|

市場調査レポート

商品コード

1443973

臨床栄養:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)Clinical Nutrition - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| 臨床栄養:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 127 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

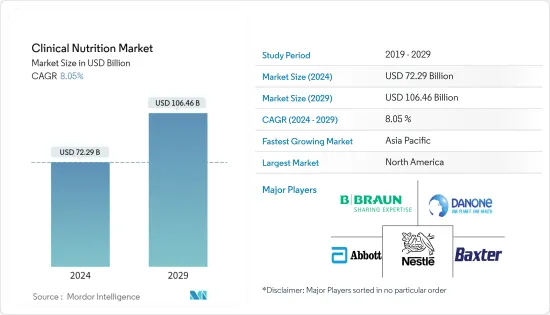

臨床栄養市場規模は2024年に722億9,000万米ドルと推定され、2029年には1,064億6,000万米ドルに達すると予測され、予測期間(2024-2029年)のCAGRは8.05%で成長する見込みです。

COVID-19パンデミックは臨床栄養市場に影響を与えました。さまざまな研究がパンデミックの影響に関する洞察を提供しています。例えば、2021年5月にNational Library of Medicineに掲載された調査研究では、COVID-19で入院した患者における栄養不良の有病率は42%であったと述べられています。したがって、このような高い有病率は、パンデミック時の栄養サポートの欠如についての洞察を与えてくれます。さらに、新たなガイドラインの発行などの取り組みが、予測期間中に市場に成長をもたらすと期待されています。例えば、欧州臨床栄養代謝学会は2021年1月、臨床栄養が感染の予防や感染に伴う栄養不良の治療に重要な役割を果たすとして、COVID-19に感染したICU患者の栄養管理に関連するガイドラインを発行しました。同様に、2021年2月、Tata &Lyle社は、食品メーカーが公衆衛生の課題に対処するのに役立つ成分に関する権威ある科学に簡単にアクセスできる新しいデジタルハブ、Tata &Lyle Nutrition Centreを立ち上げました。このように、この市場は本調査の予測期間中に好影響を与えると予想されます。

臨床栄養市場の成長を後押ししている要因には、代謝異常の有病率の増加、ヘルスケアへの高額支出、新興国における中間層の台頭などがあります。過去10年間で、代謝障害の有病率は増加しています。例えば、2021年11月に更新されたゴーシェ研究所の論文によると、ゴーシェ病は男性でも女性でも同じように有病率が高く、世界の有病率は10万人当たり0.70~1.75人であると報告されています。また、一般人口におけるゴーシェ病の標準出生率は、10万人当たり0.39~5.80人であることも報告されています。このような疾病負担が臨床栄養製品の必要性を生み出し、市場の成長を牽引しています。手術中、臨床栄養は患者の悪影響を最小限に抑え、外科医が制御された環境で作業できるようにする上で大きな役割を果たしています。2022年8月に更新された経済協力開発機構によると、2021年にポルトガル、デンマーク、アイルランド、ノルウェーなどの新興諸国で実施された手術件数(単位:1,000件)には、94.87件、49.33件、32.84件、21.5件が含まれています。このように、疾病負担の増加や手術件数の増加に伴い、臨床栄養市場は予測期間中に盛り上がりを見せると予想されます。

同様に、製品の発売も市場成長の要因の一つです。例えば、2021年8月、Esperer Nutrition社は、骨と関節の健康、免疫、尿路の健康、睡眠時無呼吸症候群、糖尿病予備軍ケアのための一連の消費者向け栄養補助食品を発売しました。このような製品の発売により、臨床栄養の採用が増加し、予測期間中の市場成長が期待されます。したがって、高齢者人口の増加と高齢化社会に特化した臨床栄養製品の開発が市場の成長を押し上げると予想されます。

しかし、臨床栄養に関する不正確な認識や出生率の低下が市場成長の妨げになると予想されます。

臨床栄養市場の動向

予測期間中、経口および経腸投与セグメントが大きな市場シェアを占める見込み

臨床栄養に利用可能なすべての投与経路の中で、経口および経腸経路が最も多く使用され、非経口経路がそれに続いています。これは主に、非経口経路では製品/栄養素の加工に追加コストがかかるためです。他の投与経路が必要と判断されるまでは、他の2つの投与経路に比べ、複雑さやコストが少ない経口経路が主に使用されます。経腸療法には、タンパク質、炭水化物、脂肪、ビタミン、ミネラル、および生きるために必要なその他の栄養素を含む特殊な液体栄養剤が含まれます。これらの栄養サポート製品は、さまざまな病状や状態に対する個々のニーズを満たすように処方されます。これに加えて、臨床栄養の投与に経口経路が使用される疾患状態のほとんどは、慢性疾患および非急性疾患です。2021年にJournal of Nephrology誌に発表された論文によると、末期腎不全(ESRD)の場合、患者には移植(ドナーが見つからないため、必ずしも可能とは限らない;ドナーが見つかった場合でも、数ヶ月から数年かかる場合もある)を選択するか、通常の血液透析を受けるかの2つの選択肢しかありません。このような患者には、クレアチニン、尿酸、ビリルビンなどの排泄産物の産生をコントロールできるように、腎臓への負担を軽減するために、経口・経腸栄養による専門的な臨床栄養が処方されます。主要な市場参入企業による取り組みも、市場成長の一因となっています。例えば、2021年4月にNutiFood社はBASF社と提携し、ヒトミルクオリゴ糖(HMO)製品を生産しました。NutiFoodは、HMOを栄養製品のラインに取り入れるために欧州企業と協力した最初のベトナムの乳製品会社です。これらの製品は経口摂取が可能です。

したがって、上記の要因は、予測期間にわたってこのセグメントの成長に寄与すると予想されます。

北米は臨床栄養市場で大きなシェアを占めており、予測期間中も同じ動向をたどると予想されます。

北米は他の地域と比較して市場成長に大きく貢献しています。COVID-19の出現により、この地域では臨床栄養製品が不足しています。米国非経口・経腸栄養学会(ASPEN)が提供するデータによると、2021年1月現在、マルチビタミン輸液(成人用および小児用)、アミノ酸、酢酸カリウム注射液(USP)、酢酸ナトリウム注射液(USP)、塩化ナトリウム注射液など、特定の非経口製品は現在23.4%が不足しています。

COVID-19の大流行の中、新たな消費者の購買行動によってもたらされた進化する需要に対応するため、メーカーは増産を行い、小売業者や政府機関と協力して、経口臨床栄養製品の十分な供給と継続的な入手の確保に努めています。臨床栄養市場の成長をもたらす主な要因には、代謝障害の有病率の増加があります。例えば、2021年8月に発表されたカナダ政府のプレスリリースによると、糖尿病はカナダ人に影響を及ぼす主要な慢性疾患の1つであり、2021年8月時点で人口の8.8%にあたる300万人以上のカナダ人が糖尿病と診断され、カナダ成人の6.1%が糖尿病を発症するリスクが高いとされています。このような疾患は長期的な臨床栄養サポートを必要とするため、糖尿病のような疾患は予測期間中に市場成長を増加させると予想されます。

したがって、このような事例は臨床栄養製品に対する需要の高まりを示し、それによって市場の成長が促進されます。

臨床栄養業界の概要

市場企業は、大きな市場シェアを獲得し、製品ポートフォリオを強化するために、買収、合併、戦略的提携など、さまざまな無機的成長戦略を通じて存在感の拡大に継続的に取り組んでいます。市場の主要企業には、Abbott Nutrition、Nestle Health Science、Baxter Healthcare、B. Braun SE、Nutriciaなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 代謝疾患の有病率の増加

- ヘルスケアへの高額支出

- 老年人口の増加

- 市場抑制要因

- 臨床栄養に関する不正確な認識

- 出生率の低下

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競合企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 投与経路別

- 経口および経腸

- 非経口

- 用途別

- 栄養不良に対する栄養補給

- 代謝障害の栄養サポート

- 消化器疾患の栄養サポート

- がんに対する栄養サポート

- 神経疾患における栄養サポート

- その他の疾患における栄養サポート

- エンドユーザー別

- 小児

- 成人

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Abbott Laboratories(Abbott Nutrition)

- Nestle Health Science

- Baxter Healthcare

- B. Braun SE

- Danone(Nutricia)

- Perrigo Company PLC

- Fresenius Kabi

- AYMES International Ltd

- Reckitt Benckiser

- Medifood International Ltd

- Ajinomoto Cambrooke Inc.(Nualtra Ltd)

第7章 市場機会と今後の動向

The Clinical Nutrition Market size is estimated at USD 72.29 billion in 2024, and is expected to reach USD 106.46 billion by 2029, growing at a CAGR of 8.05% during the forecast period (2024-2029).

The COVID-19 pandemic had an effect on the clinical nutrition market. Various studies provide insight into the effects of the pandemic. For instance, in May 2021 a research study published in the National Library of Medicine stated that the prevalence of malnutrition was 42% in patients hospitalized with COVID-19. Thus, such high prevalence provides insight into the lack of nutritional support during the pandemic. Moreover, initiatives such as issuing new guidelines are expected to provide growth to the market over the forecast period. For instance, the European Society for Clinical Nutrition and Metabolism issued guidelines in January 2021, related to nutritional management in ICU patients infected with COVID-19, as clinical nutrition played a crucial role in preventing infection and treating infection-associated malnutrition. Similarly, in February 2021, Tata and Lyle launched Tata & Lyle Nutrition Centre, a new digital hub providing easy access to authoritative science on ingredients that would help food manufacturers address public health challenges. Thus, the market is expected to have a favorable impact during the forecast period of the study.

Certain factors are propelling the clinical nutrition growth of the market, including the increasing prevalence of metabolic disorders, high spending on healthcare, and the rise of the middle class in emerging economies. Over the past decade, the prevalence of metabolic disorders has increased. For instance, the Gaucher's Institute article updated in November 2021 reported that Gaucher disease is equally prevalent in males and females and has a worldwide prevalence of 0.70 to 1.75 per 100,000 individuals. The same source also reported that the standardized birth incidence of Gaucher disease within the general population varies from 0.39 to 5.80 per 100,000 individuals. Such a burden of diseases creates the need for clinical nutrition products and thus drives the growth of the market. During surgeries, clinical nutrition plays a major part in minimizing patient adverse consequences and enabling surgeons to work in a controlled environment. According to the Organization for Economic Co-operation and Development updated in August 2022, the number of surgeries (in thousand) performed in some European countries such as Portugal, Denmark, Ireland, and Norway in 2021 include 94.87, 49.33, 32.84, 21.5. Thus, with the rising burden of diseases and the volume of surgeries, the clinical nutrition market is expected to boost during the forecast period.

Similarly, product launches are another factor in market growth. For instance, in August 2021, Esperer Nutrition launched a range of consumer nutraceuticals for bone and joint health, immunity, urinary tract health, sleep apnea, and pre-diabetic care. Such product launches are expected to increase the adoption of clinical nutrition which is expected to increase market growth over the forecast period. Hence, the growing number of the elderly population and the development of clinical nutrition products specific to the aging population are expected to boost market growth.

However, imprecise perceptions about clinical nutrition and reduction in birth rates are expected to hinder the market growth.

Clinical Nutrition Market Trends

Oral and Enteral Segment is Expected to Hold a Significant Market Share Over the Forecast Period

Of the all routes of administration available for clinical nutrition, oral and enteral routes are used the most, followed by the parenteral route. This is mainly because of the additional cost of processing the product/nutrient involved in parenteral routes. Until other routes of administration are deemed necessary, physicians mostly prefer the oral route, as it involves fewer complexities and costs, when compared to the other two routes of administration. Enteral therapy includes specialized liquid feedings containing protein, carbohydrates, fats, vitamins, minerals, and other nutrients needed to live. These nutrition support products are formulated to meet individual needs for a variety of disease states and conditions. In addition to this, most of the disease conditions, for which the oral route is used for the administration of clinical nutrition, are chronic conditions and non-acute conditions. According to the paper published in the Journal of Nephrology in 2021, in the case of end-stage renal disease (ESRD), the patients only have two options: opting for a transplant (which may not always be possible, due to the unavailability of donors; even in cases where a donor is found, it could take anywhere between a few months to several years) or undergoing regular hemodialysis. Specialized clinical nutrition through oral and enteral feeding is prescribed for these patients to reduce the burden on their kidneys, so that the production of excretory products, such as creatinine, uric acid, and bilirubin, is in control. Initiatives by key market players are another factor in market growth. For instance, in April 2021, NutiFood partnered with BASF to produce Human Milk Oligosaccharides (HMO) products. NutiFood is the first Vietnamese dairy company to cooperate with a European corporation to bring HMO into its line of nutrition products. These products can be consumed through oral feeding.

Thus, the above-mentioned factors are expected to contribute to the growth of the segment over the forecast period.

North America Hold Significant Share in the Clinical Nutrition Market and is Expected to Follow the Same Trend over the Forecast Period

North America contributes heavily to the market growth compared to the other regions. The emergence of COVID-19 has led to shortages of clinical nutritional products in this region. As per the data provided by the American Society for Parenteral and Enteral Nutrition (ASPEN), as of January 2021, certain parenteral products, including multi-vitamin infusion (adult and pediatric), amino acids, potassium acetate injection, USP, sodium acetate injection, USP, and sodium chloride, 23.4% of injections are currently at a shortage.

To meet the evolving demands driven by new consumer buying behavior amid the COVID-19 pandemic, manufacturers have increased production and are working with retailers and government agencies to help ensure adequate availability of and continued access to oral clinical nutrition products. Some of the primary factors attributing to the growth of the clinical nutrition market include an increase in the prevalence of metabolic disorders. For instance, as per a press release by the government of Canada published in August 2021, diabetes is one of the major chronic diseases affecting Canadians where over 3 million Canadians, or 8.8% of the population were diagnosed with diabetes and 6.1% of Canadian adults were at high risk of developing diabetes as of August 2021. Such diseases require long-term clinical nutritional support thus, diseases such as diabetes are expected to increase market growth over the forecast period.

Hence, such instances indicate a rising demand for clinical nutrition products, thereby driving market growth.

Clinical Nutrition Industry Overview

The market players are continuously engaged in expanding their presence through various inorganic growth strategies, such as acquisition, merger, and strategic collaboration, to gain significant market share and strengthen their product portfolios. Some of the key players in the market include Abbott Nutrition, Nestle Health Science, Baxter Healthcare, B. Braun SE, and Nutricia among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Prevalence of Metabolic Disorders

- 4.2.2 High Spending on Healthcare

- 4.2.3 Growing Geriatric Population

- 4.3 Market Restraints

- 4.3.1 Imprecise Perception About Clinical Nutrition

- 4.3.2 Reduction in Birth Rates

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD Million)

- 5.1 By Route of Administration

- 5.1.1 Oral and Enteral

- 5.1.2 Parenteral

- 5.2 By Application

- 5.2.1 Nutritional Support for Malnutrition

- 5.2.2 Nutritional Support for Metabolic Disorders

- 5.2.3 Nutritional Support for Gastrointestinal Diseases

- 5.2.4 Nutritional Support for Cancer

- 5.2.5 Nutritional Support in Neurological Diseases

- 5.2.6 Nutritional Support in Other Diseases

- 5.3 By End User

- 5.3.1 Pediatric

- 5.3.2 Adult

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Abbott Laboratories (Abbott Nutrition)

- 6.1.2 Nestle Health Science

- 6.1.3 Baxter Healthcare

- 6.1.4 B. Braun SE

- 6.1.5 Danone (Nutricia)

- 6.1.6 Perrigo Company PLC

- 6.1.7 Fresenius Kabi

- 6.1.8 AYMES International Ltd

- 6.1.9 Reckitt Benckiser

- 6.1.10 Medifood International Ltd

- 6.1.11 Ajinomoto Cambrooke Inc. (Nualtra Ltd)