|

|

市場調査レポート

商品コード

1091015

低温機器の世界市場 (2022-2030年):市場規模 (製品・寒剤・用途・エンドユーザー別)・地域的展望・成長の潜在性・市場シェア・予測Cryogenic Equipment Market Size By Product, By Cryogen, By Application, By End-user, Regional Outlook, Growth Potential, Competitive Market Share & Forecast, 2022 - 2030 |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| 低温機器の世界市場 (2022-2030年):市場規模 (製品・寒剤・用途・エンドユーザー別)・地域的展望・成長の潜在性・市場シェア・予測 |

|

出版日: 2022年06月03日

発行: Global Market Insights Inc.

ページ情報: 英文 580 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

低温機器の市場は、天然ガスへの需要の急増により、2030年にかけて大きく成長すると予想されています。

また、ヘルスケア、化学、食品加工の各産業の活況や、既存の製造施設の拡張に向けた継続的な投資も今後の市場成長をさらに後押しするものと思われます。さらに、温室効果ガス排出量削減のための厳格な法的要件も市場成長を大幅に後押ししています。

製品別で見ると、気化器の部門が、2030年にかけて大きく成長すると予測されています。また、エンドユーザー別では、新興経済諸国を中心に、ガスを利用したインフラ整備への投資が増加していることから、電力部門で製品需要が高まると予想されています。一方、食品・飲料の部門も、包装食品や冷凍食品への需要の増加、飲料輸送の急増などにより、堅調な伸びを示すと予測されています。

当レポートでは、世界の低温機器の市場を調査し、市場の定義と概要、市場成長への各種影響因子の分析、法規制環境、イノベーション・技術の情勢、市場規模の推移・予測、各種区分・地域/主要国別の内訳、競合環境、主要企業のプロファイルなどをまとめています。

目次

第1章 調査手法・調査範囲

第2章 エグゼクティブサマリー

第3章 低温機器産業の考察

- 産業のエコシステム分析

- イノベーション・技術の情勢

- 規制状況

- 医療用途全体の将来の可能性と機会

- COVID-19の影響

- 寒剤の生産・消費

- 産業への影響要因

- 成長要因

- 潜在的リスク&課題

- 成長の可能性

- ポーターの分析

- 競合情勢

- PESTEL分析

第4章 低温機器市場:製品別

- 市場シェア

- タンク

- バルブ

- 気化器

- ポンプ

- パイプ

- その他

第5章 低温機器市場:寒剤別

- 市場シェア

- 窒素

- 空気

- 天然ガス

- アルゴン

- その他

第6章 低温機器市場:用途別

- 市場シェア

- 保管

- 流通

第7章 低温機器市場:エンドユーザー別

- 市場シェア

- 石油・ガス

- 電力

- 食品・飲料

- 化学

- ゴム・プラスチック

- 冶金

- ヘルスケア

- 運送

- 農林漁業

- その他

第8章 低温機器市場:地域別

- 市場シェア

- 北米

- 欧州

- アジア太平洋

- 中東・アフリカ

- ラテンアメリカ

第9章 企業プロファイル

- Emerson Electric Co.

- INOXCVA

- Cryostar

- Linde PLC

- Air Liquide

- Air Products and Chemicals, Inc.

- Shell-n-Tube

- HEROSE GmbH

- Schlumberger Limited

- Fives Group

- PACKO Industry

- Oxford Instruments

- SHI Cryogenics Group

- Abhijit Enterprises

- VRV S.r.L

- Vacker

- Wessington Cryogenics

- Cryofab

- sinoCleansky

- Flowserve Corporation

- Oswal Industries Limited

- Super Cryogenic Systems Private Limited

- Cryogenic Liquide

- Cryogas Equipment Pvt. Ltd.

- IWI Cryogenic Vaporization Systems(India)Pvt. Ltd.

- AIR WATER INC

- Chart Industries

- FIBA Technologies, Inc.

- Suretank

- Auguste Cryogenics

- Vijay Tanks & Vessels(P)Limited

- Brugg Group AG

- DEMACO

- TMK

- Cryoworld

- Vacuum Barrier Corporation

- Kelvin Technology

- Thames Cryogenics Ltd.

- SPS Cryogenics B.V.

- PraxEidos Srl

- CRYOSPAIN

- Cryo Anlagenbau GmbH

The cryogenic equipment market is expected to grow massively by 2030 owing to surging demand for natural gas. In addition, booming healthcare, chemicals, and food processing industries, along with ongoing investments in the expansion of existing manufacturing facilities, are likely to further impel market growth in the forecast years.

Stringent legislative requirements in efforts to reduce greenhouse gas emissions have considerably aided market growth. Moreover, major players in the industry have been focusing on prominent growth strategies, such as partnerships and acquisitions, to improve their market standing. For instance, in May 2022, Chart Industries, a prominent manufacturer of highly engineered equipment, acquired Cryogenic Service Center, a Swedish turnkey solutions company, for approximately $4 million. The acquisition allowed Chart to broaden its geographical reach and increase its manufacturing capacity and broaden its geographical presence in the Nordic Region.

The cryogenic equipment market has been bifurcated based on end-user, product, application, cryogen, and region.

In terms of product, the cryogenic equipment industry has been divided into pipe, tanks, pumps, valves, and vaporizers. The vaporizers segment is speculated to observe significant progress by 2030 as a result of reinforcing consumer awareness toward the adoption of sustainable solutions equipment.

The market has been categorized based on end-user into agriculture forestry & fishing, O&G industry, shipping, power, healthcare, food & beverage, metallurgy, chemical, and rubber & plastics. Increasing investments toward the development of gas-based infrastructure, primarily across developing economies, are anticipated to boost product demand across the power end-use sector. Meanwhile, the cryogenic equipment market share from the food & beverage segment is estimated to witness robust growth due to rising demand for packaged and frozen food products, along with an upsurge in the transportation of beverages.

Additionally, the rubber & plastics segment is projected to grow substantially by 2030 due to the development and expansion of new industrial establishments, mainly across developing countries. The metallurgy segment is primed to expand drastically over the review period on account of increasing foreign direct investment across emerging nations for technological enhancement.

Moreover, the cryogenic equipment industry share from the shipping segment is contemplated to record notable expansion by 2030 owing to soaring demand for LNG as a fuel, coupled with an upsurge in the transportation of natural gas. Accelerating investments toward the development of sustainable ponds and food grain infrastructure is likely to bolster product uptake in the agriculture forestry & fishing segment.

In the regional frame of reference, the Latin America cryogenic equipment market is slated to grow enormously over the forecast period due to sizable growth in several industries, including chemical manufacturing, metallurgy, E&P, and food & beverage, in the LATAM region.

Table of Contents

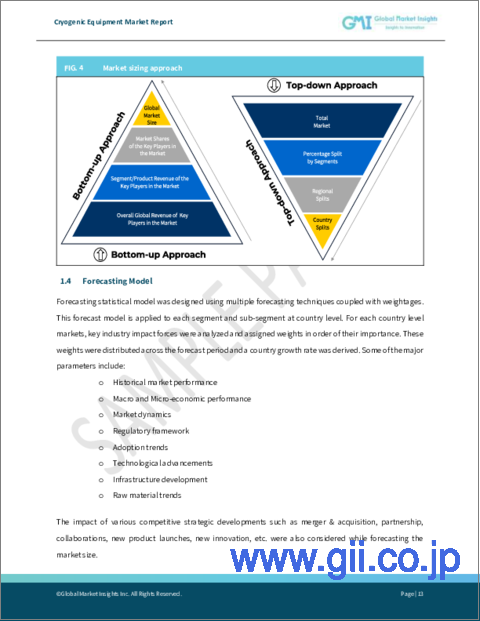

Chapter 1 Methodology

- 1.1 Methodology

- 1.2 Market definitions

- 1.3 Market estimation & forecast parameters

- 1.4 Data Sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid Sources

- 1.4.2.2 Public Sources

Chapter 2 Executive Summary

- 2.1 Cryogenic equipment industry 360 degree synopsis, 2018 - 2030

- 2.1.1 Business trends

- 2.1.2 Product trends

- 2.1.3 Cryogen type trends

- 2.1.4 Application trends

- 2.1.5 End-user trends

- 2.1.6 Regional trends

Chapter 3 Cryogenic Equipment Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Vendor Matrix

- 3.2 Innovation & technology landscape

- 3.2.1 Emerson Electric

- 3.2.2 INOXCVA

- 3.2.3 Cryostar

- 3.2.4 Air Products

- 3.2.5 Shell-n-Tube

- 3.2.6 Fives

- 3.2.7 PACKO Industry

- 3.2.8 Oxford Instruments

- 3.2.9 SHI Cryogenics Group

- 3.3 Regulatory landscape

- 3.3.1 International standards and codes

- 3.3.1.1 ISO 20421-1:2019: Cryogenic vessels - Large transportable vacuum-insulated vessels - Part 1: Design, fabrication, inspection, and testing

- 3.3.1.2 ISO 21009-1:2008: Cryogenic vessels - Static vacuum-insulated vessels - Part 1: Design, fabrication, inspection, and tests

- 3.3.1.3 ISO 21010:2017: Cryogenic vessels - Gas/material compatibility

- 3.3.1.4 ISO 21011:2008: Cryogenic vessels - Valves for cryogenic service

- 3.3.1.5 ISO 12991:2012: Liquefied natural gas (LNG) - Tanks for on-board storage as a fuel for automotive vehicles

- 3.3.1.6 ISO 21012:2018: Cryogenic vessels - Hoses

- 3.3.1.7 ISO 21013-1:2008: Cryogenic vessels - Pressure-relief accessories for cryogenic service - Part 1: Reclosable pressure-relief valves

- 3.3.1.8 ISO 21014:2019: Cryogenic vessels - Cryogenic insulation performance

- 3.3.1.9 ISO 21028-2:2018: Cryogenic vessels - Toughness requirements for materials at cryogenic temperature - Part 2: Temperatures between -80 degrees C and -20 degrees C

- 3.3.1.10 ISO 21029-1:2018: Cryogenic vessels - Transportable vacuum insulated vessels of not more than 1 000 litres volume - Part 1: Design, fabrication, inspection, and tests

- 3.3.1.11 ISO 23208:2017: Cryogenic vessels - Cleanliness for cryogenic service

- 3.3.1.12 ISO 24490:2016: Cryogenic vessels - Pumps for cryogenic service

- 3.3.2 U.S.

- 3.3.2.1 United States Standards and Codes of Practice

- 3.3.2.2 National Fire Protection Association

- 3.3.2.3 ASME B31: Code of pressure piping

- 3.3.2.3.1 B31.1 - Power Piping (2016)

- 3.3.2.3.2 B31.3: Process Piping (2016)

- 3.3.2.3.3 B31.4 - Pipeline Transportation Systems for Liquid Hydrocarbon and Other Liquids (2016)

- 3.3.2.3.4 B31.5 - Refrigeration Piping and Heat Transfer Components (2016)

- 3.3.2.3.5 B31.9 - Building Services Piping (2014)

- 3.3.2.3.6 B31.12 - Hydrogen Piping and Pipelines (2014)

- 3.3.3 Europe

- 3.3.3.1 The Cryogenics Society of Europe

- 3.3.3.2 Safety codes & standards - ISO

- 3.3.3.3 European and International Standards

- 3.3.3.4 National European Standards

- 3.3.3.5 Technical requirements

- 3.3.3.6 Classification

- 3.3.3.7 Essential safety requirements (ESR)

- 3.3.3.8 Conformity Assessment Procedure

- 3.3.3.9 CE Marking for the European market

- 3.3.4 China

- 3.3.4.1 Pressure vessels

- 3.3.4.1.1 Scope

- 3.3.4.1 Pressure vessels

- 3.3.5 Malaysia

- 3.3.6 Australia

- 3.3.6.1 Dangerous Goods (Storage and Handling) Regulations 2000

- 3.3.6.2 Series of standards

- 3.3.7 India

- 3.3.7.1 The Petroleum and Natural Gas Regulatory Board (Technical Standards and Specifications including Safety Standards for Liquefied Natural Gas Facilities) Regulations, 2016.

- 3.3.7.2 IS 5931: Indian Standard code of safety for handling cryogenic liquids

- 3.3.1 International standards and codes

- 3.4 Future potential & opportunity across medical applications

- 3.5 Covid- 19 impact on the industry outlook

- 3.6 Production/consumption of cryogens

- 3.6.1 Natural gas, by region

- 3.6.1.1 Production

- 3.6.1.2 Consumption

- 3.6.2 Helium production

- 3.6.3 Nitrogen

- 3.6.4 Oxygen

- 3.6.5 Hydrogen

- 3.6.6 Argon

- 3.6.7 Neon

- 3.6.1 Natural gas, by region

- 3.7 Industry impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Growing demand for natural gas

- 3.7.1.2 Positive outlook towards healthcare, chemical, and food processing industries

- 3.7.1.3 Growing power sector

- 3.7.1.4 Robust industrial growth

- 3.7.2 Industry Pitfalls & Challenges

- 3.7.2.1 Safety concerns related to cryogenic liquid

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's Analysis

- 3.9.1 Bargaining power of suppliers

- 3.9.2 Bargaining power of buyers

- 3.9.3 Threat of new entrants

- 3.9.4 Threat of substitutes

- 3.10 Competitive landscape, 2021

- 3.10.1 Strategy dashboard

- 3.10.1.1 Cryospain

- 3.10.1.1.1 Projects

- 3.10.1.2 Chart Industries

- 3.10.1.2.1 Agreements

- 3.10.1.2.2 Strategic ventures

- 3.10.1.3 TMK

- 3.10.1.3.1 Agreements

- 3.10.1.3.2 Strategic ventures

- 3.10.1.4 Thames Cryogenic Ltd

- 3.10.1.4.1 Agreement

- 3.10.1.5 Emerson Electric

- 3.10.1.5.1 Product launch

- 3.10.1.5.2 Mergers & acquisition

- 3.10.1.5.3 Agreement

- 3.10.1.6 INOXCVA

- 3.10.1.6.1 Project

- 3.10.1.7 Cryostar

- 3.10.1.7.1 Agreement

- 3.10.1.7.2 Product launch

- 3.10.1.8 Cryoquip

- 3.10.1.8.1 Mergers & Acquisition

- 3.10.1.9 Linde Plc

- 3.10.1.9.1 Contracts and Agreements

- 3.10.1.9.2 Mergers & Acquisitions

- 3.10.1.9.3 Agreement

- 3.10.1.10 Air Liquide

- 3.10.1.10.1 Joint Venture

- 3.10.1.10.2 Innovative programs

- 3.10.1.10.3 Mergers and acquisition

- 3.10.1.10.4 Agreement

- 3.10.1.11 Air Products and Chemicals, Inc.

- 3.10.1.11.1 Contracts and Agreements

- 3.10.1.11.2 Product launch

- 3.10.1.11.3 Joint Venture

- 3.10.1.11.4 Mergers & Acquisition

- 3.10.1.11.5 Agreement

- 3.10.1.12 HEROSE GmbH

- 3.10.1.12.1 Mergers & Acquisition

- 3.10.1.13 Oxford Instruments

- 3.10.1.13.1 Product launch

- 3.10.1.13.2 Innovative programs

- 3.10.1.14 SHI Cryogenics Group

- 3.10.1.14.1 Collaboration

- 3.10.1.14.2 Mergers & Acquisition

- 3.10.1.15 Abhijit Enterprises

- 3.10.1.15.1 Strategic initiative

- 3.10.1.16 Cryo Anlagenban GmbH

- 3.10.1.16.1 Agreement

- 3.10.1.17 FIBA Technologies, Inc.

- 3.10.1.17.1 Facility Expansion

- 3.10.1.18 Auguste Cryogenics

- 3.10.1.18.1 Installation/Supply

- 3.10.1.18.2 Facility Expansion

- 3.10.1.1 Cryospain

- 3.10.1 Strategy dashboard

- 3.11 PESTEL Analysis

Chapter 4 Cryogenic Equipment Market, By Product

- 4.1 Cryogenic equipment market share by product, 2021 & 2030

- 4.2 Tanks

- 4.2.1 Global market from tanks, 2018 - 2030

- 4.2.2 Global market from tanks, by region, 2018 - 2030

- 4.3 Valves

- 4.3.1 Global market from valves, 2018 - 2030

- 4.3.2 Global market from valves, by region, 2018 - 2030

- 4.4 Vaporizers

- 4.4.1 Global market from vaporizers, 2018 - 2030

- 4.4.2 Global market from vaporizers, by region, 2018 - 2030

- 4.5 Pumps

- 4.5.1 Global market from pumps, 2018 - 2030

- 4.5.2 Global market from pumps, by region, 2018 - 2030

- 4.6 Pipe

- 4.6.1 Global market from pipe, 2018 - 2030

- 4.6.2 Global market from pipe, by region, 2018 - 2030

- 4.7 Others

- 4.7.1 Global market from others, 2018 - 2030

- 4.7.2 Global market from others, by region, 2018 - 2030

Chapter 5 Cryogenic Equipment Market, By Cryogen Type

- 5.1 Cryogenic equipment market share by cryogen type, 2021 & 2030

- 5.2 Nitrogen

- 5.2.1 Global market from nitrogen, 2018 - 2030

- 5.2.2 Global market from nitrogen, by region, 2018 - 2030

- 5.3 Oxygen

- 5.3.1 Global market from oxygen, 2018 - 2030

- 5.3.2 Global market from oxygen, by region, 2018 - 2030

- 5.4 Natural gas

- 5.4.1 Global market from natural gas, 2018 - 2030

- 5.4.2 Global market from natural gas, by region, 2018 - 2030

- 5.5 Argon

- 5.5.1 Global market from argon, 2018 - 2030

- 5.5.2 Global market from argon, by region, 2018 - 2030

- 5.6 Other cryogens

- 5.6.1 Global market from other cryogens, 2018 - 2030

- 5.6.2 Global market from other cryogens, by region, 2018 - 2030

Chapter 6 Cryogenic Equipment Market, By Application

- 6.1 Cryogenic equipment market share by application, 2021 & 2030

- 6.2 Storage

- 6.2.1 Global market from storage, 2018 - 2030

- 6.2.2 Global market from storage, by region, 2018 - 2030

- 6.3 Distribution

- 6.3.1 Global market from distribution, 2018 - 2030

- 6.3.2 Global market from distribution, by region, 2018 - 2030

Chapter 7 Cryogenic Equipment Market, By End-User

- 7.1 Cryogenic equipment market share by end-user, 2021 & 2030

- 7.2 O&G industry

- 7.2.1 Global market from O&G industry, 2018 - 2030

- 7.2.2 Global market from O&G industry, by region, 2018 - 2030

- 7.3 Power

- 7.3.1 Global market from power, 2018 - 2030

- 7.3.2 Global market from power, by region, 2018 - 2030

- 7.4 Food & beverage

- 7.4.1 Global market from food & beverage, 2018 - 2030

- 7.4.2 Global market from food & beverage, by region, 2018 - 2030

- 7.5 Chemical

- 7.5.1 Global market from chemical, 2018 - 2030

- 7.5.2 Global market from chemical, by region, 2018 - 2030

- 7.6 Rubber & plastics

- 7.6.1 Global market from rubber & plastics, 2018 - 2030

- 7.6.2 Global market from rubber & plastics, by region, 2018 - 2030

- 7.7 Mettallurgy

- 7.7.1 Global market from mettallurgy, 2018 - 2030

- 7.7.2 Global market from mettallurgy, by region, 2018 - 2030

- 7.8 Healthcare

- 7.8.1 Global market from healthcare, 2018 - 2030

- 7.8.2 Global market from healthcare, by region, 2018 - 2030

- 7.9 Shipping

- 7.9.1 Global market from shipping, 2018 - 2030

- 7.9.2 Global market from shipping, by region, 2018 - 2030

- 7.10 Agriculture, forestry & fishing

- 7.10.1 Global market from agriculture, forestry & fishing, 2018 - 2030

- 7.10.2 Global market from agriculture, forestry & fishing, by region, 2018 - 2030

- 7.11 Other industries

- 7.11.1 Global market from other industries, 2018 - 2030

- 7.11.2 Global market from other industries, by region, 2018 - 2030

Chapter 8 Cryogenic Equipment Market, By Region

- 8.1 Cryogenic equipment market share by region, 2021 & 2030

- 8.2 North America

- 8.2.1 North America market, 2018 - 2030

- 8.2.2 North America market by product, 2018 - 2030

- 8.2.3 North America market by cryogen type, 2018 - 2030

- 8.2.4 North America market by application, 2018 - 2030

- 8.2.5 North America market by end-user, 2018 - 2030

- 8.2.6 U.S.

- 8.2.6.1 U.S. market, 2018 - 2030

- 8.2.6.2 U.S. market by product, 2018 - 2030

- 8.2.6.3 U.S. market by cryogen type, 2018 - 2030

- 8.2.6.4 U.S. market by application, 2018 - 2030

- 8.2.6.5 U.S. market by end-user, 2018 - 2030

- 8.2.7 Canada

- 8.2.7.1 Canada market, 2018 - 2030

- 8.2.7.2 Canada market by product, 2018 - 2030

- 8.2.7.3 Canada market by cryogen type, 2018 - 2030

- 8.2.7.4 Canada market by application, 2018 - 2030

- 8.2.7.5 Canada market by end-user, 2018 - 2030

- 8.2.8 Mexico

- 8.2.8.1 Mexico market, 2018 - 2030

- 8.2.8.2 Mexico market by product, 2018 - 2030

- 8.2.8.3 Mexico market by cryogen type, 2018 - 2030

- 8.2.8.4 Mexico market by application, 2018 - 2030

- 8.2.8.5 Mexico market by end-user, 2018 - 2030

- 8.3 Europe

- 8.3.1 Europe market, 2018 - 2030

- 8.3.2 Europe market by product, 2018 - 2030

- 8.3.3 Europe market by cryogen type, 2018 - 2030

- 8.3.4 Europe market by application, 2018 - 2030

- 8.3.5 Europe market by end-user, 2018 - 2030

- 8.3.6 UK

- 8.3.6.1 UK market, 2018 - 2030

- 8.3.6.2 UK market by product, 2018 - 2030

- 8.3.6.3 UK market by cryogen type, 2018 - 2030

- 8.3.6.4 UK market by application, 2018 - 2030

- 8.3.6.5 UK market by end-user, 2018 - 2030

- 8.3.7 Germany

- 8.3.7.1 Germany market, 2018 - 2030

- 8.3.7.2 Germany market by product, 2018 - 2030

- 8.3.7.3 Germany market by cryogen type, 2018 - 2030

- 8.3.7.4 Germany market by application, 2018 - 2030

- 8.3.7.5 Germany market by end-user, 2018 - 2030

- 8.3.8 Italy

- 8.3.8.1 Italy market, 2018 - 2030

- 8.3.8.2 Italy market by product, 2018 - 2030

- 8.3.8.3 Italy market by cryogen type, 2018 - 2030

- 8.3.8.4 Italy market by application, 2018 - 2030

- 8.3.8.5 Italy market by end-user, 2018 - 2030

- 8.3.9 France

- 8.3.9.1 France market, 2018 - 2030

- 8.3.9.2 France market by product, 2018 - 2030

- 8.3.9.3 France market by cryogen type, 2018 - 2030

- 8.3.9.4 France market by application, 2018 - 2030

- 8.3.9.5 France market by end-user, 2018 - 2030

- 8.3.10 Spain

- 8.3.10.1 Spain market, 2018 - 2030

- 8.3.10.2 Spain market by product, 2018 - 2030

- 8.3.10.3 Spain market by cryogen type, 2018 - 2030

- 8.3.10.4 Spain market by application, 2018 - 2030

- 8.3.10.5 Spain market by end-user, 2018 - 2030

- 8.3.11 Poland

- 8.3.11.1 Poland market, 2018 - 2030

- 8.3.11.2 Poland market by product, 2018 - 2030

- 8.3.11.3 Poland market by cryogen type, 2018 - 2030

- 8.3.11.4 Poland market by application, 2018 - 2030

- 8.3.11.5 Poland market by end-user, 2018 - 2030

- 8.3.12 Russia

- 8.3.12.1 Russia market, 2018 - 2030

- 8.3.12.2 Russia market by product, 2018 - 2030

- 8.3.12.3 Russia market by cryogen type, 2018 - 2030

- 8.3.12.4 Russia market by application, 2018 - 2030

- 8.3.12.5 Russia market by end-user, 2018 - 2030

- 8.3.13 Norway

- 8.3.13.1 Norway market, 2018 - 2030

- 8.3.13.2 Norway market by product, 2018 - 2030

- 8.3.13.3 Norway market by cryogen type, 2018 - 2030

- 8.3.13.4 Norway market by application, 2018 - 2030

- 8.3.13.5 Norway market by end-user, 2018 - 2030

- 8.3.14 Netherlands

- 8.3.14.1 Netherlands market, 2018 - 2030

- 8.3.14.2 Netherlands market by product, 2018 - 2030

- 8.3.14.3 Netherlands market by cryogen type, 2018 - 2030

- 8.3.14.4 Netherlands market by application, 2018 - 2030

- 8.3.14.5 Netherlands market by end-user, 2018 - 2030

- 8.4 Asia Pacific

- 8.4.1 Asia Pacific market, 2018 - 2030

- 8.4.2 Asia Pacific market by product, 2018 - 2030

- 8.4.3 Asia Pacific market by cryogen type, 2018 - 2030

- 8.4.4 Asia Pacific market by application, 2018 - 2030

- 8.4.5 Asia Pacific market by end-user, 2018 - 2030

- 8.4.6 China

- 8.4.6.1 China market, 2018 - 2030

- 8.4.6.2 China market by product, 2018 - 2030

- 8.4.6.3 China market by cryogen type, 2018 - 2030

- 8.4.6.4 China market by application, 2018 - 2030

- 8.4.6.5 China market by end-user, 2018 - 2030

- 8.4.7 India

- 8.4.7.1 India market, 2018 - 2030

- 8.4.7.2 India market by product, 2018 - 2030

- 8.4.7.3 India market by cryogen type, 2018 - 2030

- 8.4.7.4 India market by application, 2018 - 2030

- 8.4.7.5 India market by end-user, 2018 - 2030

- 8.4.8 Japan

- 8.4.8.1 Japan market, 2018 - 2030

- 8.4.8.2 Japan market by product, 2018 - 2030

- 8.4.8.3 Japan market by cryogen type, 2018 - 2030

- 8.4.8.4 Japan market by application, 2018 - 2030

- 8.4.8.5 Japan market by end-user, 2018 - 2030

- 8.4.9 South Korea

- 8.4.9.1 South Korea market, 2018 - 2030

- 8.4.9.2 South Korea market by product, 2018 - 2030

- 8.4.9.3 South Korea market by cryogen type, 2018 - 2030

- 8.4.9.4 South Korea market by application, 2018 - 2030

- 8.4.9.5 South Korea market by end-user, 2018 - 2030

- 8.4.10 Indonesia

- 8.4.10.1 Indonesia market, 2018 - 2030

- 8.4.10.2 Indonesia market by product, 2018 - 2030

- 8.4.10.3 Indonesia market by cryogen type, 2018 - 2030

- 8.4.10.4 Indonesia market by application, 2018 - 2030

- 8.4.10.5 Indonesia market by end-user, 2018 - 2030

- 8.4.11 Thailand

- 8.4.11.1 Thailand market, 2018 - 2030

- 8.4.11.2 Thailand market by product, 2018 - 2030

- 8.4.11.3 Thailand market by cryogen type, 2018 - 2030

- 8.4.11.4 Thailand market by application, 2018 - 2030

- 8.4.11.5 Thailand market by end-user, 2018 - 2030

- 8.4.12 Malaysia

- 8.4.12.1 Malaysia market, 2018 - 2030

- 8.4.12.2 Malaysia market by product, 2018 - 2030

- 8.4.12.3 Malaysia market by cryogen type, 2018 - 2030

- 8.4.12.4 Malaysia market by application, 2018 - 2030

- 8.4.12.5 Malaysia market by end-user, 2018 - 2030

- 8.4.13 Philippines

- 8.4.13.1 Philippines market, 2018 - 2030

- 8.4.13.2 Philippines market by product, 2018 - 2030

- 8.4.13.3 Philippines market by cryogen type, 2018 - 2030

- 8.4.13.4 Philippines market by application, 2018 - 2030

- 8.4.13.5 Philippines market by end-user, 2018 - 2030

- 8.4.14 Australia

- 8.4.14.1 Australia market, 2018 - 2030

- 8.4.14.2 Australia market by product, 2018 - 2030

- 8.4.14.3 Australia market by cryogen type, 2018 - 2030

- 8.4.14.4 Australia market by application, 2018 - 2030

- 8.4.14.5 Australia market by end-user, 2018 - 2030

- 8.5 Middle East & Africa

- 8.5.1 Middle East & Africa market, 2018 - 2030

- 8.5.2 Middle East & Africa market by product, 2018 - 2030

- 8.5.3 Middle East & Africa market by cryogen type, 2018 - 2030

- 8.5.4 Middle East & Africa market by application, 2018 - 2030

- 8.5.5 Middle East & Africa market by end-user, 2018 - 2030

- 8.5.6 Saudi Arabia

- 8.5.6.1 Saudi Arabia market, 2018 - 2030

- 8.5.6.2 Saudi Arabia market by product, 2018 - 2030

- 8.5.6.3 Saudi Arabia market by cryogen type, 2018 - 2030

- 8.5.6.4 Saudi Arabia market by application, 2018 - 2030

- 8.5.6.5 Saudi Arabia market by end-user, 2018 - 2030

- 8.5.7 UAE

- 8.5.7.1 UAE market, 2018 - 2030

- 8.5.7.2 UAE market by product, 2018 - 2030

- 8.5.7.3 UAE market by cryogen type, 2018 - 2030

- 8.5.7.4 UAE market by application, 2018 - 2030

- 8.5.7.5 UAE market by end-user, 2018 - 2030

- 8.5.8 Kuwait

- 8.5.8.1 Kuwait market, 2018 - 2030

- 8.5.8.2 Kuwait market by product, 2018 - 2030

- 8.5.8.3 Kuwait market by cryogen type, 2018 - 2030

- 8.5.8.4 Kuwait market by application, 2018 - 2030

- 8.5.8.5 Kuwait market by end-user, 2018 - 2030

- 8.5.9 Oman

- 8.5.9.1 Oman market, 2018 - 2030

- 8.5.9.2 Oman market by product, 2018 - 2030

- 8.5.9.3 Oman market by cryogen type, 2018 - 2030

- 8.5.9.4 Oman market by application, 2018 - 2030

- 8.5.9.5 Oman market by end-user, 2018 - 2030

- 8.5.10 Turkey

- 8.5.10.1 Turkey market, 2018 - 2030

- 8.5.10.2 Turkey market by product, 2018 - 2030

- 8.5.10.3 Turkey market by cryogen type, 2018 - 2030

- 8.5.10.4 Turkey market by application, 2018 - 2030

- 8.5.10.5 Turkey market by end-user, 2018 - 2030

- 8.5.11 Qatar

- 8.5.11.1 Qatar market, 2018 - 2030

- 8.5.11.2 Qatar market by product, 2018 - 2030

- 8.5.11.3 Qatar market by cryogen type, 2018 - 2030

- 8.5.11.4 Qatar market by application, 2018 - 2030

- 8.5.11.5 Qatar market by end-user, 2018 - 2030

- 8.5.12 Egypt

- 8.5.12.1 Egypt market, 2018 - 2030

- 8.5.12.2 Egypt market by product, 2018 - 2030

- 8.5.12.3 Egypt market by cryogen type, 2018 - 2030

- 8.5.12.4 Egypt market by application, 2018 - 2030

- 8.5.12.5 Egypt market by end-user, 2018 - 2030

- 8.5.13 South Africa

- 8.5.13.1 South Africa market, 2018 - 2030

- 8.5.13.2 South Africa market by product, 2018 - 2030

- 8.5.13.3 South Africa market by cryogen type, 2018 - 2030

- 8.5.13.4 South Africa market by application, 2018 - 2030

- 8.5.13.5 South Africa market by end-user, 2018 - 2030

- 8.6 Latin America

- 8.6.1 Latin America market, 2018 - 2030

- 8.6.2 Latin America market by product, 2018 - 2030

- 8.6.3 Latin America market by cryogen type, 2018 - 2030

- 8.6.4 Latin America market by application, 2018 - 2030

- 8.6.5 Latin America market by end-user, 2018 - 2030

- 8.6.6 Brazil

- 8.6.6.1 Brazil market, 2018 - 2030

- 8.6.6.2 Brazil market by product, 2018 - 2030

- 8.6.6.3 Brazil market by cryogen type, 2018 - 2030

- 8.6.6.4 Brazil market by application, 2018 - 2030

- 8.6.6.5 Brazil market by end-user, 2018 - 2030

- 8.6.7 Argentina

- 8.6.7.1 Argentina market, 2018 - 2030

- 8.6.7.2 Argentina market by product, 2018 - 2030

- 8.6.7.3 Argentina market by cryogen type, 2018 - 2030

- 8.6.7.4 Argentina market by application, 2018 - 2030

- 8.6.7.5 Argentina market by end-user, 2018 - 2030

- 8.6.8 Peru

- 8.6.8.1 Peru market, 2018 - 2030

- 8.6.8.2 Peru market by product, 2018 - 2030

- 8.6.8.3 Peru market by cryogen type, 2018 - 2030

- 8.6.8.4 Peru market by application, 2018 - 2030

- 8.6.8.5 Peru market by end-user, 2018 - 2030

Chapter 9 Company Profiles

- 9.1 Emerson Electric Co.

- 9.1.1 Business overview

- 9.1.2 Financial data

- 9.1.3 Product landscape

- 9.1.4 Strategic outlook

- 9.1.5 SWOT Analysis

- 9.2 INOXCVA

- 9.2.1 Business overview

- 9.2.2 Financial data

- 9.2.3 Product landscape

- 9.2.4 Strategic outlook

- 9.2.5 SWOT Analysis

- 9.3 Cryostar

- 9.3.1 Business overview

- 9.3.2 Financial data

- 9.3.3 Product landscape

- 9.3.4 Strategic outlook

- 9.3.5 SWOT Analysis

- 9.4 Linde PLC

- 9.4.1 Business overview

- 9.4.2 Financial data

- 9.4.3 Product landscape

- 9.4.4 Strategic outlook

- 9.4.5 SWOT Analysis

- 9.5 Air Liquide

- 9.5.1 Business overview

- 9.5.2 Financial data

- 9.5.3 Product landscape

- 9.5.4 Strategic Outlook

- 9.5.5 SWOT Analysis

- 9.6 Air Products and Chemicals, Inc.

- 9.6.1 Business overview

- 9.6.2 Financial data

- 9.6.3 Product landscape

- 9.6.4 Strategic outlook

- 9.6.5 SWOT Analysis

- 9.7 Shell-n-Tube

- 9.7.1 Business overview

- 9.7.2 Financial data

- 9.7.3 Product landscape

- 9.7.4 Strategic Outlook

- 9.7.5 SWOT Analysis

- 9.8 HEROSE GmbH

- 9.8.1 Business overview

- 9.8.2 Financial data

- 9.8.3 Product landscape

- 9.8.4 SWOT Analysis

- 9.9 Schlumberger Limited

- 9.9.1 Business overview

- 9.9.2 Financial data

- 9.9.3 Product landscape

- 9.9.4 SWOT Analysis

- 9.10 Fives Group

- 9.10.1 Business overview

- 9.10.2 Financial data

- 9.10.3 Product landscape

- 9.10.4 Strategic outlook

- 9.10.5 SWOT Analysis

- 9.11 PACKO Industry

- 9.11.1 Business overview

- 9.11.2 Financial data

- 9.11.3 Product landscape

- 9.11.4 SWOT Analysis

- 9.12 Oxford Instruments

- 9.12.1 Business overview

- 9.12.2 Financial data

- 9.12.3 Product landscape

- 9.12.4 Strategic outlook

- 9.12.5 SWOT Analysis

- 9.13 SHI Cryogenics Group

- 9.13.1 Business overview

- 9.13.2 Financial data

- 9.13.3 Product landscape

- 9.13.4 Strategic outlook

- 9.13.5 SWOT Analysis

- 9.14 Abhijit Enterprises

- 9.14.1 Business overview

- 9.14.2 Financial data

- 9.14.3 Product landscape

- 9.14.4 Strategic outlook

- 9.14.5 SWOT Analysis

- 9.15 VRV S.r.L

- 9.15.1 Business overview

- 9.15.2 Financial data

- 9.15.3 Product landscape

- 9.15.4 Strategic outlook

- 9.15.5 SWOT Analysis

- 9.16 Vacker

- 9.16.1 Business overview

- 9.16.2 Financial data

- 9.16.3 Product landscape

- 9.16.4 SWOT Analysis

- 9.17 Wessington Cryogenics

- 9.17.1 Business overview

- 9.17.2 Financial data

- 9.17.3 Product landscape

- 9.17.4 SWOT Analysis

- 9.18 Cryofab

- 9.18.1 Business overview

- 9.18.2 Financial data

- 9.18.3 Product Landscape

- 9.18.4 SWOT Analysis

- 9.19 sinoCleansky

- 9.19.1 Business overview

- 9.19.2 Financial data

- 9.19.3 Product Landscape

- 9.19.4 SWOT Analysis

- 9.20 Flowserve Corporation

- 9.20.1 Business Overview

- 9.20.2 Financial Data

- 9.20.3 Product Landscape

- 9.20.4 SWOT Analysis

- 9.21 Oswal Industries Limited

- 9.21.1 Business Overview

- 9.21.2 Financial Data

- 9.21.3 Product Landscape

- 9.21.4 SWOT Analysis

- 9.22 Super Cryogenic Systems Private Limited

- 9.22.1 Business Overview

- 9.22.2 Financial Data

- 9.22.3 Product Landscape

- 9.22.4 SWOT Analysis

- 9.23 Cryogenic Liquide

- 9.23.1 Business Overview

- 9.23.2 Financial Data

- 9.23.3 Product Landscape

- 9.23.4 SWOT Analysis

- 9.24 Cryogas Equipment Pvt. Ltd.

- 9.24.1 Business Overview

- 9.24.2 Financial Data

- 9.24.3 Product Landscape

- 9.24.4 Strategic Outlook

- 9.24.5 SWOT Analysis

- 9.25 IWI Cryogenic Vaporization Systems (India) Pvt. Ltd.

- 9.25.1 Business Overview

- 9.25.2 Financial Data

- 9.25.3 Product Landscape

- 9.25.4 SWOT Analysis

- 9.26 AIR WATER INC

- 9.26.1 Business Overview

- 9.26.2 Financial Data

- 9.26.3 Product Landscape

- 9.26.4 SWOT Analysis

- 9.27 Chart Industries

- 9.27.1 Business Overview

- 9.27.2 Financial Data

- 9.27.3 Product Landscape

- 9.27.4 SWOT Analysis

- 9.28 FIBA Technologies, Inc.

- 9.28.1 Business Overview

- 9.28.2 Financial Data

- 9.28.3 Product Landscape

- 9.28.4 SWOT Analysis

- 9.29 Suretank

- 9.29.1 Business Overview

- 9.29.2 Financial Data

- 9.29.3 Product Landscape

- 9.29.4 SWOT Analysis

- 9.30 Auguste Cryogenics

- 9.30.1 Business Overview

- 9.30.2 Financial Data

- 9.30.3 Product Landscape

- 9.30.4 SWOT Analysis

- 9.31 Vijay Tanks & Vessels (P) Limited

- 9.31.1 Business Overview

- 9.31.2 Financial Data

- 9.31.3 Product Landscape

- 9.31.4 SWOT Analysis

- 9.32 Brugg Group AG

- 9.32.1 Business Overview

- 9.32.2 Financial Data

- 9.32.3 Product Landscape

- 9.32.4 Strategic Outlook

- 9.32.5 SWOT Analysis

- 9.33 DEMACO

- 9.33.1 Business Overview

- 9.33.2 Financial Data

- 9.33.3 Product Landscape

- 9.33.4 SWOT Analysis

- 9.34 TMK

- 9.34.1 Business Overview

- 9.34.2 Financial Data

- 9.34.3 Product Landscape

- 9.34.4 Strategic Outlook

- 9.34.5 SWOT Analysis

- 9.35 Cryoworld

- 9.35.1 Business Overview

- 9.35.2 Financial Data

- 9.35.3 Product Landscape

- 9.35.4 SWOT Analysis

- 9.36 Vacuum Barrier Corporation

- 9.36.1 Business Overview

- 9.36.2 Financial Data

- 9.36.3 Product Landscape

- 9.36.4 SWOT Analysis

- 9.37 Kelvin Technology

- 9.37.1 Business Overview

- 9.37.2 Financial Data

- 9.37.3 Product Landscape

- 9.37.4 SWOT Analysis

- 9.38 Thames Cryogenics Ltd.

- 9.38.1 Business Overview

- 9.38.2 Financial Data

- 9.38.3 Product Landscape

- 9.38.4 SWOT Analysis

- 9.39 SPS Cryogenics B.V.

- 9.39.1 Business Overview

- 9.39.2 Financial Data

- 9.39.3 Product Landscape

- 9.39.4 SWOT Analysis

- 9.40 PraxEidos Srl

- 9.40.1 Business Overview

- 9.40.2 Financial Data

- 9.40.3 Product Landscape

- 9.40.4 SWOT Analysis

- 9.41 CRYOSPAIN

- 9.41.1 Business Overview

- 9.41.2 Financial Data

- 9.41.3 Product Landscape

- 9.41.4 Strategic Outlook

- 9.41.5 SWOT Analysis

- 9.42 Cryo Anlagenbau GmbH

- 9.42.1 Business Overview

- 9.42.2 Financial Data

- 9.42.3 Product Landscape

- 9.42.4 SWOT Analysis