|

|

市場調査レポート

商品コード

1267436

気道確保装置の世界市場:種類別・用途別・エンドユーザー別の将来予測 (2028年まで)Airway Management Devices Market by Type, Application, End User - Global Forecast to 2028 |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| 気道確保装置の世界市場:種類別・用途別・エンドユーザー別の将来予測 (2028年まで) |

|

出版日: 2023年04月28日

発行: MarketsandMarkets

ページ情報: 英文 286 Pages

納期: 即納可能

|

- 全表示

- 概要

- 目次

世界の気道確保装置の市場規模は、2022年の18億米ドルから、2028年には24億米ドルに達すると予測され、予測期間中のCAGRは5.6%と見込まれています。

この市場の成長は、慢性呼吸器疾患の発症率の上昇や、高齢者人口・早産などの増加、医療インフラへの投資拡大が主な要因となっています。しかし、特定の気道確保装置が新生児に及ぼす有害な影響が、気道確保装置市場の成長を抑制しています。

"声門下気道装置のセグメントが世界の気道確保装置市場において、予測期間中に種類別では最も高い市場シェアを占める"

声門下気道装置は、予測期間中に高い市場シェアを獲得すると予想されます。その要因として、さまざまな慢性呼吸器疾患の発生率・有病率の増加や、陽圧換気を必要とする呼吸不全に直面する患者の増加などを受けて、挿管処置や声門下気道装置の需要が世界規模で高まっていることが挙げられます。

"患者年齢別では、成人患者セグメントが予測期間中に最も高いCAGRで成長する"

患者年齢に基づくと、予測期間中、成人患者セグメントが最も高いCAGRを占めています。その要因として、高齢者人口における慢性疾患の有病率の高さや、外科的介入中や治療レジメン中の成人患者向けのさまざまな気道確保装置の採用増加などが挙げられます。

"用途別では、麻酔セグメントが予測期間中に最も高いCAGRで成長する"

用途別に見ると、麻酔セグメントが予測期間中に最も高いCAGRを占めています。肺疾患の有病率の上昇による麻酔用途のセグメントの成長や、手術中の麻酔関連問題のリスクを低減するために呼吸通路を確保する必要性といった要因が、外科手術の件数とともに拡大しています。

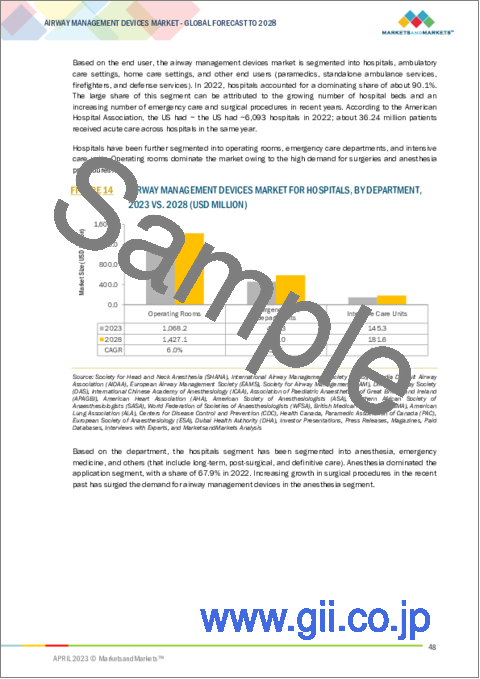

"エンドユーザー別では、病院セグメントが予測期間中に最大の市場シェアを占める"

病院セグメントは、予測期間中に最大の市場シェアを保持すると予想されています。その要因として、新興国における病院数の増加により、手術室やその他の病院部門に配備される気道確保装置の需要が促進されることが挙げられるほか、外科手術数の増加も病院セグメントの成長を支えています。

"北米が、気道確保装置市場で予測期間中に最も高いシェアを占める"

北米は、予測期間中、高い市場シェアを占めると予想されています。慢性呼吸器疾患の有病率の増加、医療環境の拡大、気道確保装置に対する有利な償還政策が、市場の成長を支えています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- イントロダクション

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

第6章 業界考察

- イントロダクション

- 業界動向

- 需要側の分析

- 規制分析

- ポーターのファイブフォース分析

- バリューチェーン分析

- エコシステム分析

- 特許分析

第7章 気道確保装置市場:種類別

- イントロダクション

- 声門下気道装置

- 気管内チューブ

- 気管切開チューブ

- 声門上気道装置

- 喉頭マスク気道装置

- 中咽頭気道装置

- 鼻咽頭気道装置

- その他の声門上気道装置

- 喉頭鏡

- 従来型喉頭鏡

- ビデオ喉頭鏡

- 蘇生器

- 輪状甲状靭帯切開キット

- その他の気道確保装置

第8章 気道確保装置市場:患者年齢別

- イントロダクション

- 成人患者

- 小児患者/新生児

第9章 気道確保装置市場:用途別

- イントロダクション

- 麻酔

- 救急医療

- その他の用途

第10章 気道確保装置市場:エンドユーザー別

- イントロダクション

- 病院

- 手術室

- 救急医療部門

- 集中治療室

- 外来診療センター

- 在宅医療

- その他のエンドユーザー

第11章 気道確保装置市場:地域別

- イントロダクション

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- フランス

- 英国

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 日本

- 中国

- インド

- その他アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第12章 競合情勢

- 概要

- 主要企業が採用した戦略

- 気道確保装置市場の主要企業が採用する主要な戦略

- 主要企業の収益シェア分析

- 市場シェア分析

- 企業評価クアドラント

- 企業評価クアドラント:スタートアップ/中小企業向け

- 企業の製品フットプリント

- 競合シナリオ

第13章 企業プロファイル

- 主要企業

- MEDTRONIC

- ICU MEDICAL, INC.

- TELEFLEX INCORPORATED

- AMBU A/S

- CONVATEC GROUP PLC

- KARL STORZ SE & CO. KG

- FLEXICARE (GROUP) LIMITED

- INTERSURGICAL LTD.

- SUNMED LLC

- VYAIRE

- VBM MEDIZINTECHNIK GMBH

- VERATHON INC.

- SOURCEMARK

- MERCURY ENTERPRISES

- ATOS MEDICAL

- P3 MEDICAL

- HENAN TUOREN MEDICAL DEVICE CO., LTD.

- MEDEREN NEOTECH LTD.

- BOMIMED

- MEDIS MEDICAL (UK) LTD.

- その他の企業

- OLYMPUS CORPORATION

- ARMSTRONG MEDICAL LTD. (EAKIN HEALTHCARE GROUP)

- NIHON KOHDEN CORPORATION

- SHENZHEN HUGEMED MEDICAL TECHNICAL DEVELOPMENT CO., LTD.

- VENNER MEDICAL MEDIZINTECHNIK

第14章 付録

The global airway management devices market is projected to reach USD 2.4 Billion by 2028 from USD 1.8 Billion in 2022, at a CAGR of 5.6% during the forecast period. The growth of this market is majorly driven by the growth in the increasing incidence of chronic respiratory disease, geriatric population, and pre-term births, and the rising investments in healthcare infrastructure. However, harmful effects of certain airway management devices on neonates restrain the growth of airway management devices market.

"The infraglottic devices segment accounted for the highest market share in the global airway management devices market, by type, during the forecast period."

Based on the type of segment, the airway management devices market has been segmented into laryngoscopes, resuscitators, infraglottic devices, supraglottic devices, cricothyrotomy kits, and other airway management devices. The infraglottic devices segment is expected to witness high market share during the forecast period. This can be attributed to factors such as the increasing incidence and prevalence rate of various chronic respiratory disorders and the increasing number of patients facing respiratory failure demanding for positive air pressure ventilation is driving the intubation procedures and infraglottic devices globally.

Based on patient age, the adult patients' segment is expected to register the highest CAGR during the forecast period.

Based on patient age, adult patients segment accounted for the highest CAGR during the forecast period. This can be attributed to factors such as the high prevalence of chronic diseases in geriatric population and increasing adoption of different airway management devices among adult patients during surgical interventions and treatment regimens.

"Based on application, anesthesia segment accounted for the highest CAGR during the forecast period."

Based on application, anesthesia segment accounted for the highest CAGR during the forecast period. Factors supporting the growth of anesthesia application segment due to increasing prevalence of pulmonary disorders and the requirement to maintain a secure breathing passage to reduce the risk of anesthesia related problems during surgery is growing along with the number of surgical operations.

"Based on end-user, the hospitals segment holds the largest market share during the forecast period.''

The hospital segment is expected to hold the largest market share during the forecast period. This can be attributed to the rising number of hospitals in developing countries which is expected to drive the demand for airway management devices deployed in operating rooms and other hospital departments in emerging economies and the rising number of surgical procedures also supports the growth of the hospitals segment.

"The North America segment accounted for the highest market share in the airway management devices market, by region, during the forecast period."

Based on the region, the global airway management devices market is categorized into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa. North America is expected to witness a high market share during the forecast period. Increasing prevalence of chronic respiratory diseases, the rising number of healthcare settings, and favorable reimbursement policies for airway management devices are supporting the growth of the market.

Breakdown of supply-side primary interviews, by company type, designation, and region:

- By Company Type: Tier 1 (35%), Tier 2 (45%), and Tier 3 (20%)

- By Designation: C-level (35%), Director-level (25%), and Others (40%)

- By Region: North America (45%), Asia- Pacific (20%), Europe (30%), Latin America (3%) and Middle East & Africa(2%)

Prominent companies include Medtronic (Ireland), ICU Medical, Inc. (US), Teleflex Incorporated (US), Ambu A/S (Denmark), ConvaTec Group Plc (UK), KARL STORZ SE & CO. KG (Germany), Flexicare Group Ltd. (UK), Intersurgical Ltd. (UK), SunMed LLC (US), Vyaire (US), Verathon Inc. (US), Sourcemark LLC (US), VBM Medizintecnik GmBH (Germany), Mercury Enterprises (US), Atos Medical (Sweden), P3 Medical (UK), Henan Tuoren Medical Device Co. Ltd. (China), BOMImed (Canada), Mederen Neotech Ltd. (Israel), and Medis Medical (UK) Ltd.(China), Olympus Corporation (Japan), Armstrong Medical Ltd. (Eakin Healthcare Group) (UK), Nihon Kohden Corporation (Japan) and Shenzen Hugemed Medical Technical Development Co. Ltd. (China).

Research Coverage

This research report categorizes the electrophoresis market by type (laryngoscopes, resuscitators, infraglottic devices, supraglottic devices, cricothyrotomy kits, and other airway management devices), by patient age (Adult patients and pediatric patients/Neonates), by application (Anesthesia, emergency medicine and other applications), by end users (Hospitals, ambulatory care settings, home care settings and others) and region (North America, Europe, Asia Pacific, Latin America and Middle East & Africa). The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the airway management devices market. A detailed analysis of the key industry players has been done to provide insights into their business overview, product offerings; key strategies; partnerships, agreements, new product & service launches, mergers and acquisitions, and recent developments associated with the airway management devices market.

Key Benefits of Buying the Report:

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall airway devices management market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and to plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

This report provides insights into the following pointers:

- Market Penetration: Comprehensive information on product portfolios offered by the top players in the global airway management devices market. The report analyzes this market by type, application, patient age, and end user.

- Product Enhancement/Innovation: Detailed insights on upcoming trends, technology, and product launches in the global airway management devices market.

- Market Development: Comprehensive information on the lucrative emerging markets by type, application, patient age, and end user and region.

- Market Diversification: Exhaustive information about new products or product enhancements, growing geographies, recent developments, and investments in the global airway management devices market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, product offerings, competitive leadership mapping, and capabilities of leading players in the global airway management devices market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.2.2 MARKETS COVERED

- 1.2.3 GEOGRAPHICAL SCOPE

- 1.2.4 YEARS CONSIDERED

- 1.3 CURRENCY CONSIDERED

- TABLE 1 EXCHANGE RATES UTILIZED FOR CONVERSION TO USD

- 1.4 RESEARCH LIMITATIONS

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

- 1.6.1 IMPACT OF ECONOMIC RECESSION ON AIRWAY MANAGEMENT DEVICES MARKET

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH APPROACH

- FIGURE 1 RESEARCH DESIGN

- 2.1.1 SECONDARY RESEARCH

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY RESEARCH

- 2.1.2.1 Primary sources

- 2.1.2.2 Key data from primary sources

- 2.1.2.3 Insights from primary experts

- 2.1.2.4 Breakdown of primary participants

- 2.2 MARKET SIZE ESTIMATION

- FIGURE 2 MARKET SIZE ESTIMATION: REVENUE SHARE ANALYSIS

- FIGURE 3 AIRWAY MANAGEMENT DEVICES MARKET: COMPANY REVENUE ESTIMATION

- FIGURE 4 CAGR PROJECTIONS

- FIGURE 5 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES IN AIRWAY MANAGEMENT MARKET (2023-2028)

- 2.3 DATA TRIANGULATION APPROACH

- FIGURE 6 DATA TRIANGULATION METHODOLOGY

- 2.4 MARKET SHARE ESTIMATION

- 2.5 STUDY ASSUMPTIONS

- 2.6 RISK ASSESSMENT

- TABLE 2 RISK ASSESSMENT: AIRWAY MANAGEMENT DEVICES MARKET

3 EXECUTIVE SUMMARY

- FIGURE 7 AIRWAY MANAGEMENT DEVICES MARKET, BY TYPE, 2023 VS. 2028 (USD MILLION)

- FIGURE 8 AIRWAY MANAGEMENT DEVICES MARKET FOR INFRAGLOTTIC AIRWAY DEVICES, BY TYPE, 2023 VS. 2028 (USD MILLION)

- FIGURE 9 AIRWAY MANAGEMENT DEVICES MARKET FOR SUPRAGLOTTIC AIRWAY DEVICES, BY TYPE, 2023 VS. 2028 (USD MILLION)

- FIGURE 10 AIRWAY MANAGEMENT DEVICES MARKET FOR LARYNGOSCOPES, BY TYPE, 2023 VS. 2028 (USD MILLION)

- FIGURE 11 AIRWAY MANAGEMENT DEVICES MARKET, BY PATIENT AGE, 2023 VS. 2028 (USD MILLION)

- FIGURE 12 AIRWAY MANAGEMENT DEVICES MARKET, BY APPLICATION, 2023 VS. 2028 (USD MILLION)

- FIGURE 13 AIRWAY MANAGEMENT DEVICES MARKET, BY END USER, 2023 VS. 2028 (USD MILLION)

- FIGURE 14 AIRWAY MANAGEMENT DEVICES MARKET FOR HOSPITALS, BY DEPARTMENT, 2023 VS. 2028 (USD MILLION)

- FIGURE 15 GEOGRAPHICAL ANALYSIS: AIRWAY MANAGEMENT DEVICES MARKET

4 PREMIUM INSIGHTS

- 4.1 AIRWAY MANAGEMENT DEVICES MARKET OVERVIEW

- FIGURE 16 INCREASING CASES OF CHRONIC RESPIRATORY DISEASES AND GROWING DEVELOPMENTS IN HEALTHCARE INFRASTRUCTURE TO DRIVE MARKET

- 4.2 ASIA PACIFIC: AIRWAY MANAGEMENT DEVICES MARKET, BY TYPE

- FIGURE 17 INFRAGLOTTIC AIRWAY DEVICES SEGMENT ACCOUNTED FOR LARGEST SHARE OF ASIA PACIFIC MARKET IN 2022

- 4.3 AIRWAY MANAGEMENT DEVICES MARKET: GEOGRAPHICAL GROWTH OPPORTUNITIES

- FIGURE 18 INDIA TO REGISTER HIGHEST REVENUE GROWTH DURING FORECAST PERIOD

- 4.4 AIRWAY MANAGEMENT DEVICES MARKET, BY REGION (2023-2028)

- FIGURE 19 NORTH AMERICA TO DOMINATE AIRWAY MANAGEMENT DEVICES MARKET DURING STUDY PERIOD

- 4.5 AIRWAY MANAGEMENT DEVICES MARKET: DEVELOPED VS. DEVELOPING MARKETS

- FIGURE 20 DEVELOPING MARKETS TO REGISTER HIGHER GROWTH RATES DURING FORECAST PERIOD

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 21 AIRWAY MANAGEMENT DEVICES MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- TABLE 3 MARKET DYNAMICS: AIRWAY MANAGEMENT DEVICES MARKET

- 5.2.1 DRIVERS

- 5.2.1.1 Increasing prevalence of chronic respiratory diseases

- TABLE 4 POPULATION AGED 65 YEARS AND ABOVE, BY REGION (%)

- 5.2.1.2 Growing demand for emergency and intensive care

- 5.2.1.3 Growing incidence of pre-term births globally

- FIGURE 22 NUMBER OF PRE-TERM BIRTHS (DEVELOPED, LATIN AMERICAN, AND CARIBBEAN COUNTRIES), 1990-2025

- 5.2.1.4 Government support for improving emergency care infrastructure

- 5.2.2 RESTRAINTS

- 5.2.2.1 Lack of reimbursement policies across developing countries

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Growing demand for single-use airway management devices

- 5.2.3.2 Increased growth potential in emerging countries

- TABLE 5 COMPARISON OF SURGERY COSTS: INDIA VS. US

- 5.2.4 CHALLENGES

- 5.2.4.1 Harmful effects of airway management devices on neonatal patients

- 5.2.4.2 Dearth of skilled professionals for airway management procedures

- 5.2.4.3 Increasing pricing pressure on key market players

6 INDUSTRY INSIGHTS

- 6.1 INTRODUCTION

- 6.2 INDUSTRY TRENDS

- 6.2.1 USE OF ECO-FRIENDLY AND BIODEGRADABLE POLYMERS IN AIRWAY MANAGEMENT DEVICE MANUFACTURING

- 6.3 DEMAND SIDE ANALYSIS

- 6.3.1 GROWING ADOPTION OF ADVANCED INTUBATION TUBE HOLDERS

- 6.4 REGULATORY ANALYSIS

- 6.4.1 NORTH AMERICA

- 6.4.1.1 US

- TABLE 6 US: FDA CLASSIFICATION OF AIRWAY MANAGEMENT DEVICES

- TABLE 7 US: REGULATORY PROCESS FOR MEDICAL DEVICES

- 6.4.1.2 Canada

- 6.4.2 EUROPE

- 6.4.3 ASIA PACIFIC

- 6.4.3.1 Japan

- TABLE 8 JAPAN: CLASSIFICATION OF MEDICAL DEVICES AND REVIEWING BODIES

- 6.4.3.2 China

- TABLE 9 NMPA MEDICAL DEVICE CLASSIFICATION

- 6.4.3.3 India

- 6.4.1 NORTH AMERICA

- 6.5 PORTER'S FIVE FORCES ANALYSIS

- TABLE 10 PORTER'S FIVE FORCES ANALYSIS

- 6.5.1 THREAT OF NEW ENTRANTS

- 6.5.2 THREAT OF SUBSTITUTES

- 6.5.3 BARGAINING POWER OF SUPPLIERS

- 6.5.4 BARGAINING POWER OF BUYERS

- 6.5.5 INTENSITY OF COMPETITIVE RIVALRY

- 6.6 VALUE CHAIN ANALYSIS

- FIGURE 23 VALUE CHAIN ANALYSIS OF AIRWAY MANAGEMENT DEVICES MARKET

- 6.7 ECOSYSTEM ANALYSIS

- FIGURE 24 AIRWAY MANAGEMENT DEVICES MARKET: ECOSYSTEM ANALYSIS

- 6.7.1 ROLE IN ECOSYSTEM

- 6.8 PATENT ANALYSIS

- 6.8.1 PATENT PUBLICATION TRENDS FOR AIRWAY MANAGEMENT DEVICES

- FIGURE 25 PATENT PUBLICATION TRENDS (JANUARY 1, 2011- APRIL 4, 2023)

- 6.8.2 JURISDICTION AND TOP APPLICANT ANALYSIS

- FIGURE 26 TOP APPLICANTS AND OWNERS (COMPANIES/INSTITUTIONS) FOR AIRWAY MANAGEMENT DEVICES (JANUARY 1, 2011- APRIL 4, 2023)

- FIGURE 27 TOP APPLICANT COUNTRIES/REGIONS FOR AIRWAY MANAGEMENT DEVICES (JANUARY 1, 2011- APRIL 4, 2023)

7 AIRWAY MANAGEMENT DEVICES MARKET, BY TYPE

- 7.1 INTRODUCTION

- TABLE 11 AIRWAY MANAGEMENT DEVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- 7.2 INFRAGLOTTIC AIRWAY DEVICES

- TABLE 12 AIRWAY MANAGEMENT DEVICES MARKET FOR INFRAGLOTTIC AIRWAY DEVICES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 13 AIRWAY MANAGEMENT DEVICES MARKET FOR INFRAGLOTTIC AIRWAY DEVICES, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 14 AIRWAY MANAGEMENT DEVICES MARKET FOR INFRAGLOTTIC AIRWAY DEVICES, BY REGION, 2021-2028 (MILLION UNITS)

- 7.2.1 ENDOTRACHEAL TUBES

- 7.2.1.1 Endotracheal tubes to be most useful devices for airway management

- TABLE 15 ENDOTRACHEAL TUBES OFFERED BY KEY MARKET PLAYERS

- TABLE 16 ENDOTRACHEAL TUBES MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 17 ENDOTRACHEAL TUBES MARKET, BY REGION, 2021-2028 (MILLION UNITS)

- 7.2.2 TRACHEOSTOMY TUBES

- 7.2.2.1 Increased use in ICUs to ensure high adoption of tracheostomy tubes

- TABLE 18 TRACHEOSTOMY TUBES OFFERED BY KEY MARKET PLAYERS

- TABLE 19 TRACHEOSTOMY TUBES MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 20 TRACHEOSTOMY TUBES MARKET, BY REGION, 2021-2028 (MILLION UNITS)

- 7.3 SUPRAGLOTTIC AIRWAY DEVICES

- TABLE 21 AIRWAY MANAGEMENT DEVICES MARKET FOR SUPRAGLOTTIC AIRWAY DEVICES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 22 AIRWAY MANAGEMENT DEVICES MARKET FOR SUPRAGLOTTIC AIRWAY DEVICES, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 23 AIRWAY MANAGEMENT DEVICES MARKET FOR SUPRAGLOTTIC AIRWAY MANAGEMENT DEVICES, BY REGION, 2021-2028 (MILLION UNITS)

- 7.3.1 LARYNGEAL MASK AIRWAY DEVICES

- 7.3.1.1 Laryngeal mask airway devices to hold largest market share during forecast period

- TABLE 24 LARYNGEAL MASK AIRWAY DEVICES OFFERED BY KEY MARKET PLAYERS

- TABLE 25 LARYNGEAL MASK AIRWAY DEVICES MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 26 LARYNGEAL MASK AIRWAY DEVICES MARKET, BY REGION, 2021-2028 (MILLION UNITS)

- 7.3.2 OROPHARYNGEAL AIRWAY DEVICES

- 7.3.2.1 Oropharyngeal airway devices to be used in unconscious or unresponsive patients

- TABLE 27 OROPHARYNGEAL AIRWAY DEVICES OFFERED BY KEY MARKET PLAYERS

- TABLE 28 OROPHARYNGEAL AIRWAY DEVICES MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 29 OROPHARYNGEAL AIRWAY DEVICES MARKET, BY REGION, 2021-2028 (MILLION UNITS)

- 7.3.3 NASOPHARYNGEAL AIRWAY DEVICES

- 7.3.3.1 Easy and effective stimulation of gag reflex to propel segment

- TABLE 30 NASOPHARYNGEAL AIRWAY DEVICES OFFERED BY KEY MARKET PLAYERS

- TABLE 31 NASOPHARYNGEAL AIRWAY DEVICES MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 32 NASOPHARYNGEAL AIRWAY DEVICES MARKET, BY REGION, 2021-2028 (MILLION UNITS)

- 7.3.4 OTHER SUPRAGLOTTIC AIRWAY DEVICES

- TABLE 33 OTHER SUPRAGLOTTIC AIRWAY DEVICES OFFERED BY KEY MARKET PLAYERS

- TABLE 34 OTHER SUPRAGLOTTIC AIRWAY DEVICES MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 35 OTHER SUPRAGLOTTIC AIRWAY DEVICES MARKET, BY REGION, 2021-2028 (MILLION UNITS)

- 7.4 LARYNGOSCOPES

- TABLE 36 AIRWAY MANAGEMENT DEVICES MARKET FOR LARYNGOSCOPES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 37 AIRWAY MANAGEMENT DEVICES MARKET FOR LARYNGOSCOPES MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 38 AIRWAY MANAGEMENT DEVICES MARKET FOR LARYNGOSCOPES MARKET, BY REGION, 2021-2028 (MILLION UNITS)

- 7.4.1 CONVENTIONAL LARYNGOSCOPES

- 7.4.1.1 Low prices and long history of use to drive segment

- TABLE 39 CONVENTIONAL LARYNGOSCOPES OFFERED BY KEY MARKET PLAYERS

- TABLE 40 CONVENTIONAL LARYNGOSCOPES MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 41 CONVENTIONAL LARYNGOSCOPES MARKET, BY REGION, 2021-2028 (MILLION UNITS)

- 7.4.2 VIDEO LARYNGOSCOPES

- 7.4.2.1 High prices of video laryngoscopes to hinder access in developing countries

- TABLE 42 VIDEO LARYNGOSCOPES OFFERED BY KEY MARKET PLAYERS

- TABLE 43 VIDEO LARYNGOSCOPES MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 44 VIDEO LARYNGOSCOPES MARKET, BY REGION, 2021-2028 (MILLION UNITS)

- 7.5 RESUSCITATORS

- 7.5.1 RESUSCITATORS TO BE PREFERRED FOR PEDIATRIC PATIENTS/NEONATES

- TABLE 45 RESUSCITATORS OFFERED BY KEY MARKET PLAYERS

- TABLE 46 AIRWAY MANAGEMENT DEVICES MARKET FOR RESUSCITATORS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 47 AIRWAY MANAGEMENT DEVICES MARKET FOR RESUSCITATORS, BY REGION, 2021-2028 (MILLION UNITS)

- 7.6 CRICOTHYROTOMY KITS

- 7.6.1 RISING NUMBER OF TRAFFIC ACCIDENTS AND RELATED HEAD AND NECK INJURIES TO PROPEL MARKET

- TABLE 48 CRICOTHYROTOMY KITS OFFERED BY KEY MARKET PLAYERS

- TABLE 49 AIRWAY MANAGEMENT DEVICES MARKET FOR CRICOTHYROTOMY KITS, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 50 AIRWAY MANAGEMENT DEVICES MARKET FOR CRICOTHYROTOMY KITS, BY REGION, 2021-2028 (MILLION UNITS)

- 7.7 OTHER AIRWAY MANAGEMENT DEVICES

- TABLE 51 OTHER AIRWAY MANAGEMENT DEVICES OFFERED BY KEY MARKET PLAYERS

- TABLE 52 AIRWAY MANAGEMENT DEVICES MARKET FOR OTHER AIRWAY MANAGEMENT DEVICES, BY COUNTRY, 2021-2028 (USD MILLION)

8 AIRWAY MANAGEMENT DEVICES MARKET, BY PATIENT AGE

- 8.1 INTRODUCTION

- TABLE 53 AIRWAY MANAGEMENT DEVICES MARKET, BY PATIENT AGE, 2021-2028 (USD MILLION)

- 8.2 ADULT PATIENTS

- 8.2.1 ADULTS PATIENTS TO HOLD LARGEST SHARE OF AIRWAY MANAGEMENT DEVICES MARKET DURING STUDY PERIOD

- FIGURE 28 AGE-ADJUSTED PREVALENCE OF COPD (2011-2020)

- TABLE 54 AIRWAY MANAGEMENT DEVICES MARKET FOR ADULT PATIENTS, BY COUNTRY, 2021-2028 (USD MILLION)

- 8.3 PEDIATRIC PATIENTS/NEONATES

- 8.3.1 AGE-RELATED DIFFERENCES IN ANATOMY AND PHYSIOLOGY TO HINDER AIRWAY MANAGEMENT

- TABLE 55 AIRWAY MANAGEMENT DEVICES MARKET FOR PEDIATRIC PATIENTS/NEONATES, BY COUNTRY, 2021-2028 (USD MILLION)

9 AIRWAY MANAGEMENT DEVICES MARKET, BY APPLICATION

- 9.1 INTRODUCTION

- TABLE 56 AIRWAY MANAGEMENT DEVICES MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- 9.2 ANESTHESIA

- 9.2.1 ANESTHESIA TO HOLD LARGEST SHARE OF AIRWAY MANAGEMENT DEVICES APPLICATIONS MARKET DURING STUDY PERIOD

- TABLE 57 AIRWAY MANAGEMENT DEVICES MARKET FOR ANESTHESIA, BY COUNTRY, 2021-2028 (USD MILLION)

- 9.3 EMERGENCY MEDICINE

- 9.3.1 RESUSCITATORS AND SUPRAGLOTTIC AIRWAY MANAGEMENT DEVICES TO BE USED IN INITIAL PHASES OF EMERGENCY CARE

- TABLE 58 AIRWAY MANAGEMENT DEVICES MARKET FOR EMERGENCY MEDICINE, BY COUNTRY, 2021-2028 (USD MILLION)

- 9.4 OTHER APPLICATIONS

- TABLE 59 AIRWAY MANAGEMENT DEVICES MARKET FOR OTHER APPLICATIONS, BY COUNTRY, 2021-2028 (USD MILLION)

10 AIRWAY MANAGEMENT DEVICES MARKET, BY END USER

- 10.1 INTRODUCTION

- TABLE 60 AIRWAY MANAGEMENT DEVICES MARKET, BY END USER, 2021-2028 (USD MILLION)

- 10.2 HOSPITALS

- TABLE 61 AIRWAY MANAGEMENT DEVICES MARKET FOR HOSPITALS, BY DEPARTMENT, 2021-2028 (USD MILLION)

- TABLE 62 AIRWAY MANAGEMENT DEVICES MARKET FOR HOSPITALS, BY COUNTRY, 2021-2028 (USD MILLION)

- 10.2.1 OPERATING ROOMS

- 10.2.1.1 Rising number of surgeries to drive demand for airway management devices in operating rooms

- TABLE 63 US: INCREASE IN NUMBER OF SURGICAL PROCEDURES PERFORMED

- TABLE 64 OPERATING ROOMS MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- 10.2.2 EMERGENCY CARE DEPARTMENTS

- 10.2.2.1 Increased number of emergencies and trauma care patients to propel market

- TABLE 65 EMERGENCY CARE DEPARTMENTS MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- 10.2.3 INTENSIVE CARE UNITS

- 10.2.3.1 Rising disease prevalence and growing need for monitoring to fuel segment

- TABLE 66 INTENSIVE CARE UNITS MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- 10.3 AMBULATORY CARE CENTERS

- 10.3.1 HIGH COSTS IN HOSPITAL OUTPATIENT DEPARTMENTS TO INCREASE FOCUS ON AMBULATORY CARE

- TABLE 67 AIRWAY MANAGEMENT DEVICES MARKET FOR AMBULATORY CARE CENTERS, BY COUNTRY, 2021-2028 (USD MILLION)

- 10.4 HOME CARE SETTINGS

- 10.4.1 RISING AWARENESS AND ACCEPTANCE OF HOME CARE TO BOOST MARKET

- TABLE 68 AIRWAY MANAGEMENT DEVICES MARKET FOR HOME CARE SETTINGS, BY COUNTRY, 2021-2028 (USD MILLION)

- 10.5 OTHER END USERS

- TABLE 69 AIRWAY MANAGEMENT DEVICES MARKET FOR OTHER END USERS, BY COUNTRY, 2021-2028 (USD MILLION)

11 AIRWAY MANAGEMENT DEVICES MARKET, BY REGION

- 11.1 INTRODUCTION

- FIGURE 29 AIRWAY MANAGEMENT DEVICES MARKET: GEOGRAPHICAL SNAPSHOT (2022)

- TABLE 70 AIRWAY MANAGEMENT MARKET, BY REGION, 2021-2028 (USD MILLION)

- 11.2 NORTH AMERICA

- 11.2.1 NORTH AMERICA: IMPACT OF ECONOMIC RECESSION

- FIGURE 30 NORTH AMERICA: AIRWAY MANAGEMENT DEVICES MARKET SNAPSHOT

- TABLE 71 NORTH AMERICA: AIRWAY MANAGEMENT DEVICES MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 72 NORTH AMERICA: AIRWAY MANAGEMENT DEVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 73 NORTH AMERICA: AIRWAY MANAGEMENT DEVICES MARKET FOR INFRAGLOTTIC AIRWAY DEVICES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 74 NORTH AMERICA: AIRWAY MANAGEMENT DEVICES MARKET FOR SUPRAGLOTTIC AIRWAY DEVICES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 75 NORTH AMERICA: AIRWAY MANAGEMENT DEVICES MARKET FOR LARYNGOSCOPES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 76 NORTH AMERICA: AIRWAY MANAGEMENT DEVICES MARKET, BY PATIENT AGE, 2021-2028 (USD MILLION)

- TABLE 77 NORTH AMERICA: AIRWAY MANAGEMENT DEVICES MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 78 NORTH AMERICA: AIRWAY MANAGEMENT DEVICES MARKET, BY END USER, 2021-2028 (USD MILLION)

- TABLE 79 NORTH AMERICA: AIRWAY MANAGEMENT DEVICES MARKET FOR HOSPITALS, BY DEPARTMENT, 2021-2028 (USD MILLION)

- 11.2.2 US

- 11.2.2.1 US to dominate North American airway management devices market during forecast period

- TABLE 80 US: AIRWAY MANAGEMENT DEVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 81 US: AIRWAY MANAGEMENT DEVICES MARKET FOR INFRAGLOTTIC AIRWAY DEVICES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 82 US: AIRWAY MANAGEMENT DEVICES MARKET FOR SUPRAGLOTTIC AIRWAY DEVICES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 83 US: AIRWAY MANAGEMENT DEVICES MARKET FOR LARYNGOSCOPES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 84 US: AIRWAY MANAGEMENT DEVICES MARKET, BY PATIENT AGE, 2021-2028 (USD MILLION)

- TABLE 85 US: AIRWAY MANAGEMENT DEVICES MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 86 US: AIRWAY MANAGEMENT DEVICES MARKET, BY END USER, 2021-2028 (USD MILLION)

- TABLE 87 US: AIRWAY MANAGEMENT DEVICES MARKET FOR HOSPITALS, BY DEPARTMENT, 2021-2028 (USD MILLION)

- 11.2.3 CANADA

- 11.2.3.1 Growing government focus on local manufacturing of medical devices to propel market

- TABLE 88 CANADA: AIRWAY MANAGEMENT DEVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 89 CANADA: AIRWAY MANAGEMENT DEVICES MARKET FOR INFRAGLOTTIC AIRWAY DEVICES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 90 CANADA: AIRWAY MANAGEMENT DEVICES MARKET FOR SUPRAGLOTTIC AIRWAY DEVICES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 91 CANADA: AIRWAY MANAGEMENT DEVICES MARKET FOR LARYNGOSCOPES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 92 CANADA: AIRWAY MANAGEMENT DEVICES MARKET, BY PATIENT AGE, 2021-2028 (USD MILLION)

- TABLE 93 CANADA: AIRWAY MANAGEMENT DEVICES MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 94 CANADA: AIRWAY MANAGEMENT DEVICES MARKET, BY END USER, 2021-2028 (USD MILLION)

- TABLE 95 CANADA: AIRWAY MANAGEMENT DEVICES MARKET FOR HOSPITALS, BY DEPARTMENT, 2021-2028 (USD MILLION)

- 11.3 EUROPE

- 11.3.1 EUROPE: IMPACT OF ECONOMIC RECESSION

- FIGURE 31 EUROPE: AIRWAY MANAGEMENT DEVICES MARKET SNAPSHOT

- TABLE 96 EUROPE: AIRWAY MANAGEMENT DEVICES MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 97 EUROPE: AIRWAY MANAGEMENT DEVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 98 EUROPE: AIRWAY MANAGEMENT DEVICES MARKET FOR INFRAGLOTTIC AIRWAY DEVICES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 99 EUROPE: AIRWAY MANAGEMENT DEVICES MARKET FOR SUPRAGLOTTIC AIRWAY DEVICES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 100 EUROPE: AIRWAY MANAGEMENT DEVICES MARKET FOR LARYNGOSCOPES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 101 EUROPE: AIRWAY MANAGEMENT DEVICES MARKET, BY PATIENT AGE, 2021-2028 (USD MILLION)

- TABLE 102 EUROPE: AIRWAY MANAGEMENT DEVICES MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 103 EUROPE: AIRWAY MANAGEMENT DEVICES MARKET, BY END USER, 2021-2028 (USD MILLION)

- TABLE 104 EUROPE: AIRWAY MANAGEMENT DEVICES MARKET FOR HOSPITALS, BY DEPARTMENT, 2021-2028 (USD MILLION)

- 11.3.2 GERMANY

- 11.3.2.1 Germany dominated European airway management devices market in 2022

- TABLE 105 GERMANY: AIRWAY MANAGEMENT DEVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 106 GERMANY: AIRWAY MANAGEMENT DEVICES MARKET FOR INFRAGLOTTIC AIRWAY DEVICES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 107 GERMANY: AIRWAY MANAGEMENT DEVICES MARKET FOR SUPRAGLOTTIC AIRWAY DEVICES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 108 GERMANY: AIRWAY MANAGEMENT DEVICES MARKET FOR LARYNGOSCOPES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 109 GERMANY: AIRWAY MANAGEMENT DEVICES MARKET, BY PATIENT AGE, 2021-2028 (USD MILLION)

- TABLE 110 GERMANY: AIRWAY MANAGEMENT DEVICES MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 111 GERMANY: AIRWAY MANAGEMENT DEVICES MARKET, BY END USER, 2021-2028 (USD MILLION)

- TABLE 112 GERMANY: AIRWAY MANAGEMENT DEVICES MARKET FOR HOSPITALS, BY DEPARTMENT, 2021-2028 (USD MILLION)

- 11.3.3 FRANCE

- 11.3.3.1 Presence of advanced and well-established healthcare system to fuel market

- TABLE 113 FRANCE: AIRWAY MANAGEMENT DEVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 114 FRANCE: AIRWAY MANAGEMENT DEVICES MARKET FOR INFRAGLOTTIC AIRWAY DEVICES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 115 FRANCE: AIRWAY MANAGEMENT DEVICES MARKET FOR SUPRAGLOTTIC AIRWAY DEVICES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 116 FRANCE: AIRWAY MANAGEMENT DEVICES MARKET FOR LARYNGOSCOPES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 117 FRANCE: AIRWAY MANAGEMENT DEVICES MARKET, BY PATIENT AGE, 2021-2028 (USD MILLION)

- TABLE 118 FRANCE: AIRWAY MANAGEMENT DEVICES MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 119 FRANCE: AIRWAY MANAGEMENT DEVICES MARKET, BY END USER, 2021-2028 (USD MILLION)

- TABLE 120 FRANCE: AIRWAY MANAGEMENT DEVICES MARKET FOR HOSPITALS, BY DEPARTMENT, 2021-2028 (USD MILLION)

- 11.3.4 UK

- 11.3.4.1 High prevalence of respiratory disorders to drive demand for airway management devices in healthcare settings

- TABLE 121 UK: AIRWAY MANAGEMENT DEVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 122 UK: AIRWAY MANAGEMENT DEVICES MARKET FOR INFRAGLOTTIC AIRWAY DEVICES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 123 UK: AIRWAY MANAGEMENT DEVICES MARKET FOR SUPRAGLOTTIC AIRWAY DEVICES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 124 UK: AIRWAY MANAGEMENT DEVICES MARKET FOR LARYNGOSCOPES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 125 UK: AIRWAY MANAGEMENT DEVICES MARKET, BY PATIENT AGE, 2021-2028 (USD MILLION)

- TABLE 126 UK: AIRWAY MANAGEMENT DEVICES MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 127 UK: AIRWAY MANAGEMENT DEVICES MARKET, BY END USER, 2021-2028 (USD MILLION)

- TABLE 128 UK: AIRWAY MANAGEMENT DEVICES MARKET FOR HOSPITALS, BY DEPARTMENT, 2021-2028 (USD MILLION)

- 11.3.5 ITALY

- 11.3.5.1 Rising surgical volumes to augment demand for general anesthesia and airway management

- TABLE 129 ITALY: AIRWAY MANAGEMENT DEVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 130 ITALY: AIRWAY MANAGEMENT DEVICES MARKET FOR INFRAGLOTTIC AIRWAY DEVICES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 131 ITALY: AIRWAY MANAGEMENT DEVICES MARKET FOR SUPRAGLOTTIC AIRWAY DEVICES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 132 ITALY: AIRWAY MANAGEMENT DEVICES MARKET FOR LARYNGOSCOPES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 133 ITALY: AIRWAY MANAGEMENT DEVICES MARKET, BY PATIENT AGE, 2021-2028 (USD MILLION)

- TABLE 134 ITALY: AIRWAY MANAGEMENT DEVICES MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 135 ITALY: AIRWAY MANAGEMENT DEVICES MARKET, BY END USER, 2021-2028 (USD MILLION)

- TABLE 136 ITALY: AIRWAY MANAGEMENT DEVICES MARKET FOR HOSPITALS, BY DEPARTMENT, 2021-2028 (USD MILLION)

- 11.3.6 SPAIN

- 11.3.6.1 Aging population and increasing prevalence of respiratory diseases to aid market

- TABLE 137 SPAIN: AIRWAY MANAGEMENT DEVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 138 SPAIN: AIRWAY MANAGEMENT DEVICES MARKET FOR INFRAGLOTTIC AIRWAY DEVICES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 139 SPAIN: AIRWAY MANAGEMENT DEVICES MARKET FOR SUPRAGLOTTIC AIRWAY DEVICES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 140 SPAIN: AIRWAY MANAGEMENT DEVICES MARKET FOR LARYNGOSCOPES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 141 SPAIN: AIRWAY MANAGEMENT DEVICES MARKET, BY PATIENT AGE, 2021-2028 (USD MILLION)

- TABLE 142 SPAIN: AIRWAY MANAGEMENT DEVICES MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 143 SPAIN: AIRWAY MANAGEMENT DEVICES MARKET, BY END USER, 2021-2028 (USD MILLION)

- TABLE 144 SPAIN: AIRWAY MANAGEMENT DEVICES MARKET FOR HOSPITALS, BY DEPARTMENT, 2021-2028 (USD MILLION)

- 11.3.7 REST OF EUROPE

- TABLE 145 REST OF EUROPE: AIRWAY MANAGEMENT DEVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 146 REST OF EUROPE: AIRWAY MANAGEMENT DEVICES MARKET FOR INFRAGLOTTIC AIRWAY DEVICES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 147 REST OF EUROPE: AIRWAY MANAGEMENT DEVICES MARKET FOR SUPRAGLOTTIC AIRWAY DEVICES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 148 REST OF EUROPE: AIRWAY MANAGEMENT DEVICES MARKET FOR LARYNGOSCOPES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 149 REST OF EUROPE: AIRWAY MANAGEMENT DEVICES MARKET, BY PATIENT AGE, 2021-2028 (USD MILLION)

- TABLE 150 REST OF EUROPE: AIRWAY MANAGEMENT DEVICES MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 151 REST OF EUROPE: AIRWAY MANAGEMENT DEVICES MARKET, BY END USER, 2021-2028 (USD MILLION)

- TABLE 152 REST OF EUROPE: AIRWAY MANAGEMENT DEVICES MARKET FOR HOSPITALS, BY DEPARTMENT, 2021-2028 (USD MILLION)

- 11.4 ASIA PACIFIC

- 11.4.1 ASIA PACIFIC: IMPACT OF ECONOMIC RECESSION

- FIGURE 32 ASIA PACIFIC: AIRWAY MANAGEMENT DEVICES MARKET SNAPSHOT

- TABLE 153 ASIA PACIFIC: AIRWAY MANAGEMENT DEVICES MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 154 ASIA PACIFIC: AIRWAY MANAGEMENT DEVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 155 ASIA PACIFIC: AIRWAY MANAGEMENT DEVICES MARKET FOR INFRAGLOTTIC AIRWAY DEVICES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 156 ASIA PACIFIC: AIRWAY MANAGEMENT DEVICES MARKET FOR SUPRAGLOTTIC AIRWAY DEVICES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 157 ASIA PACIFIC: AIRWAY MANAGEMENT DEVICES MARKET FOR LARYNGOSCOPES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 158 ASIA PACIFIC: AIRWAY MANAGEMENT DEVICES MARKET, BY PATIENT AGE, 2021-2028 (USD MILLION)

- TABLE 159 ASIA PACIFIC: AIRWAY MANAGEMENT DEVICES MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 160 ASIA PACIFIC: AIRWAY MANAGEMENT DEVICES MARKET, BY END USER, 2021-2028 (USD MILLION)

- TABLE 161 ASIA PACIFIC: AIRWAY MANAGEMENT DEVICES MARKET FOR HOSPITALS, BY DEPARTMENT, 2021-2028 (USD MILLION)

- 11.4.2 JAPAN

- 11.4.2.1 Strong healthcare system and favorable reimbursement policies to support market

- TABLE 162 JAPAN: AIRWAY MANAGEMENT DEVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 163 JAPAN: AIRWAY MANAGEMENT DEVICES MARKET FOR INFRAGLOTTIC AIRWAY DEVICES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 164 JAPAN: AIRWAY MANAGEMENT DEVICES MARKET FOR SUPRAGLOTTIC AIRWAY DEVICES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 165 JAPAN: AIRWAY MANAGEMENT DEVICES MARKET FOR LARYNGOSCOPES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 166 JAPAN: AIRWAY MANAGEMENT DEVICES MARKET, BY PATIENT AGE, 2021-2028 (USD MILLION)

- TABLE 167 JAPAN: AIRWAY MANAGEMENT DEVICES MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 168 JAPAN: AIRWAY MANAGEMENT DEVICES MARKET, BY END USER, 2021-2028 (USD MILLION)

- TABLE 169 JAPAN: AIRWAY MANAGEMENT DEVICES MARKET FOR HOSPITALS, BY DEPARTMENT, 2021-2028 (USD MILLION)

- 11.4.3 CHINA

- 11.4.3.1 Growing number of healthcare facilities and policy reforms to stimulate market

- TABLE 170 CHINA: AIRWAY MANAGEMENT DEVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 171 CHINA: AIRWAY MANAGEMENT DEVICES MARKET FOR INFRAGLOTTIC AIRWAY DEVICES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 172 CHINA: AIRWAY MANAGEMENT DEVICES MARKET FOR SUPRAGLOTTIC AIRWAY DEVICES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 173 CHINA: AIRWAY MANAGEMENT DEVICES MARKET FOR LARYNGOSCOPES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 174 CHINA: AIRWAY MANAGEMENT DEVICES MARKET, BY PATIENT AGE, 2021-2028 (USD MILLION)

- TABLE 175 CHINA: AIRWAY MANAGEMENT DEVICES MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 176 CHINA: AIRWAY MANAGEMENT DEVICES MARKET, BY END USER, 2021-2028 (USD MILLION)

- TABLE 177 CHINA: AIRWAY MANAGEMENT DEVICES MARKET FOR HOSPITALS, BY DEPARTMENT, 2021-2028 (USD MILLION)

- 11.4.4 INDIA

- 11.4.4.1 Increasing prevalence of respiratory diseases and pre-term births to drive demand for airway management devices

- TABLE 178 INDIA: AIRWAY MANAGEMENT DEVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 179 INDIA: AIRWAY MANAGEMENT DEVICES MARKET FOR INFRAGLOTTIC AIRWAY DEVICES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 180 INDIA: AIRWAY MANAGEMENT DEVICES MARKET FOR SUPRAGLOTTIC AIRWAY DEVICES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 181 INDIA: AIRWAY MANAGEMENT DEVICES MARKET FOR LARYNGOSCOPES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 182 INDIA: AIRWAY MANAGEMENT DEVICES MARKET, BY PATIENT AGE, 2021-2028 (USD MILLION)

- TABLE 183 INDIA: AIRWAY MANAGEMENT DEVICES MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 184 INDIA: AIRWAY MANAGEMENT DEVICES MARKET, BY END USER, 2021-2028 (USD MILLION)

- TABLE 185 INDIA: AIRWAY MANAGEMENT DEVICES MARKET FOR HOSPITALS, BY DEPARTMENT, 2021-2028 (USD MILLION)

- 11.4.5 REST OF ASIA PACIFIC

- TABLE 186 REST OF ASIA PACIFIC: AIRWAY MANAGEMENT DEVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 187 REST OF ASIA PACIFIC: AIRWAY MANAGEMENT DEVICES MARKET FOR INFRAGLOTTIC AIRWAY DEVICES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 188 REST OF ASIA PACIFIC: AIRWAY MANAGEMENT DEVICES MARKET FOR SUPRAGLOTTIC AIRWAY DEVICES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 189 REST OF ASIA PACIFIC: AIRWAY MANAGEMENT DEVICES MARKET FOR LARYNGOSCOPES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 190 REST OF ASIA PACIFIC: AIRWAY MANAGEMENT DEVICES MARKET, BY PATIENT AGE, 2021-2028 (USD MILLION)

- TABLE 191 REST OF ASIA PACIFIC: AIRWAY MANAGEMENT DEVICES MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 192 REST OF ASIA PACIFIC: AIRWAY MANAGEMENT DEVICES MARKET, BY END USER, 2021-2028 (USD MILLION)

- TABLE 193 REST OF ASIA PACIFIC: AIRWAY MANAGEMENT DEVICES MARKET FOR HOSPITALS, BY DEPARTMENT, 2021-2028 (USD MILLION)

- 11.5 LATIN AMERICA

- 11.5.1 FAVORABLE REIMBURSEMENT SCENARIOS AND HEALTHCARE DEVELOPMENT INITIATIVES TO BOOST MARKET

- 11.5.2 LATIN AMERICA: IMPACT OF ECONOMIC RECESSION

- TABLE 194 LATIN AMERICA: AIRWAY MANAGEMENT DEVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 195 LATIN AMERICA: AIRWAY MANAGEMENT DEVICES MARKET FOR INFRAGLOTTIC AIRWAY DEVICES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 196 LATIN AMERICA: AIRWAY MANAGEMENT DEVICES MARKET FOR SUPRAGLOTTIC AIRWAY DEVICES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 197 LATIN AMERICA: AIRWAY MANAGEMENT DEVICES MARKET FOR LARYNGOSCOPES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 198 LATIN AMERICA: AIRWAY MANAGEMENT DEVICES MARKET, BY PATIENT AGE, 2021-2028 (USD MILLION)

- TABLE 199 LATIN AMERICA: AIRWAY MANAGEMENT DEVICES MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 200 LATIN AMERICA: AIRWAY MANAGEMENT DEVICES MARKET, BY END USER, 2021-2028 (USD MILLION)

- TABLE 201 LATIN AMERICA: AIRWAY MANAGEMENT DEVICES MARKET FOR HOSPITALS, BY DEPARTMENT, 2021-2028 (USD MILLION)

- 11.6 MIDDLE EAST & AFRICA

- 11.6.1 IMPROVING HEALTH INFRASTRUCTURE AND MANDATORY HEALTH INSURANCE TO SUPPORT MARKET

- 11.6.2 MIDDLE EAST & AFRICA: IMPACT OF ECONOMIC RECESSION

- TABLE 202 MIDDLE EAST & AFRICA: AIRWAY MANAGEMENT DEVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 203 MIDDLE EAST & AFRICA: AIRWAY MANAGEMENT DEVICES MARKET FOR INFRAGLOTTIC AIRWAY DEVICES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 204 MIDDLE EAST & AFRICA: AIRWAY MANAGEMENT DEVICES MARKET FOR SUPRAGLOTTIC AIRWAY DEVICES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 205 MIDDLE EAST & AFRICA: AIRWAY MANAGEMENT DEVICES MARKET FOR LARYNGOSCOPES, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 206 MIDDLE EAST & AFRICA: AIRWAY MANAGEMENT DEVICES MARKET, BY PATIENT AGE, 2021-2028 (USD MILLION)

- TABLE 207 MIDDLE EAST & AFRICA: AIRWAY MANAGEMENT DEVICES MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 208 MIDDLE EAST & AFRICA: AIRWAY MANAGEMENT DEVICES MARKET, BY END USER, 2021-2028 (USD MILLION)

- TABLE 209 MIDDLE EAST & AFRICA: AIRWAY MANAGEMENT DEVICES MARKET FOR HOSPITALS, BY DEPARTMENT, 2021-2028 (USD MILLION)

12 COMPETITIVE LANDSCAPE

- 12.1 OVERVIEW

- 12.2 STRATEGIES ADOPTED BY KEY PLAYERS

- 12.3 KEY STRATEGIES ADOPTED BY MAJOR PLAYERS IN AIRWAY MANAGEMENT DEVICES MARKET

- 12.4 REVENUE SHARE ANALYSIS OF TOP MARKET PLAYERS

- FIGURE 33 REVENUE ANALYSIS OF TOP PLAYERS IN AIRWAY MANAGEMENT DEVICES MARKET

- 12.5 MARKET SHARE ANALYSIS

- FIGURE 34 AIRWAY MANAGEMENT DEVICES MARKET SHARE, BY KEY PLAYER, 2022

- 12.6 COMPANY EVALUATION QUADRANT

- 12.6.1 STARS

- 12.6.2 EMERGING LEADERS

- 12.6.3 PERVASIVE PLAYERS

- 12.6.4 PARTICIPANTS

- FIGURE 35 AIRWAY MANAGEMENT DEVICES MARKET: COMPANY EVALUATION QUADRANT (2022)

- 12.7 COMPANY EVALUATION QUADRANT FOR START-UPS/SMES

- 12.7.1 PROGRESSIVE COMPANIES

- 12.7.2 DYNAMIC COMPANIES

- 12.7.3 STARTING BLOCKS

- 12.7.4 RESPONSIVE COMPANIES

- FIGURE 36 AIRWAY MANAGEMENT DEVICES MARKET: COMPANY EVALUATION QUADRANT FOR START-UPS/SMES (2022)

- 12.8 COMPANY PRODUCT FOOTPRINT

- 12.8.1 TYPE FOOTPRINT

- TABLE 210 AIRWAY MANAGEMENT DEVICES MARKET: TYPE FOOTPRINT

- 12.8.2 END USER FOOTPRINT

- TABLE 211 AIRWAY MANAGEMENT DEVICES MARKET: END USER FOOTPRINT

- 12.8.3 REGIONAL FOOTPRINT

- TABLE 212 AIRWAY MANAGEMENT DEVICES MARKET: REGIONAL FOOTPRINT

- 12.9 COMPETITIVE SCENARIO

- 12.9.1 KEY PRODUCT LAUNCHES AND APPROVALS

- TABLE 213 KEY PRODUCT LAUNCHES AND APPROVALS, JANUARY 2019-APRIL 2023

- 12.9.2 KEY DEALS

- TABLE 214 KEY DEALS, JANUARY 2019-APRIL 2023

- 12.9.3 OTHER KEY DEVELOPMENTS

- TABLE 215 OTHER KEY DEVELOPMENTS, JANUARY 2019-APRIL 2023

13 COMPANY PROFILES

- 13.1 KEY PLAYERS

(Business Overview, Products Offered, Recent Developments, and MnM View (Key strengths/Right to Win, Strategic Choices Made, and Weaknesses and Competitive Threats))**

- 13.1.1 MEDTRONIC

- TABLE 216 MEDTRONIC: COMPANY OVERVIEW

- FIGURE 37 MEDTRONIC: COMPANY SNAPSHOT (2022)

- 13.1.2 ICU MEDICAL, INC.

- TABLE 217 ICU MEDICAL, INC.: COMPANY OVERVIEW

- FIGURE 38 ICU MEDICAL, INC.: COMPANY SNAPSHOT (2022)

- 13.1.3 TELEFLEX INCORPORATED

- TABLE 218 TELEFLEX INCORPORATED: COMPANY OVERVIEW

- FIGURE 39 TELEFLEX INCORPORATED: COMPANY SNAPSHOT (2022)

- 13.1.4 AMBU A/S

- TABLE 219 AMBU A/S: COMPANY OVERVIEW

- FIGURE 40 AMBU A/S: COMPANY SNAPSHOT (2022)

- 13.1.5 CONVATEC GROUP PLC

- TABLE 220 CONVATEC GROUP PLC: COMPANY OVERVIEW

- FIGURE 41 CONVATEC GROUP PLC: COMPANY SNAPSHOT (2022)

- 13.1.6 KARL STORZ SE & CO. KG

- TABLE 221 KARL STORZ SE & CO. KG: COMPANY OVERVIEW

- 13.1.7 FLEXICARE (GROUP) LIMITED

- TABLE 222 FLEXICARE (GROUP) LIMITED: COMPANY OVERVIEW

- 13.1.8 INTERSURGICAL LTD.

- TABLE 223 INTERSURGICAL LTD.: COMPANY OVERVIEW

- 13.1.9 SUNMED LLC

- TABLE 224 SUNMED LLC: COMPANY OVERVIEW

- 13.1.10 VYAIRE

- TABLE 225 VYAIRE: COMPANY OVERVIEW

- 13.1.11 VBM MEDIZINTECHNIK GMBH

- TABLE 226 VBM MEDIZINTECHNIK GMBH: COMPANY OVERVIEW

- 13.1.12 VERATHON INC.

- TABLE 227 VERATHON INC.: COMPANY OVERVIEW

- FIGURE 42 ROPER TECHNOLOGIES: COMPANY SNAPSHOT (2022)

- 13.1.13 SOURCEMARK

- TABLE 228 SOURCEMARK: COMPANY OVERVIEW

- 13.1.14 MERCURY ENTERPRISES

- TABLE 229 MERCURY ENTERPRISES: COMPANY OVERVIEW

- 13.1.15 ATOS MEDICAL

- TABLE 230 ATOS MEDICAL: COMPANY OVERVIEW

- FIGURE 43 COLOPLAST GROUP: COMPANY SNAPSHOT (2022)

- 13.1.16 P3 MEDICAL

- TABLE 231 P3 MEDICAL: COMPANY OVERVIEW

- 13.1.17 HENAN TUOREN MEDICAL DEVICE CO., LTD.

- TABLE 232 HENAN TUOREN MEDICAL DEVICE CO., LTD: COMPANY OVERVIEW

- 13.1.18 MEDEREN NEOTECH LTD.

- TABLE 233 MEDEREN NEOTECH LTD: COMPANY OVERVIEW

- 13.1.19 BOMIMED

- TABLE 234 BOMIMED: COMPANY OVERVIEW

- 13.1.20 MEDIS MEDICAL (UK) LTD.

- TABLE 235 MEDIS MEDICAL (UK) LTD.: COMPANY OVERVIEW

- 13.2 OTHER PLAYERS

- 13.2.1 OLYMPUS CORPORATION

- 13.2.2 ARMSTRONG MEDICAL LTD. (EAKIN HEALTHCARE GROUP)

- 13.2.3 NIHON KOHDEN CORPORATION

- 13.2.4 SHENZHEN HUGEMED MEDICAL TECHNICAL DEVELOPMENT CO., LTD.

- 13.2.5 VENNER MEDICAL MEDIZINTECHNIK

- *Details on Business Overview, Products Offered, Recent Developments, and MnM View (Key strengths/Right to Win, Strategic Choices Made, and Weaknesses and Competitive Threats) might not be captured in case of unlisted companies.

14 APPENDIX

- 14.1 INSIGHTS FROM INDUSTRY EXPERTS

- 14.2 DISCUSSION GUIDE

- 14.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 14.4 CUSTOMIZATION OPTIONS

- 14.5 RELATED REPORTS

- 14.6 AUTHOR DETAILS