|

市場調査レポート

商品コード

1438564

ペット用栄養補助食品:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Pet Dietary Supplements - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| ペット用栄養補助食品:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

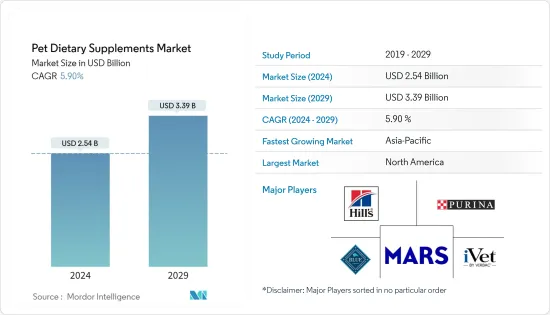

ペット用栄養補助食品市場規模は、2024年に25億4,000万米ドルと推定され、2029年までに33億9,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に5.90%のCAGRで成長します。

主なハイライト

- 栄養補助食品は、ペットの皮膚のかゆみ、消化器系の問題、肥満、アレルギーなどの病気や診断された健康障害の管理を支援するために特別に配合された動物性食品で構成されています。北米、ラテンアメリカ、アジア太平洋の新興国におけるブランド価値の向上とプレミアム製品に対する消費者の意識が市場の成長を促進します。多国籍企業は、いくつかのチャネルを通じて消費者の嗜好を強化するために、製品の認知度を高めるために多大な投資を行っています。

- さらに、市場では新興企業の成長やペット業界の大手企業による買収が市場に参入する様子が見られました。たとえば、2021年に発売されたPeople for Petsは、犬用サプリメントの新たな基準を打ち立て、目覚ましい成長を遂げました。同社はオーストラリア初の植物ベースの薬用水おやつ「ネクター・オブ・ザ・ドッグス」を発売し、2022年にオーストラリアン・リアル・ペット・フード・カンパニーに買収されました。

- さらに、栄養補助食品市場の犬セグメントは、予測期間中に最も急速な成長を遂げる可能性があります。ペットのために健康的で栄養価の高い食品を購入したいという犬の飼い主の関心により、世界中でさまざまな種類のドッグフードの販売が促進され、さまざまな栄養補助食品の発売につながっています。さらに、世界中でペットの犬の頭数が増加していることと、ペットの飼い主の健康上の懸念が増大していることにより、予測期間中の犬用栄養補助食品の世界の売上増加につながります。

ペット用栄養補助食品市場動向

ペットの栄養補助食品製品の購入決定に影響を与えるペットの人間化

ペットの飼い主が自分の動物を子供のように扱い、自分で使っているものと同等の製品を非常に受け入れる「ペットを家族として」という傾向は、ペットの人間化の自然な表現です。間違いなく、ペットを家族のように扱う飼い主が増えています。

近年、主流メディアはペットの人間化に細心の注意を払っています。ペットの人間化が消費者のペットフードの購入行動に及ぼす影響を理解することが不可欠です。ペットがますます家族の一員としてみなされるようになっているため、ペットの飼い主はペット用栄養補助食品への年間支出を積極的に増やしています。 2021年に米国ペット製品協会(APPA)が実施した調査によると、消費者の51%が高級ペットフードを購入し、33%がペットにビタミンやサプリメントを与え、21%がペットのために料理をし、18%が何らかのペットを飼っています。医療保険。ペット用食事療法製品に対する消費者の支出パターンを示しています。

さらに、ペットフード製造業者協会(PFMA)によると、2022年には英国の総人口の62%を占める1,740万世帯がペットを飼うことになり、2021年より2.3%増加すると予想されています。ペットの人間化と所有権の増加に向かう消費者の傾向と、ペットの健康問題の増加により、予測期間中にペット用栄養補助食品に十分なスペースが生まれると予想されます。

北米がペット用栄養補助食品市場を牽引

ペットや伴侶動物のための栄養補助食品や栄養補助食品の使用は北米市場でブームとなっており、米国は北米の栄養補助食品市場の75.0%以上を獲得しています。米国ペット製品協会(APPA)によると、米国には8,970万頭のペットの犬がいます。ペットの飼い主は犬のデンタルケアに年間平均49.70ドルを費やしており、2021年にはペットフードやおやつに500億米ドルを費やすと予想されています。2021年の全国ペット所有者調査によると、アメリカ人の約半数が同額を支出していることが観察されました。あるいは、自分自身のことよりも、ペットのヘルスケアに気を配っています。北米は世界のペットフード生産の31.0%を占めており、ペットケアに対する膨大な需要がアメリカのペット用栄養補助食品市場を牽引しています。

さらに、米国獣医歯科学会によると、犬の80%以上が3歳までに歯周病を発症し、猫の70%以上が同じ年齢で同じ問題に直面するとのこと。さらに、糖尿病もこの国でペットを襲う主要な病気の一つです。ペットの健康に対する意識の高まりと獣医医療支出の増加により、この地域の予測期間中に市場の成長が促進されると予想されます。

ペット用栄養補助食品業界の概要

ペット用栄養補助食品市場は統合されており、大手企業が市場のほぼ45%を占めており、特に市場参入者にとっては非常に激しい競合が生じています。買収と合併はこれらの主要企業が採用する主要な戦略活動であり、ペット用栄養補助食品市場の市場統合を強化します。企業はマーケティング支出やキャンペーンを通じてブランド認知度の向上に努めています。主要な市場プレーヤーは、買収、拡張、製品革新、パートナーシップを通じてブランド資産を構築しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 専門タイプ

- 尿路疾患

- 糖尿病

- 腎臓

- 消化器官の過敏症

- オーラルケア

- その他の専門タイプ

- ペットタイプ

- 犬

- 猫

- 鳥

- その他のペットタイプ

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 北米のその他の地域

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- スペイン

- イタリア

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東とアフリカ

- エジプト

- 南アフリカ

- その他中東およびアフリカ

- 北米

第6章 競合情勢

- 最も採用されている戦略

- 市場シェア分析

- 企業プロファイル

- Mars Inc.

- Hill's Pet Nutrition Inc.

- Nestle SA

- Blue Buffalo Pet Products Inc.

- iVet Professional Formulas

- Farmina Pet Foods

- Forza10 USA

- The Higgins Group Corp.

- NOW Foods

- Pet Naturals

- Affinity Petcare SA

第7章 市場機会と将来の動向

The Pet Dietary Supplements Market size is estimated at USD 2.54 billion in 2024, and is expected to reach USD 3.39 billion by 2029, growing at a CAGR of 5.90% during the forecast period (2024-2029).

Key Highlights

- Dietary supplements comprise animal foods specifically formulated to aid in managing illnesses and diagnosed health disorders, such as itchy skin, digestive issues, obesity, allergies, etc., in pets. Brand value enhancement in North America, Latin America, and the emerging countries of Asia-Pacific and consumer awareness about premium products fuel the growth of the market. Multinational players are making significant investments in increasing product awareness to strengthen consumer preference through several channels.

- Moreover, the market has witnessed the growth of start-up companies and acquisitions by the major players in the pet industry to enter the market. For instance, People for Pets, launched in 2021, achieved impressive growth by setting a new standard for dog supplements. The company launched Nectar of the Dogs, the first range of Australian-made, plant-based, medicinal water treats, and was acquired by the Australian Real Pet Food Company in 2022.

- Further, the dog segment of the dietary supplement market is likely to witness the fastest growth over the forecast period. Dog owners' interest in purchasing healthy and nutritious foods for their pets drives the sales of different types of dog foods globally, leading to the launch of various dietary supplement products. Further, the rising pet dog population worldwide, coupled with the increasing health concerns of pet owners, leads to an increase in global sales of dog dietary supplements during the forecast period.

Pet Dietary Supplements Market Trends

Pet Humanization to Influence the Purchase Decisions of Pet Dietary Supplement Products

The "pets as a family" trend, in which pet owners treat their animals like children and are extremely receptive to products comparable to those they use for themselves, is a natural expression of pet humanization. Undoubtedly, an increasing number of pet owners treat their animals like family.

In recent years, mainstream media has paid close attention to pet humanization.It is essential to understand the impact of pet humanization on consumer pet food buying behavior. As pets have increasingly become viewed as family members, pet owners are willing to increase their annual spending on pet dietary supplements. According to the survey conducted by the American Pet Products Association (APPA) in 2021, 51% of consumers purchase premium pet food, 33% give their pets vitamins and supplements, 21% cook for their pets, and 18% have some kind of pet medical insurance, illustrating the spending pattern of consumers on pet dietary products.

Furthermore, according to the Pet Food Manufacturers' Association (PFMA), in 2022, 17.4 million households, which constitute 62% of the total population in the United Kingdom, will own a pet, an increase of 2.3% from 2021. Thus, this consumer trend toward pet humanization and increased ownership, coupled with rising health issues in pets, is anticipated to create ample space for pet dietary supplements over the forecast period.

North America to Drive the Pet Dietary Supplements Market

The use of dietary supplements and nutraceuticals for pets and companion animals is booming in the North American market, subjecting the United States to garner more than 75.0% of the North American dietary supplement market. According to the American Pet Product Association (APPA), the United States has 89.7 million pet dogs. Pet owners spend an average of USD 49.70 on a dog's dental care annually and will spend USD 50 billion on pet food and treats in 2021. According to the National Pet Owners Survey in 2021, it was observed that around half of Americans spent the same amount or more on the healthcare of their pets than they did for themselves. North America is responsible for 31.0% of pet food production worldwide, with the huge demand for pet care driving the American pet dietary supplement market.

Further, according to the American Veterinary Dental Society, more than 80% of dogs develop gum disease by the age of three, and over 70% of cats face the same problem at the same age. Additionally, diabetes is also one of the major diseases attacking pets in the country. The rise in awareness of pet health and the increase in veterinary health expenditure are expected to propel market growth during the forecast period in the region.

Pet Dietary Supplements Industry Overview

The pet dietary supplement market is consolidated, with the major players accounting for almost 45% of the market, resulting in very stiff competition, especially for market entrants. Acquisitions and mergers are the major strategic activities adopted by these key players, strengthening market consolidation in the pet dietary supplement market. Companies are striving to increase brand awareness through marketing expenditures and campaigns. Major market players are building their brand equity through acquisitions, expansions, product innovations, and partnerships.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Specialty Type

- 5.1.1 Urinary Tract Disease

- 5.1.2 Diabetes

- 5.1.3 Renal

- 5.1.4 Digestive Sensitivity

- 5.1.5 Oral Care

- 5.1.6 Other Specialty Types

- 5.2 Pet Type

- 5.2.1 Dog

- 5.2.2 Cat

- 5.2.3 Bird

- 5.2.4 Other Pet Types

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Spain

- 5.3.2.6 Italy

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Egypt

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Mars Inc.

- 6.3.2 Hill's Pet Nutrition Inc.

- 6.3.3 Nestle SA

- 6.3.4 Blue Buffalo Pet Products Inc.

- 6.3.5 iVet Professional Formulas

- 6.3.6 Farmina Pet Foods

- 6.3.7 Forza10 USA

- 6.3.8 The Higgins Group Corp.

- 6.3.9 NOW Foods

- 6.3.10 Pet Naturals

- 6.3.11 Affinity Petcare S.A