|

|

市場調査レポート

商品コード

1088270

睡眠時無呼吸症候群用インプラントの世界市場 (2022-2030年):市場規模 (製品・適応症・エンドユーズ別)・地域的展望・用途の潜在性・市場シェア・予測Sleep Apnea Implants Market Size By Product, By Indication, By End-use, Industry Analysis Report, Regional Outlook, Application Potential, Competitive Market Share & Forecast, 2022 - 2030 |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| 睡眠時無呼吸症候群用インプラントの世界市場 (2022-2030年):市場規模 (製品・適応症・エンドユーズ別)・地域的展望・用途の潜在性・市場シェア・予測 |

|

出版日: 2022年06月02日

発行: Global Market Insights Inc.

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 図表

- 目次

睡眠時無呼吸症候群用インプラントの市場は、睡眠時無呼吸症候群の患者数の急増により、2030年にかけて堅調な成長を示すと予測されています。

また、睡眠時無呼吸症候群に関する認知度の向上や、睡眠時無呼吸症候群を患う高齢者人口の増加も予測期間中の市場成長を促進すると考えられています。

製品別で見ると、中枢性睡眠時無呼吸症候群管理のために横隔神経刺激装置の採用が増加していることから、横隔神経刺激装置の部門が2021年に2,400万米ドルを超える規模を記録しています。また、適応症別では、閉塞性睡眠時無呼吸症候群への認知度の急上昇、疾患罹患者数の増加、複数の治療選択肢のアベイラビリティなどから、閉塞性睡眠時無呼吸症候群 (OSA) の部門が2021年に92%を超える収益シェアを示しています。

当レポートでは、世界の睡眠時無呼吸症候群用インプラントの市場を調査し、市場の定義と概要、市場成長への各種影響因子の分析、法規制・償還環境、パイプラインの分析、市場規模の推移・予測、各種区分・地域/主要国別の内訳、競合環境、主要企業のプロファイルなどをまとめています。

目次

第1章 調査手法

第2章 エグゼクティブサマリー

第3章 睡眠時無呼吸症候群用インプラント産業の考察

- 産業の分類

- 産業情勢

- 産業の影響因子

- 成長要因

- 潜在的リスク&課題

- 成長の可能性の分析

- COVID-19:影響分析

- 規制状況

- 償還情勢

- パイプライン分析

- 患者ジャーニーマップ

- ポーターの分析

- 競合情勢

- PESTEL分析

第4章 睡眠時無呼吸症候群用インプラント市場:製品別

- 主要動向

- 埋め込み型舌下神経刺激装置

- 口蓋インプラント

- 骨ねじシステム

- 横隔神経刺激装置

第5章 睡眠時無呼吸症候群用インプラント市場:適応症別

- 主要動向

- 中枢性睡眠時無呼吸症

- 閉塞性睡眠時無呼吸症

第6章 睡眠時無呼吸症候群用インプラント市場:エンドユーズ別

- 主要動向

- 病院

- 外来手術センター

- その他

第7章 睡眠時無呼吸症候群用インプラント市場:地域別

- 主要動向

- 北米

- 欧州

- その他の地域

第8章 企業プロファイル

- 競合ダッシュボード

- Inspire Medical Systems, Inc.

- Medtronic plc

- Nyxoah SA

- Siesta Medical

- Respicardia, Inc.(Asahi Kasei Company)

- LivaNova

Data Tables

- TABLE 1. Sleep apnea implants industry 360 degree synopsis, 2017 - 2030

- TABLE 2. Global sleep apnea implants market, 2017 - 2021 (USD Million)

- TABLE 3. Global sleep apnea implants market, 2022 - 2030 (USD Million)

- TABLE 4. Global sleep apnea implants market, 2017 - 2021 (Units)

- TABLE 5. Global sleep apnea implants market, 2022 - 2030 (Units)

- TABLE 6. Global sleep apnea implants market, by product, 2017 - 2021 (USD Million)

- TABLE 7. Global sleep apnea implants market, by product, 2022 - 2030 (USD Million)

- TABLE 8. Global sleep apnea implants market, by product, 2017 - 2021 (Units)

- TABLE 9. Global sleep apnea implants market, by product, 2022 - 2030 (Units)

- TABLE 10. Global sleep apnea implants market, by indication, 2017 - 2021 (USD Million)

- TABLE 11. Global sleep apnea implants market, by indication, 2022 - 2030 (USD Million)

- TABLE 12. Global sleep apnea implants market, by end-use, 2017 - 2021 (USD Million)

- TABLE 13. Global sleep apnea implants market, by end-use, 2022 - 2030 (USD Million)

- TABLE 14. Global sleep apnea implants market, by region, 2017 - 2021 (USD Million)

- TABLE 15. Global sleep apnea implants market, by region, 2022 - 2030 (USD Million)

- TABLE 16. Global sleep apnea implants market, by region, 2017 - 2021 (Units)

- TABLE 17. Global sleep apnea implants market, by region, 2022 - 2030 (Units)

- TABLE 18. Industry impact forces

- TABLE 19. Hypoglossal neurostimulation devices market size, by region, 2017 - 2021 (USD Million)

- TABLE 20. Hypoglossal neurostimulation devices market size, by region, 2022 - 2030 (USD Million)

- TABLE 21. Hypoglossal neurostimulation devices market size, by region, 2017 - 2021 (Units)

- TABLE 22. Hypoglossal neurostimulation devices market size, by region, 2022 - 2030 (Units)

- TABLE 23. Palatal implants market size, by region, 2017 - 2021 (USD Million)

- TABLE 24. Palatal implants market size, by region, 2022 - 2030 (USD Million)

- TABLE 25. Palatal implants market size, by region, 2017 - 2021 (Units)

- TABLE 26. Palatal implants market size, by region, 2022 - 2030 (Units)

- TABLE 27. Bone screw system market size, by region, 2017 - 2021 (USD Million)

- TABLE 28. Bone screw system market size, by region, 2022 - 2030 (USD Million)

- TABLE 29. Bone screw system market size, by region, 2017 - 2021 (Units)

- TABLE 30. Bone screw system market size, by region, 2022 - 2030 (Units)

- TABLE 31. Phrenic nerve stimulator market size, by region, 2017 - 2021 (USD Million)

- TABLE 32. Phrenic nerve stimulator market size, by region, 2022 - 2030 (USD Million)

- TABLE 33. Phrenic nerve stimulator market size, by region, 2017 - 2021 (Units)

- TABLE 34. Phrenic nerve stimulator market size, by region, 2022 - 2030 (Units)

- TABLE 35. Central sleep apnea market size, by region, 2017 - 2021 (USD Million)

- TABLE 36. Central sleep apnea market size, by region, 2022 - 2030 (USD Million)

- TABLE 37. Obstructive sleep apnea market size, by region, 2017 - 2021 (USD Million)

- TABLE 38. Obstructive sleep apnea market size, by region, 2022 - 2030 (USD Million)

- TABLE 39. Hospitals market size, by region, 2017 - 2021 (USD Million)

- TABLE 40. Hospitals market size, by region, 2022 - 2030 (USD Million)

- TABLE 41. Ambulatory surgical centers market size, by region, 2017 - 2021 (USD Million)

- TABLE 42. Ambulatory surgical centers market size, by region, 2022 - 2030 (USD Million)

- TABLE 43. Others market size, by region, 2017 - 2021 (USD Million)

- TABLE 44. Others market size, by region, 2022 - 2030 (USD Million)

- TABLE 45. North America sleep apnea implants market size, by country, 2017 - 2021 (USD Million)

- TABLE 46. North America sleep apnea implants market size, by country, 2022 - 2030 (USD Million)

- TABLE 47. North America sleep apnea implants market size, by country, 2017 - 2021 (Units)

- TABLE 48. North America sleep apnea implants market size, by country, 2022 - 2030 (Units)

- TABLE 49. North America sleep apnea implants market size, by product, 2017 - 2021 (USD Million)

- TABLE 50. North America sleep apnea implants market size, by product, 2022 - 2030 (USD Million)

- TABLE 51. North America sleep apnea implants market size, by product, 2017 - 2021 (Units)

- TABLE 52. North America sleep apnea implants market size, by product, 2022 - 2030 (Units)

- TABLE 53. North America sleep apnea implants market size, by indication, 2017 - 2021 (USD Million)

- TABLE 54. North America sleep apnea implants market size, by indication, 2022 - 2030 (USD Million)

- TABLE 55. North America sleep apnea implants market size, by end-use, 2017 - 2021 (USD Million)

- TABLE 56. North America sleep apnea implants market size, by end-use, 2022 - 2030 (USD Million)

- TABLE 57. U.S. sleep apnea implants market size, by product, 2017 - 2021 (USD Million)

- TABLE 58. U.S. sleep apnea implants market size, by product, 2022 - 2030 (USD Million)

- TABLE 59. U.S. sleep apnea implants market size, by product, 2017 - 2021 (Units)

- TABLE 60. U.S. sleep apnea implants market size, by product, 2022 - 2030 (Units)

- TABLE 61. U.S. sleep apnea implants market size, by indication, 2017 - 2021 (USD Million)

- TABLE 62. U.S. sleep apnea implants market size, by indication, 2022 - 2030 (USD Million)

- TABLE 63. U.S. sleep apnea implants market size, by end-use, 2017 - 2021 (USD Million)

- TABLE 64. U.S. sleep apnea implants market size, by end-use, 2022 - 2030 (USD Million)

- TABLE 65. Canada sleep apnea implants market size, by product, 2017 - 2021 (USD Million)

- TABLE 66. Canada sleep apnea implants market size, by product, 2022 - 2030 (USD Million)

- TABLE 67. Canada sleep apnea implants market size, by product, 2017 - 2021 (Units)

- TABLE 68. Canada sleep apnea implants market size, by product, 2022 - 2030 (Units)

- TABLE 69. Canada sleep apnea implants market size, by indication, 2017 - 2021 (USD Million)

- TABLE 70. Canada sleep apnea implants market size, by indication, 2022 - 2030 (USD Million)

- TABLE 71. Canada sleep apnea implants market size, by end-use, 2017 - 2021 (USD Million)

- TABLE 72. Canada sleep apnea implants market size, by end-use, 2022 - 2030 (USD Million)

- TABLE 73. Europe sleep apnea implants market size, by country, 2017 - 2021 (USD Million)

- TABLE 74. Europe sleep apnea implants market size, by country, 2022 - 2030 (USD Million)

- TABLE 75. Europe sleep apnea implants market size, by country, 2017 - 2021 (Units)

- TABLE 76. Europe sleep apnea implants market size, by country, 2022 - 2030 (Units)

- TABLE 77. Europe sleep apnea implants market size, by product, 2017 - 2021 (USD Million)

- TABLE 78. Europe sleep apnea implants market size, by product, 2022 - 2030 (USD Million)

- TABLE 79. Europe sleep apnea implants market size, by product, 2017 - 2021 (Units)

- TABLE 80. Europe sleep apnea implants market size, by product, 2022 - 2030 (Units)

- TABLE 81. Europe sleep apnea implants market size, by indication, 2017 - 2021 (USD Million)

- TABLE 82. Europe sleep apnea implants market size, by indication, 2022 - 2030 (USD Million)

- TABLE 83. Europe sleep apnea implants market size, by end-use, 2017 - 2021 (USD Million)

- TABLE 84. Europe sleep apnea implants market size, by end-use, 2022 - 2030 (USD Million)

- TABLE 85. Germany sleep apnea implants market size, by product, 2017 - 2021 (USD Million)

- TABLE 86. Germany sleep apnea implants market size, by product, 2022 - 2030 (USD Million)

- TABLE 87. Germany sleep apnea implants market size, by product, 2017 - 2021 (Units)

- TABLE 88. Germany sleep apnea implants market size, by product, 2022 - 2030 (Units)

- TABLE 89. Germany sleep apnea implants market size, by indication, 2017 - 2021 (USD Million)

- TABLE 90. Germany sleep apnea implants market size, by indication, 2022 - 2030 (USD Million)

- TABLE 91. Germany sleep apnea implants market size, by end-use, 2017 - 2021 (USD Million)

- TABLE 92. Germany sleep apnea implants market size, by end-use, 2022 - 2030 (USD Million)

- TABLE 93. UK sleep apnea implants market size, by product, 2017 - 2021 (USD Million)

- TABLE 94. UK sleep apnea implants market size, by product, 2022 - 2030 (USD Million)

- TABLE 95. UK sleep apnea implants market size, by product, 2017 - 2021 (Units)

- TABLE 96. UK sleep apnea implants market size, by product, 2022 - 2030 (Units)

- TABLE 97. UK sleep apnea implants market size, by indication, 2017 - 2021 (USD Million)

- TABLE 98. UK sleep apnea implants market size, by indication, 2022 - 2030 (USD Million)

- TABLE 99. UK sleep apnea implants market size, by end-use, 2017 - 2021 (USD Million)

- TABLE 100. UK sleep apnea implants market size, by end-use, 2022 - 2030 (USD Million)

- TABLE 101. France sleep apnea implants market size, by product, 2017 - 2021 (USD Million)

- TABLE 102. France sleep apnea implants market size, by product, 2022 - 2030 (USD Million)

- TABLE 103. France sleep apnea implants market size, by product, 2017 - 2021 (Units)

- TABLE 104. France sleep apnea implants market size, by product, 2022 - 2030 (Units)

- TABLE 105. France sleep apnea implants market size, by indication, 2017 - 2021 (USD Million)

- TABLE 106. France sleep apnea implants market size, by indication, 2022 - 2030 (USD Million)

- TABLE 107. France sleep apnea implants market size, by end-use, 2017 - 2021 (USD Million)

- TABLE 108. France sleep apnea implants market size, by end-use, 2022 - 2030 (USD Million)

- TABLE 109. Spain sleep apnea implants market size, by product, 2017 - 2021 (USD Million)

- TABLE 110. Spain sleep apnea implants market size, by product, 2022 - 2030 (USD Million)

- TABLE 111. Spain sleep apnea implants market size, by product, 2017 - 2021 (Units)

- TABLE 112. Spain sleep apnea implants market size, by product, 2022 - 2030 (Units)

- TABLE 113. Spain sleep apnea implants market size, by indication, 2017 - 2021 (USD Million)

- TABLE 114. Spain sleep apnea implants market size, by indication, 2022 - 2030 (USD Million)

- TABLE 115. Spain sleep apnea implants market size, by end-use, 2017 - 2021 (USD Million)

- TABLE 116. Spain sleep apnea implants market size, by end-use, 2022 - 2030 (USD Million)

- TABLE 117. Italy sleep apnea implants market size, by product, 2017 - 2021 (USD Million)

- TABLE 118. Italy sleep apnea implants market size, by product, 2022 - 2030 (USD Million)

- TABLE 119. Italy sleep apnea implants market size, by product, 2017 - 2021 (Units)

- TABLE 120. Italy sleep apnea implants market size, by product, 2022 - 2030 (Units)

- TABLE 121. Italy sleep apnea implants market size, by indication, 2017 - 2021 (USD Million)

- TABLE 122. Italy sleep apnea implants market size, by indication, 2022 - 2030 (USD Million)

- TABLE 123. Italy sleep apnea implants market size, by end-use, 2017 - 2021 (USD Million)

- TABLE 124. Italy sleep apnea implants market size, by end-use, 2022 - 2030 (USD Million)

- TABLE 125. The Netherlands sleep apnea implants market size, by product, 2017 - 2021 (USD Million)

- TABLE 126. The Netherlands sleep apnea implants market size, by product, 2022 - 2030 (USD Million)

- TABLE 127. The Netherlands sleep apnea implants market size, by product, 2017 - 2021 (Units)

- TABLE 128. The Netherlands sleep apnea implants market size, by product, 2022 - 2030 (Units)

- TABLE 129. The Netherlands sleep apnea implants market size, by indication, 2017 - 2021 (USD Million)

- TABLE 130. The Netherlands sleep apnea implants market size, by indication, 2022 - 2030 (USD Million)

- TABLE 131. The Netherlands sleep apnea implants market size, by end-use, 2017 - 2021 (USD Million)

- TABLE 132. The Netherlands sleep apnea implants market size, by end-use, 2022 - 2030 (USD Million)

- TABLE 133. Switzerland sleep apnea implants market size, by product, 2017 - 2021 (USD Million)

- TABLE 134. Switzerland sleep apnea implants market size, by product, 2022 - 2030 (USD Million)

- TABLE 135. Switzerland sleep apnea implants market size, by product, 2017 - 2021 (Units)

- TABLE 136. Switzerland sleep apnea implants market size, by product, 2022 - 2030 (Units)

- TABLE 137. Switzerland sleep apnea implants market size, by indication, 2017 - 2021 (USD Million)

- TABLE 138. Switzerland sleep apnea implants market size, by indication, 2022 - 2030 (USD Million)

- TABLE 139. Switzerland sleep apnea implants market size, by end-use, 2017 - 2021 (USD Million)

- TABLE 140. Switzerland sleep apnea implants market size, by end-use, 2022 - 2030 (USD Million)

- TABLE 141. RoW sleep apnea implants market size, by product, 2017 - 2021 (USD Million)

- TABLE 142. RoW sleep apnea implants market size, by product, 2022 - 2030 (USD Million)

- TABLE 143. RoW sleep apnea implants market size, by product, 2017 - 2021 (Units)

- TABLE 144. RoW sleep apnea implants market size, by product, 2022 - 2030 (Units)

- TABLE 145. RoW sleep apnea implants market size, by indication, 2017 - 2021 (USD Million)

- TABLE 146. RoW sleep apnea implants market size, by indication, 2022 - 2030 (USD Million)

- TABLE 147. RoW sleep apnea implants market size, by end-use, 2017 - 2021 (USD Million)

- TABLE 148. RoW sleep apnea implants market size, by end-use, 2022 - 2030 (USD Million)

Charts & Figures

- FIG. 1 Bottom-up approach (demand side analysis)

- FIG. 2 Top-down approach (supply side analysis)

- FIG. 3 Data validation

- FIG. 4 Industry segmentation

- FIG. 5 Global sleep apnea implants market size, 2017 - 2030 (USD Million)

- FIG. 6 Growth potential analysis, by product

- FIG. 7 Growth potential analysis, by indication

- FIG. 8 Growth potential analysis, by end-use

- FIG. 9 Porter's analysis

- FIG. 10 Competitive matrix analysis, 2021

- FIG. 11 PESTEL analysis

- FIG. 12 Key segment trends, by product

- FIG. 13 Key segment trends, by indication

- FIG. 14 Key segment trends, by end-use

- FIG. 15 Key regional trends

- FIG. 16 Competitive dashboard, 2021

The sleep apnea implants market is set to grow steadily by 2030 owing to surging number of sleep apnea patients. In addition, rising awareness about sleep apnea disorders and expanding geriatric population with sleep apnea are likely to facilitate market growth through the forecast period.

During the COVID-19 pandemic, the industry witnessed a setback in business operations due to restrictions on movement and a strong focus on developing effective treatments for the coronavirus infection. However, the post-pandemic scenario has fueled market progress as a result of growing awareness pertaining to sleep apnea.

Various government initiatives, along with significant investments by public and private companies in the field, have also boosted consumer interest in the product. For instance, in February 2021, the U.S. FDA approved a tongue muscle stimulation device eXciteOSA that claims to calm mild sleep apnea in the user's waking hours. The device is the first to improve tongue muscle function during daytime, which can eventually treat tongue movement and prevent obstructive sleep apnea at night.

Notably, major players in the industry are investing in innovations in sleep apnea implant technology, coupled with growth strategies like acquisitions and partnerships, thereby fostering business growth. For instance, in April 2022, Natus Medical Incorporated, a provider of medical treatment solutions, announced that it has inked an agreement to be acquired by Archimed Group, a leading healthcare investment firm, for around $1.2 billion. Under the terms of the agreement, Natus shareholders were set to receive $33.50 in cash for each share.

The sleep apnea implants market has been bifurcated based on end-use, product, indication, and region.

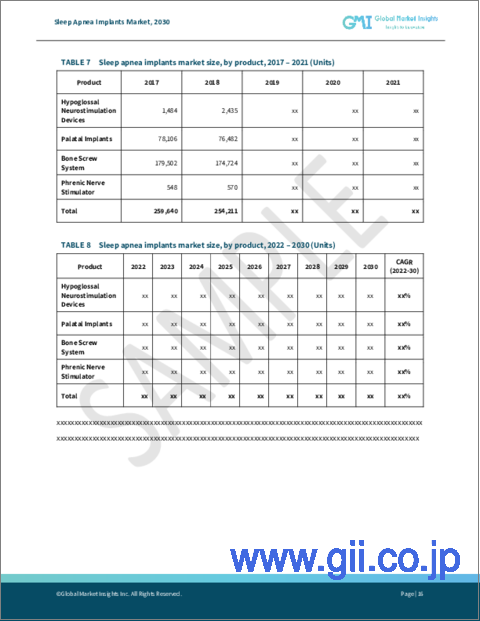

In terms of product, the industry has been divided into palatal implants, bone screw system, phrenic nerve stimulator, and hypoglossal neurostimulation devices. The phrenic nerve stimulator sub-segment registered a valuation of above $24 million in 2021 as a result of increasing adoption of phrenic nerve stimulators for central sleep apnea management.

With regards to indication, the sleep apnea implants market has been split into central sleep apnea and obstructive sleep apnea. The obstructive sleep apnea or OSA sub-segment accounted for over 92% of the market revenue in 2021 attributed to surging awareness regarding obstructive sleep apnea, rising number of disease-affected people, and availability of several treatment alternatives for the condition.

The industry has been segmented based on end-use into ambulatory surgical centers, hospitals, and others. The ambulatory surgical centers sub-segment was valued at around $128 million in 2021 due to the feasible reimbursement coverage and availability of latest surgical technologies that promote patient satisfaction and convenience.

In the regional frame of reference, apart from Europe and North America, the RoW sleep apnea implants market is expected to grow at a CAGR of approximately 19.2% through the study time span. Rising prevalence of sleep apnea, increased adoption of sleep apnea implants, and soaring awareness about the disease are slated to fuel regional market growth in the future.

Table of Contents

Chapter 1 Methodology

- 1.1 Market definition

- 1.2 Base estimates & working

- 1.3 Forecast parameters

- 1.4 Data validation

- 1.5 Data sources

- 1.5.1 Secondary

- 1.5.1.1 Paid sources

- 1.5.1.2 Unpaid sources

- 1.5.2 Primary

- 1.5.1 Secondary

Chapter 2 Executive Summary

- 2.1 Sleep apnea implants industry 360 degree synopsis, 2017 - 2030

- 2.1.1 Business trends

- 2.1.2 Product trends

- 2.1.3 Indication trends

- 2.1.4 End-use trends

- 2.1.5 Regional trends

Chapter 3 Sleep Apnea Implant Industry Insights

- 3.1 Industry segmentation

- 3.2 Industry landscape, 2017 - 2030 (USD Million)

- 3.3 Industry impact factors

- 3.3.1 Growth drivers

- 3.3.1.1 Increasing prevalence of obstructive sleep apnea

- 3.3.1.2 Low compliance & adherence towards CPAP

- 3.3.1.3 Technological advancements

- 3.3.1.4 Increasing awareness regarding sleep apnea

- 3.3.2 Industry pitfalls & challenges

- 3.3.2.1 High costs of sleep apnea implants

- 3.3.2.2 Complications associated with sleep apnea implants

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.4.1 By product

- 3.4.2 By indication

- 3.4.3 By end-use

- 3.5 COVID-19 impact analysis

- 3.6 Regulatory landscape

- 3.6.1 U.S.

- 3.6.2 Europe

- 3.7 Reimbursement landscape

- 3.8 Pipeline analysis

- 3.9 Patient journey map

- 3.10 Porter's analysis

- 3.11 Competitive landscape, 2021

- 3.11.1 Company matrix analysis, 2021

- 3.12 PESTEL analysis

Chapter 4 Sleep Apnea Implants Market, By Product

- 4.1 Key segment trends

- 4.2 Hypoglossal Neurostimulation Devices

- 4.2.1 Market size, by region, 2017 - 2030 (USD Million)

- 4.2.2 Market size, by region, 2017 - 2030 (Units)

- 4.3 Palatal Implants

- 4.3.1 Market size, by region, 2017 - 2030 (USD Million)

- 4.3.2 Market size, by region, 2017 - 2030 (Units)

- 4.4 Bone screw system

- 4.4.1 Market size, by region, 2017 - 2030 (USD Million)

- 4.4.2 Market size, by region, 2017 - 2030 (Units)

- 4.5 Phrenic Nerve Stimulator

- 4.5.1 Market size, by region, 2017 - 2030 (USD Million)

- 4.5.2 Market size, by region, 2017 - 2030 (Units)

Chapter 5 Sleep Apnea Implants Market, By Indication

- 5.1 Key segment trends

- 5.2 Central sleep apnea

- 5.2.1 Market size, by region, 2017 - 2030 (USD Million)

- 5.3 Obstructive sleep apnea

- 5.3.1 Market size, by region, 2017 - 2030 (USD Million)

Chapter 6 Sleep Apnea Implants Market, By End-use

- 6.1 Key segment trends

- 6.2 Hospitals

- 6.2.1 Market size, by region, 2017 - 2030 (USD Million)

- 6.3 Ambulatory surgical centers

- 6.3.1 Market size, by region, 2017 - 2030 (USD Million)

- 6.4 Others

- 6.4.1 Market size, by region, 2017 - 2030 (USD Million)

Chapter 7 Sleep Apnea Implants Market, By Region

- 7.1 Key regional trends

- 7.2 North America

- 7.2.1 Market size, by country, 2017 - 2030 (USD Million)

- 7.2.2 Market size, by country, 2017 - 2030 (Units)

- 7.2.3 Market size, by product, 2017 - 2030 (USD Million)

- 7.2.4 Market size, by product, 2017 - 2030 (Units)

- 7.2.5 Market size, by indication, 2017 - 2030 (USD Million)

- 7.2.6 Market size, by end-use, 2017 - 2030 (USD Million)

- 7.2.7 U.S.

- 7.2.7.1 Market size, by product, 2017 - 2030 (USD Million)

- 7.2.7.2 Market size, by product, 2017 - 2030 (Units)

- 7.2.7.3 Market size, by indication, 2017 - 2030 (USD Million)

- 7.2.7.4 Market size, by end-use, 2017 - 2030 (USD Million)

- 7.2.8 Canada

- 7.2.8.1 Market size, by product, 2017 - 2030 (USD Million)

- 7.2.8.2 Market size, by product, 2017 - 2030 (Units)

- 7.2.8.3 Market size, by indication, 2017 - 2030 (USD Million)

- 7.2.8.4 Market size, by end-use, 2017 - 2030 (USD Million)

- 7.3 Europe

- 7.3.1 Market size, by country, 2017 - 2030 (USD Million)

- 7.3.2 Market size, by country, 2017 - 2030 (Units)

- 7.3.3 Market size, by product, 2017 - 2030 (USD Million)

- 7.3.4 Market size, by product, 2017 - 2030 (Units)

- 7.3.5 Market size, by indication, 2017 - 2030 (USD Million)

- 7.3.6 Market size, by end-use, 2017 - 2030 (USD Million)

- 7.3.7 Germany

- 7.3.7.1 Market size, by product, 2017 - 2030 (USD Million)

- 7.3.7.2 Market size, by product, 2017 - 2030 (Units)

- 7.3.7.3 Market size, by indication, 2017 - 2030 (USD Million)

- 7.3.7.4 Market size, by end-use, 2017 - 2030 (USD Million)

- 7.3.8 UK

- 7.3.8.1 Market size, by product, 2017 - 2030 (USD Million)

- 7.3.8.2 Market size, by product, 2017 - 2030 (Units)

- 7.3.8.3 Market size, by indication, 2017 - 2030 (USD Million)

- 7.3.8.4 Market size, by end-use, 2017 - 2030 (USD Million)

- 7.3.9 France

- 7.3.9.1 Market size, by product, 2017 - 2030 (USD Million)

- 7.3.9.2 Market size, by product, 2017 - 2030 (Units)

- 7.3.9.3 Market size, by indication, 2017 - 2030 (USD Million)

- 7.3.9.4 Market size, by end-use, 2017 - 2030 (USD Million)

- 7.3.10 Spain

- 7.3.10.1 Market size, by product, 2017 - 2030 (USD Million)

- 7.3.10.2 Market size, by product, 2017 - 2030 (Units)

- 7.3.10.3 Market size, by indication, 2017 - 2030 (USD Million)

- 7.3.10.4 Market size, by end-use, 2017 - 2030 (USD Million)

- 7.3.11 Italy

- 7.3.11.1 Market size, by product, 2017 - 2030 (USD Million)

- 7.3.11.2 Market size, by product, 2017 - 2030 (Units)

- 7.3.11.3 Market size, by indication, 2017 - 2030 (USD Million)

- 7.3.11.4 Market size, by end-use, 2017 - 2030 (USD Million)

- 7.3.12 The Netherlands

- 7.3.12.1 Market size, by product, 2017 - 2030 (USD Million)

- 7.3.12.2 Market size, by product, 2017 - 2030 (Units)

- 7.3.12.3 Market size, by indication, 2017 - 2030 (USD Million)

- 7.3.12.4 Market size, by end-use, 2017 - 2030 (USD Million)

- 7.3.13 Switzerland

- 7.3.13.1 Market size, by product, 2017 - 2030 (USD Million)

- 7.3.13.2 Market size, by product, 2017 - 2030 (Units)

- 7.3.13.3 Market size, by indication, 2017 - 2030 (USD Million)

- 7.3.13.4 Market size, by end-use, 2017 - 2030 (USD Million)

- 7.4 RoW

- 7.4.1 Market size, by product, 2017 - 2030 (USD Million)

- 7.4.2 Market size, by product, 2017 - 2030 (Units)

- 7.4.3 Market size, by indication, 2017 - 2030 (USD Million)

- 7.4.4 Market size, by end-use, 2017 - 2030 (USD Million)

Chapter 8 Company Profiles

- 8.1 Competitive dashboard, 2021

- 8.2 Inspire Medical Systems, Inc.

- 8.2.1 Business overview

- 8.2.2 Financial data

- 8.2.3 Product landscape

- 8.2.4 Strategic outlook

- 8.2.5 SWOT analysis

- 8.3 Medtronic plc

- 8.3.1 Business overview

- 8.3.2 Financial data

- 8.3.3 Product landscape

- 8.3.4 Strategic outlook

- 8.3.5 SWOT analysis

- 8.4 Nyxoah SA

- 8.4.1 Business overview

- 8.4.2 Financial data

- 8.4.3 Product landscape

- 8.4.4 Strategic outlook

- 8.4.5 SWOT analysis

- 8.5 Siesta Medical

- 8.5.1 Business overview

- 8.5.2 Financial data

- 8.5.3 Product landscape

- 8.5.4 Strategic outlook

- 8.5.5 SWOT analysis

- 8.6 Respicardia, Inc. (Asahi Kasei Company)

- 8.6.1 Business overview

- 8.6.2 Financial data

- 8.6.3 Product landscape

- 8.6.4 Strategic outlook

- 8.6.5 SWOT analysis

- 8.7 LivaNova

- 8.7.1 Business overview

- 8.7.2 Financial data

- 8.7.3 Product landscape

- 8.7.4 Strategic outlook

- 8.7.5 SWOT analysis