|

|

市場調査レポート

商品コード

1295363

薄型ウエハー市場-2023年から2028年までの予測Thin Wafer Market - Forecasts from 2023 to 2028 |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| 薄型ウエハー市場-2023年から2028年までの予測 |

|

出版日: 2023年06月07日

発行: Knowledge Sourcing Intelligence

ページ情報: 英文 132 Pages

納期: 即日から翌営業日

|

- 全表示

- 概要

- 目次

薄型ウエハー市場のCAGRは4.03%で、2021年の84億400万米ドルから2028年には110億8,500万米ドルに成長すると推定されます。

薄型ウエハー市場は、スマートフォンやスマートウェアラブルデバイスの需要増とこの分野の技術革新により拡大しています。都市化の急速な進展と高い可処分所得により、スマートフォン、LED、スマートTVなどの電子機器の需要が増加しています。最先端のガジェットに対する需要の高まりに対応するため、アップル、サムスン、Redmi、Oneplusなど、多くのトップ家電メーカーが開発と研究に多額の投資を行っています。さらに、スリムなボディを持つスマートTVやスマートウォッチなど、その他の薄型デバイスに対する需要の増加が、薄型ウエハーの注目すべき需要を牽引すると予想されます。各国による研究開発活動への投資の増加は、今後数年間の市場成長を急増させると予想されます。

太陽光発電の採用増加と技術開拓が市場の成長を後押しします。

太陽光発電の採用増加により、薄型ウエハー市場は今後数年で急成長が見込まれます。人間の二酸化炭素排出量の増加により、環境に対する深刻な懸念が高まっており、太陽光発電の採用を含む持続可能なエネルギー生産手段の開発に対する需要が高まっています。薄型ウエハーは、太陽電池の生産に不可欠な原材料であるため、市場での需要が増加しています。例えば、2022年11月、IIT Mandiの研究者により、LEDやCFLの家庭用光源からの光にさらされると発電する可能性のある新しい光起電力材料が作られました。この研究は、現代文化におけるloT技術の普及を裏付けています。IoTデバイスは、携帯電話やホームオートメーションなど、さまざまな形態のリアルタイムデータを必要とするシステムで常用されるようになっています。これらのデバイスは、電源ケーブルの助けを借りることなく、自ら発電する独立したものでなければなりません。これらの機器は現在、主電池と二次電池の両方から電力を供給されています。どのバッテリーも寿命は有限であり、費用対効果も環境面でも有益ではありません。

民生用電子機器や照明業界における幅広い用途でLEDの使用が増加していることから、LEDへの注目が高まっており、効率的な半導体への需要が高まっています。環境問題への関心が高まり、さまざまな国で効果的なエネルギー効率化プログラムが実施されるようになったことで、LED市場の需要が大幅に増加しています。例えば、インド政府はエネルギー節約に役立つLED照明の大量調達を開始しました。これにより、LEDの薄型ウエハー採用が促進され、効率的なLEDソリューションの需要が高まり、商業/産業分野での太陽光発電の容量が増加しています。例えば、国際エネルギー協会の2022年報告書によると、太陽光発電の純容量は2021年の27GWから2022年には30GWに増加し、これが市場における薄型ウエハーの需要増加につながっています。

さらに、自動車産業におけるインダストリー4.0やloT、Alなどの技術の導入は、薄型ウエハー市場の拡大に大きな影響を与えると思われます。コネクテッドカーに対する需要の高まりは、新たな技術開発につながります。さらに、タッチフリーのヒューマンマシンインターフェイスのような現在の動向が自動車産業に革命をもたらしている結果、コネクテッドカーの関連性が拡大しています。アダプティブクルーズコントロール、インテリジェント駐車支援システム、ADAS(先進運転支援システム)などの新技術の登場は、市場の拡大にさらに拍車をかけると思われます。

さらに、先進国、新興国を問わず、政府は薄型ウエハー半導体の生産に多額の投資を行っています。半導体の成長は、主要企業の協力や研究開発費の増加にも助けられています。例えば、ドイツ政府は半導体製造の拠点を取り戻すために30億ユーロ近くを費やしています。IoTとインダストリー4.0による半導体ニーズの高まりがこの投資の原動力となっており、生産施設は最新の動向に対応するために十分なマイクロチップへのアクセスを向上させています。

市場動向:

- アルゴンヌ国立研究所のデータ別と、2023年3月に米国で販売されたハイブリッド電気自動車は93,218台で、2022年3月の販売台数の21.7%を占め、さらに米国で販売されたプラグイン自動車は合計100,605台で、その内訳はBEVが81,346台、PHEVが19,259台でした。国家エネルギー局が提供したデータによると、2022年の中国全体の太陽光発電容量は392.61GWに達し、2021年の306.GWと比較して28.1%の大幅な増加を示しました。さらに、同出典によると、同年には87.41GWが追加設置されました。

予測期間中、アジア太平洋地域が市場で最大のシェアを占めると予想されています。

地域別に見ると、薄型ウエハーの世界市場は、アメリカ、欧州・中東・アフリカ、アジア太平洋に分けられます。アジア太平洋地域は、予測期間中に大きなシェアを占め、最も速い速度で成長すると予測されています。インド、中国、韓国、ベトナム、タイなどの工業化により、これらの国々では消費者向け電子機器製造ユニットが急増し、市場を下支えしています。さらに、可処分所得の増加により、スマートフォンなどのスマートデバイスの普及が加速しており、これも市場の見通しを支えています。さらに、良好な気候条件が太陽光発電プロジェクトの建設を促進し、太陽光発電の、更に薄型ウエハーの需要が拡大しています。

目次

第1章 イントロダクション

- 市場概要

- 市場の定義

- 調査範囲

- 市場セグメンテーション

- 通貨

- 前提条件

- 基準年と予測年のタイムライン

第2章 調査手法

- 調査データ

- 調査プロセス

第3章 エグゼクティブサマリー

- 調査ハイライト

第4章 市場力学

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 業界のバリューチェーン分析

第5章 薄型ウエハー市場:厚さ別

- イントロダクション

- 100μm以下

- 100~199μm

- 200μm以上

第6章 薄型ウエハー市場:用途別

- イントロダクション

- MEMS

- メモリー

- LED

- RFデバイス

- イメージセンサー

- その他

第7章 薄型ウエハー市場:地域別

- イントロダクション

- 南北アメリカ

- 厚さ別

- 用途別

- 国別

- 欧州・中東・アフリカ

- 厚さ別

- 用途別

- 国別

- アジア太平洋

- 厚さ別

- 用途別

- 国別

第8章 競合環境と分析

- 主要企業と戦略分析

- 新興企業と市場収益性

- 合併、買収、合意およびコラボレーション

- ベンダー競争力マトリックス

第9章 企業プロファイル

- SK Siltron Co. Ltd.

- Siltronic

- Sumco Corporation

- Virginia Semiconductor Inc.

- Global Wafer Co. Ltd.

- PV Crystalox Solar plc

- Wafer Works Corporation

- Virginia Semiconductor Inc.

- Shin-Etsu Chemical Co., Ltd.

- DISCO Corporation.

The thin wafer market is estimated to witness a CAGR of 4.03% to grow from US$8.404 billion in 2021 to US$11.085 billion by 2028.

The market for thin wafers is rising due to the increasing demand for smartphones and smart wearable devices coupled with technological innovation in the sector. Rapidly growing urbanization and high disposable income has increased the demand for electronic devices such as smartphones, LEDs, and Smart TV. To meet the growing demand for cutting-edge gadgets, many top consumer electronics companies, including Apple, Samsung, Redmi, and Oneplus, are investing heavily in their development and research efforts. Moreover, increasing demand for other thin devices, such as smart TV with slim bodies, smartwatches, etc., is expected to drive noteworthy demand for thin wafers. Rising investments in R&D activities by various countries are expected to surge the market growth in the coming years.

Rising adoption of photovoltaics and technological development to boost the growth of the market.

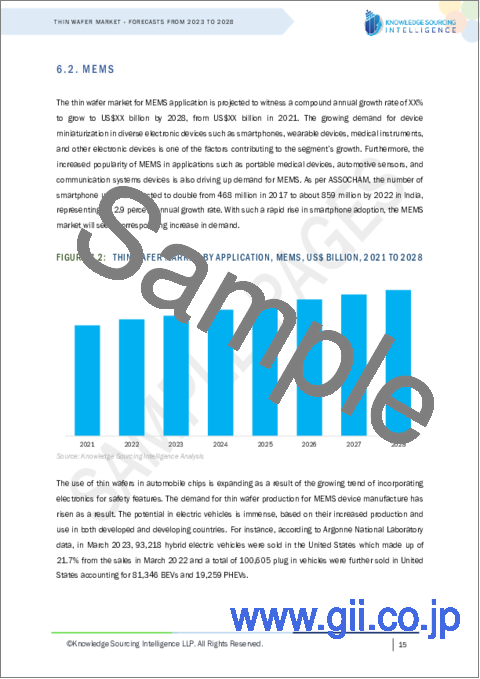

The thin wafer market is expected to surge in the coming years due to the rising adoption of photovoltaics. Increasing human carbon footprints have raised serious environmental concerns, due to which there is a high demand for the development of sustainable means of energy production, which includes the adoption of photovoltaics. The thin wafer is the essential raw material that is used to produce solar cells; hence its demand is increasing in the market. For instance, in November 2022, a new photovoltaic material has been created by researchers at the IIT Mandi that may produce electricity when exposed to light from LED or CFL household light sources. This study supports the widespread deployment of loT technology in modern culture. IoT devices are being used more regularly by cell phones, home automation, and other systems that require various forms of real-time data. These devices must be independent, producing electricity of their own without the assistance of power cables. These devices are currently powered by both the main and secondary batteries. Every battery has a finite life expectancy and is neither cost-effective nor environmentally beneficial.

Shifting focus towards LEDs on account of their increasing use in a wide range of applications in the consumer electronics and lighting industry is increasing the demand for efficient semiconductors, which is expected to increase the demand for thin wafers across the industry. Growing focus on the well-being of the environment and implementation of effective energy efficiency programs across various countries has significantly increased the demand for LED in the market. For example- The government of India has initiated the use of bulk procurement of LED lights which will help the country in conserving energy. This, in turn, is driving the adoption of thin wafers for LEDs, thus boosting the demand for efficient LED solutions and increasing the capacity of photovoltaics in commercial/industrial areas. For instance, as per the 2022 report of the International Energy Association, the net capacity of PVs increased from 27 GW in 2021 to 30 GW in 2022, which has led to an increase in the demand for thin wafers in the market.

Further, the introduction of Industry 4.0 and technologies like loT and Al in the automobile industry will have a big impact on the expansion of the thin wafer market. The growing demand for connected vehicles will lead to new technological developments. Additionally, the relevance of linked cars is expanding as a result of current trends like touch-free human-machine interfaces, which are revolutionizing the automotive industry. The advent of new technologies, including adaptive cruise control, intelligent parking assistance systems, and advanced driver assistance systems, will further spur market expansion.

Additionally, governments in both developed and developing countries are making significant investments in the production of thin wafer semiconductors. The growth of semiconductors has also been aided by key players' cooperation and increased R&D expenditures. For instance, the German government has spent close to 3 billion euros reclaiming the locations of semiconductor manufacturing. The IoT and Industry 4.0's increasing need for semiconductors are the driving forces behind this investment, and the production facilities improve access to enough microchips to keep up with the newest trends.

Market Developments:

- According to Argonne National Laboratory data, in March 2023, 93,218 hybrid electric vehicles were sold in the United States, which made up 21.7% of the sales in March 2022, and a total of 100,605 plug-in vehicles were further sold in the United States, accounting for 81,346 BEVs and 19,259 PHEVs.

- According to the data provided by the National Energy Administration, the overall solar capacity of China reached 392.61 GW in 2022, which signified a major increase of 28.1% in comparison to 306.GW was recorded in 2021. Moreover, as per the same source, the country saw an additional installation of 87.41 GW in the same year.

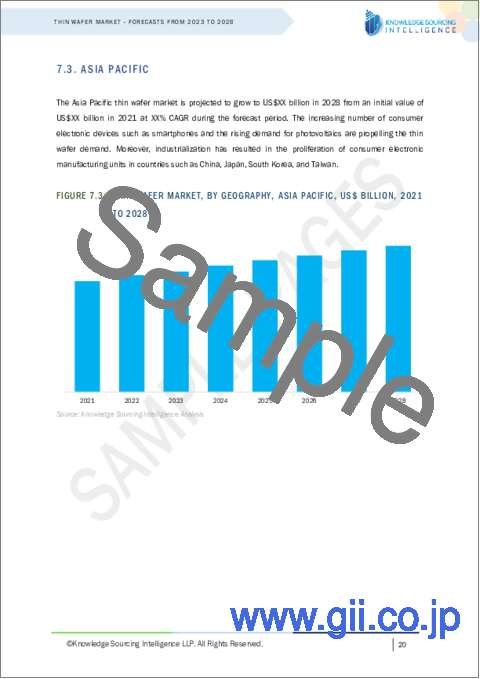

The Asia Pacific region is anticipated to hold the largest share of the market during the forecasted period.

Based on geography, the global thin wafer market is analyzed into Americas, Europe Middle East and Africa, and Asia Pacific. The Asia Pacific region is projected to hold a large share of the market and grow at the fastest rate during the forecasted period. Industrialization in countries such as India, China, South Korea, Vietnam, Thailand, and others, has led to mushrooming of consumer electronic manufacturing units in these countries that will support the market. Furthermore, increased disposable income has surged the penetration of smart devices, particularly smartphones, which also support market prospects. Moreover, favorable climatic conditions have boosted the construction of solar projects, expanding the demand for photovoltaics and hence thin wafers.

Segmentation

By Thickness

- Less than 100 μm

- 100-199 μm

- Greater than 200 μm

By Application

- MEMS

- Memory

- LED

- RF Devices

- Image Sensors

- Others

By Geography

- Americas

- USA

- Others

- Europe

- Germany

- France

- United Kingdom

- Others

- Asia Pacific

- China

- Japan

- South Korea

- Taiwan

- Others

TABLE OF CONTENTS

1. INTRODUCTION

- 1.1. Market Overview

- 1.2. Market Definition

- 1.3. Scope of the Study

- 1.4. Market Segmentation

- 1.5. Currency

- 1.6. Assumptions

- 1.7. Base, and Forecast Years Timeline

2. RESEARCH METHODOLOGY

- 2.1. Research Data

- 2.2. Research Process

3. EXECUTIVE SUMMARY

- 3.1. Research Highlights

4. MARKET DYNAMICS

- 4.1. Market Drivers

- 4.2. Market Restraints

- 4.3. Porter's Five Force Analysis

- 4.3.1. Bargaining Power of Suppliers

- 4.3.2. Bargaining Power of Buyers

- 4.3.3. Threat of New Entrants

- 4.3.4. Threat of Substitutes

- 4.3.5. Competitive Rivalry in the Industry

- 4.4. Industry Value Chain Analysis

5. THIN WAFER MARKET, BY THICKNESS

- 5.1. Introduction

- 5.2. Less than 100 μm

- 5.3. 100-199 μm

- 5.4. Greater than 200 μm

6. THIN WAFER MARKET, BY APPLICATIONS

- 6.1. Introduction

- 6.2. MEMS

- 6.3. Memory

- 6.4. LED

- 6.5. RF Devices

- 6.6. Image Sensors

- 6.7. Others

7. THIN WAFER MARKET, BY GEOGRAPHY

- 7.1. Introduction

- 7.2. Americas

- 7.2.1. By Thickness

- 7.2.2. By Application

- 7.2.3. By Country

- 7.2.3.1. USA

- 7.2.3.2. Others

- 7.3. Europe Middle East and Africa

- 7.3.1. By Thickness

- 7.3.2. By Application

- 7.3.3. By Country

- 7.3.3.1. UK

- 7.3.3.2. Germany

- 7.3.3.3. France

- 7.3.3.4. Others

- 7.4. Asia Pacific

- 7.4.1. By Thickness

- 7.4.2. By Application

- 7.4.3. By Country

- 7.4.3.1. China

- 7.4.3.2. Japan

- 7.4.3.3. Taiwan

- 7.4.3.4. South Korea

- 7.4.3.5. Others

8. COMPETITIVE ENVIRONMENT AND ANALYSIS

- 8.1. Major Players and Strategy Analysis

- 8.2. Emerging Players and Market Lucrativeness

- 8.3. Mergers, Acquisitions, Agreements, and Collaborations

- 8.4. Vendor Competitiveness Matrix

9. COMPANY PROFILES

- 9.1. SK Siltron Co. Ltd.

- 9.2. Siltronic

- 9.3. Sumco Corporation

- 9.4. Virginia Semiconductor Inc.

- 9.5. Global Wafer Co. Ltd.

- 9.6. PV Crystalox Solar plc

- 9.7. Wafer Works Corporation

- 9.8. Virginia Semiconductor Inc.

- 9.9. Shin-Etsu Chemical Co., Ltd.

- 9.10. DISCO Corporation.