industry was estimated at JPY 11,124.3 billion (USD 85.19 billion) in 2022, witnessing a growth rate of 2% compared to the previous year.

- Thus, rising demand from the end-user mentioned above industries is expected to drive growth in the Asia-Pacific region.

Polyphenylene Industry Overview

The polyphenylene market is partially fragmented in nature. The major players in the studied market (not in any particular order) include SABIC, Ensinger, Celanese Corporation, DIC CORPORATION, and Solvay, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Usage in Electrical and Electronics Industry

- 4.1.2 Increasing Demand from Hybrid Electric Vehicles

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Availability of Substitute

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Polyphenylene Sulfide

- 5.1.2 Polyphenylene Oxide

- 5.1.3 Polyphenylene Ether

- 5.2 End-user Industry

- 5.2.1 Electrical and Electronics

- 5.2.2 Automotive and Transportation

- 5.2.3 Other End-user Industries (Coatings, Etc.)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Mexico

- 5.3.2.3 Canada

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers & Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Biesterfeld AG

- 6.4.2 Celanese Corporation

- 6.4.3 Chevron Phillips Chemical Company LLC

- 6.4.4 DIC Corporation

- 6.4.5 Emco Industrial Plastics

- 6.4.6 Ensinger

- 6.4.7 KUREHA CORPORATION

- 6.4.8 LG Chem

- 6.4.9 Mitsubishi Chemical Group of companies

- 6.4.10 Nagase America LLC

- 6.4.11 RTP Company

- 6.4.12 SABIC

- 6.4.13 Solvay

- 6.4.14 Sumitomo Bakelite Co., Ltd.

- 6.4.15 TORAY INDUSTRIES, INC.

- 6.4.16 Tosoh Europe B.V.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Applications in 5G Circuit Board

- 7.2 Other Opportunities