|

市場調査レポート

商品コード

1406583

抗体薬物複合体:市場シェア分析、産業動向と統計、成長予測、2024~2029年Antibody-drug Conjugates - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| 抗体薬物複合体:市場シェア分析、産業動向と統計、成長予測、2024~2029年 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 200 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

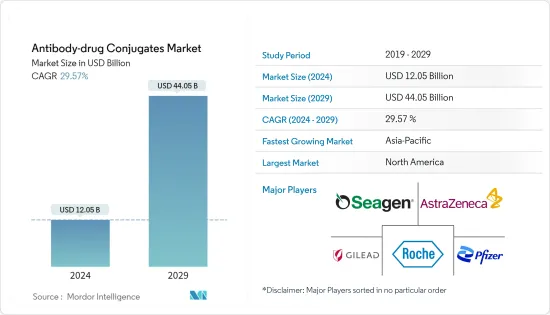

抗体薬物複合体の市場規模は2024年に120億5,000万米ドルと推定され、2029年には440億5,000万米ドルに達すると予測され、予測期間(2024-2029年)のCAGRは29.57%で成長する見込みです。

COVID-19パンデミックは抗体薬物複合体市場に顕著なインパクトを与えました。例えば、英国の国民保健サービス(NHS)によると、2023年のパンデミックでは、封鎖規制により自宅待機が必要となったため、緊急の紹介が激減し、がん治療が不足したため、抗体薬物複合体を含むがん治療全体の需要が大幅に減少しました。

さらに、抗体薬物複合体の大手メーカーであるセーゲン社のアニュアルレポート2022によると、COVID-19パンデミックは、商業化への取り組み、サプライチェーン、規制活動、臨床開発活動など、同社の事業に悪影響を及ぼしました。このように、COVID-19パンデミックは抗体薬物複合体製造企業の事業運営に大きな影響を及ぼし、抗体薬物複合体の販売に影響を与えました。しかし、パンデミック後の抗体薬結合体の承認と上市の増加は、今後数年間の市場の成長を約束するものです。

抗体薬物複合体市場の成長の主な要因としては、がんの有病率の増加、高齢者人口の増加、新規治療薬開発のための研究開発活動の活発化などが挙げられます。抗体薬物複合体は、がん患者にとって最も効果的な治療法のひとつです。抗体薬物複合体は、モノクローナル抗体の標的抗原に対する特異性を利用して、潜在的な細胞傷害性薬剤を放出することができ、化学療法と比較して活性が高く毒性が低いです。

さまざまな国でがんの発生率が上昇しているため、抗体薬物複合体の治療への利用が増加しています。例えば、カナダがん協会による2022年5月の最新情報によると、2022年に乳がんと診断されたカナダ人女性は28,600人で、2022年の女性の新規がん患者全体の25%に相当します。また、2022年には1日平均78人のカナダ人女性が乳がんと診断されると予想されています。このように、女性の乳がん罹患率の高さと罹患確率の増加により、抗体薬物複合体の需要は増加し、予測期間中の市場成長を促進すると考えられます。

同市場への投資の増加は、抗体薬物複合体のパイプラインを強化し、その用途を拡大すると予想され、市場成長にプラスの影響を与える可能性があります。例えば、2022年6月、Spirea Limited社は、英国および米国の著名投資家からの投資により240万英ポンド(306万米ドル)の資金を確保しました。同社はこれらの資金を固形がん治療における優れた差別化された抗体薬物複合体のパイプラインを開始するために使用し、市場の成長に貢献しています。

しかし、政府の規制が厳しく、抗体薬物複合体の製造コストが高いため、予測期間中の市場の成長は抑制されると予想されます。

抗体薬物複合体市場の動向

乳がんセグメントが市場で最大シェアを占める

- 世界の乳がん罹患率の上昇により、乳がん分野は予測期間中に大幅な成長が見込まれます。加えて、抗体薬物複合体を用いた乳がんに対する製品の承認・上市の増加や進行中の臨床試験が、予測期間中の市場成長に寄与しています。

- 乳がんにおける抗体薬物複合体の成功により、多くの新薬の臨床研究が行われるようになり、市場の成長を後押しする可能性が高いです。例えば、2022年2月にJournal of Cancer Research誌に掲載された調査では、TROP2指向性datopotamab deruxtecanと思われる最も有望な新規抗体薬物複合体が、進行再発/難治性HER2陰性乳がんにおいて有望な初期段階の活性を示したことが報告されています。

- 同様に、2023年3月、Ambrx Biopharma Inc.は、パートナーであるNovoCodex Biopharmaceuticals, Inc.から、Ambrxの抗HER2抗体薬物複合体(ADC)であるARX788を対象としたランダム化第3相乳がん臨床試験であるACE-Breast-02の中間解析において、事前に指定された主要評価項目を統計学的に有意に達成し、アクティブコントロールと比較して無増悪生存期間(PFS)の延長が認められたとの報告を受けました。このように、このような臨床試験は、乳がん治療のためのより優れた抗体薬物複合体の開発につながっています。

- 乳がんに対する抗体薬物複合体の新たな承認と上市は、この薬剤の需要を増加させ、調査期間中の同分野の成長を押し上げる可能性が高いです。例えば、2023年2月にGilead Sciences, Inc.は、米国食品医薬品局(FDA)から、切除不能な局所進行性または転移性のホルモン受容体(HR)陽性、ヒト上皮成長因子受容体2(HER2)陰性(IHC 0、IHC 1+、またはIHC 2+/ISH-)の乳がんで、内分泌療法を受けたことがあり、転移性では少なくとも2種類の全身療法を追加した成人患者の治療薬として、トロデルビー(sacituzumab govitecan-hziy)の承認を取得しました。

- このように、乳がん治療のための研究開発および製品承認の増加は、乳がん治療における抗体薬物複合体の使用を増加させ、予測期間中の同分野の成長を押し上げると予想されます。

北米が予測期間中に大きな成長を遂げる見込み

- 北米は、がん患者数の増加と技術開発により、予測期間中に大きな成長が見込まれます。この地域は、技術の進歩、主要プレイヤーの現地プレゼンス、米国やカナダなどの国のリーダーによる戦略的イニシアチブにより、大きな成長を観察しています。2021年4月、ファイザーは、抗体薬物複合体やがんのための他のいくつかの治療法を開発するためにAmplyx Pharmaceuticals Inc.を買収しました。

- 北米諸国はがん患者が多いことが特徴です。がん患者数の増加が同地域の市場成長を牽引しています。例えば、米国がん協会(ACS)が発表した2021年と2023年の統計によると、がん罹患者数は2021年の191万人から2023年には196万人に増加すると推定されており、わずか2年間で6万人以上増加しており、同国におけるがん罹患者数の急激な増加を示しています。同国ではがん罹患率が上昇する可能性が高く、そのため高度ながん治療に対する需要が高まり、結果的に市場の成長を後押ししています。

- 市場プレーヤーは、パートナーシップや新製品の承認によって抗体薬物複合体のポートフォリオを拡大しており、市場の大きな成長が期待されています。例えば、2023年2月、Corbus Pharmaceuticals Holdings, Inc.は、CSPC Pharmaceutical Group Limitedの子会社であるCSPC Megalith Biopharmaceuticalと、CRB-701(SYS6002)の開発と商業化に関する独占ライセンス契約を締結しました。本契約は、米国およびカナダにおけるCRB-701の独占的商業化権を対象としています。さらに2022年2月、Adcentrx TherapeuticsとAvantGenは、新規抗体薬物複合体治療薬候補として開発される抗体の探索に関して、3年間のマルチターゲット提携を締結しました。

- このように、がん患者数の増加と主要企業間の戦略的提携、規制当局の承認により、北米の抗体薬物複合体市場は予測期間中に大きく成長すると予想されます。

抗体薬物複合体産業の概要

抗体薬物複合体市場は、世界各地に複数の企業が存在するため、その性質上やや細分化されており、競合も激しいです。競合情勢には、Seagen Inc.、ImmunoGen Inc.、Pfizer Inc.、F. Hoffmann-La Roche Ltd.、AbbVie Inc.、AstraZeneca PLC、Gilead Sciences Inc.など、主要な市場シェアを保有する国際企業や現地企業の分析が含まれます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- がん罹患率の増加

- 高齢者人口の増加

- 新規治療薬開発のための研究開発活動の活発化

- 市場抑制要因

- 厳しい政府規制

- 抗体薬物複合体の高い製造コスト

- 業界の魅力- ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(市場規模、金額ベース)

- 製品タイプ別

- アドセトリス

- カドサイラ

- その他の製品タイプ

- 用途別

- 血液がん

- 乳がん

- 卵巣がん

- 肺がん

- 皮膚がん

- 脳腫瘍

- その他の用途

- 技術別

- 切断可能リンカー

- 非開裂リンカー

- ターゲットタイプ別

- CD30抗体

- HER2抗体

- その他のターゲットタイプ

- エンドユーザー別

- 病院および専門がんセンター

- バイオテクノロジーおよび製薬会社

- その他のエンドユーザー

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Seagen Inc.

- ImmunoGen Inc.

- Mersana Therapeutics Inc.

- Pfizer Inc.

- F. Hoffmann-La Roche Ltd

- Sorrento Therapeutics Inc.

- Oxford BioTherapeutics Ltd

- AbbVie Inc.

- Takeda Pharmaceutical Company Ltd

- AstraZeneca PLC

- ADC Therapeutics SA

- Gilead Sciences Inc.

- GSK plc.

- Daiichi Sankyo Company, Limited

第7章 市場機会と今後の動向

The Antibody-drug Conjugates Market size is estimated at USD 12.05 billion in 2024, and is expected to reach USD 44.05 billion by 2029, growing at a CAGR of 29.57% during the forecast period (2024-2029).

The COVID-19 pandemic had a notable impact on the antibody-drug conjugates market since many cancer consultations and treatments were postponed or canceled due to the lockdown restrictions. For instance, according to the National Health Service (NHS) of the United Kingdom, in 2023, there was a shortfall in cancer treatments during the pandemic, driven by a sharp drop in urgent referrals as people needed the stay-at-home due to the lockdown restrictions, which significantly reduced the demand for overall cancer therapies including antibody-drug conjugates.

Moreover, according to the Annual Report 2022 of Seagen Inc., a leading manufacturer of antibody-drug conjugates, the COVID-19 pandemic had adverse impacts on the company's business, including commercialization efforts, supply chain, regulatory activities, clinical development activities, and others. Thus, the COVID-19 pandemic significantly impacted the business operations of antibody-drug conjugate manufacturing companies, thus impacting the sale of antibody-drug conjugates. However, the increasing approvals and launches of antibody-drug conjugates in the post-pandemic period attain growth in the market over the coming years.

The major factors responsible for the growth of the antibody-drug conjugates market include the growing prevalence of cancer, the increasing geriatric population, and increasing R&D activities for the development of novel therapeutics. Antibody-drug conjugates offer one of the most effective treatments for cancer patients. They can exploit the specificity of monoclonal antibodies toward targeted antigens for the release of potential cytotoxic drugs, with increased activity and decreased toxicity as compared to chemotherapies.

The rising incidence of cancer in various countries increases the usage of antibody-drug conjugates for treatment. For instance, according to the May 2022 update by the Canadian Cancer Society, 28,600 Canadian women were diagnosed with breast cancer in 2022, representing 25% of all new cancer cases in women in 2022. Also, on average, 78 Canadian women were expected to be diagnosed with breast cancer daily in 2022. Thus, owing to the high prevalence and increase in the probability of acquiring breast cancer among females, the demand for antibody-drug conjugates is likely to rise, fueling the market growth over the forecast period.

The increasing investments in the market are expected to boost the antibody-drug conjugates pipeline and expand its applications, which may positively impact the market's growth. For instance, in June 2022, Spirea Limited secured funding of GBP 2.4 (USD 3.06) million with investments from high-profile investors from the United Kingdom and the United States. The company uses these funds to initiate its pipeline of superior and differentiated antibody-drug conjugates in the treatment of solid tumors, thereby contributing to the growth of the market.

However, the stringent government regulations and high manufacturing costs of antibody drug conjugates are expected to restrain the market's growth over the forecast period.

Antibody Drug Conjugates Market Trends

Breast Cancer Segment accounted for the Largest Share of the Market

- The breast cancer segment is expected to witness significant growth over the forecast period due to the rising incidences of breast cancer worldwide. In addition, the growing product approvals and launches and ongoing clinical trials for breast cancers using antibody-drug conjugates contribute to market growth over the forecast period.

- The success of antibody-drug conjugates in breast cancer has led to many new drug clinical studies that are likely to boost the market's growth. For instance, the study published in the Journal of Cancer Research in February 2022 reported the most promising new antibody-drug conjugates, which appear to be the TROP2-directed datopotamab deruxtecan, has shown encouraging early-phase activity in advanced relapsed/refractory HER2-negative breast cancer.

- Similarly, in March 2023, Ambrx Biopharma Inc. was informed by its partner, NovoCodex Biopharmaceuticals, Inc., that an interim analysis for ACE-Breast-02, a randomized Phase 3 breast cancer clinical trial investigating Ambrx's ARX788, an anti-HER2 antibody-drug conjugate (ADC), has met its pre-specified interim primary efficacy endpoint with statistical significance, demonstrating a greater progression-free survival (PFS) benefit compared to the active control. Thus, such clinical trials are leading to the development of better antibody-drug conjugates for the treatment of breast cancer.

- The new approvals and launches of antibody-drug conjugates for breast cancers increase the demand for this drug, which likely boosts the segment growth over the study period. For instance, in February 2023, Gilead Sciences, Inc. received approval from the United States Food and Drug Administration (FDA) for Trodelvy (sacituzumab govitecan-hziy) for the treatment of adult patients with unresectable locally advanced or metastatic hormone receptor (HR)-positive, human epidermal growth factor receptor 2 (HER2)-negative (IHC 0, IHC 1+ or IHC 2+/ISH-) breast cancer who have received endocrine-based therapy and at least two additional systemic therapies in the metastatic setting.

- Thus, the increasing R&D for breast cancer treatment and product approvals are anticipated to increase the use of antibody-drug conjugates in the treatment of breast cancer, thus boosting the segment's growth over the forecast period.

North America is Expected to Witness Significant Growth Over the Forecast Period

- North America is expected to witness significant growth over the forecast period due to rising cancer cases and technological developments. The region is observing significant growth due to technological advancements, the local presence of key players, and strategic initiatives by leaders in countries such as the United States and Canada. In April 2021, Pfizer acquired Amplyx Pharmaceuticals Inc. to develop antibody-drug conjugates and several other therapies for cancer.

- North American countries are marked by high cancer cases. The increasing number of cancer cases is driving the growth of the market in the region. For instance, according to the 2021 and 2023 statistics published by the American Cancer Society (ACS), the incidence of cancer cases is estimated to increase from 1.91 million in 2021 to 1.96 million in 2023, an increase of more than 60 thousand cases in just two years, demonstrating a rapid increase in the incidence of cancer cases in the country. The chance of an increase in the incidence of cancer is likely to be high in the country, thus raising the demand for advanced oncology treatment, which ultimately boosts the market growth.

- The market players are expanding the antibody-drug conjugate portfolio with partnerships and new product approvals, which are expected to have significant growth in the market. For instance, in February 2023, Corbus Pharmaceuticals Holdings, Inc. entered into an exclusive licensing agreement with CSPC Megalith Biopharmaceutical Co., Ltd, a subsidiary of CSPC Pharmaceutical Group Limited, for the development and commercialization of CRB-701 (SYS6002). The agreement covers exclusive commercialization rights to CRB-701 in the United States and Canada. In addition, in February 2022, Adcentrx Therapeutics and AvantGen entered a three-year, multi-target partnership for the discovery of antibodies to be developed into novel antibody-drug conjugates therapeutic candidates.

- Thus, owing to the growing number of cancer cases and strategic partnerships among the key players, along with regulatory approvals, the North American antibody drug conjugates market is expected to grow significantly during the forecast period.

Antibody Drug Conjugates Industry Overview

The antibody-drug conjugates market is slightly fragmented in nature and competitive due to the presence of several companies across the globe. The competitive landscape includes an analysis of a few international and local companies that hold major market shares, including Seagen Inc., ImmunoGen Inc., Pfizer Inc., F. Hoffmann-La Roche Ltd, AbbVie Inc., AstraZeneca PLC, Gilead Sciences Inc, and others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Incidences of Cancer

- 4.2.2 Growing Geriatic Population

- 4.2.3 Increasing R&D Activities for the Development of Novel Therapeutics

- 4.3 Market Restraints

- 4.3.1 Stringent Government Regulations

- 4.3.2 High Manufacturing Costs of Antibody Drug Conjugates

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Product Type

- 5.1.1 Adcetris

- 5.1.2 Kadcyla

- 5.1.3 Other Product Types

- 5.2 By Application

- 5.2.1 Blood Cancer

- 5.2.2 Breast Cancer

- 5.2.3 Ovary Cancer

- 5.2.4 Lung Cancer

- 5.2.5 Skin Cancer

- 5.2.6 Brain Tumor

- 5.2.7 Other Applications

- 5.3 By Technology

- 5.3.1 Clevable Linker

- 5.3.2 Non-cleavable Linker

- 5.4 By Target Type

- 5.4.1 CD30 Antibodies

- 5.4.2 HER2 Antibodies

- 5.4.3 Other Target Types

- 5.5 By End User

- 5.5.1 Hospitals and Speciality Cancer Centers

- 5.5.2 Biotechnology and Pharmaceutical Companies

- 5.5.3 Other End Users

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Seagen Inc.

- 6.1.2 ImmunoGen Inc.

- 6.1.3 Mersana Therapeutics Inc.

- 6.1.4 Pfizer Inc.

- 6.1.5 F. Hoffmann-La Roche Ltd

- 6.1.6 Sorrento Therapeutics Inc.

- 6.1.7 Oxford BioTherapeutics Ltd

- 6.1.8 AbbVie Inc.

- 6.1.9 Takeda Pharmaceutical Company Ltd

- 6.1.10 AstraZeneca PLC

- 6.1.11 ADC Therapeutics SA

- 6.1.12 Gilead Sciences Inc.

- 6.1.13 GSK plc.

- 6.1.14 Daiichi Sankyo Company, Limited