|

|

市場調査レポート

商品コード

1069667

電池用コーティングの世界市場 - 2027年までの予測:電池コンポーネント別 (電極用コーティング、セパレーター用コーティング、電池パック用コーティング) 、材料の種類別 (PVDF、セラミック、アルミナ、酸化物、炭素) 、地域別Battery Coating Market by Battery Component (Electrode Coating, Separator Coating, Battery Pack Coating), Material Type (PVDF, Ceramic, Alumina, Oxide, Carbon), and Region (Asia Pacific, North America, Europe, ROW) - Global Forecast to 2027 |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| 電池用コーティングの世界市場 - 2027年までの予測:電池コンポーネント別 (電極用コーティング、セパレーター用コーティング、電池パック用コーティング) 、材料の種類別 (PVDF、セラミック、アルミナ、酸化物、炭素) 、地域別 |

|

出版日: 2022年04月07日

発行: MarketsandMarkets

ページ情報: 英文 256 Pages

納期: 即納可能

|

- 全表示

- 概要

- 目次

世界の電池用コーティングの市場規模は、2022年の3億2,900万米ドルから、2027年までに6億5,800万米ドルに達し、2022年~2027年のCAGRで14.9%の成長が予測されています。

EV、HEV、PHEVの生産台数の多さや、スマートデバイスやその他のコンシューマーエレクトロニクスに対する需要の拡大が、電池用コーティング市場を牽引すると予想されます。ただし、コーティング技術の高コストが、市場の成長を抑制する要因となっています。

当レポートでは、世界の電池用コーティング市場について調査分析し、市場概要、業界動向、セグメント別の市場分析、競合情勢、主要企業などについて、最新の情報を提供しています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- ポーターのファイブフォース分析

第6章 業界動向

- バリューチェーン分析

- 電池用コーティング市場のエコシステム

- 顧客のビジネスに影響を与える動向と混乱

- ケーススタディ分析

- 特許分析

- 主要な会議とイベント

- 平均販売価格分析

- 規制情勢

- COVID-19の影響分析

第7章 電池用コーティング市場:技術タイプ別

- 原子層堆積 (ALD)

- プラズマCVD (PECVD)

- 化学蒸着 (CVD)

- 乾式粉体塗装

- 物理蒸着 (PVD)

第8章 電池用コーティング市場:電池コンポーネント別

- 電極用コーティング

- セパレーター用コーティング

- 電池パック用コーティング

第9章 電池用コーティング市場:電池の種類別

- リチウムイオン電池

- 鉛蓄電池

- ニッケルカドミウム電池

- グラフェン電池

第10章 電池用コーティング市場:材料の種類別

- ポリフッ化ビニリデン (PVDF)

- セラミック

- アルミナ

- 酸化物

- 炭素

- ポリウレタン (PU)

- エポキシ

- その他

第11章 地域分析

- アジア太平洋地域

- 中国

- 韓国

- 日本

- インド

- その他のアジア太平洋地域

- 欧州

- ドイツ

- フランス

- 英国

- その他の欧州

- 北米

- 米国

- その他の北米

- その他の地域

第12章 競合情勢

- 概要

- 主要企業の戦略

- 収益分析

- 市場シェア分析:電池用コーティング

- 競合情勢マッピング

- 競合ベンチマーキング

- 中小企業のマトリックス

- 主要な市場発展

第13章 企業プロファイル

- SOLVAY SA

- ARKEMA SA

- PPG INDUSTRIES, INC.

- ASAHI KASEI CORPORATION

- MITSUBISHI PAPER MILLS LTD.

- UBE INDUSTRIES LTD.

- TANAKA CHEMICAL CORPORATION

- SK INNOVATION CO., LTD.

- DURR GROUP

- ASHLAND GLOBAL HOLDINGS INC.

- AXALTA COATING SYSTEMS, LTD.

- APV ENGINEERED COATINGS

- SAMCO INC.

- UNIFRAX

- TARGRAY TECHNOLOGY INTERNATIONAL INC.

- その他の企業

- NEI CORPORATION

- ALTEO

- NEXEON LIMITED

- NANO ONE MATERIALS CORP.

- BENEQ

- FORGE NANO INC.

- XIAMEN ACEY NEW ENERGY TECHNOLOGY CO., LTD.

- SHANDONG HENGYI NEW MATERIAL TECHNOLOGY CO., LTD

- GUJARAT FLUOROCHEMICALS LIMITED

- PULRON

- WRIGHT COATING TECHNOLOGIES

- ALCOLOR

- AKZO NOBEL N.V.

第14章 付録

The battery coating market is projected to grow from USD 329 million in 2022 to USD 658 million by 2027, at a CAGR of 14.9% from 2022 to 2027. The high production of EVs, HEVs, and PHEVs and the growing demand for smart devices and other consumer electronics are expected to drive the battery coating market. High coating technology costs, however, act as a restraint for the growth of this market.

"The electrode coating in component type segment is projected to register the highest CAGR during the forecast period."

Based on battery component, the electrode coating is projected to register the highest CAGR during the forecast period. This projected growth is attributed to the increase in demand for electrode coating in lithium-ion batteries for high performance and safety of the batteries. There is an increase in demand for more sustainable batteries, especially in EVs, smart devices, and energy storage systems. This demand will, in return, drive the growth of the electrode coating segment of the battery coating market.

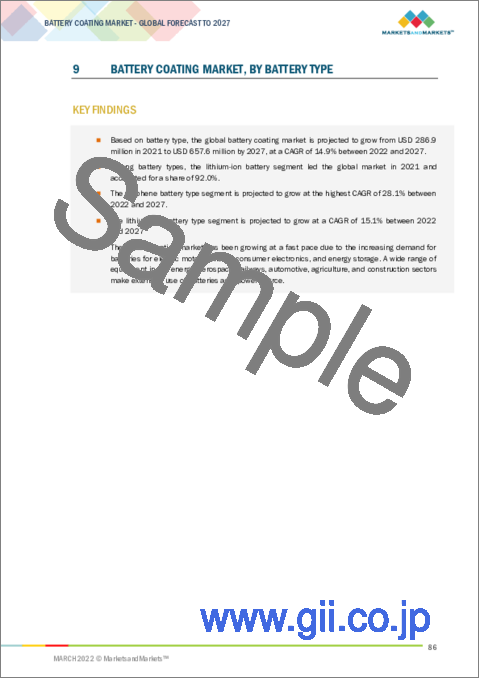

"The graphene battery in battery type segment is projected to register the highest CAGR during the forecast period."

Based on battery type, the graphene battery is projected to register the highest CAGR during the forecast period. A graphene battery is light, durable, and suitable for high-capacity energy storage, as well as shorter charging times. The battery life is negatively linked to the amount of carbon that is coated on the material or added to electrodes to achieve conductivity. However, graphene adds conductivity without the requirement of the amount of carbon which is used in conventional batteries.

"The alumina in material type segment is projected to register the highest CAGR during the forecast period."

Based on material type, the alumina is projected to grow at the highest rate during the forecast period. Continuous innovation and technological advances in battery materials will lead to the rapid adoption of electrode and separator coatings in the battery material industry. This rapid adoption, in turn, provides an opportunity for the alumina material type segment to grow.

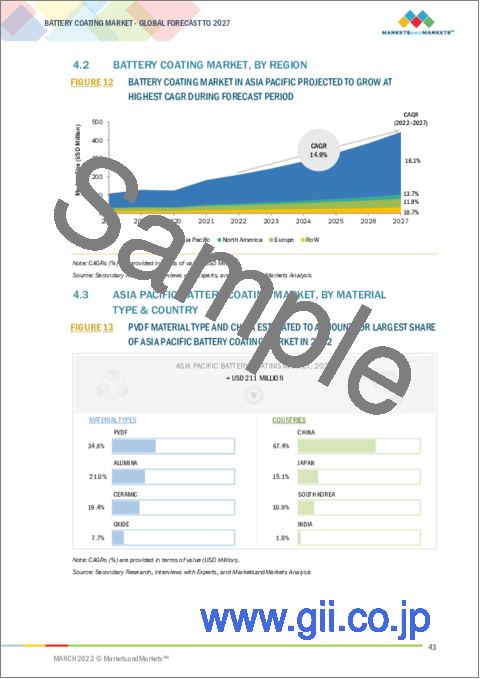

The battery coating market in Asia Pacific is projected to witness the highest CAGR during the forecast period."

Asia Pacific region is projected to register the highest CAGR in the battery coating market from 2022 to 2027. In recent years, the region has emerged as a hub for automobile production. Recent infrastructural developments and industrialization activities in the emerging nations of this region have opened new avenues and opportunities for OEMs. The presence of leading li-ion battery manufacturing companies such as Samsung (South Korea), LG (South Korea), BYD (China), Panasonic (Japan), and Sony (Japan) is also driving the demand for battery coatings in the Asia Pacific region.

Profile break-up of primary participants for the report:

- By Company Type: Tier 1 - 40%, Tier 2 - 20%, and Tier 3 - 40%

- By Designation: C-level Executives - 10%, Directors - 70%, and Others - 20%

- By Region: Asia Pacific - 25%, North America - 20%, Europe - 45% and Rest of the World - 10%

The battery coating report is dominated by players, such as Solvay SA (Belgium), Arkema SA (France), PPG Industries, Inc. (US), Asahi Kasei Corporation (Japan), Mitsubishi Paper Mills Ltd (Japan), Ube Industries Ltd. (Japan), Tanaka Chemical Corporation (Japan), SK Innovation Co., Ltd (South Korea), Durr Group (Germany), Ashland Global Holdings Inc (US), Axalta Coating Systems Ltd (US), APV Engineered Coatings (US), Samco Inc (Japan), Unifrax (US), and Targray Technology International Inc (US)

Research Coverage:

The report defines, segments, and projects the size of the battery coating market based on battery component, material type, and region. It strategically profiles the key players and comprehensively analyzes their market share and core competencies. It also tracks and analyzes competitive developments, such as expansions, product developments, investments, agreements, and partnerships, undertaken by them in the market.

Reasons to Buy the Report:

The report is expected to help the market leaders/new entrants in the market by providing them the closest approximations of revenue numbers of the battery coating market and its segments. This report is also expected to help stakeholders obtain an improved understanding of the competitive landscape of the market, gain insights to improve the position of their businesses and make suitable go-to-market strategies. It also enables stakeholders to understand the pulse of the market and provide them information on key market drivers, restraints, challenges, and opportunities.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 OBJECTIVES OF THE STUDY

- 1.2 MARKET DEFINITION

- 1.3 INCLUSIONS & EXCLUSIONS

- TABLE 1 BATTERY COATING MARKET, BY BATTERY COMPONENT: INCLUSIONS & EXCLUSIONS

- TABLE 2 BATTERY COATING MARKET, BY BATTERY TYPE: INCLUSIONS & EXCLUSIONS

- TABLE 3 BATTERY COATING MARKET, BY MATERIAL TYPE: INCLUSIONS & EXCLUSIONS

- TABLE 4 BATTERY COATING MARKET, BY REGION: INCLUSIONS & EXCLUSIONS

- 1.3.1 MARKETS COVERED

- FIGURE 1 BATTERY COATING MARKET SEGMENTATION

- FIGURE 2 BATTERY COATING MARKET: REGIONS COVERED

- 1.3.2 YEARS CONSIDERED FOR THE REPORT

- 1.4 CURRENCY

- 1.5 PACKAGE SIZE

- 1.6 LIMITATIONS

- 1.7 STAKEHOLDERS

- 1.8 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 3 BATTERY COATING MARKET: RESEARCH DESIGN

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 List of participating companies for primary research

- 2.1.2.3 Key industry insights

- 2.1.2.4 Breakdown of primary interviews

- 2.2 MARKET SIZE ESTIMATION

- 2.3 BASE NUMBER CALCULATION

- 2.3.1 DEMAND SIDE APPROACH

- 2.3.2 MARKET ENGINEERING PROCESS

- 2.3.3 BOTTOM-UP APPROACH

- FIGURE 4 MARKET SIZE ESTIMATION: BOTTOM-UP APPROACH

- 2.3.4 TOP-DOWN APPROACH

- FIGURE 5 MARKET SIZE ESTIMATION: TOP-DOWN APPROACH

- 2.4 MARKET BREAKDOWN AND DATA TRIANGULATION

- FIGURE 6 MARKET BREAKDOWN AND DATA TRIANGULATION

- 2.5 ASSUMPTIONS

- 2.6 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

- TABLE 5 BATTERY COATING MARKET SNAPSHOT, 2022 AND 2027

- FIGURE 7 ELECTRODE COATING SEGMENT ACCOUNTED FOR LARGEST SHARE OF BATTERY COATING COMPONENT MARKET IN 2021

- FIGURE 8 LITHIUM-ION BATTERY SEGMENT ACCOUNTED FOR LARGEST SHARE OF BATTERY TYPE COATING MARKET IN 2021

- FIGURE 9 PVDF SEGMENT ACCOUNTED FOR LARGEST SHARE OF BATTERY COATING MATERIAL MARKET IN 2021

- FIGURE 10 ASIA PACIFIC ACCOUNTED FOR LARGEST SHARE OF BATTERY COATING MARKET IN 2021

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES IN BATTERY COATING MARKET

- FIGURE 11 HIGH PRODUCTION OF HEVS, PHEVS, AND EVS EXPECTED TO DRIVE BATTERY COATING MARKET FROM 2022 TO 2027

- 4.2 BATTERY COATING MARKET, BY REGION

- FIGURE 12 BATTERY COATING MARKET IN ASIA PACIFIC PROJECTED TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- 4.3 ASIA PACIFIC BATTERY COATING MARKET, BY MATERIAL TYPE & COUNTRY

- FIGURE 13 PVDF MATERIAL TYPE AND CHINA ESTIMATED TO ACCOUNT FOR LARGEST SHARE OF ASIA PACIFIC BATTERY COATING MARKET IN 2022

- 4.4 BATTERY COATING MARKET, BY MAJOR COUNTRIES

- FIGURE 14 BATTERY COATING MARKET IN CHINA PROJECTED TO GROW AT HIGHEST CAGR FROM 2022 TO 2027

5 MARKET OVERVIEW

- 5.1 MARKET DYNAMICS

- FIGURE 15 BATTERY COATING MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- 5.1.1 DRIVERS

- 5.1.1.1 High production of EVs, HEVs, and PHEVs

- FIGURE 16 GLOBAL SALES OF BEVS AND PHEVS-2012-2021

- FIGURE 17 ELECTRIC VEHICLE STOCK IN EV30@30 SCENARIO, 2018-2030

- 5.1.1.2 Rising demand for smart devices and other consumer electronics

- FIGURE 18 GLOBAL CONSUMER ELECTRONICS REVENUE

- 5.1.2 RESTRAINTS

- 5.1.2.1 High cost of technology

- 5.1.2.2 Safety and environmental concerns due to use of hazardous metals

- 5.1.3 OPPORTUNITIES

- 5.1.3.1 Innovations and technological advances in battery materials

- 5.1.3.2 Lithium-ion batteries in energy storage devices

- FIGURE 19 INSTALLED CAPACITY OF UTILITY-SCALE BATTERY STORAGE SYSTEMS IN NEW POLICIES SCENARIO, 2020-2040

- 5.1.4 CHALLENGES

- 5.1.4.1 Expected utilization of solid electrolytes

- 5.2 PORTER'S FIVE FORCES ANALYSIS

- FIGURE 20 PORTER'S FIVE FORCES ANALYSIS

- TABLE 6 BATTERY COATING MARKET: PORTER'S FIVE FORCES ANALYSIS

- 5.2.1 THREAT OF NEW ENTRANTS

- 5.2.2 THREAT OF SUBSTITUTES

- 5.2.3 BARGAINING POWER OF BUYERS

- 5.2.4 BARGAINING POWER OF SUPPLIERS

- 5.2.5 INTENSITY OF COMPETITIVE RIVALRY

6 INDUSTRY TRENDS

- 6.1 VALUE CHAIN ANALYSIS

- FIGURE 21 VALUE CHAIN ANALYSIS: HIGHEST VALUE ADDED DURING COATING PHASE

- 6.2 ECOSYSTEM FOR BATTERY COATING MARKET

- FIGURE 22 ECOSYSTEM MAP OF BATTERY COATING MARKET

- TABLE 7 BATTERY COATING MARKET: ECOSYSTEM

- 6.3 TRENDS & DISRUPTIONS IMPACTING CUSTOMER BUSINESSES

- FIGURE 23 TRENDS & DISRUPTIONS IMPACTING BATTERY COATING MARKET

- 6.4 CASE STUDY ANALYSIS

- 6.4.1 IMPROVEMENTS IN ANODE COATING IN LITHIUM-ION BATTERY

- 6.4.1.1 Objective

- 6.4.1.2 Solution statement

- 6.4.2 PROTECTIVE COATINGS ON SILICON PARTICLES AND THEIR EFFECT ON ENERGY DENSITY AND SPECIFIC ENERGY IN LITHIUM-ION BATTERY

- 6.4.2.1 Objective

- 6.4.2.2 Solution statement

- 6.4.1 IMPROVEMENTS IN ANODE COATING IN LITHIUM-ION BATTERY

- 6.5 PATENT ANALYSIS

- 6.5.1 METHODOLOGY

- 6.5.2 PATENT PUBLICATION TRENDS

- FIGURE 24 NUMBER OF PATENTS YEAR-WISE DURING LAST TEN YEARS

- 6.5.3 INSIGHT

- 6.5.4 JURISDICTION ANALYSIS

- FIGURE 25 CHINA ACCOUNTED FOR HIGHEST NUMBER OF PATENTS

- 6.5.5 TOP COMPANIES/APPLICANTS

- FIGURE 26 TOP TEN COMPANIES/APPLICANTS WITH HIGHEST NUMBER OF PATENTS

- TABLE 8 LIST OF MAJOR PATENTS

- 6.6 KEY CONFERENCES & EVENTS IN 2021-2022

- TABLE 9 BATTERY COATING MARKET: DETAILED LIST OF CONFERENCES & EVENTS

- 6.7 AVERAGE SELLING PRICE ANALYSIS

- FIGURE 27 BATTERY COATING MATERIALS AVERAGE SELLING PRICE ANALYSIS (2021) (USD/TON)

- 6.8 REGULATORY LANDSCAPE

- 6.8.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 10 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 11 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 6.8.2 REGULATIONS ON ELECTRIC VEHICLE BATTERIES

- TABLE 12 REGULATIONS/VOLUNTARY PROCEDURES FOR EV BATTERY PERFORMANCE

- TABLE 13 REGULATIONS/VOLUNTARY PROCEDURES FOR EV BATTERY DURABILITY

- TABLE 14 REGULATIONS/VOLUNTARY PROCEDURES FOR EV BATTERY SAFETY

- TABLE 15 REGULATIONS/VOLUNTARY PROCEDURES FOR EV BATTERY RECYCLING

- 6.8.3 EUROPE AND US REGULATIONS ON LITHIUM-ION BATTERY PRODUCTION

- 6.8.4 REGULATIONS ON BATTERIES AND ACCUMLATORS

- 6.8.5 REGULATIONS ON TRANSPORT OF LITHIUM-ION BATTERIES

- 6.9 COVID-19 IMPACT ANALYSIS

- 6.9.1 COVID-19 HEALTH ASSESSMENT

- FIGURE 28 COUNTRY-WISE SPREAD OF COVID-19

- FIGURE 29 ECONOMIC OUTPUT OF DIFFERENT COUNTRIES, 2020 VS. 2021

- TABLE 16 THREE SCENARIO-BASED ANALYSES OF IMPACT OF COVID-19 ON GLOBAL ECONOMY

- 6.9.2 IMPACT OF COVID-19 ON BATTERY COATING MARKET

- 6.9.2.1 COVID-19 pandemic affected production of lithium-ion batteries

- 6.9.2.2 Impact on electric vehicle industry

- FIGURE 30 IMPACT OF COVID-19 ON SALE OF ELECTRIC VEHICLES

- 6.9.2.3 Impact on electronics industry

- 6.9.2.4 Impact of Ukraine-Russia war on electric car supply chain

7 BATTERY COATING MARKET, BY TECHNOLOGY TYPE

- 7.1 INTRODUCTION

- 7.2 ATOMIC LAYER DEPOSITION (ALD)

- 7.3 PLASMA ENHANCED CHEMICAL VAPOR DEPOSITION (PECVD)

- 7.4 CHEMICAL VAPOR DEPOSITION (CVD)

- 7.5 DRY POWDER COATING

- 7.6 PHYSICAL VAPOR DEPOSITION (PVD)

8 BATTERY COATING MARKET, BY BATTERY COMPONENT

- 8.1 INTRODUCTION

- FIGURE 31 BATTERY COATING MARKET, BY BATTERY COMPONENT, 2022 & 2027 (USD MILLION)

- TABLE 17 BATTERY COATING MARKET SIZE, BY BATTERY COMPONENT, 2018-2021 (USD MILLION)

- TABLE 18 BATTERY COATING MARKET SIZE, BY BATTERY COMPONENT, 2022-2027 (USD MILLION)

- 8.2 ELECTRODE COATING

- TABLE 19 ELECTRODE COATING MARKET SIZE, BY REGION, 2018-2021 (USD MILLION)

- TABLE 20 ELECTRODE COATING MARKET SIZE, BY REGION, 2022-2027 (USD MILLION)

- 8.3 SEPARATOR COATING

- TABLE 21 SEPARATOR COATING MARKET SIZE, BY REGION, 2018-2021 (USD MILLION)

- TABLE 22 SEPARATOR COATING MARKET SIZE, BY REGION, 2022-2027 (USD MILLION)

- 8.4 BATTERY PACK COATING

- TABLE 23 BATTERY PACK COATING MARKET SIZE, BY REGION, 2018-2021 (USD MILLION)

- TABLE 24 BATTERY PACK COATING MARKET SIZE, BY REGION, 2022-2027 (USD MILLION)

9 BATTERY COATING MARKET, BY BATTERY TYPE

- 9.1 INTRODUCTION

- FIGURE 32 BATTERY COATING MARKET, BY BATTERY TYPE, 2022 & 2027 (USD MILLION)

- TABLE 25 BATTERY COATING MARKET SIZE, BY BATTERY TYPE, 2018-2021 (USD MILLION)

- TABLE 26 BATTERY COATING MARKET SIZE, BATTERY TYPE, 2022-2027 (USD MILLION)

- 9.2 LITHIUM-ION BATTERY

- 9.2.1 ELECTRIC VEHICLES AND PORTABLE ELECTRONIC DEVICES INCREASE DEMAND FOR LITHIUM-ION BATTERIES

- 9.3 LEAD-ACID BATTERY

- 9.3.1 WIDELY USED AS SLI BATTERIES

- 9.4 NICKEL-CADMIUM BATTERY

- 9.4.1 NICKEL-CADMIUM BATTERIES ARE MAJORLY USED IN INDUSTRIAL APPLICATIONS

- 9.5 GRAPHENE BATTERY

- 9.5.1 GRAPHENE BATTERIES CAN BE NEXT-GENERATION ENERGY STORAGE SYSTEMS

10 BATTERY COATING MARKET, BY MATERIAL TYPE

- 10.1 INTRODUCTION

- FIGURE 33 BATTERY COATING MARKET, BY MATERIAL TYPE, 2022-2027 (USD MILLION)

- TABLE 27 BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2018-2021 (TONS)

- TABLE 28 BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2022-2027 (TONS)

- TABLE 29 BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2018-2021 (USD MILLION)

- TABLE 30 BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2022-2027 (USD MILLION)

- 10.2 POLYVINYLIDENE FLUORIDE (PVDF)

- 10.2.1 PVDF COATED SEPARATOR OFFERS HIGHER POROSITY AND ELECTROCHEMICAL STABILITY

- TABLE 31 PVDF: BATTERY COATING MARKET SIZE, BY REGION, 2018-2021 (TONS)

- TABLE 32 PVDF: BATTERY COATING MARKET SIZE, BY REGION, 2022-2027 (TONS)

- TABLE 33 PVDF: BATTERY COATING MARKET SIZE, BY REGION, 2018-2021 (USD MILLION)

- TABLE 34 PVDF: BATTERY COATING MARKET SIZE, BY REGION, 2022-2027 (USD MILLION)

- 10.3 CERAMIC

- 10.3.1 CERAMIC COATING SEPARATORS HAVE NEGLIGIBLE SHRINKAGE AT HIGH TEMPERATURES

- TABLE 35 CERAMIC: BATTERY COATING MARKET SIZE, BY REGION, 2018-2021 (TONS)

- TABLE 36 CERAMIC: BATTERY COATING MARKET SIZE, BY REGION, 2022-2027 (TONS)

- TABLE 37 CERAMIC: BATTERY COATING MARKET SIZE, BY REGION, 2018-2021 (USD MILLION)

- TABLE 38 CERAMIC: BATTERY COATING MARKET SIZE, BY REGION, 2022-2027 (USD MILLION)

- 10.4 ALUMINA

- 10.4.1 ALUMINA CAN IMPROVE MECHANICAL STRENGTH OF BATTERY SEPARATOR

- TABLE 39 ALUMINA: BATTERY COATING MARKET SIZE, BY REGION, 2018-2021 (TONS)

- TABLE 40 ALUMINA: BATTERY COATING MARKET SIZE, BY REGION, 2022-2027 (TONS)

- TABLE 41 ALUMINA: BATTERY COATING MARKET SIZE, BY REGION, 2018-2021 (USD MILLION)

- TABLE 42 ALUMINA: BATTERY COATING MARKET SIZE, BY REGION, 2022-2027 (USD MILLION)

- 10.5 OXIDE

- 10.5.1 OXIDE COATING IS A PROMISING METHOD FOR CATHODE STABILIZATION

- TABLE 43 OXIDE: BATTERY COATING MARKET SIZE, BY REGION, 2018-2021 (TONS)

- TABLE 44 OXIDE: BATTERY COATING MARKET SIZE, BY REGION, 2022-2027 (TONS)

- TABLE 45 OXIDE: BATTERY COATING MARKET SIZE, BY REGION, 2018-2021 (USD MILLION)

- TABLE 46 OXIDE: BATTERY COATING MARKET SIZE, BY REGION, 2022-2027 (USD MILLION)

- 10.6 CARBON

- 10.6.1 CARBON-COATED GRAPHITE ANODE MATERIALS OFFER IMPROVED CYCLING AND ELECTROCHEMICAL PERFORMANCE

- TABLE 47 CARBON: BATTERY COATING MARKET SIZE, BY REGION, 2018-2021 (TONS)

- TABLE 48 CARBON: BATTERY COATING MARKET SIZE, BY REGION, 2022-2027 (TONS)

- TABLE 49 CARBON: BATTERY COATING MARKET SIZE, BY REGION, 2018-2021 (USD MILLION)

- TABLE 50 CARBON: BATTERY COATING MARKET SIZE, BY REGION, 2022-2027 (USD MILLION)

- 10.7 POLYURETHANE (PU)

- 10.7.1 PU IS CONSIDERED PROMISING MATERIAL FOR BATTERY PACK COATING

- TABLE 51 POLYURETHANE: BATTERY COATING MARKET SIZE, BY REGION 2018-2021 (TONS)

- TABLE 52 POLYURETHANE: BATTERY COATING MARKET SIZE, BY REGION, 2022-2027 (TONS)

- TABLE 53 POLYURETHANE: BATTERY COATING MARKET SIZE, BY REGION, 2018-2021 (USD MILLION)

- TABLE 54 POLYURETHANE: BATTERY COATING MARKET SIZE, BY REGION, 2022-2027 (USD MILLION)

- 10.8 EPOXY

- 10.8.1 EPOXY HELPS DELIVER APPROPRIATE LEVELS OF THERMAL AND MECHANICAL SHOCK RESISTANCE TO ELECTRIC VEHICLE BATTERY COMPONENTS

- TABLE 55 EPOXY: BATTERY COATING MARKET SIZE, BY REGION, 2018-2021 (TONS)

- TABLE 56 EPOXY: BATTERY COATING MARKET SIZE, BY REGION, 2022-2027 (TONS)

- TABLE 57 EPOXY: BATTERY COATING MARKET SIZE, BY REGION, 2018-2021 (USD MILLION)

- TABLE 58 EPOXY: BATTERY COATING MARKET SIZE, BY REGION, 2022-2027 (USD MILLION)

- 10.9 OTHERS

- TABLE 59 OTHERS: BATTERY COATING MARKET SIZE, BY REGION, 2018-2021 (TONS)

- TABLE 60 OTHERS: BATTERY COATING MARKET SIZE, BY REGION, 2022-2027 (TONS)

- TABLE 61 OTHERS: BATTERY COATING MARKET SIZE, BY REGION, 2018-2021 (USD MILLION)

- TABLE 62 OTHERS: BATTERY COATING MARKET SIZE, BY REGION, 2022-2027 (USD MILLION)

11 REGIONAL ANALYSIS

- 11.1 INTRODUCTION

- FIGURE 34 REGIONAL SNAPSHOT: ASIAN COUNTRIES SUCH AS CHINA, SOUTH KOREA, AND JAPAN TO OFFER LUCRATIVE GROWTH OPPORTUNITIES TO BATTERY COATING MARKET DURING FORECAST PERIOD

- TABLE 63 GLOBAL BATTERY COATING MARKET SIZE, BY REGION, 2018-2021 (TONS)

- TABLE 64 GLOBAL BATTERY COATING MARKET SIZE, BY REGION, 2022-2027 (TONS)

- TABLE 65 GLOBAL BATTERY COATING MARKET SIZE, BY REGION, 2018-2021 (USD MILLION)

- TABLE 66 GLOBAL BATTERY COATING MARKET SIZE, BY REGION, 2022-2027 (USD MILLION)

- TABLE 67 GLOBAL BATTERY COATING MARKET SIZE, BY BATTERY COMPONENT, 2018-2021 (USD MILLION)

- TABLE 68 GLOBAL BATTERY COATING MARKET SIZE, BY BATTERY COMPONENT, 2022-2027 (USD MILLION)

- TABLE 69 GLOBAL BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2018-2021 (TONS)

- TABLE 70 GLOBAL BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2022-2027 (TONS)

- TABLE 71 GLOBAL BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2018-2021 (USD MILLION)

- TABLE 72 GLOBAL BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2022-2027 (USD MILLION)

- 11.2 ASIA PACIFIC

- FIGURE 35 ASIA PACIFIC BATTERY COATING MARKET SNAPSHOT

- TABLE 73 ASIA PACIFIC: BATTERY COATING MARKET SIZE, BY COUNTRY, 2018-2021(TONS)

- TABLE 74 ASIA PACIFIC: BATTERY COATING MARKET SIZE, BY COUNTRY, 2022-2027(TONS)

- TABLE 75 ASIA PACIFIC: BATTERY COATING MARKET SIZE, BY COUNTRY, 2018-2021(USD MILLION)

- TABLE 76 ASIA PACIFIC: BATTERY COATING MARKET SIZE, BY COUNTRY, 2022-2027(USD MILLION)

- TABLE 77 ASIA PACIFIC: BATTERY COATING MARKET SIZE, BY BATTERY COMPONENT, 2018-2021 (USD MILLION)

- TABLE 78 ASIA PACIFIC: BATTERY COATING MARKET SIZE, BY BATTERY COMPONENT, 2022-2027 (USD MILLION)

- TABLE 79 ASIA PACIFIC: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2018-2021 (TONS)

- TABLE 80 ASIA PACIFIC: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2022-2027 (TONS)

- TABLE 81 ASIA PACIFIC: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2018-2021 (USD MILLION)

- TABLE 82 ASIA PACIFIC: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2022-2027 (USD MILLION)

- 11.2.1 CHINA

- 11.2.1.1 Accounts for largest share in battery coating market in Asia Pacific

- TABLE 83 CHINA: BATTERY COATING MARKET SIZE, BY BATTERY COMPONENT, 2018-2021 (USD MILLION)

- TABLE 84 CHINA: BATTERY COATING MARKET SIZE, BY BATTERY COMPONENT, 2022-2027 (USD MILLION)

- TABLE 85 CHINA: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2018-2021 (TONS)

- TABLE 86 CHINA: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2022-2027 (TONS)

- TABLE 87 CHINA: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2018-2021 (USD MILLION)

- TABLE 88 CHINA: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2022-2027 (USD MILLION)

- 11.2.2 SOUTH KOREA

- 11.2.2.1 Government initiatives in EV and battery storage sector to drive market growth

- TABLE 89 SOUTH KOREA: BATTERY COATING MARKET SIZE, BY BATTERY COMPONENT, 2018-2021 (USD MILLION)

- TABLE 90 SOUTH KOREA: BATTERY COATING MARKET SIZE, BY BATTERY COMPONENT, 2022-2027 (USD MILLION)

- TABLE 91 SOUTH KOREA: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2018-2021 (TONS)

- TABLE 92 SOUTH KOREA: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2022-2027 (TONS)

- TABLE 93 SOUTH KOREA: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2018-2021 (USD MILLION)

- TABLE 94 SOUTH KOREA: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2022-2027 (USD MILLION)

- 11.2.3 JAPAN

- 11.2.3.1 Presence of major battery manufacturers to spur market growth

- TABLE 95 JAPAN: BATTERY COATING MARKET SIZE, BY BATTERY COMPONENT, 2018-2021 (USD MILLION)

- TABLE 96 JAPAN: BATTERY COATING MARKET SIZE, BY BATTERY COMPONENT, 2022-2027 (USD MILLION)

- TABLE 97 JAPAN: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2018-2021 (TONS)

- TABLE 98 JAPAN: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2022-2027 (TONS)

- TABLE 99 JAPAN: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2018-2021 (USD MILLION)

- TABLE 100 JAPAN: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2022-2027 (USD MILLION)

- 11.2.4 INDIA

- 11.2.4.1 Growing solar industry to boost market for battery coating

- TABLE 101 INDIA: BATTERY COATING MARKET SIZE, BY BATTERY COMPONENT, 2018-2021 (USD MILLION)

- TABLE 102 INDIA: BATTERY COATING MARKET SIZE, BY BATTERY COMPONENT, 2022-2027 (USD MILLION)

- TABLE 103 INDIA: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2018-2021 (TONS)

- TABLE 104 INDIA: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2022-2027 (TONS)

- TABLE 105 INDIA: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2018-2021 (USD MILLION)

- TABLE 106 INDIA: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2022-2027 (USD MILLION)

- 11.2.5 REST OF ASIA PACIFIC

- TABLE 107 REST OF ASIA PACIFIC: BATTERY COATING MARKET SIZE, BY BATTERY COMPONENT, 2018-2021 (USD MILLION)

- TABLE 108 REST OF ASIA PACIFIC: BATTERY COATING MARKET SIZE, BY BATTERY COMPONENT, 2022-2027 (USD MILLION)

- TABLE 109 REST OF ASIA PACIFIC: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2018-2021 (TONS)

- TABLE 110 REST OF ASIA PACIFIC: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2022-2027 (TONS)

- TABLE 111 REST OF ASIA PACIFIC: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2018-2021 (USD MILLION)

- TABLE 112 REST OF ASIA PACIFIC: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2022-2027 (USD MILLION)

- 11.3 EUROPE

- FIGURE 36 EUROPE BATTERY COATING MARKET SNAPSHOT

- TABLE 113 EUROPE: BATTERY COATING MARKET SIZE, BY COUNTRY, 2018-2021 (TONS)

- TABLE 114 EUROPE: BATTERY COATING MARKET SIZE, BY COUNTRY, 2022-2027 (TONS)

- TABLE 115 EUROPE: BATTERY COATING MARKET SIZE, BY COUNTRY, 2018-2021 (USD MILLION)

- TABLE 116 EUROPE: BATTERY COATING MARKET SIZE, BY COUNTRY, 2022-2027 (USD MILLION))

- TABLE 117 EUROPE: BATTERY COATING MARKET SIZE, BY BATTERY COMPONENT, 2018-2021 (USD MILLION)

- TABLE 118 EUROPE: BATTERY COATING MARKET SIZE, BY BATTERY COMPONENT, 2022-2027 (USD MILLION)

- TABLE 119 EUROPE: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2018-2021 (TONS)

- TABLE 120 EUROPE: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2022-2027 (TONS)

- TABLE 121 EUROPE: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2018-2021 (USD MILLION)

- TABLE 122 EUROPE: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2022-2027 (USD MILLION)

- 11.3.1 GERMANY

- 11.3.1.1 Presence of key battery and EV manufacturers to spur market growth

- TABLE 123 GERMANY: BATTERY COATING MARKET SIZE, BY BATTERY COMPONENT, 2018-2021 (USD MILLION)

- TABLE 124 GERMANY: BATTERY COATING MARKET SIZE, BY BATTERY COMPONENT, 2022-2027 (USD MILLION)

- TABLE 125 GERMANY: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2018-2021 (USD MILLION)

- TABLE 126 GERMANY: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2022-2027 (USD MILLION)

- TABLE 127 GERMANY: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2018-2021 (TONS)

- TABLE 128 GERMANY: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2022-2027 (TONS)

- 11.3.2 FRANCE

- 11.3.2.1 Government initiatives in EV industry to boost battery coating market

- TABLE 129 FRANCE: BATTERY COATING MARKET SIZE, BY BATTERY COMPONENT, 2018-2021 (USD MILLION)

- TABLE 130 FRANCE: BATTERY COATING MARKET SIZE, BY BATTERY COMPONENT, 2022-2027 (USD MILLION)

- TABLE 131 FRANCE: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2018-2021 (USD MILLION)

- TABLE 132 FRANCE: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2022-2027 (USD MILLION)

- TABLE 133 FRANCE: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2018-2021 (TONS)

- TABLE 134 FRANCE: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2022-2027 (TONS)

- 11.3.3 UK

- 11.3.3.1 Increasing investments in energy storage market to drive battery coating market

- TABLE 135 UK: BATTERY COATING MARKET SIZE, BY BATTERY COMPONENT, 2018-2021 (USD MILLION)

- TABLE 136 UK: BATTERY COATING MARKET SIZE, BY BATTERY COMPONENT, 2022-2027 (USD MILLION)

- TABLE 137 UK: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2018-2021 (USD MILLION)

- TABLE 138 UK: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2022-2027 (USD MILLION)

- TABLE 139 UK: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2018-2021 (TONS)

- TABLE 140 UK: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2022-2027 (TONS)

- 11.3.4 REST OF EUROPE

- TABLE 141 REST OF EUROPE: BATTERY COATING MARKET SIZE, BY BATTERY COMPONENT, 2018-2021 (USD MILLION)

- TABLE 142 REST OF EUROPE: BATTERY COATING MARKET SIZE, BY BATTERY COMPONENT, 2022-2027 (USD MILLION)

- TABLE 143 REST OF EUROPE: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2018-2021 (USD MILLION)

- TABLE 144 REST OF EUROPE: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2022-2027 (USD MILLION)

- TABLE 145 REST OF EUROPE: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2018-2021 (TONS)

- TABLE 146 REST OF EUROPE: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2022-2027 (TONS)

- 11.4 NORTH AMERICA

- FIGURE 37 NORTH AMERICA BATTERY COATING MARKET SNAPSHOT

- TABLE 147 NORTH AMERICA: BATTERY COATING MARKET SIZE, BY COUNTRY, 2018-2021 (TONS)

- TABLE 148 NORTH AMERICA: BATTERY COATING MARKET SIZE, BY COUNTRY, 2022-2027 (TONS)

- TABLE 149 NORTH AMERICA: BATTERY COATING MARKET SIZE, BY COUNTRY, 2018-2021 (USD MILLION)

- TABLE 150 NORTH AMERICA: BATTERY COATING MARKET SIZE, BY COUNTRY, 2022-2027 (USD MILLION)

- TABLE 151 NORTH AMERICA: BATTERY COATING MARKET SIZE, BY BATTERY COMPONENT, 2018-2021 (USD MILLION)

- TABLE 152 NORTH AMERICA: BATTERY COATING MARKET SIZE, BY BATTERY COMPONENT, 2022-2027 (USD MILLION)

- TABLE 153 NORTH AMERICA: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2018-2021 (TONS)

- TABLE 154 NORTH AMERICA: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2022-2027 (TONS)

- TABLE 155 NORTH AMERICA: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2018-2021 (USD MILLION)

- TABLE 156 NORTH AMERICA: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2022-2027 (USD MILLION)

- 11.4.1 US

- 11.4.1.1 Accounts for largest market share of battery coating in North America

- TABLE 157 US: BATTERY COATING MARKET SIZE, BY BATTERY COMPONENT, 2018-2021 (USD MILLION)

- TABLE 158 US: BATTERY COATING MARKET SIZE, BY BATTERY COMPONENT, 2022-2027 (USD MILLION)

- TABLE 159 US: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2018-2021 (TONS)

- TABLE 160 US: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2022-2027 (TONS)

- TABLE 161 US: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2018-2021 (USD MILLION)

- TABLE 162 US: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2022-2027 (USD MILLION)

- 11.4.2 REST OF NORTH AMERICA

- TABLE 163 REST OF NORTH AMERICA: BATTERY COATING MARKET SIZE, BY BATTERY COMPONENT, 2018-2021 (USD MILLION)

- TABLE 164 REST OF NORTH AMERICA: BATTERY COATING MARKET SIZE, BY BATTERY COMPONENT, 2022-2027 (USD MILLION)

- TABLE 165 REST OF NORTH AMERICA: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2018-2021 (TONS)

- TABLE 166 REST OF NORTH AMERICA: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2022-2027 (TONS)

- TABLE 167 REST OF NORTH AMERICA: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2018-2021 (USD MILLION)

- TABLE 168 REST OF NORTH AMERICA: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2022-2027 (USD MILLION)

- 11.5 REST OF THE WORLD (ROW)

- TABLE 169 REST OF THE WORLD: BATTERY COATING MARKET SIZE, BY BATTERY COMPONENT, 2018-2021 (USD MILLION)

- TABLE 170 REST OF THE WORLD: BATTERY COATING MARKET SIZE, BY BATTERY COMPONENT, 2022-2027 (USD MILLION)

- TABLE 171 REST OF THE WORLD: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2018-2021 (TONS)

- TABLE 172 REST OF THE WORLD: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2022-2027 (TONS)

- TABLE 173 REST OF THE WORLD: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2018-2021 (USD MILLION)

- TABLE 174 REST OF THE WORLD: BATTERY COATING MARKET SIZE, BY MATERIAL TYPE, 2022-2027 (USD MILLION)

12 COMPETITIVE LANDSCAPE

- 12.1 OVERVIEW

- 12.2 KEY PLAYER STRATEGIES

- TABLE 175 OVERVIEW OF STRATEGIES ADOPTED BY BATTERY COATING MANUFACTURERS

- 12.3 REVENUE ANALYSIS

- 12.3.1 REVENUE ANALYSIS OF TOP PLAYERS IN BATTERY COATING MARKET

- FIGURE 38 TOP PLAYERS - REVENUE ANALYSIS (2016-2020)

- 12.4 MARKET SHARE ANALYSIS: BATTERY COATING

- FIGURE 39 MARKET SHARE: BATTERY COATING MARKET

- 12.5 COMPETITIVE LANDSCAPE MAPPING, 2021

- 12.5.1 STAR

- 12.5.2 EMERGING LEADERS

- 12.5.3 PERVASIVE

- 12.5.4 PARTICIPANTS

- FIGURE 40 BATTERY COATING MARKET: COMPETITIVE LANDSCAPE MAPPING

- 12.6 COMPETITIVE BENCHMARKING

- 12.6.1 STRENGTH OF PRODUCT PORTFOLIO

- FIGURE 41 PRODUCT PORTFOLIO ANALYSIS OF TOP PLAYERS IN BATTERY COATING MARKET

- 12.6.2 BUSINESS STRATEGY EXCELLENCE

- FIGURE 42 BUSINESS STRATEGY EXCELLENCE OF TOP PLAYERS IN BATTERY COATING MARKET

- 12.7 SME MATRIX, 2021

- 12.7.1 PROGRESSIVE COMPANIES

- 12.7.2 DYNAMIC COMPANIES

- 12.7.3 RESPONSIVE COMPANIES

- 12.7.4 STARTING BLOCKS

- FIGURE 43 BATTERY COATING MARKET: COMPETITIVE LEADERSHIP MAPPING OF EMERGING COMPANIES

- TABLE 176 COMPANY BATTERY TYPE FOOTPRINT, 2020

- TABLE 177 COMPANY MATERIAL TYPE FOOTPRINT, 2020

- TABLE 178 COMPANY REGION FOOTPRINT, 2020

- TABLE 179 COMPANY APPLICATION FOOTPRINT, 2020

- TABLE 180 BATTERY COATING: DETAILED LIST OF KEY STARTUPS/SMES

- TABLE 181 BATTERY COATING: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- 12.8 KEY MARKET DEVELOPMENTS

- TABLE 182 BATTERY COATING MARKET: NEW PRODUCT LAUNCHES, 2016-2022

- TABLE 183 BATTERY COATING MARKET: DEALS, 2016-2022

13 COMPANY PROFILES

- (Business Overview, Products Offered, Recent Developments, and MnM View (Key strengths/Right to Win, Strategic Choices Made, and Weaknesses and Competitive Threats))**

- 13.1 SOLVAY SA

- TABLE 184 SOLVAY SA: COMPANY OVERVIEW

- FIGURE 44 SOLVAY SA: COMPANY SNAPSHOT

- 13.2 ARKEMA SA

- TABLE 185 ARKEMA SA: COMPANY OVERVIEW

- FIGURE 45 ARKEMA SA: COMPANY SNAPSHOT

- 13.3 PPG INDUSTRIES, INC.

- TABLE 186 PPG INDUSTRIES, INC.: COMPANY OVERVIEW

- FIGURE 46 PPG INDUSTRIES, INC.: COMPANY SNAPSHOT

- 13.4 ASAHI KASEI CORPORATION

- TABLE 187 ASAHI KASEI CORPORATION: COMPANY OVERVIEW

- FIGURE 47 ASAHI KASEI CORPORATION: COMPANY SNAPSHOT

- 13.5 MITSUBISHI PAPER MILLS LTD.

- TABLE 188 MITSUBISHI PAPER MILLS LTD.: COMPANY OVERVIEW

- FIGURE 48 MITSUBISHI PAPER MILLS LTD.: COMPANY SNAPSHOT

- 13.6 UBE INDUSTRIES LTD.

- TABLE 189 UBE INDUSTRIES LTD.: COMPANY OVERVIEW

- FIGURE 49 UBE INDUSTRIES LTD.: COMPANY SNAPSHOT

- 13.7 TANAKA CHEMICAL CORPORATION

- TABLE 190 TANAKA CHEMICAL CORPORATION: COMPANY OVERVIEW

- FIGURE 50 TANAKA CHEMICAL CORPORATION: COMPANY SNAPSHOT

- 13.8 SK INNOVATION CO., LTD.

- TABLE 191 SK INNOVATION CO., LTD.: COMPANY OVERVIEW

- FIGURE 51 SK INNOVATION CO., LTD.: COMPANY SNAPSHOT

- 13.9 DURR GROUP

- TABLE 192 DURR GROUP: COMPANY OVERVIEW

- FIGURE 52 DURR GROUP: COMPANY SNAPSHOT

- 13.10 ASHLAND GLOBAL HOLDINGS INC.

- TABLE 193 ASHLAND GLOBAL HOLDINGS INC.: COMPANY OVERVIEW

- FIGURE 53 ASHLAND GLOBAL HOLDINGS INC.: COMPANY SNAPSHOT

- 13.11 AXALTA COATING SYSTEMS, LTD.

- 13.11.1 BUSINESS OVERVIEW

- TABLE 194 AXALTA COATING SYSTEMS LTD.: COMPANY OVERVIEW

- FIGURE 54 AXALTA COATING SYSTEMS LTD.: COMPANY SNAPSHOT

- 13.12 APV ENGINEERED COATINGS

- TABLE 195 APV ENGINEERED COATINGS: COMPANY OVERVIEW

- 13.13 SAMCO INC.

- TABLE 196 SAMCO INC.: COMPANY OVERVIEW

- 13.14 UNIFRAX

- TABLE 197 UNIFRAX: COMPANY OVERVIEW

- 13.15 TARGRAY TECHNOLOGY INTERNATIONAL INC.

- TABLE 198 TARGRAY TECHNOLOGY INTERNATIONAL INC.: COMPANY OVERVIEW

- 13.16 OTHER COMPANIES

- 13.16.1 NEI CORPORATION

- TABLE 199 NEI CORPORATION: COMPANY OVERVIEW

- 13.16.2 ALTEO

- TABLE 200 ALTEO: COMPANY OVERVIEW

- 13.16.3 NEXEON LIMITED

- TABLE 201 NEXEON LIMITED: COMPANY OVERVIEW

- 13.16.4 NANO ONE MATERIALS CORP.

- TABLE 202 NANO ONE MATERIALS CORP.: COMPANY OVERVIEW

- 13.16.5 BENEQ

- TABLE 203 BENEQ: COMPANY OVERVIEW

- 13.16.6 FORGE NANO INC.

- TABLE 204 FORGE NANO INC.: COMPANY OVERVIEW

- 13.16.7 XIAMEN ACEY NEW ENERGY TECHNOLOGY CO., LTD.

- TABLE 205 XIAMEN ACEY NEW ENERGY TECHNOLOGY CO., LTD.: COMPANY OVERVIEW

- 13.16.8 SHANDONG HENGYI NEW MATERIAL TECHNOLOGY CO., LTD

- TABLE 206 SHANDONG HENGYI NEW MATERIAL TECHNOLOGY CO., LTD: COMPANY OVERVIEW

- 13.16.9 GUJARAT FLUOROCHEMICALS LIMITED

- TABLE 207 GUJARAT FLUOROCHEMICALS LIMITED: COMPANY OVERVIEW

- 13.16.10 PULRON

- TABLE 208 PULRON: COMPANY OVERVIEW

- 13.16.11 WRIGHT COATING TECHNOLOGIES

- TABLE 209 WRIGHT COATING TECHNOLOGIES: COMPANY OVERVIEW

- 13.16.12 ALCOLOR

- TABLE 210 ALCOLOR: COMPANY OVERVIEW

- 13.16.13 AKZO NOBEL N.V.

- TABLE 211 AKZO NOBEL N.V.: COMPANY OVERVIEW

- *Details on Business Overview, Products Offered, Recent Developments, and MnM View (Key strengths/Right to Win, Strategic Choices Made, and Weaknesses and Competitive Threats) might not be captured in case of unlisted companies.

14 APPENDIX

- 14.1 DISCUSSION GUIDE

- 14.2 KNOWLEDGE STORE: MARKETSANDMARKETS SUBSCRIPTION PORTAL

- 14.3 AVAILABLE CUSTOMIZATIONS

- 14.4 RELATED REPORTS

- 14.5 AUTHOR DETAILS