|

市場調査レポート

商品コード

1444710

スマートメーター:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Smart Meters - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| スマートメーター:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 276 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

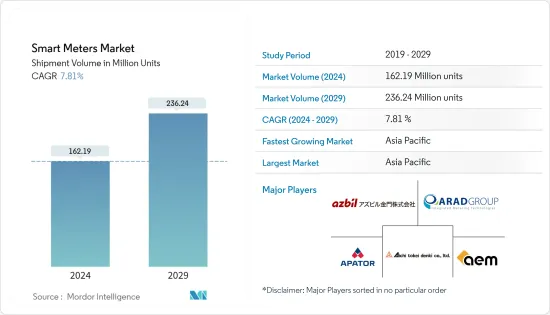

出荷量の観点からのスマートメーター市場規模は、予測期間(2024年から2029年)中に7.81%のCAGRで、2024年の1億6,219万台から2029年までに2億3,624万台に成長すると予想されています。

電力ネットワークの有効性を高めるために、スマートグリッドが世界中で導入されています。その結果、スマート電力メーターを含むスマートグリッドが世界中で導入されています。環境に対する汚染の悪影響と闘うために、世界中の国が排出規制規則を制定しています。これが市場を動かす主な要因です。

主なハイライト

- スマートメーターは、その双方向通信機能により、電気、ガス、水道などのさまざまな導入に世界中で広く採用されています。この機能により、公共事業の供給者と消費者の両方が公共事業の使用状況をリアルタイムで追跡できるようになり、供給者がリモートで供給を開始、読み取り、または停止することが奨励されます。

- 家庭用電化製品、オフィス機器、その他のプラグ負荷は、主モードではないときに、住宅および商用電力の合計のほぼ15%~20%を消費します。このエネルギーのほとんどは、低電力モードで動作するときに(使用されていないときでも)消費されます。消費者は、そのようなシナリオを追跡するためにスマートエネルギー管理システムをインストールする傾向がますます高まっています。

- スマートメーターの導入により、個々の住宅や建物全体の電力使用量を見える化するホームエネルギー管理システム(HEMS)やビルエネルギー管理システム(BEMS)の導入も可能になります。

- さらに、デジタル化はエネルギー効率対策の加速と最新化を進めており、これにより、供給を動的に最適化し、太陽光発電などの再生可能エネルギー源からの大量の電力供給を促進できるスマートグリッドの導入が世界的に増加しています。

- さらに、政府の支援と投資の増加により、国内でのスマートメーターの導入と展開が促進されると予想されます。たとえば、インドの国営エネルギー効率サービス株式会社(EESL)は、インド政府のスマートメーター国家プログラムに基づいて、インド全土で約100万台のスマートメーターの設置を完了しました。 EESLは、今後数年間で2,500万台のスマートメーターを設置するという目標を設定しました。また、独占を排除し、全国に設置される適切な数のメーターを適切に供給するために、国内にスマート電力メーターの製造拠点を設立する必要性も大きな推進力となると予想されます。

- COVID-19の世界の流行によって引き起こされたロックダウンにより、多くの業界で多くの業務が停止しました。その結果、スマートメーターの出荷台数や設置台数が減少しました。

- ただし、COVID-19の要件が段階的に緩和されるにつれて、時間の経過とともにスマートメーターの設置も増加すると予想されます。エネルギープロバイダーの多くは、多くの先進地域でスマートメーターに更新するよう消費者に容易に奨励しています。

スマートメーター市場動向

スマート電力メーターが市場を独占し、予測期間中その優位性は継続する

- 政府の支援と投資の拡大により、アジア太平洋地域でのスマートメーターの導入と展開が加速すると予想されます。独占を防ぎ、地域全域に設置可能なスマート電力メーターを適切に供給するためには、地域内に製造拠点を設けることも必要です。州政府はスマートメーターを3年以内に導入するよう求められ、電力および再生可能エネルギー部門に約2,200億ルピー(約26億7,700万米ドル)の割り当てを受けました。

- GSMAによると、2025年までに北米、主に米国とカナダに約14億のスマートビルディングと7億戸のスマートホームが設置されると予想されており、スマートビルディングとスマートホームの数の増加により、スマートハウスの数も増加すると予想されます。スマート電力メーターの販売。

- さらに、都市化の進行と都市型ライフスタイルの発展に重点を置く傾向の高まりにより、無駄を避けるための電気、光、エネルギーの自動制御を含むスマートホーム技術とデバイスの導入が拡大しました。したがって、世界中の家庭でスマートホームデバイスとテクノロジーの採用が増加しており、住宅分野でのスマートメーターの成長がさらに促進されることが予想されます。

- 家庭用電化製品、オフィス機器、その他のプラグ負荷は、主モードではないときに、住宅および商用電力の合計のほぼ15%~20%を消費します。このエネルギーのほとんどは、低電力モードで動作するときに(使用されていないときでも)消費されます。消費者は、そのようなシナリオを追跡するためにスマートエネルギー管理システムをインストールする傾向が高まっています。

- エネルギー情報局(EIA)によると、世界の発電容量は今後30年間で2倍以上に増加し、2050年までに約14.7テラワットに達すると予想されています。2020年の世界の設置電力容量は7.1テラワットであり、これは需要の増加を示しています。なぜなら、世界中の電力は継続的に増加しているからです。電力会社がエネルギー供給ネットワークを管理し、最適化する必要性が高まっています。したがって、消費者がスマート電力メーターを使用してエネルギー使用量を削減し、お金を節約する機会を特定するのに役立つエネルギー消費に関する詳細な情報が入手可能になると、スマート電力メーターの採用が世界中で増加すると予測されます。

アジア太平洋が大きなシェアを握る

- 中国は現在、アジア太平洋地域の主要セグメントであり、このプロセスを推進している中国唯一の送電会社である華南政府とステートグリッド政府による厳格な命令により、展開はピークに達しています。しかし、中国は現在完全配備に近づいており、打ち上げの段階的な終了により年間需要が大幅に減少することになります。

- 中国はスマート電力メーターの大手メーカーであり、現地企業の存在感が強いです。同社はまた、展開段階では家庭用に消費されていたスマート電気メーターの最大のメーカーの1つです。中国市場は国有企業が独占しています。したがって、中国以外の企業がこの国で競争することはほぼ不可能です。

- 日本は世界で第5位の二酸化炭素排出国です。 2021年、日本政府は多くの環境団体や欧州諸国からの圧力を受けて、2030年までに排出量を46%削減すると約束しました。スマートグリッドの導入、強化された電力および配電ネットワーク、低炭素エネルギー源がこの目標の達成に役立つと考えられます。

- その時までに、日本では、政府からの強力な支援、規制緩和、そしていくつかの大規模プロジェクトによるコストの一般的な低下により、スマートグリッド技術に対する投資家の関心が大幅に高まっているように見えました。 Asian Powerの記事によると、2024年までに全国に最大8,000万個のスマートメーターが設置されると予想されています。

- これらの改善は主に、スマート電力メーター、DES、およびエネルギー貯蔵技術の導入によってもたらされましたが、多数のパイロットプロジェクトや、仮想発電所(VPP)、ブロックチェーン、および車両間送電網(V2G)技術などの他のイノベーションへの発展も見られました。さらに、日本政府は、国の二酸化炭素排出量を削減するための新しい送電網技術、省エネ住宅、その他の技術への投資促進に20兆円(1,550億米ドル)を支出する予定です。

- 残りのアジア太平洋地域には、ニュージーランド、インド、オーストラリア、フィリピン、インドネシア、タイ、韓国、マレーシア、シンガポール、ベトナム、バングラデシュ、パキスタンなどの国や大陸が含まれます。いくつかの政府の取り組み、パートナーシップ、イノベーション、買収により、予測期間中にこの地域の市場成長が促進されると予想されます。

スマートメーター業界の概要

スマートメーター市場は競争が激しく、AEM、愛知時計電機、Apator SA、Arad Group、Azbil Kimmonなどの大手プレーヤーで構成されている大規模投資の関与により、既存プレーヤーの障壁が高まり、業界を押し上げている競合に向けて。また、スマートメーターはさまざまなエンドユーザーによって導入されることが増えています。したがって、需要の大幅な増加と、さまざまな地域での展開数を増やすための政府の取り組みにより、市場参加者間の競合の度合いが高まることが予想されます。

2023年 1月、Badger Meter Inc.は、インテリジェントな水監視ソリューションのプロバイダーであるSyrinix Ltd.の戦略的買収を発表しました。同社はこの買収を通じて、Syrinixのハードウェア対応ソフトウェア機能を当社のスマートウォーターソリューションポートフォリオに追加することを目指しています。同様に、インテリジェント測定とスマート水質監視のリーダーであるAnalytical Technology, Inc.(Ati)とScan GmbHも買収しました。

2023年 1月、Diehl Stiftung &Co. KGは、ルワンダの首都キガリにある水道衛生公社(WASAC)が持続可能性への取り組みのためネットワークを最新化するためのメーター技術としてDiehl Meteringを選択したと発表しました。 WASACは、信頼性の高いメーターを設置することで無収水を削減するという主な目的を達成するためにAURIGAが適切であることを認めました。 AURIGA水道メーターは、将来のAMRソリューションの基礎を形成します。

2022年 12月、Apator SAは、産業用途向けに特別に設計されたsmartESOX proと、双方向スマート電力メーターであるOTUS 3を発表しました。 Ultrimis W超音波水道メーターやiSMART2ガスメーターなど、その他のスマートなオプションも紹介されました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替製品の脅威

- 競合の程度

- 業界のバリューチェーン分析

- COVID-19の業界への影響

第5章 市場力学

- 市場促進要因

- スマートグリッドプロジェクトへの投資の増加

- 光利用効率の向上の必要性

- 政府の支援規制

- スマートシティ導入の成長

- すべてのエンドユーザーに対する持続可能なユーティリティ供給の需要

- 市場の課題

- 高コストとセキュリティ上の懸念

- スマートメーターとの統合の難しさ

- インフラ設置のための設備投資の不足とROIの不足

- 公共事業会社の切り替えコスト

第6章 市場セグメンテーション

- 地域別- スマートガスメーター

- 北米

- 米国

- カナダと中米

- 欧州

- 英国

- フランス

- イタリア

- その他欧州

- アジア太平洋地域

- 中国

- 日本

- その他アジア太平洋地域

- 世界のその他の地域

- 北米

- 地域別- スマート水道メーター

- 北米

- 米国

- カナダと中米

- 欧州

- 英国

- フランス

- イタリア

- その他欧州

- アジア太平洋

- 中国

- 日本

- その他アジア太平洋地域

- 世界のその他の地域

- 北米

- 地域別- スマート電力メーター

- 北米

- 米国

- カナダと中米

- 欧州

- 英国

- フランス

- イタリア

- その他欧州

- アジア太平洋地域

- 中国

- 日本

- その他アジア太平洋地域

- 世界のその他の地域

- 北米

第7章 競合情勢

- 企業プロファイル

- AEM

- Aichi Tokei Denki Co.Ltd.

- Apator SA

- Arad Group

- Azbil Kimmon Co. Ltd.

- Badger Meter Inc.

- Diehl Stiftung &Co. KG

- Elster Group GmbH(Honeywell International Inc.)

- General Electric Company

- Hexing Electric company Ltd.

- Holley Technology Ltd.

- Itron Inc.

- Jiangsu Linyang Energy Co. Ltd.

- Kamstrup A/S

- Landis+GYR Group AG

- Mueller Systems LLC(Muller Water Products Inc.)

- EDMI Limited(OSAKI ELECTRIC CO. LTD.)

- Neptune Technology Group Inc.(Roper Technologies, Inc.)

- Ningbo Sanxing Medical Electric Co., Ltd

- Pietro Fiorentini SpA

- Sagemcom SAS

- Sensus USA Inc.(Xylem Inc.)

- Aclara Technologies LLC(Hubbell Inc.)

- Wasion Holdings Limited

- Yazaki Corporation

- Zenner International GmbH &Co. KG

第8章 市場機会と将来の動向

- 市場の将来- スマート電力メーター

- 市場の将来- スマートガスメーター

- 市場の将来- スマート水道メーター

The Smart Meters Market size in terms of shipment volume is expected to grow from 162.19 Million units in 2024 to 236.24 Million units by 2029, at a CAGR of 7.81% during the forecast period (2024-2029).

In order to increase the effectiveness of electrical networks, smart grids are being introduced all over the world. As a result, smart grids, which include smart electricity meters, are being deployed globally. To combat the negative impacts of pollution on the environment, nations all over the world are enacting emission control rules. This is the main factor driving the market.

Key Highlights

- Due to their two-way communication capability, smart meters are being adopted more widely across the globe for various deployments, including electricity, gas, and water. This feature allows both utility suppliers and consumers to track utility usage in real-time and encourages suppliers to start, read, or cut off supply remotely.

- Consumer electronics, office equipment, and other plug loads consume nearly 15% to 20% of the total residential and commercial electricity while not in the primary mode. Most of this energy is consumed when they operate in low-power modes (even while they are not in use). Consumers are increasingly tending to install a smart energy management system to track such scenarios.

- Smart meters deployment also enables the implementation of a Home Energy Management System (HEMS) or Building Energy Management System (BEMS) that allows visualization of the electric power usage in individual homes or entire buildings.

- Further, digitization is accelerating and modernizing energy efficiency measures, due to which the deployment of smart grids is increasing globally, as they are capable of dynamically optimizing supply and fostering supply of large amounts of electricity from renewable energy sources such as solar power.

- Moreover, increasing government support and investments are expected to boost smart meters adoption and deployment in the country. For instance, India's state-owned Energy Efficiency Services Limited (EESL) completed the installation of approximately 10 lakh smart meters across India under the Government of India's Smart Meter National Programme. EESL set the target to install 25 crore smart meters over the next few years. Also, the need to establish a manufacturing base of smart electricity meters in the country to ensure an adequate supply of an adequate number of meters to be installed all over the country, by ruling out monopoly, is expected to act as a major driver.

- Lockdowns caused by the global COVID-19 epidemic caused a number of operations in many industries to come to a standstill. As a result, there was a decline in smart meter shipments and installations.

- However, as the COVID-19 requirements are gradually relaxed, it is anticipated that over time, the installation of smart meters will rise as well. The majority of energy providers are easily encouraging their consumers to update to smart meters in many developed locations.

Smart Meters Market Trends

Smart Electricity Meter Dominates the Market and will Continue its Dominance Over the Forecast Period

- Greater government support and investments are anticipated to accelerate the adoption and deployment of smart meters in Asia and the Pacific. In order to prevent monopolies and ensure an adequate supply of smart electricity meters that can be installed throughout the region, it is also necessary to establish a manufacturing base in the area. The state governments were urged to implement smart meters in three years and received an allocation of about INR 2,20,000 million (USD 2.677 billion) for the power and renewable energy sectors.

- According to the GSMA, by 2025, around 1.4 billion smart buildings and 700 million smart homes are expected to be in North America, mainly the United States and Canada, so an increasing number of smart buildings and homes are expected to also lead to an increase in the sale of smart electricity meters.

- Moreover, increasing urbanization and the increasing inclination toward a focus on developing urban lifestyles led to the expansion of the deployment of smart home technologies and devices, which involve automatic control of electricity, light, and energy to avoid wastage. Hence, the increasing adoption of smart home devices and technologies across homes globally is further expected to foster the growth of smart meters in the residential segment.

- Consumer electronics, office equipment, and other plug loads consume nearly 15% to 20% of the total residential and commercial electricity while not in the primary mode. Most of this energy is consumed when they operate in low-power modes (even while they are not in use). Consumers are increasingly inclined to install a smart energy management system to track such scenarios.

- According to the Energy Information Administration (EIA), global electricity generation capacity is expected to more than double in the next three decades, reaching approximately 14.7 terawatts by 2050. In 2020, the world's installed electricity capacity stood at 7.1 terawatts, which shows the demand for electricity around the globe is growing continuously. There is a growing need for utilities to manage and optimize their energy distribution networks. Thus, the availability of detailed information about energy consumption, which can help the consumer identify opportunities to reduce energy usage and save money with smart electricity meters, is projected to increase the adoption of smart electricity meters globally.

Asia-Pacific to Hold Major Share

- China is currently the leading segment in Asia Pacific, with the rollout at its peak due to strict mandates by the government of South China and State Grid, the only two grid companies in the country that drive the process. However, China is currently approaching full deployment, and the gradual end of the launch results in a significant reduction in annual demand.

- China is a major manufacturer of smart electricity meters, with a strong presence of local companies. It is also one of the largest producers of smart electric meters, which were consumed for domestic purposes during the rollout phase. State-owned enterprises dominate the Chinese market. Thus, it is nearly impossible for non-Chinese companies to compete in the country.

- Japan is the fifth-largest carbon emitter in the world. In 2021, the Japanese government promised to reduce emissions by 46% by 2030 due to pressure from many environmental organizations and European nations. Smart grid implementation, enhanced power and distribution networks, and low-carbon energy sources will likely help achieve this objective.

- By then, investor interest in smart grid technology was seen to have significantly increased in Japan due to the country's strong backing from the government, deregulation, and generally declining costs, with several large-scale projects. According to an Asian Power article, it is anticipated that up to 80 million smart meters will be installed nationwide by 2024.

- These improvements have mainly resulted from deploying smart electricity meters, DES, and energy storage technologies but have also seen numerous pilot projects and developments into other innovations like virtual power plants (VPPs), blockchain, and vehicle-to-grid (V2G) technologies. Additionally, the Japanese government plans to spend JPY 20 trillion (USD 155 billion) on promoting investments in new power grid technology, energy-saving homes, and other technology to reduce the nation's carbon footprint.

- The rest of the Asia-Pacific region contains countries and continents like New Zealand, India, Australia, the Philippines, Indonesia, Thailand, South Korea, Malaysia, Singapore, Vietnam, Bangladesh, Pakistan, and many more. Several government initiatives, partnerships, innovations, and acquisitions are expected to fuel market growth in the region during the projected period.

Smart Meters Industry Overview

The smart meter market is highly competitive and consists of several major players such as AEM, Aichi Tokei Denki Co., Ltd., Apator SA, Arad Group, and Azbil Kimmon Co., Ltd. The involvement of large-scale investments is increasing the barriers for the existing players, thereby pushing the industry toward competition. Also, smart meters are increasingly being deployed by various end users. Hence, the substantial increase in demand and government initiatives to increase the number of rollouts in various regions are expected to increase the degree of competition among the market players.

In January 2023, Badger Meter Inc. announced the strategic acquisition of Syrinix Ltd., a provider of intelligent water monitoring solutions. Through this acquisition, the company aims to add the hardware-enabled software capabilities of Syrinix to our smart water solutions portfolio. Similarly, it has also acquired Analytical Technology, Inc. (Ati) and Scan GmbH, leaders in intelligent measurement and smart water quality monitoring.

In January 2023, Diehl Stiftung & Co. KG announced that the Water and Sanitation Corporation (WASAC) in Rwanda's capital, Kigali, chose Diehl Metering for meter technology to modernize its network for its sustainability efforts. WASAC recognized the suitability of AURIGA to achieve its primary objective of reducing non-revenue water by installing reliable meters. The AURIGA water meter will form the basis for a future AMR solution.

In December 2022, Apator SA presented the smartESOX pro, which was specially designed for industrial applications, and the OTUS 3, a bidirectional smart electricity meter. Other smart options were presented, such as the Ultrimis W ultrasonic water meter and the iSMART2 gas meter.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Degree of Competition

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increased Investments in Smart Grid Projects

- 5.1.2 Need for Improvement in Utility Efficiency

- 5.1.3 Supportive Government Regulations

- 5.1.4 Growth in Smart City Deployment

- 5.1.5 Demand for Sustainable Utility Supply for All End Users

- 5.2 Market Challenges

- 5.2.1 High Costs and Security Concerns

- 5.2.2 Integration Difficulties with Smart Meters

- 5.2.3 Lack of Capital Investment for Infrastructure Installation and Lack of ROI

- 5.2.4 Utility Supplier Switching Costs

6 MARKET SEGMENTATION

- 6.1 By Geography - Smart Gas Meter

- 6.1.1 North America

- 6.1.1.1 United States

- 6.1.1.2 Canada and Central America

- 6.1.2 Europe

- 6.1.2.1 United Kingdom

- 6.1.2.2 France

- 6.1.2.3 Italy

- 6.1.2.4 Rest of Europe

- 6.1.3 Asia Pacific

- 6.1.3.1 China

- 6.1.3.2 Japan

- 6.1.3.3 Rest of Asia Pacific

- 6.1.4 Rest of the World

- 6.1.1 North America

- 6.2 By Geography - Smart Water Meter

- 6.2.1 North America

- 6.2.1.1 United States

- 6.2.1.2 Canada and Central America

- 6.2.2 Europe

- 6.2.2.1 United Kingdom

- 6.2.2.2 France

- 6.2.2.3 Italy

- 6.2.2.4 Rest of Europe

- 6.2.3 Asia-Pacific

- 6.2.3.1 China

- 6.2.3.2 Japan

- 6.2.3.3 Rest of Asia-Pacific

- 6.2.4 Rest of the World

- 6.2.1 North America

- 6.3 By Geography - Smart Electricity Meter

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada and Central America

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 France

- 6.3.2.3 Italy

- 6.3.2.4 Rest of Europe

- 6.3.3 Asia Pacific

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 Rest of Asia Pacific

- 6.3.4 Rest of the World

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 AEM

- 7.1.2 Aichi Tokei Denki Co.Ltd.

- 7.1.3 Apator SA

- 7.1.4 Arad Group

- 7.1.5 Azbil Kimmon Co. Ltd.

- 7.1.6 Badger Meter Inc.

- 7.1.7 Diehl Stiftung & Co. KG

- 7.1.8 Elster Group GmbH (Honeywell International Inc.)

- 7.1.9 General Electric Company

- 7.1.10 Hexing Electric company Ltd.

- 7.1.11 Holley Technology Ltd.

- 7.1.12 Itron Inc.

- 7.1.13 Jiangsu Linyang Energy Co. Ltd.

- 7.1.14 Kamstrup A/S

- 7.1.15 Landis+ GYR Group AG

- 7.1.16 Mueller Systems LLC (Muller Water Products Inc.)

- 7.1.17 EDMI Limited (OSAKI ELECTRIC CO. LTD.)

- 7.1.18 Neptune Technology Group Inc. (Roper Technologies, Inc.)

- 7.1.19 Ningbo Sanxing Medical Electric Co., Ltd

- 7.1.20 Pietro Fiorentini SpA

- 7.1.21 Sagemcom SAS

- 7.1.22 Sensus USA Inc. (Xylem Inc.)

- 7.1.23 Aclara Technologies LLC (Hubbell Inc.)

- 7.1.24 Wasion Holdings Limited

- 7.1.25 Yazaki Corporation

- 7.1.26 Zenner International GmbH & Co. KG

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 8.1 Future of the Market - Smart Electricity Meter

- 8.2 Future of the Market - Smart Gas Meter

- 8.3 Future of the Market - Smart Water Meter