|

|

市場調査レポート

商品コード

1136861

自動運航船の世界市場:自律性別 (完全自動運航、遠隔操作、部分自動運航)・船舶の種類別 (軍艦、商船)・ソリューション別・エンドユーザー別・推進方式別・地域別 (北米、欧州、アジア太平洋、他の国々 (RoW)) の将来予測 (2030年まで)Autonomous Ships Market by Autonomy (Fully Autonomous, Remotely Operated, Partially Autonomous), Ship Type (Military, Commercial), Solution, End User, Propulsion and Region (North America, Europe, APAC and Rest of the World) - Forecast to 2030 |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| 自動運航船の世界市場:自律性別 (完全自動運航、遠隔操作、部分自動運航)・船舶の種類別 (軍艦、商船)・ソリューション別・エンドユーザー別・推進方式別・地域別 (北米、欧州、アジア太平洋、他の国々 (RoW)) の将来予測 (2030年まで) |

|

出版日: 2022年10月10日

発行: MarketsandMarkets

ページ情報: 英文 288 Pages

納期: 即納可能

|

- 全表示

- 概要

- 目次

世界の自動運航船市場は、2022年に39億米ドルと推定され、2022年から2030年の間に9.6%のCAGRで成長し、2030年には82億米ドルに達すると予測されています。

市場の主な成長要因として、自動運航船の開発プロジェクトの増加や、世界の海上貿易の増加などが挙げられます。

ソリューション別 (システム別) では、知的認識システムが最大セグメントとなっています。船舶の種類別に見ると、今後はタンカー需要の増大に伴って自動運航船の市場需要も増加すると期待されています。

ノルウェーには多くの海洋オートメーションシステムメーカーや造船会社が立地しており、それが自動運航船市場の牽引役になると考えられています。同国は2022年時点で、欧州の自動運航船市場で最大のシェア(18.2%)を占めると推定されています。ノルウェーの自動運航船市場は、2022年から2030年の間に9.9%のCAGRで成長し、2030年までに6億1,000万米ドルに達すると予測されます。

当レポートでは、世界の自動運航船の市場について分析し、市場の基本構造や最新情勢、主な市場促進・抑制要因、自律性別・ソリューション別・船舶の種類別・エンドユーザー別・推進方式別・地域別の市場動向の見通し、市場競争の状態、主要企業のプロファイルなどを調査しております。

目次

第1章 イントロダクション

第2章 調査方法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- イントロダクション

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- 需要側への影響

- 主な動向 (2019年1月~2022年8月)

- 顧客のビジネスに影響を与える動向/混乱

- 市場のエコシステム

- 価格分析

- 関税・規制状況

- 貿易データ

- 特許分析

- 自動運航船市場のバリューチェーン分析

- 研究開発

- 原材料

- コンポーネント/製品メーカー(OEM)

- アセンブラ・インテグレータ

- エンドユーザー

- 技術分析

- 主要

- サポート技術

- ポーターのファイブフォース分析

- 主な利害関係者と購入基準

- ユースケース

- 主な会議とイベント (2022年~2023年)

- 運用データ

第6章 産業動向

- イントロダクション

- サプライチェーン分析

- 主要企業

- 中小企業

- エンドユーザー/顧客

- 業界の新たな動向

- デジタル船舶オートメーションシステム

- 制御アルゴリズム

- コニングシステム (航海情報表示装置)

- コネクティビティソリューション

- オートパイロット

- 係留制御・監視システム

- ARPA (自動衝突予防援助装置) / NRS (ナビゲーションレーダーサーバー)

- EDICS (電子海図表示情報システム)

- 通信システム

- 意思決定支援システム

- 船舶航行管理システム

- 自動運航船

- 統合船舶自動化システム

- メガトレンドの影響

- 人工知能

- ビッグデータ分析

- モノのインターネット(IoT)

- 宇宙技術を利用した衛星測位への関心増大

- イノベーションと特許登録

第7章 自動運航船市場:自律性別

- イントロダクション

- 部分的自動運航

- 遠隔操作

- 完全自動運航

第8章 自動運航船市場:ソリューション別

- イントロダクション

- システム

- 通信・コネクティビティ

- 知的認識システム

- ソフトウェア

- フリート管理ソフトウェア

- データ分析ソフトウェア

- 人工知能

- 構造物

第9章 自動運航船市場:船舶の種類別

- イントロダクション

- 商船

- 旅客船

- 貨物船

- その他

- 軍艦

- 航空母艦

- 水陸両用船

- 駆逐艦

- フリゲート艦

- 潜水艦

- 原子力潜水艦

第10章 自動運航船市場:エンドユーザー別

- イントロダクション

- ラインフィット・新造船

- レトロフィット

第11章 自動運航船市場:推進方式別

- イントロダクション

- 完全電動

- ハイブリッド

- 従来型

第12章 地域分析

- イントロダクション

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- デンマーク

- ノルウェー

- 英国

- ロシア

- オランダ

- 他の欧州諸国

- アジア太平洋

- 中国

- インド

- 日本

- シンガポール

- 韓国

- マレーシア

- 他のアジア太平洋諸国

- 他の国々 (RoW)

- 中東・アフリカ

- ラテンアメリカ

第13章 競合情勢

- イントロダクション

- 主要企業の戦略

- 主要企業の市場シェア分析 (2021年)

- 上位5社の収益シェア分析 (2019年~2021年)

- ランク分析 (2021年)

- 競合評価クアドラント

- 競合ベンチマーキング

- 主要なスタートアップ/中小企業の一覧と競合ベンチマーキング

- 競合シナリオ

- 新製品の発売

- 資本取引

第14章 企業プロファイル

- イントロダクション

- 主要企業

- KONGSBERG MARITIME

- ABB

- ROLLS-ROYCE PLC

- HYUNDAI HEAVY INDUSTRIES

- FUGRO

- WARTSILA

- HONEYWELL INTERNATIONAL INC.

- SIEMENS

- GENERAL ELECTRIC

- L3HARRIS ASV

- NORTHROP GRUMMAN CORPORATION

- MITSUI E&S HOLDINGS CO., LTD.

- VALMET

- ASELSAN A.S.

- BAE SYSTEMS

- SAMSUNG HEAVY INDUSTRIES CO., LTD.

- MARINE TECHNOLOGIES LLC

- PRAXIS AUTOMATION TECHNOLOGY B.V.

- DNV GL

- ULSTEIN

- VIGOR INDUSTRIAL LLC

- その他の企業

- RH MARINE

- MARLINK

- SEA MACHINES ROBOTICS, INC.

- SHONE AUTOMATION, INC.

- ORCA AI

- BUFFALO AUTOMATION

- LADAR LTD.

第15章 付録

The autonomous ships market is estimated to be USD 3.9 billion in 2022 and is projected to reach USD 8.2 billion by 2030, at a CAGR of 9.6% from 2022 to 2030. Growth of this market can be attributed to the rise in increasing number of autonomous ship development projects, and rise in global seaborne trade, among others.

"Control Algorithms for Autonomous Ships"

Navigation and collision avoidance systems are particularly important in autonomous ships, as these systems allow control algorithms to decide the actions that need to be undertaken in accordance with the information received from different sensors. These actions are required to adhere to maritime rules and regulations. Thus, control algorithms of autonomous ships should be able to accurately interpret the information obtained from different sensors, thereby leading to interpretation challenges for programmers developing control algorithms for these ships. The development of control algorithms for autonomous ships is expected to take place gradually as it is an iterative process, which is subject to extensive testing and simulation. For example, in 2020, ProMare (US) and IBM (US) partnered for advancements in machine learning algorithms for the development of the fully autonomous Mayflower ship.

"Connectivity Solutions for Autonomous ships"

The evolution of communication technology, from Wi-Fi to 5G connectivity, has led to the conceptualization of autonomous ships. These ships allow operators to access live audio as well as HD and 3D videos from onboard recording devices, thereby eliminating the requirement for physical onboard surveying of ships. Advancements in communication technology are expected to help improve decision-making for enhanced ship management. They are also expected to ensure autonomous ships' smooth operations and uninterrupted and improved communication between crew members and onshore stations. For example, Raytheon Anschutz (Germany) has developed a 5G-based connectivity module for passenger ferries in Kiel, Germany.

.

"Intelligent Awareness System: The largest segment of the autonomous ship Solution market, by Systems"

The intelligent awareness system is designed for operational safety and efficiency. This system is further segmented into alarm management systems, surveillance & safety systems, and navigation systems. Major market leaders are developing intelligent awareness systems. In 2018, Rolls-Royce launched the Intelligent Awareness (IA) system, a part of the ongoing development of autonomous ship projects like the development of fully autonomous cruise ships for Finferries.

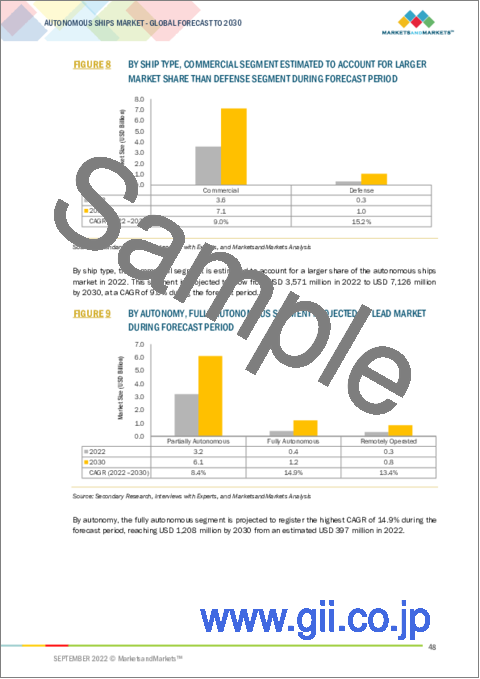

"Tankers: The largest segment of the commercial autonomous ships market, by Cargo vessel Type"

Tankers are ships that serve specific operational purposes, such as transporting chemicals and liquid assets in bulk. A rise in demand for chemical tankers by ship merchants is expected due to an increase in the international trade of chemicals and liquid materials. An increase in oil exploration and international trade in liquid natural gas is expected to drive the demand for tankers, which, in turn, is expected to drive demand for automation systems.

"Norway: The largest contributing country in the European autonomous ships market"

Most marine automation system manufacturers and shipbuilders such as Kongsberg, Ulstein, and Vard are based in Norway, which is expected to drive the market for autonomous ships in this country. Norway is estimated to account for the largest share (18.2%) of the overall European autonomous ships market in 2022.

The autonomous ships market in Norway is projected to reach USD 610 million by 2030, at a CAGR of 9.9% between 2022 and 2030.

Breakdown of primaries

The study contains insights from various industry experts, ranging from component suppliers to Tier 1 companies and OEMs. The break-up of the primaries is as follows:

- By Company Type: Tier 1-35%; Tier 2-45%; and Tier 3-20%

- By Designation: C Level-35%; Directors-25%; and Others-40%

- By Region: North America-25%; Europe-15%; Asia Pacific-45%; Middle East- 10%; and Rest of the World -5%

Kongsberg Maritime (Norway), Fugro (Netherlands), Hyundai Heavy Industries (South Korea), BAE Systems (UK), and Rolls-Royce PLC (UK) are the key players in the autonomous ships market.

Research Coverage

The study covers the autonomous ships market across various segments and subsegments. It aims at estimating the size and growth potential of this market across different segments based on Autonomy, Ship Type, End User, Solution, Propulsion, and region. This study also includes an in-depth competitive analysis of the key players in the market, along with their company profiles, key observations related to their product and business offerings, recent developments undertaken by them, and key market strategies adopted by them.

Reasons to Buy this Report

This report is expected to help market leaders/new entrants with information on the closest approximations of the revenue numbers for the overall autonomous ships market and its segments. This study is also expected to provide region wise information about the end use, and wherein autonomous ships are used. This report aims at helping the stakeholders understand the competitive landscape of the market, gain insights to improve the position of their businesses and plan suitable go-to-market strategies. This report is also expected to help them understand the pulse of the market and provide them with information on key drivers, restraints, challenges, and opportunities influencing the growth of the market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKETS SCOPE

- 1.3.1 MARKETS COVERED

- FIGURE 1 AUTONOMOUS SHIPS MARKET SEGMENTATION

- 1.3.2 REGIONAL SCOPE

- 1.3.3 YEARS CONSIDERED

- 1.4 INCLUSIONS AND EXCLUSIONS

- 1.5 CURRENCY CONSIDERED

- 1.6 USD EXCHANGE RATES

- 1.7 LIMITATIONS

- 1.8 MARKET STAKEHOLDERS

- 1.9 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 2 REPORT PROCESS FLOW

- FIGURE 3 RESEARCH DESIGN

- 2.1.1 SECONDARY DATA

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Key primary sources

- FIGURE 4 BREAKDOWN OF PRIMARY INTERVIEWS: BY COMPANY TYPE, DESIGNATION, AND REGION

- 2.2 FACTOR ANALYSIS

- 2.2.1 DEMAND-SIDE INDICATORS

- 2.2.2 SUPPLY-SIDE ANALYSIS

- 2.3 MARKET SIZE ESTIMATION

- 2.3.1 SEGMENTS AND SUBSEGMENTS

- 2.4 RESEARCH APPROACH & METHODOLOGY

- 2.4.1 BOTTOM-UP APPROACH

- TABLE 1 AUTONOMOUS SHIPS MARKET ESTIMATION PROCEDURE

- FIGURE 5 MARKET SIZE ESTIMATION METHODOLOGY: BOTTOM-UP APPROACH

- 2.4.2 TOP-DOWN APPROACH

- FIGURE 6 MARKET SIZE ESTIMATION METHODOLOGY: TOP-DOWN APPROACH

- 2.5 DATA TRIANGULATION

- FIGURE 7 DATA TRIANGULATION

- 2.5.1 TRIANGULATION THROUGH PRIMARY AND SECONDARY RESEARCH

- 2.6 GROWTH RATE ASSUMPTIONS

- 2.7 ASSUMPTIONS FOR RESEARCH STUDY

- 2.8 RISKS

3 EXECUTIVE SUMMARY

- FIGURE 8 BY SHIP TYPE, COMMERCIAL SEGMENT ESTIMATED TO ACCOUNT FOR LARGER MARKET SHARE THAN DEFENSE SEGMENT DURING FORECAST PERIOD

- FIGURE 9 BY AUTONOMY, FULLY AUTONOMOUS SEGMENT PROJECTED TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 10 BY SOLUTION, SYSTEMS SEGMENT ESTIMATED TO LEAD AUTONOMOUS SHIPS MARKET DURING FORECAST PERIOD

- FIGURE 11 BY END USER, LINE-FIT & NEWBUILD SEGMENT ESTIMATED TO ACCOUNT FOR LARGER MARKET SHARE DURING FORECAST PERIOD

- FIGURE 12 BY PROPULSION, HYBRID SEGMENT PROJECTED TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 13 AUTONOMOUS SHIPS MARKET IN ASIA PACIFIC TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN AUTONOMOUS SHIPS MARKET FROM 2022 TO 2030

- FIGURE 14 INCREASING INVESTMENTS IN AUTONOMOUS SHIPS TECHNOLOGY TO DRIVE MARKET

- 4.2 AUTONOMOUS SHIPS MARKET, BY AUTONOMY

- FIGURE 15 PARTIALLY AUTONOMOUS SEGMENT EXPECTED TO DOMINATE MARKET DURING FORECAST PERIOD

- 4.3 AUTONOMOUS SHIPS MARKET, BY SHIP TYPE

- FIGURE 16 COMMERCIAL SEGMENT ESTIMATED TO LEAD MARKET FROM 2022 TO 2030

- 4.4 AUTONOMOUS SHIPS MARKET, BY SOLUTION

- FIGURE 17 SYSTEMS SEGMENT ESTIMATED TO DOMINATE MARKET DURING FORECAST PERIOD

- 4.5 AUTONOMOUS SHIPS MARKET, BY END USER

- FIGURE 18 LINE-FIT & NEWBUILD SEGMENT ESTIMATED TO LEAD MARKET DURING FORECAST PERIOD

- 4.6 AUTONOMOUS SHIPS MARKET, BY PROPULSION

- FIGURE 19 CONVENTIONAL SEGMENT ESTIMATED TO DOMINATE MARKET DURING FORECAST PERIOD

- 4.7 AUTONOMOUS SHIPS MARKET, BY COUNTRY

- FIGURE 20 AUTONOMOUS SHIPS MARKET IN SOUTH KOREA TO REGISTER HIGHEST CAGR FROM 2022 TO 2030

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 21 AUTONOMOUS SHIPS MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Development of next-generation autonomous vessels

- 5.2.1.2 Increasing development of software

- 5.2.1.3 Growing use of automated systems to reduce human errors and risks

- FIGURE 22 NUMBER OF MARINE ACCIDENTS, BY GEOGRAPHY

- 5.2.1.4 Increased budgets of shipping companies to incorporate ICT in vessels

- 5.2.1.5 Rising demand for situational awareness in vessels

- 5.2.2 RESTRAINTS

- 5.2.2.1 Vulnerability associated with cyber threats

- FIGURE 23 POTENTIAL CYBERATTACK ROUTES FOR MARINE VESSELS

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Initiatives to develop autonomous ships

- FIGURE 24 TIMELINE AND DESIGN DEVELOPMENT TARGETS FOR AUTONOMOUS SHIPS

- 5.2.3.2 Revision and formulation of marine safety regulations in several countries

- 5.2.3.3 Advancements in sensor technology for improved navigation in autonomous ships

- 5.2.3.4 Development of propulsion systems for autonomous ships

- 5.2.4 CHALLENGES

- 5.2.4.1 Cost-intensive customization of marine automation systems

- 5.2.4.2 Lack of skilled personnel to handle and operate marine automation systems

- 5.2.4.3 Lack of common standards for data generated from different subsystems in ships

- 5.2.4.4 Regulatory barriers to autonomous ships

- 5.3 DEMAND-SIDE IMPACT

- 5.3.1 KEY DEVELOPMENTS FROM JANUARY 2019 TO AUGUST 2022

- TABLE 2 KEY DEVELOPMENTS IN AUTONOMOUS SHIPS MARKET IN 2022

- 5.4 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- FIGURE 25 TRENDS AND DISRUPTIONS IMPACTING CUSTOMERS

- 5.5 MARKET ECOSYSTEM

- FIGURE 26 AUTONOMOUS SHIPS MARKET ECOSYSTEM

- 5.5.1 PROMINENT COMPANIES

- 5.5.2 PRIVATE AND SMALL ENTERPRISES

- 5.5.3 END USERS

- TABLE 3 AUTONOMOUS SHIPS MARKET ECOSYSTEM

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE ANALYSIS OF AUTONOMOUS SYSTEMS, 2021

- FIGURE 27 AVERAGE SELLING PRICE OF AUTONOMOUS SHIPS OFFERED BY TOP PLAYERS

- 5.7 TARIFF REGULATORY LANDSCAPE

- 5.7.1 NORTH AMERICA

- TABLE 4 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHERS

- 5.7.2 EUROPE

- TABLE 5 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHERS

- 5.7.3 ASIA PACIFIC

- TABLE 6 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHERS

- 5.7.4 MIDDLE EAST

- TABLE 7 MIDDLE EAST: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHERS

- 5.7.5 REST OF THE WORLD

- TABLE 8 REST OF THE WORLD: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHERS

- 5.8 TRADE DATA

- TABLE 9 COUNTRY-WISE IMPORTS, 2019-2021 (USD THOUSAND)

- TABLE 10 COUNTRY-WISE EXPORTS, 2019-2021 (USD THOUSAND)

- 5.9 PATENT ANALYSIS

- FIGURE 28 LIST OF MAJOR PATENTS FOR AUTONOMOUS SHIPS

- TABLE 11 LIST OF MAJOR PATENTS FOR AUTONOMOUS SHIPS

- 5.10 VALUE CHAIN ANALYSIS OF AUTONOMOUS SHIPS MARKET

- FIGURE 29 VALUE CHAIN ANALYSIS

- 5.10.1 RESEARCH & DEVELOPMENT

- 5.10.2 RAW MATERIALS

- 5.10.3 COMPONENT/PRODUCT MANUFACTURERS (OEMS)

- 5.10.4 ASSEMBLERS & INTEGRATORS

- 5.10.5 END USERS

- 5.11 TECHNOLOGY ANALYSIS

- 5.11.1 KEY TECHNOLOGY

- 5.11.1.1 Autonomous navigation systems for marine vessels

- 5.11.1.2 AI-based marine autonomous systems

- 5.11.2 SUPPORTING TECHNOLOGY

- 5.11.2.1 Sensor fusion solutions

- 5.11.2.2 Voyage data recorders

- 5.11.1 KEY TECHNOLOGY

- 5.12 PORTER'S FIVE FORCES ANALYSIS

- TABLE 12 PORTER'S FIVE FORCES ANALYSIS

- FIGURE 30 PORTER'S FIVE FORCES ANALYSIS

- 5.12.1 THREAT OF NEW ENTRANTS

- 5.12.2 THREAT OF SUBSTITUTES

- 5.12.3 BARGAINING POWER OF SUPPLIERS

- 5.12.4 BARGAINING POWER OF BUYERS

- 5.12.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.13 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.13.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 31 INFLUENCE OF STAKEHOLDERS IN BUYING AUTONOMOUS SHIPS, BY SHIP TYPE

- TABLE 13 INFLUENCE OF STAKEHOLDERS IN BUYING AUTONOMOUS SHIPS, BY SHIP TYPE (%)

- 5.13.2 BUYING CRITERIA

- FIGURE 32 KEY BUYING CRITERIA FOR AUTONOMOUS SHIPS, BY AUTONOMY

- TABLE 14 KEY BUYING CRITERIA FOR AUTONOMOUS SHIPS, BY AUTONOMY

- 5.14 USE CASES

- 5.14.1 USE OF 5G COMMUNICATION SYSTEMS IN ENVIRONMENTALLY FRIENDLY, AUTONOMOUS MOBILITY CHAIN FOR LOCAL PUBLIC TRANSPORT IN KIEL, GERMANY

- 5.14.2 CHINA LAUNCHES FIRST AUTONOMOUS CONTAINER SHIP INTO COMMERCIAL SERVICE

- 5.14.3 AUTONOMOUS MARINE SURVEYING

- 5.15 KEY CONFERENCES AND EVENTS, 2022-23

- TABLE 15 AUTONOMOUS SHIPS MARKET: DETAILED LIST OF CONFERENCES AND EVENTS

- 5.16 OPERATIONAL DATA

- TABLE 16 NEW COMMERCIAL SHIP DELIVERIES, BY SHIP TYPE, 2017-2020

6 INDUSTRY TRENDS

- 6.1 INTRODUCTION

- 6.2 SUPPLY CHAIN ANALYSIS

- FIGURE 33 SUPPLY CHAIN ANALYSIS

- 6.2.1 MAJOR COMPANIES

- 6.2.2 SMALL AND MEDIUM ENTERPRISES

- 6.2.3 END USERS/CUSTOMERS

- 6.3 EMERGING INDUSTRY TRENDS

- TABLE 17 ADVANCEMENTS IN AUTONOMOUS SHIPS IN KEY NATIONS

- 6.3.1 DIGITAL MARINE AUTOMATION SYSTEMS

- 6.3.2 CONTROL ALGORITHMS

- 6.3.3 CONNING SYSTEMS

- 6.3.4 CONNECTIVITY SOLUTIONS

- 6.3.5 AUTOPILOT

- 6.3.6 MOORING CONTROL AND MONITORING SYSTEMS

- 6.3.7 AUTOMATED RADAR PLOTTING AID/NAVIGATION RADAR SERVERS (NRS)

- 6.3.8 ELECTRONIC CHART DISPLAY AND INFORMATION SYSTEMS

- 6.3.9 COMMUNICATION SYSTEMS

- 6.3.10 DECISION SUPPORT SYSTEMS

- 6.3.11 VESSEL TRAFFIC MANAGEMENT SYSTEMS

- 6.3.12 AUTONOMOUS SHIPS

- 6.3.13 INTEGRATED SHIP AUTOMATION SYSTEMS

- 6.4 IMPACT OF MEGATRENDS

- 6.4.1 ARTIFICIAL INTELLIGENCE

- 6.4.2 BIG DATA ANALYTICS

- 6.4.3 INTERNET OF THINGS (IOT)

- 6.4.4 INCREASING FOCUS ON SATELLITE-BASED POSITIONING USING SPACE TECHNOLOGIES

- 6.5 INNOVATIONS AND PATENT REGISTRATIONS

- TABLE 18 INNOVATIONS AND PATENT REGISTRATIONS, 2014-2021

7 AUTONOMOUS SHIPS MARKET, BY AUTONOMY

- 7.1 INTRODUCTION

- FIGURE 34 AUTONOMOUS SHIPS MARKET, BY AUTONOMY, 2022 & 2030 (USD MILLION)

- TABLE 19 AUTONOMOUS SHIPS MARKET, BY AUTONOMY, 2018-2021 (USD MILLION)

- TABLE 20 AUTONOMOUS SHIPS MARKET, BY AUTONOMY, 2022-2030 (USD MILLION)

- 7.2 PARTIALLY AUTONOMOUS

- 7.2.1 INCREASING DEMAND FOR ONBOARD AUTOMATION SYSTEMS TO DRIVE SEGMENT

- 7.3 REMOTELY OPERATED

- 7.3.1 INCREASING INVESTMENTS IN REMOTELY OPERATED SHIPS TO DRIVE SEGMENT

- 7.4 FULLY AUTONOMOUS

- 7.4.1 INCREASING INVESTMENTS IN DEVELOPMENT OF AUTONOMOUS SHIPS TO FUEL SEGMENT

8 AUTONOMOUS SHIPS MARKET, BY SOLUTION

- 8.1 INTRODUCTION

- FIGURE 35 AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2022 & 2030 (USD MILLION)

- TABLE 21 AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2018-2021 (USD MILLION)

- TABLE 22 AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2022-2030 (USD MILLION)

- 8.2 SYSTEMS

- FIGURE 36 SYSTEMS IN AUTONOMOUS SHIPS MARKET, BY TYPE, 2022 & 2030 (USD MILLION)

- TABLE 23 SYSTEMS IN AUTONOMOUS SHIPS MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 24 SYSTEMS IN AUTONOMOUS SHIPS MARKET, BY TYPE, 2022-2030 (USD MILLION)

- 8.2.1 COMMUNICATION & CONNECTIVITY

- 8.2.1.1 Rising demand for satellite connectivity and mobile satellite devices to drive segment

- TABLE 25 COMMUNICATION & CONNECTIVITY IN AUTONOMOUS SHIPS MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 26 COMMUNICATION & CONNECTIVITY IN AUTONOMOUS SHIPS MARKET, BY TYPE, 2022-2030 (USD MILLION)

- 8.2.1.2 Satellite systems

- 8.2.1.2.1 Use of satellite systems to achieve safe operation in deep sea drives segment's growth

- 8.2.1.3 Very small aperture terminals

- 8.2.1.3.1 Increasing use of VSAT systems in ship-to-shore communication to drive segment

- 8.2.1.4 Terrestrial communication systems

- 8.2.1.4.1 Use of terrestrial communication systems for ship-to-ship connectivity to drive demand

- 8.2.1.5 5G mobile communication networks

- 8.2.1.5.1 Increasing popularity and benefits of 5G mobile communication networks in maritime industry to drive segment

- 8.2.1.2 Satellite systems

- 8.2.2 INTELLIGENT AWARENESS SYSTEM

- 8.2.2.1 Increasing use of advanced sensor technology in surveillance & safety systems to drive segment

- TABLE 27 INTELLIGENT AWARENESS SYSTEM IN AUTONOMOUS SHIPS MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 28 INTELLIGENT AWARENESS SYSTEM IN AUTONOMOUS SHIPS MARKET, BY TYPE, 2022-2030 (USD MILLION)

- 8.2.2.2 Alarm management systems

- 8.2.2.2.1 Need to avoid system failures & accidents to drive demand for alarm management systems in autonomous ships

- 8.2.2.3 Surveillance and safety systems

- 8.2.2.3.1 Integration of visual data with surveillance command and control systems responsible for technological advancement and increasing use of surveillance and safety systems

- 8.2.2.3.2 Radar

- 8.2.2.3.3 Automatic identification system

- 8.2.2.3.4 Optical and infra-red cameras

- 8.2.2.3.5 High-resolution sonar

- 8.2.2.4 Navigation systems

- 8.2.2.4.1 Need for safe navigation of autonomous vessels to drive demand for navigation systems

- 8.2.2.4.2 LiDAR

- 8.2.2.4.3 GPS

- 8.2.2.4.4 Inertial navigation systems

- 8.2.2.5 Machinery management systems

- 8.2.2.5.1 Importance of monitoring health and functions of vessel systems fuels demand for machinery management systems

- 8.2.2.6 Power management systems

- 8.2.2.6.1 Importance of power supply in vessels boosts PMS market

- 8.2.2.7 Propulsion control systems

- 8.2.2.7.1 Optimum performance of propulsion systems drives demand for propulsion control systems

- 8.2.2.8 Other systems

- 8.2.2.8.1 Reliability, health, and safety management systems

- 8.2.2.8.2 Ship information management systems

- 8.2.2.8.3 Ballast management systems

- 8.2.2.8.4 Thruster control systems

- 8.2.2.2 Alarm management systems

- 8.3 SOFTWARE

- FIGURE 37 SOFTWARE IN AUTONOMOUS SHIPS MARKET, BY TYPE, 2022 & 2030 (USD MILLION)

- TABLE 29 SOFTWARE IN AUTONOMOUS SHIPS MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 30 SOFTWARE IN AUTONOMOUS SHIPS MARKET, BY TYPE, 2022-2030 (USD MILLION)

- 8.3.1 FLEET MANAGEMENT SOFTWARE

- 8.3.1.1 Increase in marine vessel deliveries to boost demand for fleet management software

- 8.3.2 DATA ANALYSIS SOFTWARE

- 8.3.2.1 Increasing need for voyage planning to drive data analysis software demand

- 8.3.3 ARTIFICIAL INTELLIGENCE

- 8.3.3.1 Increasing adoption of autonomous ships to drive demand for artificial intelligence

- 8.3.3.2 Machine learning

- 8.3.3.3 Computer vision

- 8.4 STRUCTURES

- 8.4.1 INCREASING DEPLOYMENT OF FULLY AUTONOMOUS SHIPS TO DRIVE DEMAND FOR STRUCTURES

9 AUTONOMOUS SHIPS MARKET, BY SHIP TYPE

- 9.1 INTRODUCTION

- FIGURE 38 AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2022 & 2030 (USD MILLION)

- TABLE 31 AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2018-2021 (USD MILLION)

- TABLE 32 AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2022-2030 (USD MILLION)

- 9.2 COMMERCIAL

- FIGURE 39 COMMERCIAL AUTONOMOUS SHIPS MARKET, BY TYPE, 2022-2030 (USD MILLION)

- TABLE 33 COMMERCIAL AUTONOMOUS SHIPS MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 34 COMMERCIAL AUTONOMOUS SHIPS MARKET, BY TYPE, 2022-2030 (USD MILLION)

- 9.2.1 PASSENGER VESSELS

- TABLE 35 PASSENGER AUTONOMOUS VESSELS MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 36 PASSENGER AUTONOMOUS VESSELS MARKET, BY TYPE, 2022-2030 (USD MILLION)

- 9.2.1.1 Cruise ships

- 9.2.1.1.1 Growth in international sea travel to boost demand for passenger ships & cruises

- 9.2.1.2 Passenger ferries

- 9.2.1.2.1 Development in small autonomous inland passenger ferries to drive segment

- 9.2.1.3 Yachts & motorboats

- 9.2.1.3.1 Growing demand for yachts for luxury sailing in North America and Europe

- 9.2.1.1 Cruise ships

- 9.2.2 CARGO VESSELS

- TABLE 37 CARGO AUTONOMOUS VESSELS MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 38 CARGO AUTONOMOUS VESSELS MARKET, BY TYPE, 2022-2030 (USD MILLION)

- 9.2.2.1 Bulk carriers

- 9.2.2.1.1 Growth in world seaborne trade to drive demand for bulk carriers

- 9.2.2.2 Gas tankers

- 9.2.2.2.1 Increasing LPG trade to drive segment

- 9.2.2.3 Tankers

- 9.2.2.3.1 Transportation of chemicals and liquid assets in bulk drives demand for tankers

- 9.2.2.4 Dry cargo vessels

- 9.2.2.4.1 Growing demand for dry cargo ships for international maritime trade to drive market

- 9.2.2.5 Container vessels

- 9.2.2.5.1 Increasing seaborne trade to drive demand for container ships

- 9.2.2.6 Barges and tugboats

- 9.2.2.6.1 Growing demand for oil exploration and construction work to drive segment

- 9.2.2.1 Bulk carriers

- 9.2.3 OTHERS

- 9.2.3.1 Research vessels

- 9.2.3.1.1 Increasing demand for research vessels for various applications to drive autonomous ships market

- 9.2.3.2 Dredgers

- 9.2.3.2.1 Increasing demand for dredgers to remove debris and sediments

- 9.2.3.1 Research vessels

- 9.3 DEFENSE

- FIGURE 40 DEFENSE AUTONOMOUS SHIPS MARKET, BY TYPE, 2022-2030 (USD MILLION)

- TABLE 39 DEFENSE AUTONOMOUS SHIPS MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 40 DEFENSE AUTONOMOUS SHIPS MARKET, BY TYPE, 2022-2030 (USD MILLION)

- 9.3.1 AIRCRAFT CARRIERS

- 9.3.1.1 Upgrading of aircraft carriers with new autonomous systems to drive market

- 9.3.2 AMPHIBIOUS SHIPS

- 9.3.2.1 Increasing demand for amphibious warfare ships by various countries to drive autonomous ships market

- 9.3.3 DESTROYERS

- 9.3.3.1 Destroyers protect large vessels against small but powerful short-range attackers

- 9.3.4 FRIGATES

- 9.3.4.1 Increasing use of autonomous systems on frigates to drive market

- 9.3.5 SUBMARINES

- 9.3.5.1 Increasing investment in submarine developments to drive market

- 9.3.6 NUCLEAR SUBMARINES

- 9.3.6.1 Increasing use of automation in nuclear submarines to drive market

10 AUTONOMOUS SHIPS MARKET, BY END USER

- 10.1 INTRODUCTION

- FIGURE 41 AUTONOMOUS SHIPS MARKET, BY END USER, 2022 & 2030

- TABLE 41 AUTONOMOUS SHIPS MARKET, BY END USER, 2018-2021 (USD MILLION)

- TABLE 42 AUTONOMOUS SHIPS MARKET, BY END USER, 2022-2030 (USD MILLION)

- 10.2 LINE-FIT & NEWBUILD

- 10.2.1 INCREASING DEMAND FOR AUTOMATED SYSTEMS IN NEW SHIPS TO DRIVE SEGMENT

- 10.3 RETROFIT

- 10.3.1 RETROFITTING INVOLVES INTEGRATING COMPONENTS AND SYSTEMS IN EXISTING SHIPS DURING MAINTENANCE, REPAIR, AND OVERHAUL

11 AUTONOMOUS SHIPS MARKET, BY PROPULSION

- 11.1 INTRODUCTION

- FIGURE 42 AUTONOMOUS SHIPS MARKET, BY PROPULSION, 2022 & 2030 (USD MILLION)

- TABLE 43 AUTONOMOUS SHIPS MARKET, BY PROPULSION, 2018-2021 (USD MILLION)

- TABLE 44 AUTONOMOUS SHIPS MARKET, BY PROPULSION, 2022-2030 (USD MILLION)

- 11.2 FULLY ELECTRIC

- 11.2.1 TECHNOLOGICAL DEVELOPMENTS RESULT IN ADOPTION OF ELECTRIC PROPULSION IN NAVAL DESTROYERS IN UK AND US

- 11.3 HYBRID

- 11.3.1 HYBRID PROPULSION SYSTEMS HELP REDUCE SIGNIFICANT GREENHOUSE GASES

- 11.4 CONVENTIONAL

- 11.4.1 INCREASING R&D ACTIVITIES IN MARINE INDUSTRY TO DRIVE SEGMENT

12 REGIONAL ANALYSIS

- 12.1 INTRODUCTION

- FIGURE 43 EUROPE ESTIMATED TO ACCOUNT FOR LARGEST MARKET SHARE IN 2022

- TABLE 45 AUTONOMOUS SHIPS MARKET, BY REGION, 2018-2021 (USD MILLION)

- TABLE 46 AUTONOMOUS SHIPS MARKET, BY REGION, 2022-2030 (USD MILLION)

- 12.2 NORTH AMERICA

- 12.2.1 PESTLE ANALYSIS: NORTH AMERICA

- FIGURE 44 NORTH AMERICA AUTONOMOUS SHIPS MARKET SNAPSHOT

- TABLE 47 NORTH AMERICA: AUTONOMOUS SHIPS MARKET, BY COUNTRY, 2018-2021 (USD MILLION)

- TABLE 48 NORTH AMERICA: AUTONOMOUS SHIPS MARKET, BY COUNTRY, 2022-2030 (USD MILLION)

- TABLE 49 NORTH AMERICA: AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2018-2021 (USD MILLION)

- TABLE 50 NORTH AMERICA: AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2022-2030 (USD MILLION)

- TABLE 51 NORTH AMERICA: COMMERCIAL AUTONOMOUS SHIPS MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 52 NORTH AMERICA: COMMERCIAL AUTONOMOUS SHIPS MARKET, BY TYPE, 2022-2030 (USD MILLION)

- TABLE 53 NORTH AMERICA: DEFENSE AUTONOMOUS SHIPS MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 54 NORTH AMERICA: DEFENSE AUTONOMOUS SHIPS MARKET, BY TYPE, 2022-2030 (USD MILLION)

- TABLE 55 NORTH AMERICA: AUTONOMOUS SHIPS MARKET, BY AUTONOMY, 2018-2021 (USD MILLION)

- TABLE 56 NORTH AMERICA: AUTONOMOUS SHIPS MARKET, BY AUTONOMY, 2022-2030 (USD MILLION)

- TABLE 57 NORTH AMERICA: AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2018-2021 (USD MILLION)

- TABLE 58 NORTH AMERICA: AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2022-2030 (USD MILLION)

- TABLE 59 NORTH AMERICA: SYSTEMS FOR AUTONOMOUS SHIPS MARKET, BY CATEGORY, 2018-2021 (USD MILLION)

- TABLE 60 NORTH AMERICA: SYSTEMS FOR AUTONOMOUS SHIPS MARKET, BY CATEGORY, 2022-2030 (USD MILLION)

- TABLE 61 NORTH AMERICA: INTELLIGENT AWARENESS SYSTEM FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 62 NORTH AMERICA: INTELLIGENT AWARENESS SYSTEM FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2022-2030 (USD MILLION)

- TABLE 63 NORTH AMERICA: SOFTWARE FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 64 NORTH AMERICA: SOFTWARE FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2022-2030 (USD MILLION)

- TABLE 65 NORTH AMERICA: AUTONOMOUS SHIPS MARKET, BY END USER, 2018-2021 (USD MILLION)

- TABLE 66 NORTH AMERICA: AUTONOMOUS SHIPS MARKET, BY END USER, 2022-2030 (USD MILLION)

- TABLE 67 NORTH AMERICA: AUTONOMOUS SHIPS MARKET, BY PROPULSION, 2018-2021 (USD MILLION)

- TABLE 68 NORTH AMERICA: AUTONOMOUS SHIPS MARKET, BY PROPULSION, 2022-2030 (USD MILLION)

- 12.2.2 US

- 12.2.2.1 Increase in naval shipbuilding to drive market

- TABLE 69 US: AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2018-2021 (USD MILLION)

- TABLE 70 US: AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2022-2030 (USD MILLION)

- TABLE 71 US: AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2018-2021 (USD MILLION)

- TABLE 72 US: AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2022-2030 (USD MILLION)

- TABLE 73 US: SYSTEMS FOR AUTONOMOUS SHIPS MARKET, BY CATEGORY, 2018-2021 (USD MILLION)

- TABLE 74 US: SYSTEMS FOR AUTONOMOUS SHIPS MARKET, BY CATEGORY, 2022-2030 (USD MILLION)

- TABLE 75 US: SOFTWARE FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 76 US: SOFTWARE FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2022-2030 (USD MILLION)

- TABLE 77 US: AUTONOMOUS SHIPS MARKET, BY END USER, 2018-2021 (USD MILLION)

- TABLE 78 US: AUTONOMOUS SHIPS MARKET, BY END USER, 2022-2030 (USD MILLION)

- 12.2.3 CANADA

- 12.2.3.1 Increased trade activities to drive market

- TABLE 79 CANADA: AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2018-2021 (USD MILLION)

- TABLE 80 CANADA: AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2022-2030 (USD MILLION)

- TABLE 81 CANADA: AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2018-2021 (USD MILLION)

- TABLE 82 CANADA: AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2022-2030 (USD MILLION)

- TABLE 83 CANADA: SYSTEMS FOR AUTONOMOUS SHIPS MARKET, BY CATEGORY, 2018-2021 (USD MILLION)

- TABLE 84 CANADA: SYSTEMS FOR AUTONOMOUS SHIPS MARKET, BY CATEGORY, 2022-2030 (USD MILLION)

- TABLE 85 CANADA: SOFTWARE FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 86 CANADA: SOFTWARE FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2022-2030 (USD MILLION)

- TABLE 87 CANADA: AUTONOMOUS SHIPS MARKET, BY END USER, 2018-2021 (USD MILLION)

- TABLE 88 CANADA: AUTONOMOUS SHIPS MARKET, BY END USER, 2022-2030 (USD MILLION)

- 12.3 EUROPE

- 12.3.1 PESTLE ANALYSIS: EUROPE

- FIGURE 45 EUROPE AUTONOMOUS SHIPS MARKET SNAPSHOT

- TABLE 89 EUROPE: AUTONOMOUS SHIPS MARKET, BY COUNTRY, 2018-2021 (USD MILLION)

- TABLE 90 EUROPE: AUTONOMOUS SHIPS MARKET, BY COUNTRY, 2022-2030 (USD MILLION)

- TABLE 91 EUROPE: AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2018-2021 (USD MILLION)

- TABLE 92 EUROPE: AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2022-2030 (USD MILLION)

- TABLE 93 EUROPE: COMMERCIAL AUTONOMOUS SHIPS MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 94 EUROPE: COMMERCIAL AUTONOMOUS SHIPS MARKET, BY TYPE, 2022-2030 (USD MILLION)

- TABLE 95 EUROPE: DEFENSE AUTONOMOUS SHIPS MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 96 EUROPE: DEFENSE AUTONOMOUS SHIPS MARKET, BY TYPE, 2022-2030 (USD MILLION)

- TABLE 97 EUROPE: AUTONOMOUS SHIPS MARKET, BY AUTONOMY, 2018-2021 (USD MILLION)

- TABLE 98 EUROPE: AUTONOMOUS SHIPS MARKET, BY AUTONOMY, 2022-2030 (USD MILLION)

- TABLE 99 EUROPE: AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2018-2021 (USD MILLION)

- TABLE 100 EUROPE: AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2022-2030 (USD MILLION)

- TABLE 101 EUROPE: SYSTEMS FOR AUTONOMOUS SHIPS MARKET, BY CATEGORY, 2018-2021 (USD MILLION)

- TABLE 102 EUROPE: SYSTEMS FOR AUTONOMOUS SHIPS MARKET, BY CATEGORY, 2022-2030 (USD MILLION)

- TABLE 103 EUROPE: INTELLIGENT AWARENESS SYSTEM FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 104 EUROPE: INTELLIGENT AWARENESS SYSTEM FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2022-2030 (USD MILLION)

- TABLE 105 EUROPE: SOFTWARE FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 106 EUROPE: SOFTWARE FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2022-2030 (USD MILLION)

- TABLE 107 EUROPE: AUTONOMOUS SHIPS MARKET, BY END USER, 2018-2021 (USD MILLION)

- TABLE 108 EUROPE: AUTONOMOUS SHIPS MARKET, BY END USER, 2022-2030 (USD MILLION)

- TABLE 109 EUROPE: AUTONOMOUS SHIPS MARKET, BY PROPULSION, 2018-2021 (USD MILLION)

- TABLE 110 EUROPE: AUTONOMOUS SHIPS MARKET, BY PROPULSION, 2022-2030 (USD MILLION)

- 12.3.2 GERMANY

- 12.3.2.1 Upgrading of ship equipment to boost demand for autonomous ship systems

- TABLE 111 GERMANY: AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2018-2021 (USD MILLION)

- TABLE 112 GERMANY: AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2022-2030 (USD MILLION)

- TABLE 113 GERMANY: AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2018-2021 (USD MILLION)

- TABLE 114 GERMANY: AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2022-2030 (USD MILLION)

- TABLE 115 GERMANY: SYSTEMS FOR AUTONOMOUS SHIPS MARKET, BY CATEGORY, 2018-2021 (USD MILLION)

- TABLE 116 GERMANY: SYSTEMS FOR AUTONOMOUS SHIPS MARKET, BY CATEGORY, 2022-2030 (USD MILLION)

- TABLE 117 GERMANY: SOFTWARE FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 118 GERMANY: SOFTWARE FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2022-2030 (USD MILLION)

- TABLE 119 GERMANY: AUTONOMOUS SHIPS MARKET, BY END USER, 2018-2021 (USD MILLION)

- TABLE 120 GERMANY: AUTONOMOUS SHIPS MARKET, BY END USER, 2022-2030 (USD MILLION)

- 12.3.3 DENMARK

- 12.3.3.1 Increasing demand for naval vessels to drive market

- TABLE 121 DENMARK: AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2018-2021 (USD MILLION)

- TABLE 122 DENMARK: AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2022-2030 (USD MILLION)

- TABLE 123 DENMARK: AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2018-2021 (USD MILLION)

- TABLE 124 DENMARK: AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2022-2030 (USD MILLION)

- TABLE 125 DENMARK: SYSTEMS FOR AUTONOMOUS SHIPS MARKET, BY CATEGORY, 2018-2021 (USD MILLION)

- TABLE 126 DENMARK: SYSTEMS FOR AUTONOMOUS SHIPS MARKET, BY CATEGORY, 2022-2030 (USD MILLION)

- TABLE 127 DENMARK: SOFTWARE FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 128 DENMARK: SOFTWARE FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2022-2030 (USD MILLION)

- TABLE 129 DENMARK: AUTONOMOUS SHIPS MARKET, BY END USER, 2018-2021 (USD MILLION)

- TABLE 130 DENMARK: AUTONOMOUS SHIPS MARKET, BY END USER, 2022-2030 (USD MILLION)

- 12.3.4 NORWAY

- 12.3.4.1 Increasing investment by major automation companies in fully autonomous vessels to drive market

- TABLE 131 NORWAY: AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2018-2021 (USD MILLION)

- TABLE 132 NORWAY: AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2022-2030 (USD MILLION)

- TABLE 133 NORWAY: AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2018-2021 (USD MILLION)

- TABLE 134 NORWAY: AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2022-2030 (USD MILLION)

- TABLE 135 NORWAY: SYSTEMS FOR AUTONOMOUS SHIPS MARKET, BY CATEGORY, 2018-2021 (USD MILLION)

- TABLE 136 NORWAY: SYSTEMS FOR AUTONOMOUS SHIPS MARKET, BY CATEGORY, 2022-2030 (USD MILLION)

- TABLE 137 NORWAY: SOFTWARE FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 138 NORWAY: SOFTWARE FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2022-2030 (USD MILLION)

- TABLE 139 NORWAY: AUTONOMOUS SHIPS MARKET, BY END USER, 2018-2021 (USD MILLION)

- TABLE 140 NORWAY: AUTONOMOUS SHIPS MARKET, BY END USER, 2022-2030 (USD MILLION)

- 12.3.5 UK

- 12.3.5.1 Increasing investment to upgrade marine systems to drive market

- TABLE 141 UK: AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2018-2021 (USD MILLION)

- TABLE 142 UK: AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2022-2030 (USD MILLION)

- TABLE 143 UK: AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2018-2021 (USD MILLION)

- TABLE 144 UK: AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2022-2030 (USD MILLION)

- TABLE 145 UK: SYSTEMS FOR AUTONOMOUS SHIPS MARKET, BY CATEGORY, 2018-2021 (USD MILLION)

- TABLE 146 UK: SYSTEMS FOR AUTONOMOUS SHIPS MARKET, BY CATEGORY, 2022-2030 (USD MILLION)

- TABLE 147 UK: SOFTWARE FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 148 UK: SOFTWARE FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2022-2030 (USD MILLION)

- TABLE 149 UK: AUTONOMOUS SHIPS MARKET, BY END USER, 2018-2021 (USD MILLION)

- TABLE 150 UK: AUTONOMOUS SHIPS MARKET, BY END USER, 2022-2030 (USD MILLION)

- 12.3.6 RUSSIA

- 12.3.6.1 Introduction of automation technologies in naval ships to boost demand for automation systems

- TABLE 151 RUSSIA: AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2018-2021 (USD MILLION)

- TABLE 152 RUSSIA: AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2022-2030 (USD MILLION)

- TABLE 153 RUSSIA: AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2018-2021 (USD MILLION)

- TABLE 154 RUSSIA: AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2022-2030 (USD MILLION)

- TABLE 155 RUSSIA: SYSTEMS FOR AUTONOMOUS SHIPS MARKET, BY CATEGORY, 2018-2021 (USD MILLION)

- TABLE 156 RUSSIA: SYSTEMS FOR AUTONOMOUS SHIPS MARKET, BY CATEGORY, 2022-2030 (USD MILLION)

- TABLE 157 RUSSIA: SOFTWARE FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 158 RUSSIA: SOFTWARE FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2022-2030 (USD MILLION)

- TABLE 159 RUSSIA: AUTONOMOUS SHIPS MARKET, BY END USER, 2018-2021 (USD MILLION)

- TABLE 160 RUSSIA: AUTONOMOUS SHIPS MARKET, BY END USER, 2022-2030 (USD MILLION)

- 12.3.7 NETHERLANDS

- 12.3.7.1 Increasing use of autonomous inland vessels to drive market

- TABLE 161 NETHERLANDS: AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2018-2021 (USD MILLION)

- TABLE 162 NETHERLANDS: AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2022-2030 (USD MILLION)

- TABLE 163 NETHERLANDS: AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2018-2021 (USD MILLION)

- TABLE 164 NETHERLANDS: AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2022-2030 (USD MILLION)

- TABLE 165 NETHERLANDS: SYSTEMS FOR AUTONOMOUS SHIPS MARKET, BY CATEGORY, 2018-2021 (USD MILLION)

- TABLE 166 NETHERLANDS: SYSTEMS FOR AUTONOMOUS SHIPS MARKET, BY CATEGORY, 2022-2030 (USD MILLION)

- TABLE 167 NETHERLANDS: SOFTWARE FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 168 NETHERLANDS: SOFTWARE FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2022-2030 (USD MILLION)

- TABLE 169 NETHERLANDS: AUTONOMOUS SHIPS MARKET, BY END USER, 2018-2021 (USD MILLION)

- TABLE 170 NETHERLANDS: AUTONOMOUS SHIPS MARKET, BY END USER, 2022-2030 (USD MILLION)

- 12.3.8 REST OF EUROPE

- 12.3.8.1 Increasing investment in autonomous ship projects to fuel market growth

- TABLE 171 REST OF EUROPE: AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2018-2021 (USD MILLION)

- TABLE 172 REST OF EUROPE: AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2022-2030 (USD MILLION)

- TABLE 173 REST OF EUROPE: AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2018-2021 (USD MILLION)

- TABLE 174 REST OF EUROPE: AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2022-2030 (USD MILLION)

- TABLE 175 REST OF EUROPE: SYSTEMS FOR AUTONOMOUS SHIPS MARKET, BY CATEGORY, 2018-2021 (USD MILLION)

- TABLE 176 REST OF EUROPE: SYSTEMS FOR AUTONOMOUS SHIPS MARKET, BY CATEGORY, 2022-2030 (USD MILLION)

- TABLE 177 REST OF EUROPE: SOFTWARE FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 178 REST OF EUROPE: SOFTWARE FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2022-2030 (USD MILLION)

- TABLE 179 REST OF EUROPE: AUTONOMOUS SHIPS MARKET, BY END USER, 2018-2021 (USD MILLION)

- TABLE 180 REST OF EUROPE: AUTONOMOUS SHIPS MARKET, BY END USER, 2022-2030 (USD MILLION)

- 12.4 ASIA PACIFIC

- 12.4.1 PESTLE ANALYSIS: ASIA PACIFIC

- FIGURE 46 ASIA PACIFIC AUTONOMOUS SHIPS MARKET SNAPSHOT

- TABLE 181 ASIA PACIFIC: AUTONOMOUS SHIPS MARKET, BY COUNTRY, 2018-2021 (USD MILLION)

- TABLE 182 ASIA PACIFIC: AUTONOMOUS SHIPS MARKET, BY COUNTRY, 2022-2030 (USD MILLION)

- TABLE 183 ASIA PACIFIC: AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2018-2021 (USD MILLION)

- TABLE 184 ASIA PACIFIC: AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2022-2030 (USD MILLION)

- TABLE 185 ASIA PACIFIC: COMMERCIAL AUTONOMOUS SHIPS MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 186 ASIA PACIFIC: COMMERCIAL AUTONOMOUS SHIPS MARKET, BY TYPE, 2022-2030 (USD MILLION)

- TABLE 187 ASIA PACIFIC: DEFENSE AUTONOMOUS SHIPS MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 188 ASIA PACIFIC: DEFENSE AUTONOMOUS SHIPS MARKET, BY TYPE, 2022-2030 (USD MILLION)

- TABLE 189 ASIA PACIFIC: AUTONOMOUS SHIPS MARKET, BY AUTONOMY, 2018-2021 (USD MILLION)

- TABLE 190 ASIA PACIFIC: AUTONOMOUS SHIPS MARKET, BY AUTONOMY, 2022-2030 (USD MILLION)

- TABLE 191 ASIA PACIFIC: AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2018-2021 (USD MILLION)

- TABLE 192 ASIA PACIFIC: AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2022-2030 (USD MILLION)

- TABLE 193 ASIA PACIFIC: SYSTEMS FOR AUTONOMOUS SHIPS MARKET, BY CATEGORY, 2018-2021 (USD MILLION)

- TABLE 194 ASIA PACIFIC: SYSTEMS FOR AUTONOMOUS SHIPS MARKET, BY CATEGORY, 2022-2030 (USD MILLION)

- TABLE 195 ASIA PACIFIC: INTELLIGENT AWARENESS SYSTEM FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 196 ASIA PACIFIC: INTELLIGENT AWARENESS SYSTEM FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2022-2030 (USD MILLION)

- TABLE 197 ASIA PACIFIC: SOFTWARE FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 198 ASIA PACIFIC: SOFTWARE FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2022-2030 (USD MILLION)

- TABLE 199 ASIA PACIFIC: AUTONOMOUS SHIPS MARKET, BY END USER, 2018-2021 (USD MILLION)

- TABLE 200 ASIA PACIFIC: AUTONOMOUS SHIPS MARKET, BY END USER, 2022-2030 (USD MILLION)

- TABLE 201 ASIA PACIFIC: AUTONOMOUS SHIPS MARKET, BY PROPULSION, 2018-2021 (USD MILLION)

- TABLE 202 ASIA PACIFIC: AUTONOMOUS SHIPS MARKET, BY PROPULSION, 2022-2030 (USD MILLION)

- 12.4.2 CHINA

- 12.4.2.1 Increase in naval spending and rise in domestic ship production to drive market

- TABLE 203 CHINA: AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2018-2021 (USD MILLION)

- TABLE 204 CHINA: AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2022-2030 (USD MILLION)

- TABLE 205 CHINA: AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2018-2021 (USD MILLION)

- TABLE 206 CHINA: AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2022-2030 (USD MILLION)

- TABLE 207 CHINA: SYSTEMS FOR AUTONOMOUS SHIPS MARKET, BY CATEGORY, 2018-2021 (USD MILLION)

- TABLE 208 CHINA: SYSTEMS FOR AUTONOMOUS SHIPS MARKET, BY CATEGORY, 2022-2030 (USD MILLION)

- TABLE 209 CHINA: SOFTWARE FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 210 CHINA: SOFTWARE FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2022-2030 (USD MILLION)

- TABLE 211 CHINA: AUTONOMOUS SHIPS MARKET, BY END USER, 2018-2021 (USD MILLION)

- TABLE 212 CHINA: AUTONOMOUS SHIPS MARKET, BY END USER, 2022-2030 (USD MILLION)

- 12.4.3 INDIA

- 12.4.3.1 Upgrading of old ships with new systems to drive market

- TABLE 213 INDIA: AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2018-2021 (USD MILLION)

- TABLE 214 INDIA: AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2022-2030 (USD MILLION)

- TABLE 215 INDIA: AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2018-2021 (USD MILLION)

- TABLE 216 INDIA: AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2022-2030 (USD MILLION)

- TABLE 217 INDIA: SYSTEMS FOR AUTONOMOUS SHIPS MARKET, BY CATEGORY, 2018-2021 (USD MILLION)

- TABLE 218 INDIA: SYSTEMS FOR AUTONOMOUS SHIPS MARKET, BY CATEGORY, 2022-2030 (USD MILLION)

- TABLE 219 INDIA: SOFTWARE FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 220 INDIA: SOFTWARE FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2022-2030 (USD MILLION)

- TABLE 221 INDIA: AUTONOMOUS SHIPS MARKET, BY END USER, 2018-2021 (USD MILLION)

- TABLE 222 INDIA: AUTONOMOUS SHIPS MARKET, BY END USER, 2022-2030 (USD MILLION)

- 12.4.4 JAPAN

- 12.4.4.1 Increasing delivery of commercial ships to fuel market growth

- TABLE 223 JAPAN: AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2018-2021 (USD MILLION)

- TABLE 224 JAPAN: AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2022-2030 (USD MILLION)

- TABLE 225 JAPAN: AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2018-2021 (USD MILLION)

- TABLE 226 JAPAN: AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2022-2030 (USD MILLION)

- TABLE 227 JAPAN: SYSTEMS FOR AUTONOMOUS SHIPS MARKET, BY CATEGORY, 2018-2021 (USD MILLION)

- TABLE 228 JAPAN: SYSTEMS FOR AUTONOMOUS SHIPS MARKET, BY CATEGORY, 2022-2030 (USD MILLION)

- TABLE 229 JAPAN: SOFTWARE FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 230 JAPAN: SOFTWARE FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2022-2030 (USD MILLION)

- TABLE 231 JAPAN: AUTONOMOUS SHIPS MARKET, BY END USER, 2018-2021 (USD MILLION)

- TABLE 232 JAPAN: AUTONOMOUS SHIPS MARKET, BY END USER, 2022-2030 (USD MILLION)

- 12.4.5 SINGAPORE

- 12.4.5.1 Retrofitting of autonomous technologies in vessels to drive market

- TABLE 233 SINGAPORE: AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2018-2021 (USD MILLION)

- TABLE 234 SINGAPORE: AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2022-2030 (USD MILLION)

- TABLE 235 SINGAPORE: AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2018-2021 (USD MILLION)

- TABLE 236 SINGAPORE: AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2022-2030 (USD MILLION)

- TABLE 237 SINGAPORE: SYSTEMS FOR AUTONOMOUS SHIPS MARKET, BY CATEGORY, 2018-2021 (USD MILLION)

- TABLE 238 SINGAPORE: SYSTEMS FOR AUTONOMOUS SHIPS MARKET, BY CATEGORY, 2022-2030 (USD MILLION)

- TABLE 239 SINGAPORE: SOFTWARE FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 240 SINGAPORE: SOFTWARE FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2022-2030 (USD MILLION)

- TABLE 241 SINGAPORE: AUTONOMOUS SHIPS MARKET, BY END USER, 2018-2021 (USD MILLION)

- TABLE 242 SINGAPORE: AUTONOMOUS SHIPS MARKET, BY END USER, 2022-2030 (USD MILLION)

- 12.4.6 SOUTH KOREA

- 12.4.6.1 Integration of automated ship systems by various shipbuilding players to drive market

- TABLE 243 SOUTH KOREA: AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2018-2021 (USD MILLION)

- TABLE 244 SOUTH KOREA: AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2022-2030 (USD MILLION)

- TABLE 245 SOUTH KOREA: AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2018-2021 (USD MILLION)

- TABLE 246 SOUTH KOREA: AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2022-2030 (USD MILLION)

- TABLE 247 SOUTH KOREA: SYSTEMS FOR AUTONOMOUS SHIPS MARKET, BY CATEGORY, 2018-2021 (USD MILLION)

- TABLE 248 SOUTH KOREA: SYSTEMS FOR AUTONOMOUS SHIPS MARKET, BY CATEGORY, 2022-2030 (USD MILLION)

- TABLE 249 SOUTH KOREA: SOFTWARE FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 250 SOUTH KOREA: SOFTWARE FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2022-2030 (USD MILLION)

- TABLE 251 SOUTH KOREA: AUTONOMOUS SHIPS MARKET, BY END USER, 2018-2021 (USD MILLION)

- TABLE 252 SOUTH KOREA: AUTONOMOUS SHIPS MARKET, BY END USER, 2022-2030 (USD MILLION)

- 12.4.7 MALAYSIA

- 12.4.7.1 Increasing use of autonomous systems in offshore vessels to drive market

- TABLE 253 MALAYSIA: AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2018-2021 (USD MILLION)

- TABLE 254 MALAYSIA: AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2022-2030 (USD MILLION)

- TABLE 255 MALAYSIA: AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2018-2021 (USD MILLION)

- TABLE 256 MALAYSIA: AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2022-2030 (USD MILLION)

- TABLE 257 MALAYSIA: SYSTEMS FOR AUTONOMOUS SHIPS MARKET, BY CATEGORY, 2018-2021 (USD MILLION)

- TABLE 258 MALAYSIA: SYSTEMS FOR AUTONOMOUS SHIPS MARKET, BY CATEGORY, 2022-2030 (USD MILLION)

- TABLE 259 MALAYSIA: SOFTWARE FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 260 MALAYSIA: SOFTWARE FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2022-2030 (USD MILLION)

- TABLE 261 MALAYSIA: AUTONOMOUS SHIPS MARKET, BY END USER, 2018-2021 (USD MILLION)

- TABLE 262 MALAYSIA: AUTONOMOUS SHIPS MARKET, BY END USER, 2022-2030 (USD MILLION)

- 12.4.8 REST OF ASIA PACIFIC

- 12.4.8.1 Focus on enhancing coastal security to drive market

- TABLE 263 REST OF ASIA PACIFIC: AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2018-2021 (USD MILLION)

- TABLE 264 REST OF ASIA PACIFIC: AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2022-2030 (USD MILLION)

- TABLE 265 REST OF ASIA PACIFIC: AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2018-2021 (USD MILLION)

- TABLE 266 REST OF ASIA PACIFIC: AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2022-2030 (USD MILLION)

- TABLE 267 REST OF ASIA PACIFIC: SYSTEMS FOR AUTONOMOUS SHIPS MARKET, BY CATEGORY, 2018-2021 (USD MILLION)

- TABLE 268 REST OF ASIA PACIFIC: SYSTEMS FOR AUTONOMOUS SHIPS MARKET, BY CATEGORY, 2022-2030 (USD MILLION)

- TABLE 269 REST OF ASIA PACIFIC: SOFTWARE FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 270 REST OF ASIA PACIFIC: SOFTWARE FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2022-2030 (USD MILLION)

- TABLE 271 REST OF ASIA PACIFIC: AUTONOMOUS SHIPS MARKET, BY END USER, 2018-2021 (USD MILLION)

- TABLE 272 REST OF ASIA PACIFIC: AUTONOMOUS SHIPS MARKET, BY END USER, 2022-2030 (USD MILLION)

- 12.5 REST OF THE WORLD

- 12.5.1 PESTLE ANALYSIS: REST OF THE WORLD

- FIGURE 47 REST OF THE WORLD: AUTONOMOUS SHIPS MARKET SNAPSHOT

- TABLE 273 REST OF THE WORLD: AUTONOMOUS SHIPS MARKET, BY REGION, 2018-2021 (USD MILLION)

- TABLE 274 REST OF THE WORLD: AUTONOMOUS SHIPS MARKET, BY REGION, 2022-2030 (USD MILLION)

- TABLE 275 REST OF THE WORLD: AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2018-2021 (USD MILLION)

- TABLE 276 REST OF THE WORLD: AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2022-2030 (USD MILLION)

- TABLE 277 REST OF THE WORLD: COMMERCIAL AUTONOMOUS SHIPS MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 278 REST OF THE WORLD: COMMERCIAL AUTONOMOUS SHIPS MARKET, BY TYPE, 2022-2030 (USD MILLION)

- TABLE 279 REST OF THE WORLD: DEFENSE AUTONOMOUS SHIPS MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 280 REST OF THE WORLD: DEFENSE AUTONOMOUS SHIPS MARKET, BY TYPE, 2022-2030 (USD MILLION)

- TABLE 281 REST OF THE WORLD: AUTONOMOUS SHIPS MARKET, BY AUTONOMY, 2018-2021 (USD MILLION)

- TABLE 282 REST OF THE WORLD: AUTONOMOUS SHIPS MARKET, BY AUTONOMY, 2022-2030 (USD MILLION)

- TABLE 283 REST OF THE WORLD: AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2018-2021 (USD MILLION)

- TABLE 284 REST OF THE WORLD: AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2022-2030 (USD MILLION)

- TABLE 285 REST OF THE WORLD: SYSTEMS FOR AUTONOMOUS SHIPS MARKET, BY CATEGORY, 2018-2021 (USD MILLION)

- TABLE 286 REST OF THE WORLD: SYSTEMS FOR AUTONOMOUS SHIPS MARKET, BY CATEGORY, 2022-2030 (USD MILLION)

- TABLE 287 REST OF THE WORLD: INTELLIGENT AWARENESS SYSTEM FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 288 REST OF THE WORLD: INTELLIGENT AWARENESS SYSTEM FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2022-2030 (USD MILLION)

- TABLE 289 REST OF THE WORLD: SOFTWARE FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 290 REST OF THE WORLD: SOFTWARE FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2022-2030 (USD MILLION)

- TABLE 291 REST OF THE WORLD: AUTONOMOUS SHIPS MARKET, BY END USER, 2018-2021 (USD MILLION)

- TABLE 292 REST OF THE WORLD: AUTONOMOUS SHIPS MARKET, BY END USER, 2022-2030 (USD MILLION)

- TABLE 293 REST OF THE WORLD: AUTONOMOUS SHIPS MARKET, BY PROPULSION, 2018-2021 (USD MILLION)

- TABLE 294 REST OF THE WORLD: AUTONOMOUS SHIPS MARKET, BY PROPULSION, 2022-2030 (USD MILLION)

- 12.5.2 MIDDLE EAST & AFRICA

- 12.5.2.1 Increasing development of autonomous vessels to fuel market growth

- TABLE 295 MIDDLE EAST & AFRICA: AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2018-2021 (USD MILLION)

- TABLE 296 MIDDLE EAST & AFRICA: AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2022-2030 (USD MILLION)

- TABLE 297 MIDDLE EAST & AFRICA: AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2018-2021 (USD MILLION)

- TABLE 298 MIDDLE EAST & AFRICA: AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2022-2030 (USD MILLION)

- TABLE 299 MIDDLE EAST & AFRICA: SYSTEMS FOR AUTONOMOUS SHIPS MARKET, BY CATEGORY, 2018-2021 (USD MILLION)

- TABLE 300 MIDDLE EAST & AFRICA: SYSTEMS FOR AUTONOMOUS SHIPS MARKET, BY CATEGORY, 2022-2030 (USD MILLION)

- TABLE 301 MIDDLE EAST & AFRICA: SOFTWARE FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 302 MIDDLE EAST & AFRICA: SOFTWARE FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2022-2030 (USD MILLION)

- TABLE 303 MIDDLE EAST & AFRICA: AUTONOMOUS SHIPS MARKET, BY END USER, 2018-2021 (USD MILLION)

- TABLE 304 MIDDLE EAST & AFRICA: AUTONOMOUS SHIPS MARKET, BY END USER, 2022-2030 (USD MILLION)

- 12.5.3 LATIN AMERICA

- 12.5.3.1 Rise in maritime trade and ship overhauling to drive demand for autonomous ships

- TABLE 305 LATIN AMERICA: AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2018-2021 (USD MILLION)

- TABLE 306 LATIN AMERICA: AUTONOMOUS SHIPS MARKET, BY SHIP TYPE, 2022-2030 (USD MILLION)

- TABLE 307 LATIN AMERICA: AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2018-2021 (USD MILLION)

- TABLE 308 LATIN AMERICA: AUTONOMOUS SHIPS MARKET, BY SOLUTION, 2022-2030 (USD MILLION)

- TABLE 309 LATIN AMERICA: SYSTEMS FOR AUTONOMOUS SHIPS MARKET, BY CATEGORY, 2018-2021 (USD MILLION)

- TABLE 310 LATIN AMERICA: SYSTEMS FOR AUTONOMOUS SHIPS MARKET, BY CATEGORY, 2022-2030 (USD MILLION)

- TABLE 311 LATIN AMERICA: SOFTWARE FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 312 LATIN AMERICA: SOFTWARE FOR AUTONOMOUS SHIPS MARKET, BY TYPE, 2022-2030 (USD MILLION)

- TABLE 313 LATIN AMERICA: AUTONOMOUS SHIPS MARKET, BY END USER, 2018-2021 (USD MILLION)

- TABLE 314 LATIN AMERICA: AUTONOMOUS SHIPS MARKET, BY END USER, 2022-2030 (USD MILLION)

13 COMPETITIVE LANDSCAPE

- 13.1 INTRODUCTION

- 13.2 KEY PLAYERS' STRATEGIES

- 13.3 MARKET SHARE ANALYSIS OF LEADING PLAYERS, 2021

- TABLE 315 DEGREE OF COMPETITION

- FIGURE 48 REVENUE GENERATED BY MAJOR PLAYERS IN AUTONOMOUS SHIPS MARKET, 2021

- 13.4 REVENUE SHARE ANALYSIS OF TOP 5 PLAYERS (2019-2021)

- FIGURE 49 COLLECTIVE REVENUE SHARE OF TOP 5 PLAYERS (2019-2021)

- 13.5 RANK ANALYSIS, 2021

- FIGURE 50 REVENUE SHARE OF TOP 5 PLAYERS IN AUTONOMOUS SHIPS MARKET IN 2021

- TABLE 316 COMPANY REGION FOOTPRINT

- TABLE 317 COMPANY SHIP TYPE FOOTPRINT

- TABLE 318 COMPANY AUTONOMY FOOTPRINT

- 13.6 COMPETITIVE EVALUATION QUADRANT

- 13.6.1 STARS

- 13.6.2 PERVASIVE COMPANIES

- 13.6.3 EMERGING LEADERS

- 13.6.4 PARTICIPANTS

- FIGURE 51 AUTONOMOUS SHIPS MARKET COMPETITIVE LEADERSHIP MAPPING, 2021

- 13.7 COMPETITIVE BENCHMARKING

- FIGURE 52 AUTONOMOUS SHIPS MARKET COMPETITIVE LEADERSHIP MAPPING (SME)

- 13.7.1 PROGRESSIVE COMPANIES

- 13.7.2 RESPONSIVE COMPANIES

- 13.7.3 STARTING BLOCKS

- 13.7.4 DYNAMIC COMPANIES

- 13.8 DETAILED LIST AND COMPETITIVE BENCHMARKING OF KEY START-UPS/SMES

- TABLE 319 AUTONOMOUS SHIPS MARKET: DETAILED LIST OF KEY START-UPS/SMES

- TABLE 320 AUTONOMOUS SHIPS MARKET: COMPETITIVE BENCHMARKING OF KEY START-UPS/SMES

- 13.9 COMPETITIVE SCENARIO

- 13.9.1 NEW PRODUCT LAUNCHES

- TABLE 321 NEW PRODUCT DEVELOPMENT, JANUARY 2019-AUGUST 2022

- 13.9.2 DEALS

- TABLE 322 DEALS, JANUARY 2019-AUGUST 2022

14 COMPANY PROFILES

- 14.1 INTRODUCTION

- 14.2 KEY PLAYERS

- (Business overview, Products offered, Recent developments, Deals, New product developments, MnM view, Key strengths, Strategic choices made, and Weaknesses and competitive threats)**

- 14.2.1 KONGSBERG MARITIME

- TABLE 323 KONGSBERG MARITIME: BUSINESS OVERVIEW

- FIGURE 53 KONGSBERG MARITIME: COMPANY SNAPSHOT

- 14.2.2 ABB

- TABLE 324 ABB: BUSINESS OVERVIEW

- FIGURE 54 ABB: COMPANY SNAPSHOT

- 14.2.3 ROLLS-ROYCE PLC

- TABLE 325 ROLLS-ROYCE PLC: BUSINESS OVERVIEW

- FIGURE 55 ROLLS-ROYCE PLC: COMPANY SNAPSHOT

- 14.2.4 HYUNDAI HEAVY INDUSTRIES

- TABLE 326 HYUNDAI HEAVY INDUSTRIES: BUSINESS OVERVIEW

- FIGURE 56 HYUNDAI HEAVY INDUSTRIES: COMPANY SNAPSHOT

- 14.2.5 FUGRO

- TABLE 327 FUGRO: BUSINESS OVERVIEW

- FIGURE 57 FUGRO: COMPANY SNAPSHOT

- 14.2.6 WARTSILA

- TABLE 328 WARTSILA: BUSINESS OVERVIEW

- FIGURE 58 WARTSILA: COMPANY SNAPSHOT

- 14.2.7 HONEYWELL INTERNATIONAL INC.

- TABLE 329 HONEYWELL INTERNATIONAL INC.: BUSINESS OVERVIEW

- FIGURE 59 HONEYWELL INTERNATIONAL INC.: COMPANY SNAPSHOT

- 14.2.8 SIEMENS

- TABLE 330 SIEMENS: BUSINESS OVERVIEW

- FIGURE 60 SIEMENS: COMPANY SNAPSHOT

- 14.2.9 GENERAL ELECTRIC

- TABLE 331 GENERAL ELECTRIC: BUSINESS OVERVIEW

- FIGURE 61 GENERAL ELECTRIC: COMPANY SNAPSHOT

- 14.2.10 L3HARRIS ASV

- TABLE 332 L3HARRIS ASV: BUSINESS OVERVIEW

- FIGURE 62 L3HARRIS TECHNOLOGIES INC. (PARENT ORGANIZATION OF L3HARRIS ASV): COMPANY SNAPSHOT

- 14.2.11 NORTHROP GRUMMAN CORPORATION

- TABLE 333 NORTHROP GRUMMAN CORPORATION: BUSINESS OVERVIEW

- FIGURE 63 NORTHROP GRUMMAN CORPORATION: COMPANY SNAPSHOT

- 14.2.12 MITSUI E&S HOLDINGS CO., LTD.

- TABLE 334 MITSUI E&S HOLDINGS CO., LTD.: BUSINESS OVERVIEW

- FIGURE 64 MITSUI E&S HOLDINGS CO., LTD.: COMPANY SNAPSHOT

- 14.2.13 VALMET

- TABLE 335 VALMET: BUSINESS OVERVIEW

- FIGURE 65 VALMET: COMPANY SNAPSHOT

- 14.2.14 ASELSAN A.S.

- TABLE 336 ASELSAN A.S.: BUSINESS OVERVIEW

- FIGURE 66 ASELSAN A.S.: COMPANY SNAPSHOT

- 14.2.15 BAE SYSTEMS

- TABLE 337 BAE SYSTEMS: BUSINESS OVERVIEW

- FIGURE 67 BAE SYSTEMS: COMPANY SNAPSHOT

- 14.2.16 SAMSUNG HEAVY INDUSTRIES CO., LTD.

- TABLE 338 SAMSUNG HEAVY INDUSTRIES CO., LTD.: BUSINESS OVERVIEW

- FIGURE 68 SAMSUNG HEAVY INDUSTRIES CO., LTD.: COMPANY SNAPSHOT

- 14.2.17 MARINE TECHNOLOGIES LLC

- TABLE 339 MARINE TECHNOLOGIES LLC: BUSINESS OVERVIEW

- 14.2.18 PRAXIS AUTOMATION TECHNOLOGY B.V.

- TABLE 340 PRAXIS AUTOMATION TECHNOLOGY B.V.: BUSINESS OVERVIEW

- 14.2.19 DNV GL

- TABLE 341 DNV GL: BUSINESS OVERVIEW

- 14.2.20 ULSTEIN

- TABLE 342 ULSTEIN: BUSINESS OVERVIEW

- 14.2.21 VIGOR INDUSTRIAL LLC

- TABLE 343 VIGOR INDUSTRIAL LLC: BUSINESS OVERVIEW

- 14.3 OTHER PLAYERS

- 14.3.1 RH MARINE

- TABLE 344 RH MARINE: BUSINESS OVERVIEW

- 14.3.2 MARLINK

- TABLE 345 MARLINK: BUSINESS OVERVIEW

- 14.3.3 SEA MACHINES ROBOTICS, INC.

- TABLE 346 SEA MACHINES ROBOTICS, INC.: BUSINESS OVERVIEW

- 14.3.4 SHONE AUTOMATION, INC.

- TABLE 347 SHONE AUTOMATION, INC.: BUSINESS OVERVIEW

- 14.3.5 ORCA AI

- TABLE 348 ORCA AI: BUSINESS OVERVIEW

- 14.3.6 BUFFALO AUTOMATION

- TABLE 349 BUFFALO AUTOMATION: BUSINESS OVERVIEW

- 14.3.7 LADAR LTD.

- TABLE 350 LADAR LTD.: BUSINESS OVERVIEW

- *Details on Business overview, Products offered, Recent developments, Deals, New product developments, MnM view, Key strengths, Strategic choices made, and Weaknesses and competitive threats might not be captured in case of unlisted companies.

15 APPENDIX

- 15.1 DISCUSSION GUIDE

- 15.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 15.3 CUSTOMIZATION OPTIONS

- 15.4 RELATED REPORTS

- 15.5 AUTHOR DETAILS