|

市場調査レポート

商品コード

1248150

高速切削工具市場- 成長、動向、予測(2023年-2028年)High Speed Cutting Tools Market - Growth, Trends, and Forecasts (2023 - 2028) |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| 高速切削工具市場- 成長、動向、予測(2023年-2028年) |

|

出版日: 2023年03月25日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

高速切削工具の市場規模は今年度68億1,000万米ドル、予測期間中のCAGRは3%超と予測されます。

主なハイライト

- 市場の成長は、世界中の自動車、航空宇宙、その他など、いくつかのエンドユーザー産業からの需要の増加が主な要因です。工作機械は、穴あけ、フライス、研削、タップ、ドリルなどの加工に使用され、製造された製品の品質を決定するため、工具は製造工程の重要な部分です。工作機械の世界生産量は、数年の穏やかな時期を経て、爆発的な伸びを見せました。切削加工は工作機械の最終工程に組み込まれるため、工作機械市場の成長に伴い、より多くの工具が必要となります。一般に、HSS切削工具はCNC工作機械に固定され、複雑な製品や形状を開発します。

- 中国は工作機械市場で世界をリードしています。世界的に見ても、成形技術に比べ、工作機械の切削加工部門は生産量において大きなシェアを占めています。

- 高速度鋼(HSS)は、高い加工硬度、耐久性、高い摩耗硬度、硬度保持の良さなどの特性から、切削工具の製造において需要が伸びています。HSSの使用により、従来使用されていた炭素鋼に比べ、切削速度が4倍に向上しています。メーカーにとって、効率的で信頼性の高い機械加工へのニーズは高まっています。上記のような特性から、黄銅製切削工具は量産品や高温作業への道を歩んでいます。また、顧客満足度と製品品質への関心の高まりも、高性能切削工具の市場を後押ししています。

- また、新しいコーティング技術や組成の調整により、HSS工具は機械加工や金属加工に不可欠な材料として、その地位を確立しています。

高速度鋼切削工具の市場動向

自動車産業のポジティブな見通し

HSS切削工具の成長を後押ししている主な要因は、自動車産業からの需要の増加です。自動車業界ではHSS系切削工具が主流であり、自動車部品のフライス加工、研削加工、ブローチ加工に使用されています。HSS切削工具は、製造工程における高精度、耐久性、再現性に優れているため、全体的な生産性を高めるための効率的で経済的な選択肢を提供します。

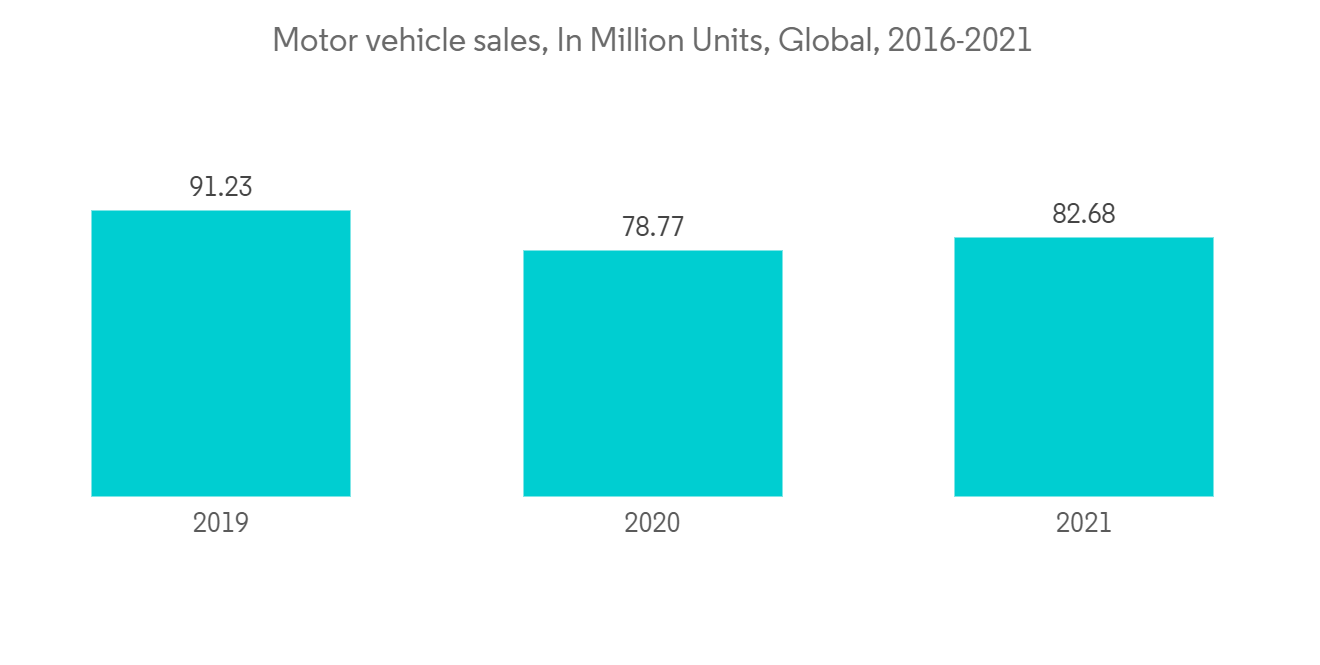

いくつかの逆風はあるもの、自動車産業は世界的に明るい見通しです。米国の軽自動車小売販売台数は、2021年に1,490万台でピークを迎えました。業界関係者によると、世界の軽自動車生産台数は目覚ましい成長を遂げており、今後もその傾向は続くと予想されています。

生産台数の成長率はAPACが最も高く、次いで北米が続くと予想されています。このシナリオにより、製造工程に関連する切削工具やその他の機器の需要が創出されると予想されます。

APAC地域の鋼材需要の増加が鋼材切削工具市場を牽引する

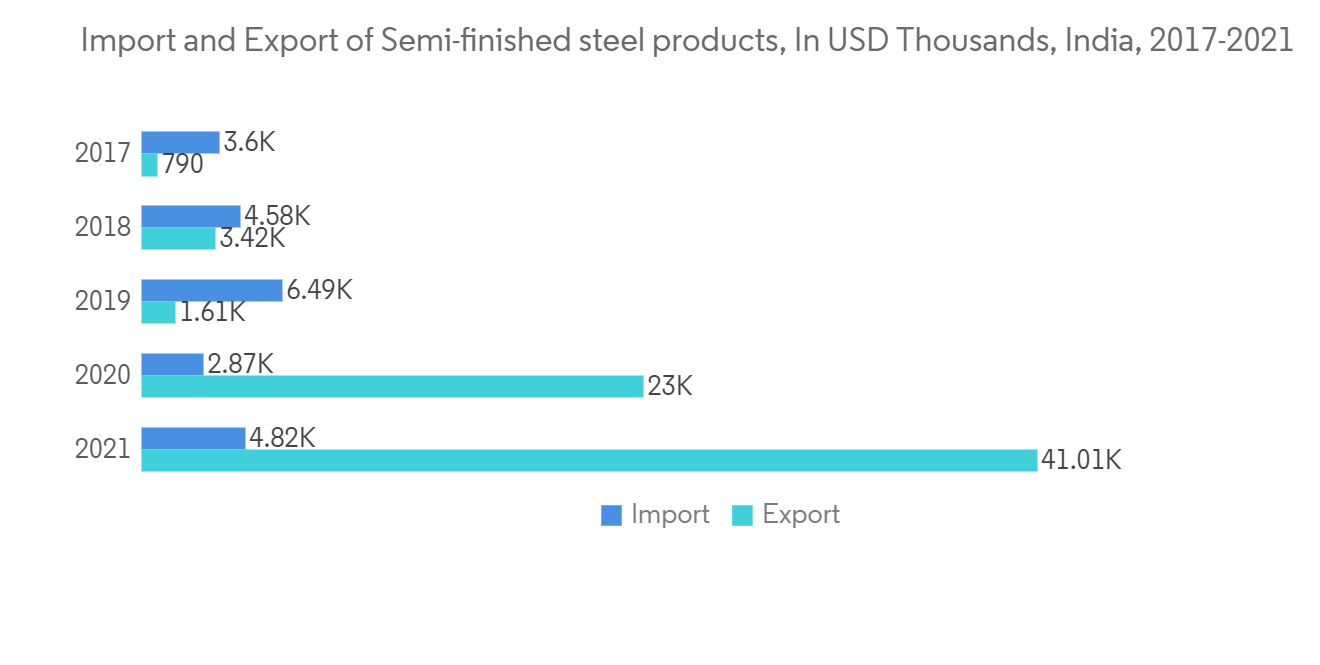

世界鉄鋼協会は、鉄鋼需要が2022年に0.4%増の18億4,000万トン、2023年にさらに2.2%増の18億8,000万トンになると予測しています。世界の先進国では、2021年に16.5%増加した鉄鋼需要は、2022年には1.1%減、2023年には2.4%増となる見込みです。世界中の鉄鋼メーカーは、高い需要に対応するため、大規模な設備投資により生産能力を増強しています。

業界の専門家によると、インドの鉄鋼需要は、2020年の100MTPAから2030-31年には230MTPAに増加すると予想されています。例えば、インドでは、JSW Steelが2,800億ルピー(37億米ドル)を投じて、製鉄能力を2021年3月の24.5MTPAから2024年3月の36.5MTPAへと増強しました。タタ・スチールは、カリンガナガル工場の拡張工事の完了に向けて800億ルピー(11億米ドル)を投資し、生産能力を3MTPAから8MTPAに引き上げるとともに、鉱山事業やリサイクル事業の拡大を発表しました。SAILも7,000億ルピー(93億米ドル)の近代化・拡張計画が終了し、生産能力を21.4MTPAに拡大する予定です。

中国は大規模な鉄鋼生産能力を構築し、現在では世界最大の鉄鋼生産国となっており、年間粗鋼生産量は過去2年連続で10億トンを超えています。生産された鉄鋼の大半は中国で消費されますが、中国の鉄鋼メーカーにとって輸出も重要です。

日本も世界有数の鉄鋼生産国であり、建設業や自動車製造業などの国内産業が生産量の大部分を消費しています。日本では、鉄鋼は依然として欠かせない存在です。鉄鉱石や原料炭の輸入に頼ってはいるもの、世界第2位の鉄鋼輸出国です。

高速度鋼切削工具市場の競合他社分析

高速度鋼切削工具市場は、世界な大手プレーヤーとローカルな中小プレーヤーが存在し、かなりの数のプレーヤーが市場シェアを占めている、かなり細分化された市場です。市場の主要企業としては、BIG Kaiser Precision Tooling、Erasteel、Kennametal, Inc.、OSG Korea Corporation、Niagara Cutter, Inc.などがあります。

また、多くの世界企業が主要国に拠点を構えていることも判明しています。HSS工具市場で活動する主要企業は、需要の高まりに対応し、有利な場所でのカバレッジを獲得するために、販売拠点の強化に注力しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提条件条件

- 調査対象範囲

第2章 調査手法

- 分析手法

- 調査フェーズ

第3章 エグゼクティブサマリー

第4章 市場の概要

- 現在の市場シナリオ

- 市場力学

- 促進要因

- 抑制要因

- 機会

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 産業バリューチェーン分析

- 世界の製造業(概要、動向、研究開発、主要統計データなど)

- 製造業に関する政府の主な規制と取り組み

- 鉄鋼業界スナップショット(概要、主な指標、発展、など)

- 技術スナップショット

- 粉末冶金のスポットライト

- ツールポストとツールホルダーに関する洞察

- COVID-19の市場への影響について

第5章 市場セグメンテーション

- タイプ別

- ミーリング

- ドリリング

- タッピング

- その他

- エンドユーザー別

- 製造業・自動車

- 石油・ガス分野

- 鉱業、および採石業

- 農業・漁業・林業

- コンストラクション

- ディストリビューション・トレード

- ヘルスケア・医薬

- その他のエンドユーザー

- 地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- APACのその他諸国

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米地域

- 中東・アフリカ地域

- 南アフリカ

- サウジアラビア

- その他中東・アフリカ地域

- アジア太平洋地域

第6章 競合情勢について

- 企業プロファイル

- Erasteel

- Kennametal, Inc.

- Nachi America, Inc.

- OSG Korea Corporation

- Niagara Cutter, Inc.

- Addison & Co., Ltd

- Sumitomo Electric Industries

- Tiangong International

- Walter AG

- NACHI-FUJIKOSHI CORP

- DeWALT

- Somta Tools(Pty)Ltd

- Morse Cutting Tools

- Sandvik Group

- Arch Cutting Tools

第7章 市場機会と今後の動向

第8章 付録

- GDP分布(活動別)-主要国

- 資本移動に関する洞察-主要国

- 経済統計製造業、経済への貢献度(主要国)

- 世界の製造業統計

The size of the High-Speed Cutting Tools market is USD 6.81 billion in the current year and is anticipated to register a CAGR of over 3% during the forecast period

Key Highlights

- The growth of the market is majorly driven by the increasing demand from several end-user industries, such as automotive, aerospace, and others, across the world. Tooling is an important part of the manufacturing process since machine tools are used to bore, mill, grind, tap, drill, etc., and determine the quality of the manufactured product. Following a few years of quiet moderation, the worldwide production of machine tools underwent explosive growth. Since cutting is an integrated part of the machine tools in the final operation, the growth of the machine tool market demands more tools. Generally, HSS cutting tools are fixed on CNC machine tools to develop complex products and shapes.

- China is the global leader in the machine tool market. Worldwide, the machine tool-cutting sector represents a major share in terms of production volume compared to forming technology.

- The demand for high-speed steel (HSS) is growing for manufacturing cutting tools due to its properties such as high working hardness, durability, high wear hardness, and good retention of hardness. The use of HSS has increased the cutting speed by four times compared to previously-used carbon steels. The need for efficient and reliable machining is increasing for manufacturers. Due to the above-mentioned properties, HSS cutting tools are making their way for mass production and high-temperature operations. The growing focus on customer satisfaction and product quality is also helping to boost the market for high-performance cutting tools.

- Adapting new coating technologies and adjusting their composition accordingly, HSS tools continue to gain ground, thereby retaining their position as vital materials in the machining and metal-cutting industries.

High Speed Steel Cutting Tools Market Trends

Positive Outlook for the Automotive Industry

The major factor boosting the growth of HSS cutting tools is the increasing demand from the automotive industry. HSS cutting tools dominate the automotive industry and are used for milling, grinding, and broaching automotive car parts. HSS cutting tools provide an efficient and economical option to increase overall productivity, owing to their high precision, durability, and repeatability during manufacturing operations.

Despite some headwinds, the automotive industry is looking bright globally. U.S. light-vehicle retail sales peaked in 2021 at 14.9 million units. According to industry sources, global light vehicle production units have seen remarkable growth and continue to do so.

APAC is expected to register the highest growth rates in production volumes, followed by North America. This scenario is expected to create demand for cutting tools and other equipment associated with the manufacturing process.

Higher Demand for Steel from the APAC Region is Driving the Steel Cutting Tools Market

The World Steel Association forecasts steel demand to edge up 0.4% in 2022 to 1.84 billion mt and grow a further 2.2% in 2023 to 1.88 billion mt. In the developed nations of the world, steel demand is expected to increase by a lower 1.1% in 2022 and 2.4% in 2023, after rising 16.5% in 2021. Steelmakers around the world are increasing capacity through large capital investments to meet the high demand.

Steel demand in India is expected to rise from 100 MTPA in 2020 to 230 MTPA in 2030-31, according to industry experts. For example, In India, JSW Steel spent Rs. 280 billion (USD 3.7 billion) to increase its steelmaking capacity from 24.5 MTPA in March 2021 to 36.5 MTPA in March 2024. Tata Steel announced an investment of Rs. 80 billion (USD 1.1 billion) toward the completion of the Kalinganagar plant expansion, which will increase capacity to 8 MTPA from 3 MTPA, as well as the expansion of the mining operations and recycling business. SAIL, too, is nearing the end of an Rs. 700 billion (USD 9.3 billion) modernization and expansion program that will increase its capacity to 21.4 MTPA.

China has built up massive iron and steel production capacity and is now the world's largest steel producer, with annual crude steel production volume exceeding one billion metric tons for the past two years in a row. Although China consumes the majority of the steel produced, exports are also important for Chinese steelmakers.

Japan is also one of the world's largest steel producers, with domestic industries such as construction and automotive manufacturing consuming a large portion of the output. Steel remains indispensable in Japan. It is the world's second-largest steel exporter, despite relying on price-driving iron ore and coking coal imports.

High Speed Steel Cutting Tools Market Competitor Analysis

The high-speed steel-cutting tools market is fairly fragmented in nature, with the presence of large global players and small and medium-sized local players, with quite a few players who occupy the market share. Some of the major players in the market are BIG Kaiser Precision Tooling, Erasteel, Kennametal, Inc., OSG Korea Corporation, and Niagara Cutter, Inc.

It has also been found that many global companies have a footprint in major countries. Key players operating in the HSS tools market focus on strengthening their distribution footprint to keep pace with growing demand and gain coverage in lucrative locations.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Current Market Scenario

- 4.2 Market Dynamics

- 4.2.1 Drivers

- 4.2.2 Restraints

- 4.2.3 Opportunities

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Industry Value Chain Analysis

- 4.5 Global Manufacturing Sector (Overview, Trends, R&D, Key Statistics, etc.)

- 4.6 Key Government Regulations and Initiatives for Manufacturing Sector

- 4.7 Steel Industry Snapshot (Overview, Key Metrics, Developments, etc.)

- 4.8 Technology Snapshot

- 4.9 Spotlight on Powder Metallurgy

- 4.10 Insights on Tool Posts and Tool Holders

- 4.11 Impact of COVID - 19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Milling

- 5.1.2 Drilling

- 5.1.3 Tapping

- 5.1.4 Others

- 5.2 By End-user

- 5.2.1 Manufacturing and Automotive

- 5.2.2 Oil and Gas

- 5.2.3 Mining, and Quarrying

- 5.2.4 Agriculture, Fishing, and Forestry

- 5.2.5 Construction

- 5.2.6 Distributive Trade

- 5.2.7 Healthcare and Pharmaceutical

- 5.2.8 Other End Users

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of APAC

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 United Kingdom

- 5.3.3.2 Germany

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East & Africa

- 5.3.5.1 South Africa

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Rest of Middle East & Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Erasteel

- 6.1.2 Kennametal, Inc.

- 6.1.3 Nachi America, Inc.

- 6.1.4 OSG Korea Corporation

- 6.1.5 Niagara Cutter, Inc.

- 6.1.6 Addison & Co., Ltd

- 6.1.7 Sumitomo Electric Industries

- 6.1.8 Tiangong International

- 6.1.9 Walter AG

- 6.1.10 NACHI-FUJIKOSHI CORP

- 6.1.11 DeWALT

- 6.1.12 Somta Tools (Pty) Ltd

- 6.1.13 Morse Cutting Tools

- 6.1.14 Sandvik Group

- 6.1.15 Arch Cutting Tools*

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

8 APPENDIX

- 8.1 GDP Distribution, by Activity-Key Countries

- 8.2 Insights on Capital Flows-Key Countries

- 8.3 Economic Statistics Manufacturing Sector, Contribution to Economy (Key Countries)

- 8.4 Global Manufacturing Industry Statistics