|

|

市場調査レポート

商品コード

1078878

軍用バッテリーの世界市場:タイプ(充電式、非充電式)、設置(OEM、アフターマーケット)、用途(推進、非推進)、プラットフォーム(地上、空中、海上)、組成、電圧、電力密度、地域別 - 2027年までの予測Military Battery Market by Type (Rechargeable, Non-rechargeable), Installation (OEM, Aftermarket), Application (Propulsion, Non-propulsion), Platform (Ground, Airborne, Marine), Composition, Voltage, Power Density and Region - Global Forecast to 2027 |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| 軍用バッテリーの世界市場:タイプ(充電式、非充電式)、設置(OEM、アフターマーケット)、用途(推進、非推進)、プラットフォーム(地上、空中、海上)、組成、電圧、電力密度、地域別 - 2027年までの予測 |

|

出版日: 2022年05月19日

発行: MarketsandMarkets

ページ情報: 英文 205 Pages

納期: 即納可能

|

- 全表示

- 概要

- 目次

世界の軍用バッテリーの市場規模は、2022年から2027年にかけてCAGR4.1%で成長する見通しで、2022年の13億米ドルから、2027年までに16億米ドルへに達すると予測されています。

同市場を牽引する要因には、軍事用途の地上車両やUAVのニーズの高まりが挙げられます。しかし、リチウム電池に関する規制により、市場成長の妨げとなっています。

当レポートでは、世界の軍用バッテリー市場について調査し、市場力学、特許、貿易などの分析、ケーススタディ、セグメント・地域別の市場分析、競合情勢、主要企業のプロファイルなどの情報を提供しています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- 市場力学

- 促進要因

- 抑制要因

- 市場機会

- 課題

- 平均価格分析

- 範囲とシナリオ

- 軍用バッテリー市場のバリューチェーン分析

- 動向のビジネスに影響を与える傾向/混乱

- 軍用バッテリー市場のエコシステム

- 貿易データ統計

- ポーターのファイブフォース分析

- 主要な利害関係者と購入基準

- 主な会議とイベント(2022-2023)

- 関税と規制状況

第6章 動向

- テクノロジーの動向

- テクノロジー分析

- ユースケース分析

- メガトレンドの影響

- イノベーションと特許登録

第7章 プラットフォーム別:軍用バッテリー市場

- 陸上

- 装甲車両

- 運営拠点

- 兵隊

- 航空

- 戦闘機

- 特殊任務機

- 輸送機

- 軍用ヘリコプター

- 海洋

- 駆逐艦

- フリゲート艦

- 強襲艦

- 潜水艦

- オフショア巡視船

- コルベット

第8章 組成別:軍用バッテリー市場

- リチウムベース

- リチウムニッケルマンガンコバルト酸化物(LI-NMC)

- リン酸鉄リチウム(LFP)

- コバルト酸リチウム(LCO)

- チタン酸リチウム酸化物(LTO)

- リチウムマンガン酸化物(LMO)

- リチウムニッケルコバルトアルミニウムオキシド(NCA)

- 鉛蓄電池

- ニッケルベース

- サーマル

- その他

第9章 用途別:軍用バッテリー市場

- 推進

- 非推進

第10章 タイプ別:軍用バッテリー市場

- 再充電不可

- 予備

- 一次

- 再充電可能

第11章 設置別:軍用バッテリー市場

- OEM

- アフターマーケット

第12章 電力密度別:軍用バッテリー市場

- 100 WH/KG未満

- 100~200 WH/KG

- 200 WH/KG超

第13章 電圧別:軍用バッテリー市場

- 12V未満

- 12~24 V

- 24V超

第14章 地域分析

- 北米

- PESTLE分析

- 米国

- カナダ

- 欧州

- PESTLE分析

- 英国

- フランス

- ドイツ

- ロシア

- イタリア

- その他

- アジア太平洋

- PESTLE分析

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- その他

- 中東

- PESTLE分析

- サウジアラビア

- イスラエル

- アラブ首長国連邦

- その他

- その他の地域

- PESTLE分析

- ラテンアメリカ

- アフリカ

第15章 競合情勢

- 主要企業の市場ランキング分析(2020)

- 企業の製品フットプリント分析

- 企業評価クアドラント

- スタートアップ/中小企業の評価クアドラント

- 競合ベンチマーキング

- 競合シナリオ

第16章 企業プロファイル:主要企業

- 主要企業

- ENERSYS

- BAE SYSTEMS PLC

- GS YUASA INTERNATIONAL LTD

- SAFT(TOTAL)

- EXIDE TECHNOLOGIES

- EXIDE INDUSTRIES

- ULTRALIFE CORPORATION

- AROTECH CORPORATION

- BREN-TRONICS

- EAGLEPICHER TECHNOLOGIES

- BST SYSTEMS, INC.

- CONCORDE

- LINCAD

- KOREA SPECIAL BATTERY CO., LTD.

- ECOBAT BATTERY TECHNOLOGIES

- その他の企業

- DENCHI POWER

- KOKAM

- MATHEW ASSOCIATES

- NAVITAS SYSTEMS

- TELEDYNE TECHNOLOGIES

- CELL-CON

- LECLANCHE SA

- STERLING PLANB ENERGY SOLUTIONS

- SION POWER

- LIFELINE BATTERIES

第17章 付録

The military battery market is projected to grow from USD 1.3 billion in 2022 to USD 1.6 billion by 2027, at a CAGR of 4.1% from 2022 to 2027. The market is driven by rising need for ground vehicles and UAVs in military applications. However, the market's growth is limited by the regulations on lithium batteries to foresee the market growth.

The COVID-19 outbreak has had an impact on the military battery supply chain. The spread of COVID-19 in the United States and Europe is expected to be slowed by lockdowns at military battery vehicle research and development centres.As a result of the Asia Pacific lockdown, many businesses in the military battery industry have lost revenue. Many startups have failed to continue operating in the area due to delays in development and a lack of funds. The commercialization of military battery appears to have been delayed by a year when compared with pre conditions.

The lead-acid segment is expected to hold major share of the market during the forecast periodon the basis ofcomposition

Military batteries are segmented into lithium-based, lead-acid, nickel-based, thermal, and otherson the basis of composition. Lead-acid batteries use sponge lead and lead peroxide to convert chemical energy into electrical power. The application of these batteries in militaries is declining due to the introduction of lithium-based and nickel-based batteries. Lead-acid batteries are dangerous for use under harsh military warfare conditions due to the problem of spillage of the acid. However, these batteries are still being used because of their low cost and low maintenance requirement. Increasing demand for armored vehicles and military aircraft is expected to drive the market for lead-acid batteries.

The ground segment is anticipated to lead the military battery market in near future

Military battery market has been segmented into ground, marine and airborne. Ground platforms are any equipment used by militaries or armed forces for navigation, communication, transportation, or any other purposes.

Rechargeable battery segment led the military battery market

Military battery market is segmented into rechargeable and non-rechargeable batteries. Rechargeable batteries held major share in the global market owing to higher adoption in military platforms.

Europe held largest market share in terms of value

Europe is estimated to account for 31% of the military battery market in 2022. The market in Europe is projected to grow from USD 395.8 million in 2022 to USD 478.3 million by 2027, at a CAGR of 3.86% from 2022 to 2027.

Break-up of profiles of primary participants in this report:

- By Company Type: Tier 1 - 35%, Tier 2 - 45% and Tier 3 - 20%

- By Designation: C level - 35%, Director level - 25%, Others - 40%

- By Region: North America - 45%, Europe - 25%, AsiaPacific - 15%, Middle East- 10%,Rest of the World - 5%

Research Coverage

The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the ground support equipment market. A detailed analysis of the key industry players has been done to provide insights into their business overviews; solutions and services; key strategies; contracts, joint ventures, partnerships & agreements, acquisitions, and new product launches associated with the ground support equipment market. Competitive analysis of upcoming startups in the ground support equipment market ecosystem is covered in this report.

Reasons to Buy This Report:

From an insight perspective, this research report has focused on various levels of analyses-industry analysis (industry trends), market ranking analysis of top players, value chain analysis, and company profiles, which together comprise and discuss basic views on the competitive landscape, emerging and high-growth segments of the military battery market, high-growth regions, and market drivers, restraints, and opportunities.

The report provides insights on the following pointers:

- Market Penetration: Comprehensive information on military batterysoffered by top market players

- Market Sizing: The estimated size of the market in 2022 and its projection to 2027

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product launches in the military battery market

- Market Overview: Market dynamics and subsequent analysis of associated trends as well as drivers, opportunities, and challenges prevailing in the military battery market

- Market Development: Comprehensive information about lucrative markets - the report analyzes the markets for military batteryacross regions

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the military battery market

- Regional Analysis: Factors influencing the growth of the military battery marketin North America, Europe, Asia Pacific,Middle East and Rest of the World.

- Competitive Assessment: In-depth assessment of market shares, strategies, products, and manufacturing capabilities of leading players in the military battery market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 OBJECTIVES OF THE STUDY

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED

- 1.3.2 REGIONAL SCOPE

- 1.4 YEARS CONSIDERED FOR THE STUDY

- 1.5 CURRENCY & PRICING

- TABLE 1 USD EXCHANGE RATES

- 1.6 LIMITATIONS

- 1.7 INCLUSIONS & EXCLUSIONS

- 1.8 SUMMARY OF CHANGES

- 1.9 STAKEHOLDERS

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 1 REPORT PROCESS FLOW

- FIGURE 2 RESEARCH DESIGN

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Breakdown of primaries

- 2.1.2.3 Primaries insights

- 2.2 FACTOR ANALYSIS

- 2.2.1 INTRODUCTISSSSON

- 2.2.2 DEMAND-SIDE INDICASSTORS

- 2.2.2.1 Increase in number of military fleet deliveries

- 2.2.3 SUPPLY-SIDE INDICATORS

- 2.3 MARKET SIZE ESTIMATION

- 2.3.1 BOTTOM-UP APPROACH

- FIGURE 3 MARKET SIZE ESTIMATION METHODOLOGY: BOTTOM-UP APPROACH

- 2.3.2 TOP-DOWN APPROACH

- FIGURE 4 MARKET SIZE ESTIMATION METHODOLOGY: TOP-DOWN APPROACH

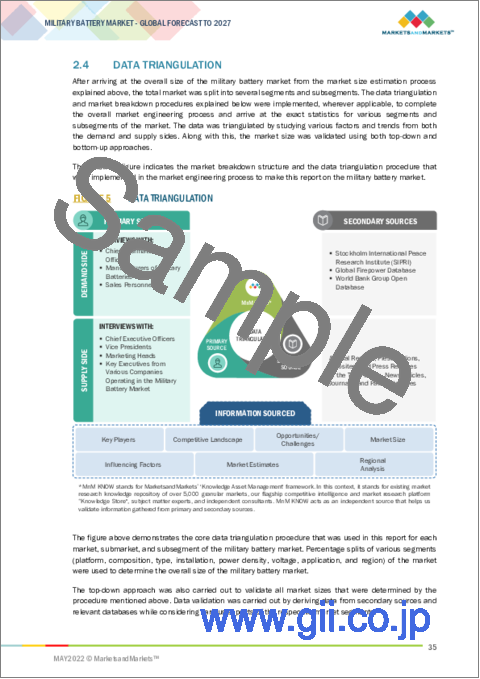

- 2.4 DATA TRIANGULATION

- FIGURE 5 DATA TRIANGULATION

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 RISK ANALYSIS

3 EXECUTIVE SUMMARY

- FIGURE 6 MILITARY BATTERY MARKET, BY TYPE, 2022 & 2027 (USD MILLION)

- FIGURE 7 MILITARY BATTERY MARKET, BY INSTALLATION, 2022 & 2027 (USD MILLION)

- FIGURE 8 MILITARY BATTERY MARKET, BY PLATFORM, 2022-2027 (USD MILLION)

- FIGURE 9 MILITARY BATTERY MARKET, BY PLATFORM, 2022-2027 (USD MILLION)

- FIGURE 10 NORTH AMERICA ESTIMATED TO LEAD MILITARY BATTERY MARKET IN 2022

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE GROWTH OPPORTUNITIES IN MILITARY BATTERY MARKET

- FIGURE 11 INCREASING DEMAND FOR FIGHTER AIRCRAFT IN MILITARY OPERATIONS EXPECTED TO DRIVE MILITARY BATTERY MARKET FROM 2022 TO 2027

- 4.2 MILITARY BATTERY MARKET, BY INSTALLATION

- FIGURE 12 OEM SEGMENT ESTIMATED TO LEAD MILITARY BATTERY MARKET IN 2022

- 4.3 MILITARY BATTERY MARKET, BY POWER DENSITY

- FIGURE 13 LESS THAN 100 WH/KG SEGMENT PROJECTED LEAD MILITARY BATTERY MARKET FROM 2022 TO 2027

- 4.4 MILITARY BATTERY MARKET, BY COMPOSITION

- FIGURE 14 LEAD-ACID SEGMENT PROJECTED TO LEAD MILITARY BATTERY MARKET FROM 2022 TO 2027

- 4.5 MILITARY BATTERY MARKET, BY APPLICATION

- FIGURE 15 NON-PROPULSION SEGMENT PROJECTED TO LEAD MILITARY BATTERY MARKET FROM 2022 TO 2027

- 4.6 MILITARY BATTERY MARKET, BY COUNTRY

- FIGURE 16 CHINA PROJECTED TO REGISTER HIGHEST CAGR IN MILITARY BATTERY MARKET FROM 2022 TO 2027

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 17 MILITARY BATTERY MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- 5.2.1 DRIVERS

- 5.2.1.1 Rising adoption of ground vehicles and UAVs

- 5.2.1.2 Increased use of lightweight and high-power density batteries in sophisticated military systems

- 5.2.1.3 Rising military expenditure on new platforms

- 5.2.2 RESTRAINTS

- 5.2.2.1 Regulations on lithium batteries

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Advancements in material sciences and battery technology

- 5.2.3.2 Innovations in smart battery technology

- 5.2.3.3 Emerging markets in Southeast Asia

- 5.2.4 CHALLENGES

- 5.2.4.1 Design challenges associated with manufacturing batteries

- 5.2.4.2 Recovery from pandemic

- 5.3 AVERAGE PRICE ANALYSIS

- 5.3.1 AVERAGE SELLING PRICE OF MILITARY BATTERIES

- FIGURE 18 AVERAGE SELLING PRICES OF KEY PLAYERS

- 5.3.2 AVERAGE SELLING PRICE OF MILITARY BATTERY TYPES

- TABLE 2 AVERAGE SELLING PRICE TRENDS OF MILITARY BATTERIES, 2020 (USD MILLION)

- 5.4 RANGES AND SCENARIOS

- FIGURE 19 COVID-19 IMPACT ON MILITARY BATTERY MARKET: 3 GLOBAL SCENARIOS

- 5.5 VALUE CHAIN ANALYSIS OF MILITARY BATTERY MARKET

- FIGURE 20 VALUE CHAIN ANALYSIS

- 5.6 TRENDS/DISRUPTION IMPACTING CUSTOMER BUSINESS

- 5.6.1 REVENUE SHIFT AND NEW REVENUE POCKETS FOR MILITARY BATTERY MANUFACTURERS

- FIGURE 21 REVENUE SHIFT FOR MILITARY BATTERY MARKET PLAYERS

- 5.7 MILITARY BATTERY MARKET ECOSYSTEM

- 5.7.1 PROMINENT COMPANIES

- 5.7.2 PRIVATE AND SMALL ENTERPRISES

- 5.7.3 MARKET ECOSYSTEM

- FIGURE 22 MARKET ECOSYSTEM MAP: MILITARY BATTERY MARKET

- TABLE 3 MILITARY BATTERY MARKET ECOSYSTEM

- 5.8 TRADE DATA STATISTICS

- 5.8.1 IMPORT DATA STATISTICS

- TABLE 4 IMPORT VALUE OF LITHIUM-ION BATTERIES (PRODUCT HARMONIZED SYSTEM CODE: 850760) (USD THOUSAND)

- 5.8.2 EXPORT DATA STATISTICS

- TABLE 5 EXPORT VALUE OF LITHIUM-ION BATTERIES (PRODUCT HARMONIZED SYSTEM CODE: 850760) (USD THOUSAND)

- 5.9 PORTER'S FIVE FORCES ANALYSIS

- TABLE 6 MILITARY BATTERY MARKET: PORTER'S FIVE FORCE ANALYSIS

- 5.9.1 THREAT OF NEW ENTRANTS

- 5.9.2 THREAT OF SUBSTITUTES

- 5.9.3 BARGAINING POWER OF SUPPLIERS

- 5.9.4 BARGAINING POWER OF BUYERS

- 5.9.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.10 KEY STAKEHOLDERS & BUYING CRITERIA

- 5.10.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 23 INFLUENCE OF STAKEHOLDERS IN BUYING PROCESS FOR TOP 3 APPLICATIONS

- TABLE 7 INFLUENCE OF STAKEHOLDERS IN BUYING PROCESS FOR TOP 3 APPLICATIONS (%)

- 5.10.2 BUYING CRITERIA

- FIGURE 24 KEY BUYING CRITERIA FOR TOP 3 APPLICATIONS

- TABLE 8 KEY BUYING CRITERIA FOR TOP 3 APPLICATIONS

- 5.11 KEY CONFERENCES & EVENTS IN 2022-2023

- TABLE 9 AEROSTRUCTURES MARKET: DETAILED LIST OF CONFERENCES & EVENTS

- 5.11.1 TARIFF AND REGULATORY LANDSCAPE

- 5.11.1.1 Regulatory bodies, government agencies, and other organizations

- TABLE 10 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 11 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 12 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, SAND OTHER ORGANIZATIONS

- 5.12 TARIFF AND REGULATORY LANDSCAPE

- 5.12.1 NORTH AMERICA

- 5.12.2 EUROPE

6 INDUSTRY TRENDS

- 6.1 INTRODUCTION

- 6.2 TECHNOLOGY TRENDS

- FIGURE 25 TECHNOLOGY TRENDS IN MILITARY BATTERY MARKET

- 6.2.1 WIRELESS CHARGING FOR DRONES

- 6.2.2 CONFORMABLE WEARABLE BATTERIES

- 6.2.3 ADVANCEMENTS IN LITHIUM-ION FILM TECHNOLOGY

- 6.2.4 NEXT-GENERATION SOLID-STATE BATTERY TECHNOLOGY

- 6.2.5 HYBRID BATTERIES

- 6.3 TECHNOLOGY ANALYSIS

- 6.4 USE CASE ANALYSIS

- 6.4.1 SMALL TACTICAL UNIVERSAL BATTERY FOR HANDHELD MILITARY APPLICATIONS

- 6.4.2 THALES' STRATOBUS POWERED USING LIGHTWEIGHT LITHIUM METAL BATTERIES

- 6.5 IMPACT OF MEGATRENDS

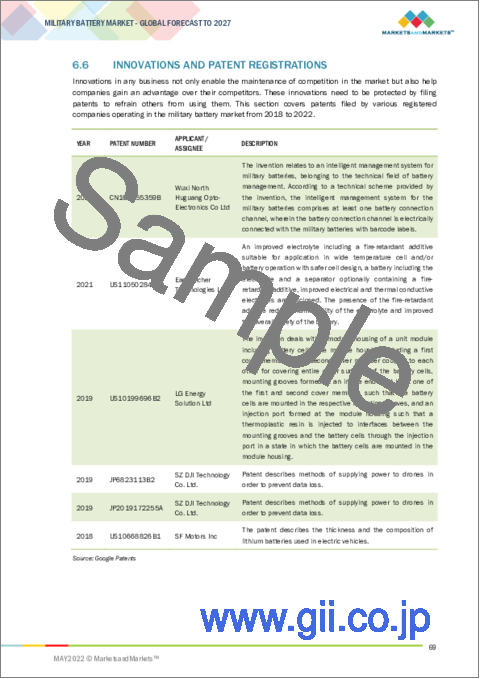

- 6.6 INNOVATIONS AND PATENT REGISTRATIONS

7 MILITARY BATTERY MARKET, BY PLATFORM

- 7.1 INTRODUCTION

- FIGURE 26 BY PLATFORM, GROUND SEGMENT PROJECTED TO LEAD MARKET FROM 2022 TO 2027

- TABLE 13 MILITARY BATTERY MARKET, BY PLATFORM, 2018-2021 (USD MILLION)

- TABLE 14 MILITARY BATTERY MARKET, BY PLATFORM, 2022-2027 (USD MILLION)

- 7.2 GROUND

- TABLE 15 GROUND: MILITARY BATTERY MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 16 GROUND: MILITARY BATTERY MARKET, BY TYPE, 2022-2027 (USD MILLION)

- 7.2.1 ARMORED VEHICLES

- 7.2.1.1 Growing demand for armored vehicles to drive segment

- 7.2.2 OPERATING BASES

- 7.2.2.1 Communication equipment and electrification of equipment to drive segment

- 7.2.3 SOLDIERS

- 7.2.3.1 Increasing adoption of advanced military wearables to drive segment

- 7.3 AIRBORNE

- TABLE 17 AIRBORNE: MILITARY BATTERY MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 18 AIRBORNE: MILITARY BATTERY MARKET, BY TYPE, 2022-2027 (USD MILLION)

- 7.3.1 FIGHTER AIRCRAFT

- 7.3.1.1 Rising need to gain airborne dominance globally to drive market growth

- 7.3.2 SPECIAL MISSION AIRCRAFT

- 7.3.2.1 Ability to carry heavy payloads and fly longer durations to drive market growth

- 7.3.3 TRANSPORT AIRCRAFT

- 7.3.3.1 Increasing demand for transport aircraft across regions to drive market growth

- 7.3.4 MILITARY HELICOPTERS

- 7.3.4.1 Increasing usage for ISR missions and rescue operations to drive demand

- 7.4 MARINE

- TABLE 19 MARINE: MILITARY BATTERY MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 20 MARINE: MILITARY BATTERY MARKET, BY TYPE, 2022-2027 (USD MILLION)

- 7.4.1 DESTROYERS

- 7.4.1.1 Defense forces of several countries focusing on integrating electric propulsive destroyers into their fleet to gain high operational efficiency

- 7.4.2 FRIGATES

- 7.4.2.1 Naval forces of various countries planning to install hybrid propulsion systems for frigates

- 7.4.3 AMPHIBIOUS SHIPS

- 7.4.3.1 Amphibious warship development programs to drive segment

- 7.4.4 SUBMARINES

- 7.4.4.1 Several countries currently using or developing electric propulsion systems for their submarine fleet

- 7.4.5 OFFSHORE PATROL VESSELS

- 7.4.5.1 Growing adoption of Offshore Patrol Vessels (OPVs) for hybrid and electric propulsion setups

- 7.4.6 CORVETTES

- 7.4.6.1 Replacing aging corvettes to drive segment

8 MILITARY BATTERY MARKET, BY COMPOSITION

- 8.1 INTRODUCTION

- FIGURE 27 BY COMPOSITION, LEAD-ACID SEGMENT TO COMMAND LARGEST MARKET SIZE DURING FORECAST PERIOD

- TABLE 21 MILITARY BATTERY MARKET SIZE, BY COMPOSITION, 2018-2021 (USD MILLION)

- TABLE 22 MILITARY BATTERY MARKET SIZE, BY COMPOSITION, 2022-2027 (USD MILLION)

- 8.2 LITHIUM-BASED

- 8.2.1 LITHIUM NICKEL MANGANESE COBALT OXIDE (LI-NMC)

- 8.2.1.1 Lithium nickel manganese cobalt oxide (LI-NMC) offers longer lifecycle at low cost

- 8.2.2 LITHIUM IRON PHOSPHATE (LFP)

- 8.2.2.1 Lithium iron phosphate batteries are characterized by their safe operations

- 8.2.3 LITHIUM COBALT OXIDE (LCO)

- 8.2.3.1 Demand for high capacity batteries drives segment's growth

- 8.2.4 LITHIUM TITANATE OXIDE (LTO)

- 8.2.4.1 Demand for fast-charging batteries drives segment's growth

- 8.2.5 LITHIUM MANGANESE OXIDE (LMO)

- 8.2.5.1 Growing preference for thermally stable batteries drives segment's growth

- 8.2.6 LITHIUM NICKEL COBALT ALUMINUM OXIDE (NCA)

- 8.2.6.1 High adoption in armored vehicles drives segment's growth

- 8.2.1 LITHIUM NICKEL MANGANESE COBALT OXIDE (LI-NMC)

- 8.3 LEAD-ACID

- 8.3.1 INCREASING NUMBER OF ARMORED VEHICLES AND AIRCRAFT TO DRIVE SEGMENT

- 8.4 NICKEL-BASED

- 8.4.1 GROWING POPULARITY OF STRATEGIC DRONES IN DEFENSE SECTOR TO FUEL DEMAND

- 8.5 THERMAL

- 8.5.1 INCREASING NUMBER OF ARMS AND AMMUNITION TO DRIVE SEGMENT

- 8.6 OTHERS

9 MILITARY BATTERY MARKET, BY APPLICATION

- 9.1 INTRODUCTION

- FIGURE 28 BY APPLICATION, NON-PROPULSION SEGMENT PROJECTED TO LEAD MILITARY BATTERY MARKET DURING FORECAST PERIOD

- TABLE 23 MILITARY BATTERY MARKET SIZE, BY APPLICATION, 2018-2021 (USD MILLION)

- TABLE 24 MILITARY BATTERY MARKET SIZE, BY APPLICATION, 2022-2027 (USD MILLION)

- 9.2 PROPULSION

- 9.2.1 DEVELOPMENT OF ELECTRIC AIRCRAFT TO DRIVE MARKET GROWTH

- 9.3 NON-PROPULSION

- 9.3.1 REPLACEMENT OF ANALOG ELECTRONICS WITH DIGITAL SYSTEMS TO DRIVE MARKET GROWTH

10 MILITARY BATTERIES MARKET, BY TYPE

- 10.1 INTRODUCTION

- FIGURE 29 BY TYPE, RECHARGEABLE SEGMENT PROJECTED TO LEAD MARKET FROM 2022 TO 2027

- TABLE 25 MILITARY BATTERY MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 26 MILITARY BATTERY MARKET, BY TYPE, 2022-2027 (USD MILLION)

- 10.2 NON-RECHARGEABLE

- 10.2.1 APPLICATION IN HIGH ENERGY DENSITY REQUIREMENTS TO DRIVE SEGMENT

- 10.2.2 RESERVE

- 10.2.3 PRIMARY

- 10.3 RECHARGEABLE

- 10.3.1 INCREASING NUMBER OF HANDHELD DEVICES FOR MILITARY APPLICATIONS TO DRIVE SEGMENT

11 MILITARY BATTERY MARKET, BY INSTALLATION

- 11.1 INTRODUCTION

- FIGURE 30 AFTERMARKET SEGMENT TO COMMAND LARGEST MARKET SIZE DURING FORECAST PERIOD

- TABLE 27 MILITARY BATTERY MARKET SIZE, BY INSTALLATION, 2018-2021 (USD MILLION)

- TABLE 28 MILITARY BATTERY MARKET SIZE, BY INSTALLATION, 2022-2027 (USD MILLION)

- 11.2 OEM

- 11.2.1 ELECTRIFICATION OF SYSTEMS AND CHANGING TECHNOLOGY TO DRIVE SEGMENT

- 11.3 AFTERMARKET

- 11.3.1 REPLACEMENT OF BATTERIES TO FUEL MARKET

12 MILITARY BATTERY MARKET, BY POWER DENSITY

- 12.1 INTRODUCTION

- FIGURE 31 BY POWER DENSITY, LESS THAN 100 WH/KG SEGMENT PROJECTED TO LEAD MARKET FROM 2022 TO 2027

- TABLE 29 MILITARY BATTERY MARKET, BY POWER DENSITY, 2018-2021 (USD MILLION)

- TABLE 30 MILITARY BATTERY MARKET, BY POWER DENSITY, 2022-2027 (USD MILLION)

- 12.2 LESS THAN 100 WH/KG

- 12.2.1 GROWING ADOPTION IN ARMORED VEHICLES AND OPERATING BASES

- 12.3 100-200 WH/KG

- 12.3.1 GROWING MODERNIZATION OF SOLDIER SYSTEMS USING 100 TO 200 WH/KG BATTERIES

- 12.4 MORE THAN 200 WH/KG

- 12.4.1 ADVENT OF ELECTRIC PROPULSION IN MILITARY PLATFORMS

13 MILITARY BATTERY MARKET, BY VOLTAGE

- 13.1 INTRODUCTION

- FIGURE 32 BY VOLTAGE, 12-24 V SEGMENT PROJECTED TO LEAD MARKET FROM 2022 TO 2027

- TABLE 31 MILITARY BATTERY MARKET, BY VOLTAGE, 2018-2021 (USD MILLION)

- TABLE 32 MILITARY BATTERY MARKET, BY VOLTAGE, 2022-2027 (USD MILLION)

- 13.2 LESS THAN 12 V

- 13.2.1 RISING DEMAND FOR BETTER COMMUNICATION NETWORKS TO DRIVE SEGMENT

- 13.3 12-24 V

- 13.3.1 INCREASING NUMBER OF UNMANNED SOLUTIONS TO DRIVE SEGMENT

- 13.4 MORE THAN 24 V

- 13.4.1 INCREASING NUMBER OF MILITARY BASES TO DRIVE SEGMENT

14 REGIONAL ANALYSIS

- 14.1 INTRODUCTION

- FIGURE 33 MILITARY BATTERY MARKET IN ASIA PACIFIC PROJECTED TO GROW AT HIGHEST RATE FROM 2022 TO 2027

- TABLE 33 MILITARY BATTERY MARKET, BY PLATFORM, 2018-2021 (USD MILLION)

- TABLE 34 MILITARY BATTERY MARKET, BY PLATFORM, 2022-2027 (USD MILLION)

- TABLE 35 MILITARY BATTERY MARKET, BY COMPOSITION, 2018-2021 (USD MILLION)

- TABLE 36 MILITARY BATTERY MARKET, BY COMPOSITION, 2022-2027 (USD MILLION)

- TABLE 37 MILITARY BATTERY MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 38 MILITARY BATTERY MARKET, BY TYPE, 2022-2027 (USD MILLION)

- TABLE 39 MILITARY BATTERY MARKET, BY INSTALLATION, 2018-2021 (USD MILLION)

- TABLE 40 MILITARY BATTERY MARKET, BY INSTALLATION, 2022-2027 (USD MILLION)

- TABLE 41 MILITARY BATTERY MARKET, BY POWER DENSITY, 2018-2021 (USD MILLION)

- TABLE 42 MILITARY BATTERY MARKET, BY POWER DENSITY, 2022-2027 (USD MILLION)

- TABLE 43 MILITARY BATTERY MARKET, BY VOLTAGE, 2018-2021 (USD MILLION)

- TABLE 44 MILITARY BATTERY MARKET, BY VOLTAGE, 2022-2027 (USD MILLION)

- TABLE 45 MILITARY BATTERY MARKET, BY REGION, 2018-2021 (USD MILLION)

- TABLE 46 MILITARY BATTERY MARKET, BY REGION, 2022-2027 (USD MILLION)

- 14.2 NORTH AMERICA

- 14.2.1 PESTLE ANALYSIS: NORTH AMERICA

- FIGURE 34 NORTH AMERICA MILITARY BATTERY MARKET SNAPSHOT

- TABLE 47 NORTH AMERICA: MILITARY BATTERY MARKET, BY PLATFORM, 2018-2021 (USD MILLION)

- TABLE 48 NORTH AMERICA: MILITARY BATTERY MARKET, BY PLATFORM, 2022-2027 (USD MILLION)

- TABLE 49 NORTH AMERICA: MILITARY BATTERY MARKET, BY VOLTAGE, 2018-2021 (USD MILLION)

- TABLE 50 NORTH AMERICA: MILITARY BATTERY MARKET, BY VOLTAGE, 2022-2027 (USD MILLION)

- TABLE 51 NORTH AMERICA: MILITARY BATTERY MARKET, BY COUNTRY, 2018-2021 (USD MILLION)

- TABLE 52 NORTH AMERICA: MILITARY BATTERY MARKET, BY COUNTRY, 2022-2027 (USD MILLION)

- 14.2.2 US

- 14.2.2.1 Increased spending on innovative technologies by US defense organizations and private players to fuel market growth

- TABLE 53 US: MILITARY BATTERY MARKET, BY PLATFORM, 2018-2021 (USD MILLION)

- TABLE 54 US: MILITARY BATTERY MARKET, BY PLATFORM, 2022-2027 (USD MILLION)

- TABLE 55 US: MILITARY BATTERY MARKET, BY VOLTAGE, 2018-2021 (USD MILLION)

- TABLE 56 US: MILITARY BATTERY MARKET, BY VOLTAGE, 2022-2027 (USD MILLION)

- 14.2.3 CANADA

- 14.2.3.1 Increasing military procurements and growing demand for UAVs drive market

- TABLE 57 CANADA: MILITARY BATTERY MARKET, BY PLATFORM, 2018-2021 (USD MILLION)

- TABLE 58 CANADA: MILITARY BATTERY MARKET, BY PLATFORM, 2022-2027 (USD MILLION)

- TABLE 59 CANADA: MILITARY BATTERY MARKET, BY VOLTAGE, 2018-2021 (USD MILLION)

- TABLE 60 CANADA: MILITARY BATTERY MARKET, BY VOLTAGE, 2022-2027 (USD MILLION)

- 14.3 EUROPE

- 14.3.1 PESTLE ANALYSIS: EUROPE

- FIGURE 35 EUROPE MILITARY BATTERY MARKET SNAPSHOT

- TABLE 61 EUROPE: MILITARY BATTERY MARKET, BY PLATFORM, 2018-2021 (USD MILLION)

- TABLE 62 EUROPE: MILITARY BATTERY MARKET, BY PLATFORM, 2022-2027 (USD MILLION)

- TABLE 63 EUROPE: MILITARY BATTERY MARKET, BY VOLTAGE, 2018-2021 (USD MILLION)

- TABLE 64 EUROPE: MILITARY BATTERY MARKET, BY VOLTAGE, 2022-2027 (USD MILLION)

- TABLE 65 EUROPE: MILITARY BATTERY MARKET, BY COUNTRY, 2018-2021 (USD MILLION)

- TABLE 66 EUROPE: MILITARY BATTERY MARKET, BY COUNTRY, 2022-2027 (USD MILLION)

- 14.3.2 UK

- 14.3.2.1 Procurement of new airborne platforms including UAVs, helicopters, and aircraft to drive market

- TABLE 67 UK: MILITARY BATTERY MARKET, BY PLATFORM, 2018-2021 (USD MILLION)

- TABLE 68 UK: MILITARY BATTERY MARKET, BY PLATFORM, 2022-2027 (USD MILLION)

- TABLE 69 UK: MILITARY BATTERY MARKET, BY VOLTAGE, 2018-2021 (USD MILLION)

- TABLE 70 UK: MILITARY BATTERY MARKET, BY VOLTAGE, 2022-2027 (USD MILLION)

- 14.3.3 FRANCE

- 14.3.3.1 Increased military spending and aerospace sector fuel market growth

- TABLE 71 FRANCE: MILITARY BATTERY MARKET, BY PLATFORM, 2018-2021 (USD MILLION)

- TABLE 72 FRANCE: MILITARY BATTERY MARKET, BY PLATFORM, 2022-2027 (USD MILLION)

- TABLE 73 FRANCE: MILITARY BATTERY MARKET, BY VOLTAGE, 2018-2021 (USD MILLION)

- TABLE 74 FRANCE: MILITARY BATTERY MARKET, BY VOLTAGE, 2022-2027 (USD MILLION)

- 14.3.4 GERMANY

- 14.3.4.1 Investments in UGVs to develop multifunctional and technologically advanced land or ground robots

- TABLE 75 GERMANY: MILITARY BATTERY MARKET, BY PLATFORM, 2018-2021 (USD MILLION)

- TABLE 76 GERMANY: MILITARY BATTERY MARKET, BY PLATFORM, 2022-2027 (USD MILLION)

- TABLE 77 GERMANY: MILITARY BATTERY MARKET, BY VOLTAGE, 2018-2021 (USD MILLION)

- TABLE 78 GERMANY: MILITARY BATTERY MARKET, BY VOLTAGE, 2022-2027 (USD MILLION)

- 14.3.5 RUSSIA

- 14.3.5.1 Rising geopolitical tensions and increasing military expenditure to propel market growth

- TABLE 79 RUSSIA: MILITARY BATTERY MARKET, BY PLATFORM, 2018-2021 (USD MILLION)

- TABLE 80 RUSSIA: MILITARY BATTERY MARKET, BY PLATFORM, 2022-2027 (USD MILLION)

- TABLE 81 RUSSIA: MILITARY BATTERY MARKET, BY VOLTAGE, 2018-2021 (USD MILLION)

- TABLE 82 RUSSIA: MILITARY BATTERY MARKET, BY VOLTAGE, 2022-2027 (USD MILLION)

- 14.3.6 ITALY

- 14.3.6.1 Rising demand for drones and UAVs to drive market

- TABLE 83 ITALY: MILITARY BATTERY MARKET, BY PLATFORM, 2018-2021 (USD MILLION)

- TABLE 84 ITALY: MILITARY BATTERY MARKET, BY PLATFORM, 2022-2027 (USD MILLION)

- TABLE 85 ITALY: MILITARY BATTERY MARKET, BY VOLTAGE, 2018-2021 (USD MILLION)

- TABLE 86 ITALY: MILITARY BATTERY MARKET, BY VOLTAGE, 2022-2027 (USD MILLION)

- 14.3.7 REST OF EUROPE

- 14.3.7.1 Rising border conflicts to fuel market growth

- TABLE 87 REST OF EUROPE: MILITARY BATTERY MARKET, BY PLATFORM, 2018-2021 (USD MILLION)

- TABLE 88 REST OF EUROPE: MILITARY BATTERY MARKET, BY PLATFORM, 2022-2027 (USD MILLION)

- TABLE 89 REST OF EUROPE: MILITARY BATTERY MARKET, BY VOLTAGE, 2018-2021 (USD MILLION)

- TABLE 90 REST OF EUROPE: MILITARY BATTERY MARKET, BY VOLTAGE, 2022-2027 (USD MILLION)

- 14.4 ASIA PACIFIC

- 14.4.1 PESTLE ANALYSIS: ASIA PACIFIC

- FIGURE 36 ASIA PACIFIC MILITARY BATTERY MARKET SNAPSHOT

- TABLE 91 ASIA PACIFIC: MILITARY BATTERY MARKET, BY PLATFORM, 2018-2021 (USD MILLION)

- TABLE 92 ASIA PACIFIC: MILITARY BATTERY MARKET, BY PLATFORM, 2022-2027 (USD MILLION)

- TABLE 93 ASIA PACIFIC: MILITARY BATTERY MARKET, BY VOLTAGE, 2018-2021 (USD MILLION)

- TABLE 94 ASIA PACIFIC: MILITARY BATTERY MARKET, BY VOLTAGE, 2022-2027 (USD MILLION)

- TABLE 95 ASIA PACIFIC: MILITARY BATTERY MARKET, BY COUNTRY, 2018-2021 (USD MILLION)

- TABLE 96 ASIA PACIFIC: MILITARY BATTERY MARKET, BY COUNTRY, 2022-2027 (USD MILLION)

- 14.4.2 CHINA

- 14.4.2.1 Presence of major drone manufacturing companies to boost market growth

- TABLE 97 CHINA: MILITARY BATTERY MARKET, BY PLATFORM, 2018-2021 (USD MILLION)

- TABLE 98 CHINA: MILITARY BATTERY MARKET, BY PLATFORM, 2022-2027 (USD MILLION)

- TABLE 99 CHINA: MILITARY BATTERY MARKET, BY VOLTAGE, 2018-2021 (USD MILLION)

- TABLE 100 CHINA: MILITARY BATTERY MARKET, BY VOLTAGE, 2022-2027 (USD MILLION)

- 14.4.3 INDIA

- 14.4.3.1 In-house development of military equipment to drive market growth

- TABLE 101 INDIA: MILITARY BATTERY MARKET, BY PLATFORM, 2018-2021 (USD MILLION)

- TABLE 102 INDIA: MILITARY BATTERY MARKET, BY PLATFORM, 2022-2027 (USD MILLION)

- TABLE 103 INDIA: MILITARY BATTERY MARKET, BY VOLTAGE, 2018-2021 (USD MILLION)

- TABLE 104 INDIA: MILITARY BATTERY MARKET, BY VOLTAGE, 2022-2027 (USD MILLION)

- 14.4.4 JAPAN

- 14.4.4.1 Technological advancements and significant defense budget to drive market

- TABLE 105 JAPAN: MILITARY BATTERY MARKET, BY PLATFORM, 2018-2021 (USD MILLION)

- TABLE 106 JAPAN: MILITARY BATTERY MARKET, BY PLATFORM, 2022-2027 (USD MILLION)

- TABLE 107 JAPAN: MILITARY BATTERY MARKET, BY VOLTAGE, 2018-2021 (USD MILLION)

- TABLE 108 JAPAN: MILITARY BATTERY MARKET, BY VOLTAGE, 2022-2027 (USD MILLION)

- 14.4.5 SOUTH KOREA

- 14.4.5.1 Increased spending by armed forces on UAVs to drive market

- TABLE 109 SOUTH KOREA: MILITARY BATTERY MARKET, BY PLATFORM, 2018-2021 (USD MILLION)

- TABLE 110 SOUTH KOREA: MILITARY BATTERY MARKET, BY PLATFORM, 2022-2027 (USD MILLION)

- TABLE 111 SOUTH KOREA: MILITARY BATTERY MARKET, BY VOLTAGE, 2018-2021 (USD MILLION)

- TABLE 112 SOUTH KOREA: MILITARY BATTERY MARKET, BY VOLTAGE, 2022-2027 (USD MILLION)

- 14.4.6 AUSTRALIA

- 14.4.6.1 Increasing modernization of combat fleets drives market growth

- TABLE 113 AUSTRALIA: MILITARY BATTERY MARKET, BY PLATFORM, 2018-2021 (USD MILLION)

- TABLE 114 AUSTRALIA: MILITARY BATTERY MARKET, BY PLATFORM, 2022-2027 (USD MILLION)

- TABLE 115 AUSTRALIA: MILITARY BATTERY MARKET, BY VOLTAGE, 2018-2021 (USD MILLION)

- TABLE 116 AUSTRALIA: MILITARY BATTERY MARKET, BY VOLTAGE, 2022-2027 (USD MILLION)

- 14.4.7 REST OF ASIA PACIFIC

- TABLE 117 REST OF ASIA PACIFIC: MILITARY BATTERY MARKET, BY PLATFORM, 2018-2021 (USD MILLION)

- TABLE 118 REST OF ASIA PACIFIC: MILITARY BATTERY MARKET, BY PLATFORM, 2022-2027 (USD MILLION)

- TABLE 119 REST OF ASIA PACIFIC: MILITARY BATTERY MARKET, BY VOLTAGE, 2018-2021 (USD MILLION)

- TABLE 120 REST OF ASIA PACIFIC: MILITARY BATTERY MARKET, BY VOLTAGE, 2022-2027 (USD MILLION)

- 14.5 MIDDLE EAST

- 14.5.1 PESTLE ANALYSIS: MIDDLE EAST

- FIGURE 37 MIDDLE EAST MILITARY BATTERY MARKET SNAPSHOT

- TABLE 121 MIDDLE EAST: MILITARY BATTERY MARKET, BY PLATFORM, 2018-2021 (USD MILLION)

- TABLE 122 MIDDLE EAST: MILITARY BATTERY MARKET, BY PLATFORM, 2022-2027 (USD MILLION)

- TABLE 123 MIDDLE EAST: MILITARY BATTERY MARKET, BY VOLTAGE, 2018-2021 (USD MILLION)

- TABLE 124 MIDDLE EAST: MILITARY BATTERY MARKET, BY VOLTAGE, 2022-2027 (USD MILLION)

- TABLE 125 MIDDLE EAST: MILITARY BATTERY MARKET, BY COUNTRY, 2018-2021 (USD MILLION)

- TABLE 126 MIDDLE EAST: MILITARY BATTERY MARKET, BY COUNTRY, 2022-2027 (USD MILLION)

- 14.5.2 SAUDI ARABIA

- 14.5.2.1 High military expenditure to drive market growth

- TABLE 127 SAUDI ARABIA: MILITARY BATTERY MARKET, BY PLATFORM, 2018-2021 (USD MILLION)

- TABLE 128 SAUDI ARABIA: MILITARY BATTERY MARKET, BY PLATFORM, 2022-2027 (USD MILLION)

- TABLE 129 SAUDI ARABIA: MILITARY BATTERY MARKET, BY VOLTAGE, 2018-2021 (USD MILLION)

- TABLE 130 SAUDI ARABIA: MILITARY BATTERY MARKET, BY VOLTAGE, 2022-2027 (USD MILLION)

- 14.5.3 ISRAEL

- 14.5.3.1 Increase spending on R&D of drones to drive market growth

- TABLE 131 ISRAEL: MILITARY BATTERY MARKET, BY PLATFORM, 2018-2021 (USD MILLION)

- TABLE 132 ISRAEL: MILITARY BATTERY MARKET, BY PLATFORM, 2022-2027 (USD MILLION)

- TABLE 133 ISRAEL: MILITARY BATTERY MARKET, BY VOLTAGE, 2018-2021 (USD MILLION)

- TABLE 134 ISRAEL: MILITARY BATTERY MARKET, BY VOLTAGE, 2022-2027 (USD MILLION)

- 14.5.4 UAE

- 14.5.4.1 Tensions in neighboring states to drive market growth

- 14.5.5 REST OF MIDDLE EAST

- TABLE 135 REST OF MIDDLE EAST: MILITARY BATTERY MARKET, BY PLATFORM, 2018-2021 (USD MILLION)

- TABLE 136 REST OF MIDDLE EAST: MILITARY BATTERY MARKET, BY PLATFORM, 2022-2027 (USD MILLION)

- TABLE 137 REST OF MIDDLE EAST: MILITARY BATTERY MARKET, BY VOLTAGE, 2018-2021 (USD MILLION)

- TABLE 138 REST OF MIDDLE EAST: MILITARY BATTERY MARKET, BY VOLTAGE, 2022-2027 (USD MILLION)

- 14.6 REST OF THE WORLD

- 14.6.1 PESTLE ANALYSIS: REST OF THE WORLD

- TABLE 139 REST OF THE WORLD: MILITARY BATTERY MARKET, BY PLATFORM, 2018-2021 (USD MILLION)

- TABLE 140 REST OF THE WORLD: MILITARY BATTERY MARKET, BY PLATFORM, 2022-2027 (USD MILLION)

- TABLE 141 REST OF THE WORLD: MILITARY BATTERY MARKET, BY VOLTAGE, 2018-2021 (USD MILLION)

- TABLE 142 REST OF THE WORLD: MILITARY BATTERY MARKET, BY VOLTAGE, 2022-2027 (USD MILLION)

- TABLE 143 REST OF THE WORLD: MILITARY BATTERY MARKET, BY REGION, 2018-2021 (USD MILLION)

- TABLE 144 REST OF THE WORLD: MILITARY BATTERY MARKET, BY REGION, 2022-2027 (USD MILLION)

- 14.6.2 LATIN AMERICA

- 14.6.2.1 Increase demand for military unmanned vehicles to drive market

- TABLE 145 LATIN AMERICA: MILITARY BATTERY MARKET, BY PLATFORM, 2018-2021 (USD MILLION)

- TABLE 146 LATIN AMERICA: MILITARY BATTERY MARKET, BY PLATFORM, 2022-2027 (USD MILLION)

- TABLE 147 LATIN AMERICA: MILITARY BATTERY MARKET, BY VOLTAGE, 2018-2021 (USD MILLION)

- TABLE 148 LATIN AMERICA: MILITARY BATTERY MARKET, BY VOLTAGE, 2022-2027 (USD MILLION)

- 14.6.3 AFRICA

- 14.6.3.1 Focus on securing borders and improving military capabilities to drive market

- TABLE 149 AFRICA: MILITARY BATTERY MARKET, BY PLATFORM, 2018-2021 (USD MILLION)

- TABLE 150 AFRICA: MILITARY BATTERY MARKET, BY PLATFORM, 2022-2027 (USD MILLION)

- TABLE 151 AFRICA: MILITARY BATTERY MARKET, BY VOLTAGE, 2018-2021 (USD MILLION)

- TABLE 152 AFRICA: MILITARY BATTERY MARKET, BY VOLTAGE, 2022-2027 (USD MILLION)

15 COMPETITIVE LANDSCAPE

- 15.1 INTRODUCTION

- 15.1.1 COMPETITIVE OVERVIEW

- TABLE 153 KEY DEVELOPMENTS BY LEADING PLAYERS IN MILITARY BATTERY MARKET BETWEEN 2018 AND 2021

- FIGURE 38 MARKET EVALUATION FRAMEWORK: ACQUISITION IS KEY STRATEGY ADOPTED BY MARKET PLAYERS

- 15.2 MARKET RANKING ANALYSIS OF KEY PLAYERS, 2020

- FIGURE 39 RANKING ANALYSIS OF TOP 5 PLAYERS: MILITARY BATTERY MARKET, 2020

- FIGURE 40 MARKET SHARE OF KEY PLAYERS, 2020

- FIGURE 41 REVENUE ANALYSIS OF TOP 5 MARKET PLAYERS, 2020

- 15.3 COMPANY PRODUCT FOOTPRINT ANALYSIS

- TABLE 154 COMPANY PRODUCT FOOTPRINT

- TABLE 155 COMPANY REGION FOOTPRINT

- 15.4 COMPANY EVALUATION QUADRANT

- 15.4.1 STAR

- 15.4.2 EMERGING LEADER

- 15.4.3 PERVASIVE

- 15.4.4 PARTICIPANT

- FIGURE 42 MARKET COMPETITIVE LEADERSHIP MAPPING, 2020

- 15.5 START-UP/SME EVALUATION QUADRANT

- 15.5.1 PROGRESSIVE COMPANY

- 15.5.2 RESPONSIVE COMPANY

- 15.5.3 STARTING BLOCK

- 15.5.4 DYNAMIC COMPANY

- FIGURE 43 MILITARY BATTERY MARKET (STARTUP) COMPETITIVE LEADERSHIP MAPPING, 2020

- 15.6 COMPETITIVE BENCHMARKING

- 15.6.1 MILITARY BATTERY MARKET: DETAILED LIST OF KEY STARTUP/SMES

- 15.6.2 MILITARY BATTERY MARKET: COMPETITIVE BENCHMARKING OF KEY PLAYERS [STARTUPS/SMES]

- 15.7 COMPETITIVE SCENARIO

- 15.7.1 MARKET EVALUATION FRAMEWORK

- 15.7.2 NEW PRODUCT LAUNCHES AND DEVELOPMENTS

- TABLE 156 NEW PRODUCT LAUNCHES AND DEVELOPMENTS, 2018-2021

- 15.7.3 DEALS

- TABLE 157 CONTRACTS, 2018-2021

- 15.7.4 VENTURES/AGREEMENTS/EXPANSIONS

- TABLE 158 ACQUISITIONS/PARTNERSHIPS/JOINT VENTURES/AGREEMENTS/ EXPANSIONS, 2018-2021

16 COMPANY PROFILES: KEY PLAYERS

- 16.1 INTRODUCTION

- 16.2 KEY PLAYERS

- (Business Overview, Solutions, Products & Services, Key Insights, Recent Developments, MnM View)**

- 16.2.1 ENERSYS

- TABLE 159 ENERSYS: BUSINESS OVERVIEW

- FIGURE 44 ENERSYS: COMPANY SNAPSHOT

- TABLE 160 ENERSYS: DEALS

- TABLE 161 ENERSYS: PRODUCT LAUNCH

- TABLE 162 ENERSYS: OTHERS

- 16.2.2 BAE SYSTEMS PLC

- TABLE 163 BAE SYSTEMS PLC: BUSINESS OVERVIEW

- FIGURE 45 BAE SYSTEMS PLC: COMPANY SNAPSHOT

- 16.2.3 GS YUASA INTERNATIONAL LTD

- TABLE 164 GS YUASA INTERNATIONAL LTD: BUSINESS OVERVIEW

- FIGURE 46 GS YUASA INTERNATIONAL LTD: COMPANY SNAPSHOT

- TABLE 165 GS YUASA INTERNATIONAL LTD: DEALS

- 16.2.4 SAFT (TOTAL)

- TABLE 166 SAFT: BUSINESS OVERVIEW

- FIGURE 47 SAFT (TOTAL): COMPANY SNAPSHOT

- TABLE 167 SAFT (TOTAL): DEALS

- 16.2.5 EXIDE TECHNOLOGIES

- TABLE 168 EXIDE TECHNOLOGIES: BUSINESS OVERVIEW

- TABLE 169 EXIDE TECHNOLOGIES: PRODUCT LAUNCH

- TABLE 170 EXIDE TECHNOLOGIES: DEALS

- 16.2.6 EXIDE INDUSTRIES

- TABLE 171 EXIDE INDUSTRIES: BUSINESS OVERVIEW

- FIGURE 48 EXIDE INDUSTRIES: COMPANY SNAPSHOT

- TABLE 172 EXIDE INDUSTRIES: OTHERS

- 16.2.7 ULTRALIFE CORPORATION

- TABLE 173 ULTRALIFE CORPORATION: BUSINESS OVERVIEW

- FIGURE 49 ULTRALIFE CORPORATION: COMPANY SNAPSHOT

- TABLE 174 ULTRALIFE CORPORATION: DEALS

- 16.2.8 AROTECH CORPORATION

- TABLE 175 AROTECH CORPORATION: BUSINESS OVERVIEW

- TABLE 176 AROTECH CORPORATION: DEALS

- 16.2.9 BREN-TRONICS

- TABLE 177 BREN-TRONICS: BUSINESS OVERVIEW

- TABLE 178 BREN-TRONICS: DEALS

- 16.2.10 EAGLEPICHER TECHNOLOGIES

- TABLE 179 EAGLEPICHER TECHNOLOGIES: BUSINESS OVERVIEW

- TABLE 180 EAGLEPICHER TECHNOLOGIES: DEALS

- 16.2.11 BST SYSTEMS, INC.

- TABLE 181 BST SYSTEMS, INC: BUSINESS OVERVIEW

- TABLE 182 BST SYSTEMS, INC: DEALS

- 16.2.12 CONCORDE

- TABLE 183 CONCORDE: BUSINESS OVERVIEW

- TABLE 184 CONCORDE: DEALS

- 16.2.13 LINCAD

- TABLE 185 LINCAD: BUSINESS OVERVIEW

- TABLE 186 LINCAD: DEALS

- 16.2.14 KOREA SPECIAL BATTERY CO., LTD.

- TABLE 187 KOREA SPECIAL BATTERY CO., LTD.: BUSINESS OVERVIEW

- 16.2.15 ECOBAT BATTERY TECHNOLOGIES

- TABLE 188 ECOBAT BATTERY TECHNOLOGIES: BUSINESS OVERVIEW

- *Details on Business Overview, Solutions, Products & Services, Recent Developments, MnM View might not be captured in case of unlisted companies.

- 16.3 OTHER PLAYERS

- 16.3.1 DENCHI POWER

- 16.3.2 KOKAM

- 16.3.3 MATHEW ASSOCIATES

- 16.3.4 NAVITAS SYSTEMS

- 16.3.5 TELEDYNE TECHNOLOGIES

- 16.3.6 CELL-CON

- 16.3.7 LECLANCHE SA

- 16.3.8 STERLING PLANB ENERGY SOLUTIONS

- 16.3.9 SION POWER

- 16.3.10 LIFELINE BATTERIES

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGE STORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 AVAILABLE CUSTOMIZATIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS