|

市場調査レポート

商品コード

1432988

デジタル治療機器:世界市場シェア分析、産業動向・統計、成長予測(2024年~2029年)Global Digital Therapeutic Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| デジタル治療機器:世界市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

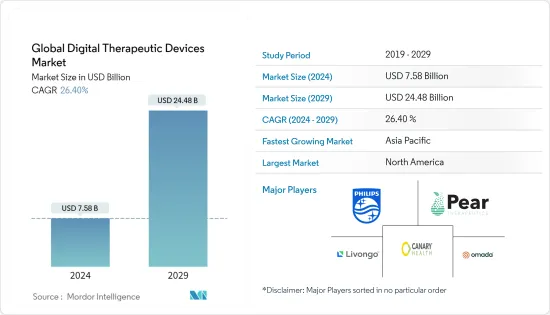

世界のデジタル治療機器の市場規模は、2024年に75億8,000万米ドルと推定され、2029年までに244億8,000万米ドルに達すると予測されており、予測期間(2024年~2029年)中に26.40%のCAGRで成長する見込みです。

COVID-19の発生により、ヘルスケア専門家は従来のシステムや手順に代わるものを模索するようになりました。これにより、医療提供者から消費者に至るまで、業界全体でデジタル医療が急速に導入されることになります。パンデミック中は必須ではない要件の優先順位が低いため、患者はデジタル治療ソリューションに目を向けています。 2020年5月に発表された「COVID-19パンデミックにおけるデジタル理学療法」というタイトルの調査研究では、COVID-19の世界のパンデミックにより、ブラジルの医療システムはさまざまな医療分野で遠隔医療を速やかに導入する必要に迫られたと述べています。デジタル診療を使用した治療効果と患者評価は、一部の急性および慢性の筋骨格疾患、心臓疾患、神経学的問題、術後のリハビリテーション、疼痛管理、骨盤底の状態、呼吸機能障害についてすでに調査されています。したがって、調査研究を増やすことで、新型コロナウイルスが市場に与える影響についての洞察が得られると考えられています。したがって、今後市場は成長すると予想されています。

2021年1月に発表された研究「インド長期老化研究(LASI)」によると、60歳以上の約7,500万人が何らかの慢性疾患を患っています。約4,500万人が心血管疾患と高血圧を患っており、約2,000万人が糖尿病に苦しんでいます。したがって、この国における慢性疾患の罹患率の高さは、デジタル治療機器などの費用対効果の高い治療法への需要を高め、調査対象市場を牽引すると考えられます。病状の治療のためのテクノロジーの使用が増加しています。先進国市場の消費者は、病状治療のための先進的な製品に対する意識を高めています。 2019年7月、経済協力開発機構によると、多くのOECD諸国で経済状況が悪化しヘルスケア支出が増加したため、GDPに占める医療支出の割合は2020年に大幅に増加しました。 16か国からなるグループの医療支出の暫定値によると、2020年には一人当たりの健康が平均約4.9%増加したことが示唆されています。したがって、治療機器の革新に対する需要の高まりなど、医療分野の高度なサービスにも優先順位が移っています。製品の承認も市場成長のもう一つの要因です。たとえば、2020年12月、米国食品医薬品局は、サンフランシスコとロンドンに本拠を置くMahana TherapeuticsにParallelと呼ばれる製品のDe Novo販売承認を与えました。同社の資料によれば、これは過敏性腸症候群の人向けの8週間の認知行動療法プログラムです。このような承認により、市場の成長が促進されます。

企業はこの分野でのベンチャー投資でもますます成長しており、それがこの市場を牽引しています。デジタル治療機器に関連する患者のデータプライバシーの懸念などの要因が、この市場の成長を妨げています。

デジタル治療機器市場動向

治療/ケア部門は予測期間中に高い成長が見込まれる

パンデミック中、患者が自分の状況を管理し、リアルタイムで対応する必要性が高まっていますが、医師は引き続き患者の状況を遠隔から監視する必要があります。したがって、デジタル治療機器の需要が増加しました。COVID-19の流行により、医療において情報に基づいた積極的な役割を果たすために、デジタルアプリケーションに対する患者の信頼性が高まりました。デジタル治療ソリューションは、患者と医師の再会に役立ちました。したがって、デジタルヘルスツールは慢性疾患を持つ患者や医療専門家にとって非常に役立つことが証明されていると結論付けることができます。

このカテゴリーの成長に貢献する重要な要因の1つは、主要な市場プレーヤーによるパートナーシップです。たとえば、2021年1月に、Hydrus 7 Labは欧州のデジタルヘルス企業であるEpilloと戦略的パートナーシップを締結しました。このような取り組みにより、将来の市場の成長が促進されると予想されています。

慢性疾患の負担が増大することで、このセグメントの成長が加速します。国際糖尿病連盟(IDF)によると、2021年には世界中で約5億3,600万人の成人(20~79歳)が糖尿病を抱えており、これは2045年までに7億8,300万人に増加すると予想されています。2型糖尿病患者の割合はほとんどの国で増加しており、糖尿病成人の79%は低所得国および中所得国に住んでおり、65歳以上の5人に1人が糖尿病を患っています。

予測期間中に北米が市場を独占すると予想される

北米は、この地域での新技術の早期採用と資金調達による投資の増加により、市場を独占すると予想されています。この資金調達は、政府、ベンチャーキャピタリスト、合併、買収からの投資の増加に関連しています。

2020年4月、米国食品医薬品局(米国FDA)は、メンタルヘルスのためのデジタル医療機器の利用可能性を高めるためのガイドラインを発行しました。これを念頭に置いて、FDAは、COVID-19公衆衛生上の緊急事態下で、自宅隔離ガイドラインに従ったり、クリニック受診を必要とせずに社会的隔離を実践した人々に助成金を与えることを目指しました。これにより、医療機関の負担も軽減され、ウイルスにさらされるリスクも軽減されます。政府によるこのような取り組みは、この地域の市場の成長を促進します。

買収も市場成長のもう一つの要因です。たとえば、2021年2月、Philipsは、米国を拠点とする遠隔心臓診断およびモニタリングの大手プロバイダーの1つであるBioTelemetry, Inc.の買収を発表しました。製品の承認も市場成長のもう1つの要因です。たとえば、2020年6月、メイン州ポートランドに本拠を置くデジタル治療会社MedRhythmsは、慢性的な脳卒中歩行障害を治療するための特許取得済みのデジタル治療法について食品医薬品局の認可を取得しました。これらの取り組みにより、将来的には市場の成長が促進されるでしょう。

さらに、高齢者人口の増加、慢性疾患の発生率の増加、ワイヤレスおよびポータブルシステムの需要の急増、支出削減を目的とした高度な償還構造の利用可能性なども、地域の成長を促進する要因のいくつかです。たとえば、2021年1月の国立慢性疾患予防健康増進センターによると、米国の成人10人中6人が慢性疾患を患っており、成人10人中4人が2つ以上の慢性疾患を抱えており、これらの症状がこの国のヘルスケア制度に毎年3兆8,000億米ドルの医療費をもたらしています。したがって、上記の要因により、市場は将来的に成長する可能性があります。

デジタル治療機器業界の概要

デジタル治療機器市場は競争が激しく、多数の大手企業が存在します。市場参加者の数の増加により、競合が激化しています。同社はまた、多くの雇用主、支払者、ヘルスケアシステム、製薬会社と提携して取り組んでいます。主要なプレーヤーには、Philips NV、Omada Health Inc.、WellDoc Inc.、LIVONGO HEALTH、Pear Therapeutics、Noom Health Inc.などがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 慢性疾患の負担増

- 技術進歩の高まり

- 政府による予防ヘルスケアへの関心の高まりとベンチャーキャピタル投資の増加

- 市場抑制要因

- 製造と設置の高コスト

- データプライバシーへの懸念と従来のヘルスケアプロバイダーからの抵抗

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 製品タイプ別

- ソフトウェアとサービス

- デバイス

- 用途別

- 予防

- 糖尿病予備軍

- 肥満

- 禁煙

- その他

- 治療/ケア

- 循環器疾患

- 糖尿病

- 神経疾患

- 呼吸器疾患

- その他

- 予防

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- 2Morrow, Inc.

- BigHealth

- Canary Health

- Koninklijke Philips NV(BioTelemetry Inc.)

- Livongo Health

- Mango Health Inc.

- Noom Health Inc.

- Omada Health Inc.

- Pear Therapeutics

- Propeller Health

- Twine Health Inc.

- WellDoc Inc.

第7章 市場機会と今後の動向

The Global Digital Therapeutic Devices Market size is estimated at USD 7.58 billion in 2024, and is expected to reach USD 24.48 billion by 2029, growing at a CAGR of 26.40% during the forecast period (2024-2029).

The outbreak of COVID-19 has also prompted healthcare professionals to seek alternatives to traditional systems and procedures. This leads to the rapid adoption of digital medical care across the industry from providers to consumers. As non-essential requirements are given low priority during the pandemic, patients turn to digital therapeutic solutions. In May 2020, a research study published titled "Digital physical therapy in the COVID-19 pandemic" stated that the worldwide COVID-19 pandemic forced the Brazilian health system to promptly adopt telehealth in different health care areas. Treatment efficacy and patient evaluation using digital practice were already investigated for some acute and chronic musculoskeletal conditions, cardiac conditions, neurological problems, post-surgical rehabilitation, pain management, pelvic floor conditions, and respiratory dysfunctions. Hence, increasing research studies would provide insight into the impact of COVID on the market. Thus, the market will grow in upcoming future.

According to the study 'The Longitudinal Ageing Study in India (LASI)' published in January 2021, approximately 75 million ages above 60 years of age suffer from some chronic disease. About 45 million have cardiovascular disease and hypertension and about 20 million suffer from diabetes. Thus, the high prevalence of chronic diseases in the country will boost the demand for cost-effective therapeutics such as digital therapeutic devices, thus driving the studied market. There has been a rise in the use of technology for therapeutics for medical conditions. Consumers in developed markets are increasingly aware of the advanced products for the treatment of medical conditions. In July 2019, according to the Organization for Economic Co-operation and Development, healthcare spending as a share of GDP has increased significantly in 2020, as the economic situation worsened and health spending increased in many OECD countries. Preliminary health spending for a group of 16 countries suggest that per capita health increased by around 4.9% on average in 2020. The preference is also, therefore, shifted toward the advanced services in the medical field, including the growing demand for innovations in therapeutic devices. Product apporval are another factor for the growth of the market. For instance, in December 2020, the United States Food and Drug Administration awarded a De Novo marketing authorization to San Francisco and London-based Mahana Therapeutics for a product called Parallel, which according to company materials is an 8-week cognitive behavioral therapy program for people with irritable bowel syndrome. Such approvals will increase the market growth.

The companies are also increasingly rising on venture investments in this domain, which drives this market. Factors, such as patient's data privacy concerns associated with digital therapeutic devices, hinder the growth of this market.

Digital Therapeutic Devices Market Trends

Treatment/Care Segment is Expected to Witness a High Growth Over the Forecast Period

During the pandemic, there has been a growing need for patients to take control of their own situation and respond in real-time, while their doctor still needs to monitor their case remotely. Therefore, digital therapeutic devices increased in demand. The outbreak of COVID-19 has increased patient reliability in digital applications to play an active and informed role in their health care. Digital treatment solutions have helped reunite patients with doctors. Therefore, it can be concluded that digital health tools prove to be very useful for patients with chronic illnesses and medical professionals.

One of the key factors contributing to the growth of this category is the partnerships by key market players. For instance, in January 2021, Hydrus 7 Lab signed a strategic partnership with European Digital Health company, Epillo. Such initiatives would increase market growth in the future.

The growing burden of chronic disorders increases the segment growth. according to the International Diabetes Federation (IDF), in 2021, approximately 536 million adults (between the ages of 20-79 years) were living with diabetes globally, and this will rise to 783 million by 2045. The proportion of people with type 2 diabetes is increasing in most countries, and 79% of adults with diabetes were living in low- and middle-income countries, where 1 in 5 people above the age of 65 years have diabetes. The proportion of people with type 2 diabetes is increasing in most countries, and 79% of adults with diabetes were living in low- and middle-income countries, where 1 in 5 people above the age of 65 years have diabetes.

North America is Expected to Dominate the Market During the Forecast Period

North America is expected to dominate the market, owing to the early adoption of new technologies and rising investment through funding in this region. The funding is associated with a rising investment from the government, venture capitalists, mergers, and acquisitions.

In April 2020, the United States Food and Drug Administration (US FDA) issued guidelines to increase the availability of digital medical devices for mental health. With this in mind, the FDA aimed to subsidize people who followed home segregation guidelines or practiced social isolation without needing a clinic visit during the COVID-19 public health emergency. This will also reduce the burden on health care facilities and reduce the risk of exposure to the virus. Such initiatives by the government boost the market growth in the region.

The acquisition is another factor in the growth of the market. For instance, in February 2021, Philips announced the acquisition of BioTelemetry, Inc., one of the leading United States-based providers of remote cardiac diagnostics and monitoring. Product approval is another factor in the growth of the market. For instance, in June 2020, MedRhythms, a Portland, Maine-based digital therapeutics company received Food and Drug Administration clearance for its patented digital therapeutic to treat chronic stroke walking deficits. These intiatives will increase the market growth in the futrue.

Furthermore, an increase in the geriatric population, a rise in incidences of chronic diseases, the surge in demand for wireless and portable systems, and the availability of a sophisticated reimbursement structure that aims to reduce expenditure are few more factors boosting regional growth. For instance, in January 2021, as per the National Center for Chronic Disease Prevention and Health Promotion, 6 in 10 adults in the United States have a chronic disease and 4 in 10 adults have two or more chronic diseases and these conditions are posing around USD 3.8 trillion of healthcare costs on the country's healthcare system every year. Hence, due to above mentioned factors the market is likely to grow in the future.

Digital Therapeutic Devices Industry Overview

The digital therapeutic devices market is competitive, with quite a number of major players. The rising number of market players is intensifying the competition. The companies are also working in partnership with many employers, payers, healthcare systems, and pharma companies. Some of the major players are Philips NV, Omada Health Inc., WellDoc Inc., LIVONGO HEALTH, Pear Therapeutics, Noom Health Inc., etc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Burden of Chronic Diseases

- 4.2.2 Rise in Technological Adavancements

- 4.2.3 Increasing Focus Toward Preventive Healthcare by Government and Rise in Venture Capital Investments

- 4.3 Market Restraints

- 4.3.1 High Cost of Manufacturing and Installation

- 4.3.2 Data Privacy Concerns and Resistance from Traditional Healthcare Providers

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Product Type

- 5.1.1 Software and Services

- 5.1.2 Devices

- 5.2 By Application

- 5.2.1 Preventive

- 5.2.1.1 Pre-diabetes

- 5.2.1.2 Obesity

- 5.2.1.3 Smoking Cessation

- 5.2.1.4 Others

- 5.2.2 Treatment/Care

- 5.2.2.1 Cardiovascular Diseases

- 5.2.2.2 Diabetes

- 5.2.2.3 Neurological Disorders

- 5.2.2.4 Respiratory Diseases

- 5.2.2.5 Others

- 5.2.1 Preventive

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle-East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle-East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 2Morrow, Inc.

- 6.1.2 BigHealth

- 6.1.3 Canary Health

- 6.1.4 Koninklijke Philips NV (BioTelemetry Inc.)

- 6.1.5 Livongo Health

- 6.1.6 Mango Health Inc.

- 6.1.7 Noom Health Inc.

- 6.1.8 Omada Health Inc.

- 6.1.9 Pear Therapeutics

- 6.1.10 Propeller Health

- 6.1.11 Twine Health Inc.

- 6.1.12 WellDoc Inc.