|

|

市場調査レポート

商品コード

1076733

自動試験装置の世界市場:コンポーネント別・種類別・業種別 (半導体製造、自動車・輸送機械、医療、航空宇宙・防衛、家電製品)・地域別 (北米、欧州、アジア太平洋など) の将来予測 (2022年~2027年)Automated Test Equipment Market by Components, Type, Vertical (Semiconductor Fabrication, Automotive and Transportation, Medical, Aerospace and Defense, Consumer Electronics), and Geography (North America, Europe, APAC, RoW) (2022-2027) |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| 自動試験装置の世界市場:コンポーネント別・種類別・業種別 (半導体製造、自動車・輸送機械、医療、航空宇宙・防衛、家電製品)・地域別 (北米、欧州、アジア太平洋など) の将来予測 (2022年~2027年) |

|

出版日: 2022年05月13日

発行: MarketsandMarkets

ページ情報: 英文 226 Pages

納期: 即納可能

|

- 全表示

- 概要

- 目次

世界の自動試験装置 (ATE) の市場規模は、2022年の70億米ドルから、2027年までに88億米ドルに成長すると予測されています。

また、予測期間中に4.7%のCAGRで成長する見通しです。市場の主な促進要因として、自動車産業での技術進歩などが挙げられます。

コンポーネント別ではマスインターコネクトが、種類別では集積回路 (IC) 試験が、最大の市場規模を有しています。地域別に見ると、欧州が最も高いCAGRで成長する見通しです。

当レポートでは、世界の自動試験装置の市場について分析し、市場の基本構造や最新情勢、主な市場促進・抑制要因、市場動向の見通し、コンポーネント別・種類別・業種別・地域別の詳細動向、市場競争の状態、主要企業のプロファイルなどを調査しております。

目次

第1章 イントロダクション

第2章 分析方法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概略

- イントロダクション

- 市場力学

- 市場促進要因

- 市場抑制要因

- 市場機会

- 課題

- バリューチェーン分析

- ポーターのファイブフォース分析

- ATEのエコシステム分析

- 顧客/バイヤーに影響を与える傾向/ディスラプション

- ケーススタディ分析

- テクノロジー分析

- IoT技術の実用化

- ATE装置のレンタルベースでの普及動向

- モジュール型試験装置の傾向

- 5Gネットワークの出現

- 特許分析

- 関税・規制状況

- 貿易分析と関税分析

- 主要な会議とイベント (2022年~2023年)

- 主要な利害関係者と購入基準

第6章 自動試験装置市場:コンポーネント別

- イントロダクション

- 産業用PC

- マスインターコネクト

- ハンドラー/プローバー

- その他

第7章 自動試験装置市場:種類別

- イントロダクション

- 集積回路 (IC) 試験

- プリント回路基板試験

- ハードディスクドライブ試験

- モジュール・その他

第8章 自動試験装置市場:業種別

- イントロダクション

- 半導体製造

- 非接触型試験装置

- 接触型試験装置

- 家電製品

- 自動車・輸送機械

- 航空宇宙・防衛

- 医療

- その他

第9章 地域分析

- イントロダクション

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- フランス

- 英国

- イタリア

- 他の欧州諸国

- アジア太平洋

- 中国

- 日本

- 韓国

- 台湾

- 他のアジア太平洋諸国

- その他の地域

- 中東・アフリカ

- 南米

第10章 競合情勢

- 概要

- 上位5社の収益分析 (今後3年間分)

- 主要企業の戦略/市場獲得戦略

- 市場シェア分析 (2021年)

- 企業評価クアドラント

- 中小企業の評価クアドラント (2021年)

- 競合シナリオ

第11章 企業プロファイル

- 主要企業

- ADVANTEST CORPORATION

- TERADYNE, INC.

- NATIONAL INSTRUMENTS

- CHROMA ATE

- COHU INC.

- ASTRONICS CORPORATION

- STAR TECHNOLOGIES

- ROOS INSTRUMENTS

- MARVIN TEST SOLUTIONS

- OMRON CORPORATION

- その他の企業

- TESEC CORPORATION

- DANAHER

- ESPEC NORTH AMERICA

- JTAG TECHNOLOGIES

- VAUNIX

- JFW INDUSTRIES

- AEMULUS

- FESTO LTD

- NIKON METROLOGY

- CARL ZEISS AG

- VISCOM AG

- KEYSIGHT TECHNOLOGIES

- ARTIFLEX ENGINEERING

- VITROX CORPORATION

- SAKI CORPORATION

- TEST RESEARCH INC. (TRI)

- SHENZHEN J-WIDE ELECTRONICS EQUIPMENT CO., LTD.

- CHINO WORKS AMERICA

第12章 付録

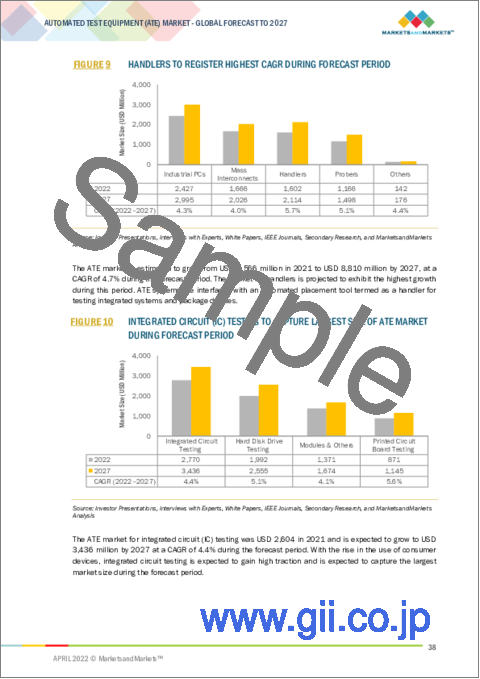

The automated test equipment market is expected to grow from USD7.0 billion in 2022 to USD 8.8 billion by 2027; it is expected to grow at a CAGR of 4.7% during the forecast period. The major driving factors for the growth of the automated test equipmentmarket include the growing advancement in automotive vertical.

Mass Interconnects to have significant market size of automated test equipmentmarket during the forecast period

The mass interconnect systems used in ATEs play the role of a connecting interface between the test instruments and the DUT. The test instruments include PCI eXtension for instruments (PXI), VME eXtension for instruments (VXI), LAN eXtension for instruments (LXI), general-purpose interface bus (GPIB), signal conditioning extensions for instruments (SCXI), and peripheral component interconnect (PCI). In mass interconnect systems, the receiver on the tester side is mated with an interchangeable test adapter (ITA) on the DUT. Mass interconnect systems find scope in aerospace and defense, industrial, as well as automotive applications. They are available in multiple sizes and configurations. They can, hence, be used virtually for any test requirement. The need for a connection between the ATE system and the DUT is ever-increasing, which proves to be a driving factor.

Integrated Circuit (IC) Testingtype to have the largest market size during the forecast period.

The increasing adoption of ICs by mobile device manufacturers, network equipment manufacturers, and telecommunication service providers is expected to drive the growth prospects of testing equipment. Increased investments in R&D, technological advancements in networking and communication, increased manufacturing activities in developing countries, and rise in demand for electronic products have led to an increase in the need for IC testing equipment.

Europe to grow with significant CAGR during the forecast period.

The European ATE market is further segmented into the UK, Germany, France, Italy, and the Rest of Europe.The European semiconductor industry is showing a favorable trend for the growth of fabrication plants and triggering progression for wafer cleaning equipment. Countries such as Germany, the UK, and Italy are showing significant growth potential owing to the presence of giant semiconductor manufacturers such as STMicroelectronics (Switzerland), Infineon Technologies AG (Germany), and X-FAB Silicon Foundries (Germany). Intel Inc. (US) has upgraded and expanded its fabrication capacity in Ireland and Israel, becoming the top consumer of ATE in these countries. The thriving automotive industry in the region acts as an opportunity for the ATE market. The growth of 4G LTE technology in the region and ongoing developments and smaller deployments of the 5G infrastructure is expected to drive the market for ATE in consumer electronics and other verticals.

In the process of determining and verifying the market size for several segments and subsegments gathered through secondary research, extensive primary interviews have been conducted with key officials in the automated test equipmentmarket. Following is the breakup of the profiles of primary participants for the report.

- By Company Type:Tier 1 - 35 %, Tier 2 - 45%, and Tier 3 - 20%

- By Designation:C-Level Executives - 35%,Directors- 25%, and Others - 40%

- By Region:North America- 45%, APAC - 30%, Europe- 20% and RoW - 5%

The automated test equipmentmarket comprises major players such as Advantest Corporation (Japan), Teradyne (US), National Instruments (US), Chroma ATE (Taiwan), Astronics Corporation (US), STAr Technologies (Taiwan), Roos Instruments (US), Marvin Test Solutions (US), Cohu (US), and OMRON Corporation (Japan), TESEC Corporation(Japan), Danaher(US), ESPEC North America(US), JTAG Technologies(Netherlands), Vaunix(US), JFW Industries(US), Aemulus(Malaysia), Festo(Germany), Nikon Metrology(Belgium), Carl Zeiss AG (Germany), Viscom AG(Germany), Keysight Technologies(US), Artiflex Engineering(South Africa), Vitrox Corporation(Malaysia), Saki Corporation(Japan), Test Research Inc. (TRI)(Taiwan), ShenZhen J-wide Electronics Equipment Co., Ltd.(China), CHINO(US).

Research Coverage

The report defines, describes, and forecasts the automated test equipmentmarket based oncomponent, type, verticaland geography. It provides detailed information regarding factors such as drivers, restraints, opportunities, and challenges influencing the growth of the automated test equipmentmarket. It also analyzes competitive developments such as product launches, acquisitions, expansions, contracts, partnerships, and developments carried out by the key players to grow in the market.

Reasons to Buy This Report

The report willhelpleaders/new entrants in the automated test equipmentmarket in the following ways:

1. The report segments the automated test equipmentmarket comprehensively and provides the closest market size estimation for all subsegments across regions.

2. The report will help stakeholders understand the pulse of the market and provide them with information on key drivers, restraints, challenges, and opportunitiesaboutthe automated test equipmentmarket.

3. The report willhelp stakeholders understand their competitorsbetter and gain insights to improve their position in the automated test equipmentmarket. The competitive landscape section describes the competitor ecosystem.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED

- FIGURE 1 AUTOMATED TEST EQUIPMENT MARKET: SEGMENTATION

- FIGURE 2 GEOGRAPHIC SCOPE

- 1.3.2 YEARS CONSIDERED

- 1.4 CURRENCY

- 1.5 LIMITATIONS

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 3 PROCESS FLOW: AUTOMATED TEST EQUIPMENT (ATE) MARKET SIZE ESTIMATION

- FIGURE 4 AUTOMATED TEST EQUIPMENT (ATE) MARKET: RESEARCH DESIGN

- 2.1.1 SECONDARY AND PRIMARY RESEARCH

- 2.1.2 SECONDARY DATA

- 2.1.2.1 Secondary sources

- 2.1.2.2 List of key secondary sources

- 2.1.3 PRIMARY DATA

- 2.1.3.1 Primary sources

- 2.1.3.2 Key industry insight

- 2.1.3.3 Primary interviews with expert

- 2.1.3.4 List of key primary respondent

- 2.1.3.5 Breakdown of primaries

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- 2.2.1.1 Approach for arriving at market size by bottom-up analysis

- FIGURE 5 AUTOMATED TEST EQUIPMENT MARKET: BOTTOM-UP APPROACH

- 2.2.2 TOP-DOWN APPROACH

- 2.2.2.1 Approach for deriving market size by top-down analysis

- FIGURE 6 AUTOMATED TEST EQUIPMENT (ATE) MARKET: TOP-DOWN APPROACH

- 2.2.1 BOTTOM-UP APPROACH

- 2.3 MARKET BREAKDOWN AND DATA TRIANGULATION

- FIGURE 7 DATA TRIANGULATION

- 2.4 RESEARCH ASSUMPTIONS

- 2.5 LIMITATIONS

- 2.6 RISK ASSESSMENT

- TABLE 1 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

- FIGURE 8 IMPACT OF COVID-19 ON AUTOMATED TEST EQUIPMENT (ATE) MARKET

- 3.1 POST-COVID-19 SCENARIO

- TABLE 2 POST-COVID-19 REALISTIC SCENARIO: ATE MARKET, 2022-2027 (USD MILLION)

- 3.2 OPTIMISTIC SCENARIO (POST-COVID-19)

- TABLE 3 OPTIMISTIC SCENARIO (POST-COVID-19): ATE MARKET, 2022-2027 (USD MILLION)

- 3.3 PESSIMISTIC SCENARIO (POST-COVID-19)

- TABLE 4 PESSIMISTIC SCENARIO (POST-COVID-19): ATE MARKET, 2022-2027 (USD MILLION)

- FIGURE 9 HANDLERS TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 10 INTEGRATED CIRCUIT (IC) TESTING TO CAPTURE LARGEST SIZE OF ATE MARKET DURING FORECAST PERIOD

- FIGURE 11 AUTOMOTIVE & TRANSPORTATION VERTICAL TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 12 APAC ACCOUNTED FOR LARGEST SHARE OF ATE MARKET IN 2021

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES IN AUTOMATED TEST EQUIPMENT MARKET

- FIGURE 13 GROWING USE OF ATE IN AUTOMOTIVE AND TRANSPORATION TO FUEL MARKET GROWTH FROM 2022 TO 2027

- 4.2 AUTOMATED TEST EQUIPMENT MARKET, BY TYPE

- FIGURE 14 PRINTED CIRCUIT BOARD TESTING TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- 4.3 AUTOMATED TEST EQUIPMENT MARKET, BY VERTICAL

- FIGURE 15 SEMICONDUCTOR FABRICATION VERTICAL TO HOLD LARGEST SHARE OF ATE MARKET DURING FORECAST PERIOD

- 4.4 AUTOMATES TEST EQUIPMENT MARKET, BY COMPONENT

- FIGURE 16 APAC TO HAVE LARGEST MARKET SIZE FOR INDUSTRIAL PCS DURING FORECAST PERIOD

- 4.5 AUTOMATED TEST EQUIPMENT MARKET, BY REGION (2027)

- FIGURE 17 ATE MARKET TO RECORD HIGHEST CAGR IN ASIA PACIFIC IN 2027

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 18 ATE MARKET: DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Use of ATE reduces manufacturing time and cost

- 5.2.1.2 Decreasing PCB real state and surge in demand for complex integrated circuits (ICs)

- 5.2.1.3 Increasing applications in consumer goods

- 5.2.2 RESTRAINTS

- 5.2.2.1 High cost associated with testers and testing components

- 5.2.2.2 Requirement for new ATE with technological advancements

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Government initiatives to boost semiconductor industry

- 5.2.3.2 Advancements in automotive sector

- 5.2.4 CHALLENGES

- 5.2.4.1 Fluctuations in semiconductor industry's supply chain due to COVID-19

- 5.2.4.2 Difficulty associated with interfacing of DUT

- 5.3 VALUE CHAIN ANALYSIS

- FIGURE 19 ATE MARKET: VALUE CHAIN

- 5.4 PORTER'S FIVE FORCES ANALYSIS

- TABLE 5 ATE MARKET: PORTER'S FIVE FORCES ANALYSIS

- 5.5 ATE ECOSYSTEM ANALYSIS

- FIGURE 20 ATE ECOSYSTEM

- TABLE 6 ATE MARKET: ECOSYSTEM

- 5.6 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS/BUYERS

- FIGURE 21 REVENUE SHIFT FOR ATE MARKET

- 5.7 CASE STUDY ANALYSIS

- 5.7.1 TBG SOLUTIONS

- TABLE 7 TBG SOLUTIONS PROVIDED AUTOMATED TEST SYSTEM TO TEST SEAT BELT QUALITY IN LESSER TIME

- 5.7.2 VIEWPOINT SYSTEMS

- TABLE 8 VIEWPOINT SYSTEMS PROVIDED RELIABLE SENSOR SUBSYSTEM THAT ENSURED UNINTERRUPTED DATA TO CLIENT

- 5.7.3 TBG SOLUTIONS

- TABLE 9 TBG SOLUTIONS PROVIDED WITH TEST SYSTEM THAT TESTED RANGE OF LED PRODUCTS

- 5.8 TECHNOLOGY ANALYSIS

- 5.8.1 COMMERCIALIZATION OF IOT TECHNOLOGY

- 5.8.2 INCLINATION TOWARD ADOPTION OF ATE EQUIPMENT ON RENTAL BASIS

- 5.8.3 TREND OF MODULAR TEST INSTRUMENTS

- 5.8.4 EMERGENCE OF 5G NETWORK

- 5.9 PATENT ANALYSIS

- FIGURE 22 TOP 10 COMPANIES WITH HIGHEST NUMBER OF PATENT APPLICATIONS IN LAST 10 YEARS

- TABLE 10 TOP 10 PATENT OWNERS IN US IN LAST 10 YEARS

- FIGURE 23 NUMBER OF PATENTS GRANTED PER YEAR FROM 2011 TO 2021

- TABLE 11 LIST OF PATENTS

- 5.10 TARIFF AND REGULATORY LANDSCAPE

- 5.10.1 REGULATIONS PERTAINING TO ELECTRIC AND ELECTRONIC TESTING

- TABLE 12 REGULATIONS IN US

- 5.10.2 STANDARDS RELATED TO ELECTRICAL EQUIPMENT

- TABLE 13 STANDARD AND DESCRIPTION

- 5.10.3 RESTRICTION OF HAZARDOUS SUBSTANCES (ROHS) AND WASTE ELECTRICAL AND ELECTRONIC EQUIPMENT (WEEE)

- 5.11 TRADE ANALYSIS AND TARIFF ANALYSIS

- 5.11.1 TRADE ANALYSIS

- 5.11.1.1 Trade data for HS code 9030

- FIGURE 24 IMPORT DATA FOR HS CODE 9030, BY COUNTRY, 2017-2021 (USD THOUSAND)

- FIGURE 25 EXPORT DATA FOR HS CODE 9030, BY COUNTRY, 2017-2021 (USD THOUSAND)

- 5.11.1.2 Trade data for HS code 903141

- FIGURE 26 IMPORT DATA FOR HAS CODE 903141, BY COUNTRY, 2017-2021 (USD THOUSAND)

- FIGURE 27 EXPORT DATA FOR HS CODE 903041, BY COUNTRY, 2017-2021 (USD THOUSAND)

- 5.11.1 TRADE ANALYSIS

- 5.12 KEY CONFERENCES AND EVENTS IN 2022-2023

- TABLE 14 ATE MARKET: DETAILED LIST OF CONFERENCES ND EVENTS

- 5.13 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.13.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 28 INFLUENCE OF STAKEHOLDERS IN BUYING PROCESS FOR TOP 3 VERTICALS

- TABLE 15 INFLUENCE OF STAKEHOLDERS IN BUYING PROCESS FOR TOP 3 VERTICALS (%)

6 AUTOMATED TEST EQUIPMENT MARKET, BY COMPONENT

- 6.1 INTRODUCTION

- FIGURE 29 AUTOMATED TEST EQUIPMENT MARKET, BY COMPONENT

- FIGURE 30 HANDLERS TO WITNESS HIGHEST GROWTH DURING FORECAST PERIOD

- TABLE 16 AUTOMATED TEST EQUIPMENT MARKET, BY COMPONENT, 2018-2021 (USD MILLION)

- TABLE 17 AUTOMATED TEST EQUIPMENT MARKET, BY COMPONENT, 2022-2027 (USD MILLION)

- 6.2 INDUSTRIAL PCS

- 6.2.1 DEMAND FOR INDUSTRIAL PCS IS INCREASING DUE TO THEIR EFFICIENT DESIGN

- TABLE 18 INDUSTRIAL PCS: AUTOMATED TEST EQUIPMENT MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 19 INDUSTRIAL PCS: AUTOMATED TEST EQUIPMENT MARKET, BY TYPE, 2022-2027 (USD MILLION)

- TABLE 20 INDUSTRIAL PCS: AUTOMATED TEST EQUIPMENT MARKET, BY REGION, 2018-2021 (USD MILLION)

- TABLE 21 INDUSTRIAL PC: AUTOMATED TEST EQUIPMENT MARKET, BY REGION, 2022-2027 (USD MILLION)

- 6.3 MASS INTERCONNECTS

- 6.3.1 AEROSPACE AND DEFENSE INDUSTRIES TO FUEL DEMAND FOR MASS INTERCONNECT SYSTEMS

- TABLE 22 MASS INTERCONNECTS: AUTOMATED TEST EQUIPMENT MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 23 MASS INTERCONNECTS: AUTOMATED TEST EQUIPMENT MARKET, BY TYPE, 2022-2027 (USD MILLION)

- TABLE 24 MASS INTERCONNECTS: AUTOMATED TEST EQUIPMENT MARKET, BY REGION, 2018-2021 (USD MILLION)

- TABLE 25 MASS INTERCONNECTS: AUTOMATED TEST EQUIPMENT MARKET, BY REGION, 2022-2027 (USD MILLION)

- 6.4 HANDLERS/PROBERS

- 6.4.1 HANDLERS

- 6.4.1.1 Handlers help in sorting different types of packages available in ICs

- TABLE 26 HANDLERS: AUTOMATED TEST EQUIPMENT MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 27 HANDLERS: AUTOMATED TEST EQUIPMENT MARKET, BY TYPE, 2022-2027 (USD MILLION)

- TABLE 28 HANDLERS: AUTOMATED TEST EQUIPMENT MARKET, BY REGION, 2018-2021 (USD MILLION)

- TABLE 29 HANDLERS: AUTOMATED TEST EQUIPMENT MARKET, BY REGION, 2022-2027(USD MILLION)

- 6.4.2 PROBERS

- 6.4.2.1 Probers act as interface between wafers and automated test equipment

- TABLE 30 PROBERS: AUTOMATED TEST EQUIPMENT MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 31 PROBERS: AUTOMATED TEST EQUIPMENT MARKET, BY TYPE, 2022-2027 (USD MILLION)

- TABLE 32 PROBERS: AUTOMATED TEST EQUIPMENT MARKET, BY REGION, 2018-2021 (USD MILLION)

- TABLE 33 PROBERS: AUTOMATED TEST EQUIPMENT MARKET, BY REGION, 2022-2027 (USD MILLION)

- 6.4.1 HANDLERS

- 6.5 OTHERS

- TABLE 34 OTHERS: AUTOMATED TEST EQUIPMENT MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 35 OTHERS: AUTOMATED TEST EQUIPMENT MARKET, BY TYPE, 2022-2027 (USD MILLION)

- TABLE 36 OTHERS: AUTOMATED TEST EQUIPMENT MARKET, BY REGION, 2018-2021 (USD MILLION)

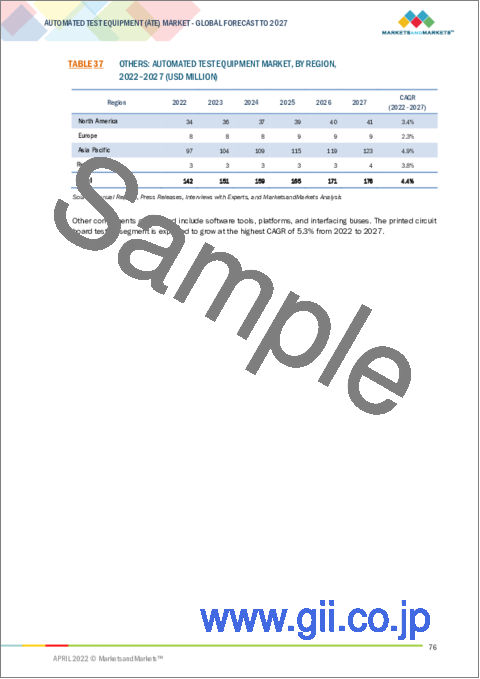

- TABLE 37 OTHERS: AUTOMATED TEST EQUIPMENT MARKET, BY REGION, 2022-2027 (USD MILLION)

7 AUTOMATED TEST EQUIPMENT MARKET, BY TYPE

- 7.1 INTRODUCTION

- FIGURE 31 AUTOMATED TEST EQUIPMENT MARKET, BY TYPE

- FIGURE 32 PRINTED CIRCUIT BOARD TESTING TO REGISTER HIGHEST GROWTH DURING FORECAST PERIOD

- TABLE 38 AUTOMATED TEST EQUIPMENT MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 39 AUTOMATED TEST EQUIPMENT MARKET, BY TYPE, 2022-2027 (USD MILLION)

- 7.2 INTEGRATED CIRCUIT (IC) TESTING

- 7.2.1 INCREASING USE OF ICS IN CONSUMER ELECTRONICS TO DRIVE DEMAND FOR IC TESTING

- TABLE 40 INTEGRATED CIRCUIT TESTING: AUTOMATED TEST EQUIPMENT MARKET, BY COMPONENT, 2018-2021 (USD MILLION)

- TABLE 41 INTEGRATED CIRCUIT TESTING: AUTOMATED TEST EQUIPMENT MARKET, BY COMPONENT, 2022-2027 (USD MILLION)

- TABLE 42 INTEGRATED CIRCUIT TESTING: AUTOMATED TEST EQUIPMENT MARKET, BY REGION, 2018-2021 (USD MILLION)

- TABLE 43 INTEGRATED CIRCUIT TESTING: AUTOMATED TEST EQUIPMENT MARKET, BY REGION, 2022-2027 (USD MILLION)

- 7.3 PRINTED CIRCUIT BOARD TESTING

- 7.3.1 COMPLEX PCBS TO DRIVE DEMAND FOR AUTOMATED TEST EQUIPMENT

- TABLE 44 PRINTED CIRCUIT BOARD TESTING: AUTOMATED TEST EQUIPMENT MARKET, BY COMPONENT, 2018-2021 (USD MILLION)

- TABLE 45 PRINTED CIRCUIT BOARD TESTING: AUTOMATED TEST EQUIPMENT MARKET, BY COMPONENT, 2022-2027 (USD MILLION)

- TABLE 46 PRINTED CIRCUIT BOARD TESTING: AUTOMATED TEST EQUIPMENT MARKET, BY REGION, 2018-2021 (USD MILLION)

- TABLE 47 PRINTED CIRCUIT BOARD TESTING: AUTOMATED TEST EQUIPMENT MARKET, BY REGION, 2022-2027 (USD MILLION)

- 7.4 HARD DISK DRIVE TESTING

- 7.4.1 INCREASE IN STORAGE DEMAND TO FUEL NEED FOR HARD DISK DRIVE TESTING

- TABLE 48 HARD DISK DRIVE TESTING: AUTOMATED TEST EQUIPMENT MARKET, BY COMPONENT, 2018-2021 (USD MILLION)

- TABLE 49 HARD DISK DRIVE TESTING: AUTOMATED TEST EQUIPMENT MARKET, BY COMPONENT, 2022-2027 (USD MILLION)

- TABLE 50 HARD DISK DRIVE TESTING: AUTOMATED TEST EQUIPMENT MARKET, BY REGION, 2018-2021 (USD MILLION)

- TABLE 51 HARD DISK DRIVE TESTING: AUTOMATED TEST EQUIPMENT MARKET, BY REGION, 2022-2027 (USD MILLION)

- 7.5 MODULES & OTHERS

- TABLE 52 MODULES & OTHERS: AUTOMATED TEST EQUIPMENT MARKET, BY COMPONENT, 2018-2021 (USD MILLION)

- TABLE 53 MODULES & OTHERS: AUTOMATED TEST EQUIPMENT MARKET, BY COMPONENT, 2022-2027 (USD MILLION)

- TABLE 54 MODULES & OTHERS: AUTOMATED TEST EQUIPMENT MARKET, BY REGION, 2018-2021 (USD MILLION)

- TABLE 55 MODULES & OTHERS: AUTOMATED TEST EQUIPMENT MARKET, BY REGION, 2022-2027 (USD MILLION)

8 AUTOMATED TEST EQUIPMENT MARKET, BY VERTICAL

- 8.1 INTRODUCTION

- FIGURE 33 AUTOMATED TEST EQUIPMENT MARKET, BY VERTICAL

- TABLE 56 AUTOMATED TEST EQUIPMENT MARKET, BY VERTICAL, 2018-2021 (USD MILLION)-

- TABLE 57 AUTOMATED TEST EQUIPMENT MARKET, BY VERTICAL, 2022-2027 (USD MILLION)

- 8.2 SEMICONDUCTOR FABRICATION

- 8.2.1 INCREASING CHIP SHORTAGE TO DRIVE DEMAND FOR ATE FROM SEMICONDUCTOR FABRICATION FACILITIES

- TABLE 58 SEMICONDUCTOR FABRICATION: AUTOMATED TEST EQUIPMENT MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 59 SEMICONDUCTOR FABRICATION: AUTOMATED TEST EQUIPMENT MARKET, BY TYPE, 2022-2027 (USD MILLION)

- TABLE 60 SEMICONDUCTOR FABRICATION: AUTOMATED TEST EQUIPMENT MARKET, BY REGION, 2018-2021 (USD MILLION)

- TABLE 61 SEMICONDUCTOR FABRICATION: AUTOMATED TEST EQUIPMENT MARKET, BY REGION, 2022-2027 (USD MILLION)

- 8.2.2 NON-CONTACT TEST EQUIPMENT

- 8.2.2.1 Automated optical inspection (AOI)

- 8.2.2.2 Automated X-ray inspection (AXI)

- TABLE 62 NON-CONTACT TEST EQUIPMENT MARKET, BY TECHNOLOGY, 2018-2021 (USD MILLION)

- TABLE 63 NON-CONTACT TEST EQUIPMENT MARKET, BY TECHNOLOGY, 2022-2027 (USD MILLION)

- 8.2.3 CONTACT TEST EQUIPMENT

- 8.3 CONSUMER ELECTRONICS

- 8.3.1 INCREASING CONSUMER ELECTRONICS DEVICE MANUFACTURING CREATING DEMAND FOR ATE

- TABLE 64 CONSUMER ELECTRONICS: AUTOMATED TEST EQUIPMENT MARKET, BY REGION, 2018-2021 (USD MILLION)

- TABLE 65 CONSUMER ELECTRONICS: AUTOMATED TEST EQUIPMENT MARKET, BY REGION, 2022-2027 (USD MILLION)

- 8.4 AUTOMOTIVE AND TRANSPORTATION

- 8.4.1 INCORPORATION OF SOPHISTICATED ELECTRONIC SYSTEMS IN VEHICLES FUELING DEMAND FOR ATE

- TABLE 66 AUTOMOTIVE & TRANSPORTATION: AUTOMATED TEST EQUIPMENT MARKET, BY REGION, 2018-2021 (USD MILLION)

- TABLE 67 AUTOMOTIVE & TRANSPORTATION: AUTOMATED TEST EQUIPMENT MARKET, BY REGION, 2022-2027 (USD MILLION)

- 8.5 AEROSPACE & DEFENSE

- 8.5.1 AEROSPACE & DEFENSE INDUSTRY USES ATE FOR RADAR AND ELECTRONIC WARFARE EQUIPMENT

- TABLE 68 AEROSPACE & DEFENSE: AUTOMATED TEST EQUIPMENT MARKET, BY REGION, 2018-2021 (USD MILLION)

- TABLE 69 AEROSPACE & DEFENSE: AUTOMATED TEST EQUIPMENT MARKET, BY REGION, 2022-2027 (USD MILLION)

- 8.6 MEDICAL

- 8.6.1 NEED TO ENHANCE EFFICIENCY AND ACCURACY OF MEDICAL DEVICES ACCELERATES DEMAND FOR ATE

- TABLE 70 MEDICAL: AUTOMATED TEST EQUIPMENT MARKET, BY REGION, 2018-2021 (USD MILLION)

- TABLE 71 MEDICAL: AUTOMATED TEST EQUIPMENT MARKET, BY REGION, 2022-2027 (USD MILLION)

- 8.7 OTHERS

- TABLE 72 OTHERS: AUTOMATED TEST EQUIPMENT MARKET, BY REGION, 2018-2021 (USD MILLION)

- TABLE 73 OTHERS: AUTOMATED TEST EQUIPMENT MARKET, BY REGION, 2022-2027 (USD MILLION)

9 REGIONAL ANALYSIS

- 9.1 INTRODUCTION

- FIGURE 34 AUTOMATED TEST EQUIPMENT MARKET IN CHINA TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 74 AUTOMATED TEST EQUIPMENT MARKET, BY REGION, 2018-2021 (USD MILLION)

- TABLE 75 AUTOMATED TEST EQUIPMENT MARKET, BY REGION, 2022-2027 (USD MILLION)

- 9.2 NORTH AMERICA

- FIGURE 35 NORTH AMERICA: AUTOMATED TEST EQUIPMENT MARKET SNAPSHOT

- TABLE 76 NORTH AMERICA: ATE MARKET, BY COUNTRY, 2018-2021 (USD MILLION)

- TABLE 77 NORTH AMERICA: ATE MARKET, BY COUNTRY, 2022-2027 (USD MILLION)

- TABLE 78 NORTH AMERICA: ATE MARKET, BY VERTICAL, 2018-2021 (USD MILLION)

- TABLE 79 NORTH AMERICA: ATE MARKET, BY VERTICAL, 2022-2027 (USD MILLION)

- 9.2.1 US

- 9.2.1.1 Surging adoption of electric vehicles to garner lucrative opportunities for ATE market

- TABLE 80 US: ATE MARKET, BY VERTICAL, 2018-2021 (USD MILLION)

- TABLE 81 US: ATE MARKET, BY VERTICAL, 2022-2027(USD MILLION)

- 9.2.2 CANADA

- 9.2.2.1 Increasing initiatives and investments by government to drive market in Canada

- TABLE 82 CANADA: ATE MARKET, BY VERTICAL, 2018-2021 (USD MILLION)

- TABLE 83 CANADA: ATE MARKET, BY VERTICAL, 2022-2027 (USD MILLION)

- 9.2.3 MEXICO

- 9.2.3.1 Growing development in IoT and 5G to boost market

- TABLE 84 MEXICO: ATE MARKET, BY VERTICAL, 2018-2021 (USD MILLION)

- TABLE 85 MEXICO: ATE MARKET, BY VERTICAL, 2022-2027 (USD MILLION)

- FIGURE 36 IMPACT OF COVID-19 ON NORTH AMERICAN ATE MARKET

- TABLE 86 PRE-COVID-19 & POST-COVID-19 SCENARIO: ATE MARKET IN NORTH AMERICA, 2022-2027 (USD MILLION)

- 9.3 EUROPE

- FIGURE 37 EUROPE: AUTOMATED TESTING EQUIPMENT MARKET SNAPSHOT

- TABLE 87 EUROPE: ATE MARKET, BY COUNTRY, 2018-2021 (USD MILLION)

- TABLE 88 EUROPE: ATE MARKET, BY COUNTRY, 2022-2027 (USD MILLION)

- TABLE 89 EUROPE: ATE MARKET, BY VERTICAL, 2018-2021 (USD MILLION)

- TABLE 90 EUROPE: ATE MARKET, BY VERTICAL, 2022-2027 (USD MILLION)

- 9.3.1 GERMANY

- 9.3.1.1 Increasing demand for ADAS to create opportunities for ATE market

- TABLE 91 GERMANY: ATE MARKET, BY VERTICAL, 2018-2021 (USD MILLION)

- TABLE 92 GERMANY: ATE MARKET, BY VERTICAL, 2022-2027 (USD MILLION)

- 9.3.2 FRANCE

- 9.3.2.1 Presence of major aerospace companies to boost market growth

- TABLE 93 FRANCE: ATE MARKET, BY VERTICAL, 2018-2021 (USD MILLION)

- TABLE 94 FRANCE: ATE MARKET, BY VERTICAL, 2022-2027 (USD MILLION)

- 9.3.3 UK

- 9.3.3.1 Growing medical vertical to propel demand for ATE

- TABLE 95 UK: ATE MARKET, BY VERTICAL, 2018-2021 (USD MILLION)

- TABLE 96 UK: ATE MARKET, BY VERTICAL, 2022-2027 (USD MILLION)

- 9.3.4 ITALY

- 9.3.4.1 Increase in number of semiconductor manufacturing fabrication plants to accelerate ATE market

- TABLE 97 ITALY: ATE MARKET, BY VERTICAL, 2018-2021 (USD MILLION)

- TABLE 98 ITALY: ATE MARKET, BY VERTICAL, 2022-2027 (USD MILLION)

- 9.3.5 REST OF EUROPE

- 9.3.6 IMPACT OF COVID-19 ON EUROPEAN ATE MARKET

- TABLE 99 PRE-COVID-19 & POST-COVID19 SCENARIO: ATE MARKET IN EUROPE, 2022-2027 (USD MILLION)

- 9.4 ASIA PACIFIC

- FIGURE 38 ASIA PACIFIC: AUTOMATED TEST EQUIPMENT MARKET SNAPSHOT

- TABLE 100 ASIA PACIFIC: ATE MARKET, BY COUNTRY, 2018-2021 (USD MILLION)

- TABLE 101 ASIA PACIFIC: ATE MARKET, BY COUNTRY, 2022-2027 (USD MILLION)

- TABLE 102 ASIA PACIFIC: ATE MARKET, BY VERTICAL, 2018-2021 (USD MILLION)

- TABLE 103 ASIA PACIFIC: ATE MARKET, BY VERTICAL, 2022-2027 (USD MILLION)

- 9.4.1 CHINA

- 9.4.1.1 Rise of medical equipment manufacturing to fuel demand for automated test equipment in coming years

- TABLE 104 CHINA: ATE MARKET, BY VERTICAL, 2018-2021 (USD MILLION)

- TABLE 105 CHINA: ATE MARKET, BY VERTICAL, 2022-2027 (USD MILLION)

- 9.4.2 JAPAN

- 9.4.2.1 Increase in demand for consumer electronics and automotive to boost ATE market

- TABLE 106 JAPAN: ATE MARKET, BY VERTICAL, 2018-2021 (USD MILLION)

- TABLE 107 JAPAN: ATE MARKET, BY VERTICAL, 2022-2027 (USD MILLION)

- 9.4.3 SOUTH KOREA

- 9.4.3.1 Significant development in manufacturing sector to drive market growth

- TABLE 108 SOUTH KOREA: ATE MARKET, BY VERTICAL, 2018-2021 (USD MILLION)

- TABLE 109 SOUTH KOREA: ATE MARKET, BY VERTICAL, 2022-2027 (USD MILLION)

- 9.4.4 TAIWAN

- 9.4.4.1 Growth of automotive and transportation vertical to drive demand for ATE

- TABLE 110 TAIWAN: ATE MARKET, BY VERTICAL, 2018-2021 (USD MILLION)

- TABLE 111 TAIWAN: ATE MARKET, BY VERTICAL, 2022-2027 (USD MILLION)

- 9.4.5 REST OF APAC

- 9.4.6 IMPACT OF COVID-19 ON ATE MARKET IN ASIA PACIFIC

- TABLE 112 PRE-COVID-19 & POST-COVID-19 SCENARIO: ATE MARKET IN ASIA PACIFIC, 2022-2027 (USD MILLION)

- 9.5 ROW

- FIGURE 39 ROW: AUTOMATED TEST EQUIPMENT MARKET SNAPSHOT

- TABLE 113 ROW: ATE MARKET, BY REGION, 2018-2021 (USD MILLION)

- TABLE 114 ROW: ATE MARKET, BY REGION, 2022-2027 (USD MILLION)

- TABLE 115 ROW: ATE MARKET, BY VERTICAL, 2018-2021 (USD MILLION)

- TABLE 116 ROW: ATE MARKET, BY VERTICAL, 2022-2027 (USD MILLION)

- 9.5.1 MIDDLE EAST & AFRICA

- 9.5.1.1 Favorable government initiatives and high military investments to boost market growth

- 9.5.2 SOUTH AMERICA

- 9.5.2.1 High adoption of wireless communication to enhance market growth

- 9.5.3 IMPACT OF COVID-19 ON ATE MARKET IN ROW

- TABLE 117 PRE-COVID-19 & POST-COVID-19 SCENARIO: ATE MARKET IN ROW, 2022-2027 (USD MILLION)

10 COMPETITIVE LANDSCAPE

- 10.1 OVERVIEW

- 10.2 TOP FIVE PLAYERS - THREE-YEAR COMPANY REVENUE ANALYSIS

- FIGURE 40 REVENUE ANALYSIS, 2019-2021 (USD BILLION)

- 10.3 KEY PLAYER STRATEGIES/RIGHT TO WIN

- TABLE 118 KEY STRATEGIES OF TOP PLAYERS IN ATE MARKET

- 10.4 MARKET SHARE ANALYSIS (2021)

- TABLE 119 ATE MARKET: MARKET SHARE ANALYSIS

- FIGURE 41 MARKET SHARE ANALYSIS: ATE MARKET, 2021

- 10.5 COMPANY EVALUATION QUADRANT, 2021

- 10.5.1 STAR

- 10.5.2 PERVASIVE

- 10.5.3 EMERGING LEADER

- 10.5.4 PARTICIPANT

- FIGURE 42 ATE MARKET: COMPANY EVALUATION QUADRANT, 2021

- 10.5.5 COMPANY FOOTPRINT

- TABLE 120 COMPANY FOOTPRINT: AUTOMATED TEST EQUIPMENT MARKET

- TABLE 121 COMPANY VERTICAL FOOTPRINT: AUTOMATED TEST EQUIPMENT MARKET

- TABLE 122 COMPANY TYPE FOOTPRINT: AUTOMATED TEST EQUIPMENT MARKET

- TABLE 123 COMPANY REGION FOOTPRINT: AUTOMATED TEST EQUIPMENT(ATE) MARKET

- 10.6 SMALL AND MEDIUM ENTERPRISE (SME) EVALUATION QUADRANT, 2021

- 10.6.1 PROGRESSIVE COMPANY

- 10.6.2 RESPONSIVE COMPANY

- 10.6.3 DYNAMIC COMPANY

- 10.6.4 STARTING BLOCK

- FIGURE 43 ATE MARKET: SME EVALUATION QUADRANT, 2020

- TABLE 124 ATE MARKET: DETAILED LIST OF KEY STARTUPS/SMES

- 10.7 COMPETITIVE SCENARIO

- TABLE 125 ATE MARKET: PRODUCT LAUNCHES, JANUARY 2020 TO JANUARY 2022

- TABLE 126 ATE MARKET: DEALS, JANUARY 2020 TO JANUARY 2022

11 COMPANY PROFILES

- (Business Overview, Products Offered, Recent Developments, COVID-19-related Developments, and MnM View)**

- 11.1 KEY PLAYERS

- 11.1.1 ADVANTEST CORPORATION

- TABLE 127 ADVANTEST CORPORATION: BUSINESS OVERVIEW

- FIGURE 44 ADVANTEST CORPORATION: COMPANY SNAPSHOT

- TABLE 128 ADVANTEST CORPORATION: PRODUCTS OFFERED

- TABLE 129 ADVANTEST CORPORATION: PRODUCT LAUNCHES

- TABLE 130 ADVANTEST CORPORATION: DEALS

- TABLE 131 ADVANTEST CORPORATION: OTHERS

- 11.1.2 TERADYNE, INC.

- TABLE 132 TERADYNE, INC.: BUSINESS OVERVIEW

- FIGURE 45 TERADYNE, INC.: COMPANY SNAPSHOT

- TABLE 133 TERADYNE, INC.: PRODUCTS OFFERED

- TABLE 134 TERADYNE, INC.: PRODUCT LAUNCHES

- TABLE 135 TERADYNE, INC.: DEALS

- TABLE 136 TERADYNE, INC.: OTHERS

- 11.1.3 NATIONAL INSTRUMENTS

- TABLE 137 NATIONAL INSTRUMENTS: BUSINESS OVERVIEW

- FIGURE 46 NATIONAL INSTRUMENTS: COMPANY SNAPSHOT

- TABLE 138 NATIONAL INSTRUMENTS: PRODUCTS OFFERED

- TABLE 139 NATIONAL INSTRUMENTS: PRODUCT LAUNCHES

- TABLE 140 NATIONAL INSTRUMENTS: DEALS

- TABLE 141 NATIONAL INSTRUMENTS: OTHERS

- 11.1.4 CHROMA ATE

- TABLE 142 CHROMA ATE: BUSINESS OVERVIEW

- FIGURE 47 CHROMA ATE: COMPANY SNAPSHOT

- TABLE 143 CHROMA ATE: PRODUCTS OFFERED

- TABLE 144 CHROMA ATE: PRODUCT LAUNCHES

- TABLE 145 CHROMA ATE: DEALS

- TABLE 146 CHROMA ATE: OTHERS

- 11.1.5 COHU INC.

- TABLE 147 COHU INC.: BUSINESS OVERVIEW

- FIGURE 48 COHU INC.: COMPANY SNAPSHOT

- TABLE 148 COHU INC.: PRODUCTS OFFERED

- TABLE 149 COHU INC.: PRODUCT LAUNCHES

- TABLE 150 COHU INC.: DEALS

- TABLE 151 COHU INC.: OTHERS

- 11.1.6 ASTRONICS CORPORATION

- TABLE 152 ASTRONICS CORPORATION: BUSINESS OVERVIEW

- FIGURE 49 ASTRONICS CORPORATION: COMPANY SNAPSHOT

- TABLE 153 ASTRONICS CORPORATION: PRODUCTS OFFERED

- TABLE 154 ASTRONICS CORPORATION: PRODUCT LAUNCHES

- TABLE 155 ASTRONICS CORPORATION: DEALS

- TABLE 156 ASTRONICS CORPORATION: OTHERS

- 11.1.7 STAR TECHNOLOGIES

- TABLE 157 STAR TECHNOLOGIES: BUSINESS OVERVIEW

- TABLE 158 STAR TECHNOLOGIES: PRODUCTS OFFERED

- TABLE 159 STAR TECHNOLOGIES: PRODUCT LAUNCHES

- TABLE 160 STAR TECHNOLOGIES: OTHERS

- 11.1.8 ROOS INSTRUMENTS

- TABLE 161 ROOS INSTRUMENTS: BUSINESS OVERVIEW

- TABLE 162 ROOS INSTRUMENTS: PRODUCTS OFFERED

- TABLE 163 ROOS INSTRUMENTS: PRODUCT LAUNCHES

- 11.1.9 MARVIN TEST SOLUTIONS

- TABLE 164 MARVIN TEST SOLUTIONS: BUSINESS OVERVIEW

- TABLE 165 MARVIN TEST SOLUTIONS: PRODUCTS OFFERED

- TABLE 166 MARVIN TEST SOLUTIONS: PRODUCT LAUNCHES

- TABLE 167 MARVIN TEST SOLUTIONS: OTHERS

- 11.1.10 OMRON CORPORATION

- TABLE 168 OMRON CORPORATION: BUSINESS OVERVIEW

- FIGURE 50 OMRON CORPORATION: COMPANY SNAPSHOT

- TABLE 169 OMRON CORPORATION: PRODUCTS OFFERED

- TABLE 170 OMRON CORPORATION: PRODUCT LAUNCHES

- TABLE 171 OMRON CORPORATION: OTHERS

- 11.2 OTHER KEY PLAYERS

- 11.2.1 TESEC CORPORATION

- 11.2.2 DANAHER

- 11.2.3 ESPEC NORTH AMERICA

- 11.2.4 JTAG TECHNOLOGIES

- 11.2.5 VAUNIX

- 11.2.6 JFW INDUSTRIES

- 11.2.7 AEMULUS

- 11.2.8 FESTO LTD

- 11.2.9 NIKON METROLOGY

- 11.2.10 CARL ZEISS AG

- 11.2.11 VISCOM AG

- 11.2.12 KEYSIGHT TECHNOLOGIES

- 11.2.13 ARTIFLEX ENGINEERING

- 11.2.14 VITROX CORPORATION

- 11.2.15 SAKI CORPORATION

- 11.2.16 TEST RESEARCH INC. (TRI)

- 11.2.17 SHENZHEN J-WIDE ELECTRONICS EQUIPMENT CO., LTD.

- 11.2.18 CHINO WORKS AMERICA

- Business Overview, Products Offered, Recent Developments, COVID-19-related Developments, and MnM View might not be captured in case of unlisted companies.

12 APPENDIX

- 12.1 DISCUSSION GUIDE

- 12.2 KNOWLEDGE STORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 12.3 AVAILABLE CUSTOMIZATION

- 12.4 RELATED REPORTS

- 12.5 AUTHOR DETAILS