|

|

市場調査レポート

商品コード

1100652

POC (ポイントオブケア) 検査の世界市場 (2022-2030年):市場規模 (製品・技術・処方・用途・エンドユーザー別)・地域的展望・用途の潜在性・市場シェア・予測Point of Care Testing Market Size By Product, By Technology, By Prescription, By Application, By End-use, Industry Analysis Report, Regional Outlook, Application Potential, Competitive Market Share & Forecast, 2022 - 2030 |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| POC (ポイントオブケア) 検査の世界市場 (2022-2030年):市場規模 (製品・技術・処方・用途・エンドユーザー別)・地域的展望・用途の潜在性・市場シェア・予測 |

|

出版日: 2022年07月06日

発行: Global Market Insights Inc.

ページ情報: 英文 430 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

POC (ポイントオブケア) 検査の市場は、急性疾患患者の増加により、2030年にかけて大きな成長を遂げると予想されています。

近年、新型コロナウイルス感染症 (COVID-19) への曝露リスクから病院での検査が減少しており、POC検査の製品需要が高まっています。また、POC検査の重要な利点である迅速な検査は、COVID-19の大流行時にプラスの影響を及ぼしました。

製品別で見ると、血液検査製品の部門が2021年に約38億9,170万米ドルを示し、2030年にかけても大規模な利益を得ると予測されています。技術別では、分子診断薬の部門が予測期間中に約8.0%のCAGRを記録すると予測されています。

当レポートでは、世界のPOC (ポイントオブケア) 検査の市場を調査し、市場の定義と概要、市場成長への各種影響因子の分析、市場規模の推移・予測、各種区分・地域/主要国別の内訳、競合環境、主要企業のプロファイルなどをまとめています。

目次

第1章 調査手法

第2章 エグゼクティブサマリー

第3章 POC (ポイントオブケア) 検査産業の考察

- 産業の分類

- 産業情勢

- 産業への影響要因

- 促進要因

- 潜在的リスク&課題

- 成長の可能性

- COVID-19:影響分析

- 価格分析:心臓マーカー別

- 規制状況

- 技術情勢

- 企業シェア分析

- ポーターの分析

- 競合情勢

- PESTEL分析

第4章 POC (ポイントオブケア) 検査市場:製品別

- 主要動向

- 血糖モニタリング

- ストリップ

- メートル

- ランセット

- 心臓代謝検査製品

- 心臓マーカー検査製品

- 血液ガス/電解質検査製品

- HBA1C検査製品

- 感染症検査製品

- インフルエンザ検査製品

- HIV検査製品

- C型肝炎検査製品

- 性感染症(STD)検査製品

- 医療関連感染(HAI)検査製品

- 呼吸器感染症検査製品

- 熱帯病検査製品

- その他の感染症検査製品

- 凝固検査製品

- PT/INR検査製品

- 活性化凝固時間(ACT/APTT)検査製品

- 妊娠および出生力検査製品

- 妊娠検査製品

- 出生力検査製品

- 腫瘍/癌マーカー検査製品

- コレステロール検査製品

- 血液検査製品

- 薬物乱用(DoA)検査製品

- 便潜血検査製品

- 尿検査製品

- その他

第5章 POC (ポイントオブケア) 検査市場:技術別

- 主要動向

- イムノクロマトグラフィー

- ディップスティック

- マイクロ流体

- 分子診断

- 免疫学的検査

- 凝集アッセイ

- フロースルー

- 固相検査

- バイオセンサー

第6章 POC (ポイントオブケア) 検査市場:処方別

- 主要動向

- OTC検査

- 処方検査

第7章 POC (ポイントオブケア) 検査市場:用途別

- 主要動向

- 心臓代謝検査

- 感染症検査

- 腎臓検査

- 薬物乱用(DoA)検査

- 血糖値検査

- 妊娠検査

- 癌バイオマーカー検査

- その他

第8章 POC (ポイントオブケア) 検査市場:エンドユーザー別

- 主要動向

- 病院

- 診断センター

- 研究ラボ

- 在宅ケア

- その他

第9章 POC (ポイントオブケア) 検査市場:地域別

- 主要動向

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第10章 企業プロファイル

- 競合ダッシュボード

- Abaxis

- Abbott

- Accubiotech Co, Ltd.

- ACON Laboratories, Inc

- Becton, Dickinson and Company

- bioLytical Laboratories Inc

- BioMrieux SA

- Bio-Rad Laboratories, Inc

- HemoCue AB(Danaher Corporation)

- Dexcom, Inc

- Dragerwerk Ag & Co

- LifeScan IP Holdings, LLC

- Medtronic plc

- Meridian Bioscience, Inc

- Nova Biomedical

- OraSure Technologies, Inc

- F. Hoffmann-La Roche

- Siemens Healthineers AG

- Sysmex Corporation

- Trinity Biotech

The point of care testing market is expected to witness massive growth through 2030 owing to increasing number of patients with acute illnesses.

Recently, testing in hospitals saw a decline due to the risk of exposure to the novel coronavirus in these settings, which fueled product demand as point of care testing offers flexibility with regards to location. Additionally, rapid testing, a pivotal advantage of point of care assays, has also positively influenced market uptake during the COVID-19 pandemic.

Notably, surging research emphasis by industry players has been beneficial for the product landscape, which has enhanced overall market dynamics. For instance, in June 2022, LumiraDx, a UK-based diagnostics company reported that it had gained CE Mark for its product, the Amira Analyzer. This portable instrument is used for rapid COVID-19 testing.

The point of care testing market has been bifurcated on the basis of technology, application, product, prescription, end-use, and region.

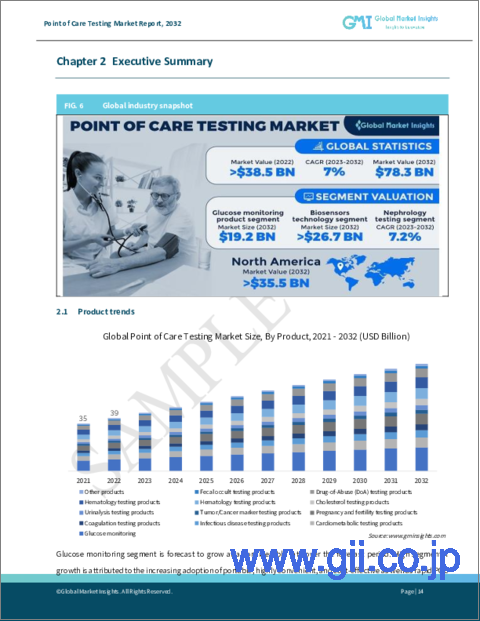

On the basis of product, the market has been bifurcated into cardiometabolic testing products, coagulation testing products, tumor/cancer marker testing products, Drug-of-Abuse (DoA) testing products, cholesterol testing products, glucose monitoring, infectious disease testing products, pregnancy and fertility testing products, urinalysis testing products, hematology testing products, fecal occult testing products, and other products. Among these, the hematology testing products segment was valued at approximately $3,891.7 million in 2021 and is speculated to amass notable gains over 2022-2030.

In terms of technology, the point of care testing market has been segmented into dipsticks, molecular diagnostics, agglutination assays, solid phase, biosensors, flow-through, immunoassays, microfluidics, and lateral flow assays. The molecular diagnostics segment is expected to register a CAGR of around 8.0% over the analysis timeframe.

In context of prescription, the market has been divided into prescription-based testing and OTC testing. The prescription-based testing segment contributed to a market share of roughly 46.1% in 2021 and is estimated to exhibit solid growth in the upcoming time period.

Based on application, the point of care testing market has been divided into infectious disease testing, Drug-of-Abuse (DoA) testing, pregnancy testing, cardio metabolic testing, nephrology testing, blood glucose testing, cancer biomarker testing, and other applications. The infectious disease testing segment is set to witness steady growth, expanding at around 8.1% CAGR through the review period.

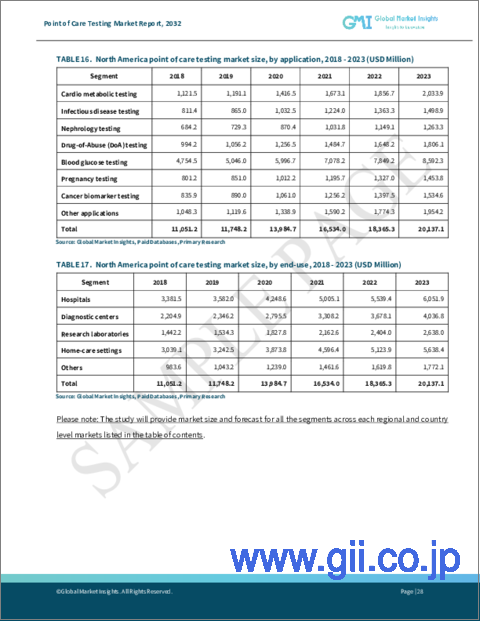

On the basis of end-use, the market has been divided into diagnostic centers, home-care settings, hospitals, research laboratories, and others. The research laboratories segment reached more than $4,111.8 million in revenue in 2021.

On the regional front, the point of care testing market in Latin America accounted for nearly 5.8% of the overall industry revenue in 2021. On the other hand, the Middle East & Africa point of care testing industry is set to experience robust growth at a CAGR of about 8.6% over the forecast period.

Table of Contents

Chapter 1 Methodology

- 1.1 Market definitions

- 1.2 Base estimates & working

- 1.3 Forecast parameters

- 1.4 Data validation

- 1.5 Data Sources

- 1.5.1 Secondary

- 1.5.1.1 Paid sources

- 1.5.1.2 Unpaid sources

- 1.5.2 Primary

- 1.5.1 Secondary

Chapter 2 Executive Summary

- 2.1 Point of care testing industry 360 degree synopsis, 2017 - 2030

- 2.1.1 Business trends

- 2.1.2 Product trends

- 2.1.3 Technology trends

- 2.1.4 Prescription trends

- 2.1.5 Application trends

- 2.1.6 End-use trends

- 2.1.7 Regional trends

Chapter 3 Point of Care Testing Industry Insights

- 3.1 Industry segmentation

- 3.2 Industry landscape, 2017 - 2030

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Upward trend in disease prevalence among developing countries

- 3.3.1.2 Surging number of pathology labs and services equipped with advanced diagnostic equipment in North America

- 3.3.1.3 Technological advancements

- 3.3.1.4 Increasing R&D investment

- 3.3.1.5 Growing geriatric population base globally

- 3.3.2 Industry pitfalls & challenges

- 3.3.2.1 Increasing R&D investment

- 3.3.2.2 High cost of product development

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.4.1 By product

- 3.4.2 By technology

- 3.4.3 By prescription

- 3.4.4 By application

- 3.4.5 By end-use

- 3.5 COVID-19 impact analysis

- 3.6 Pricing analysis, by cardiac markers, 2021

- 3.7 Regulatory landscape

- 3.8 Technology landscape

- 3.9 Company share analysis, 2021 (by region)

- 3.9.1 Global market share analysis, 2021

- 3.9.2 North America

- 3.9.3 Europe

- 3.9.4 Asia Pacific

- 3.9.5 Latin America

- 3.9.6 MEA

- 3.10 Porter's analysis

- 3.11 Competitive landscape, 2021

- 3.11.1 Company matrix analysis, 2021

- 3.12 PESTEL analysis

Chapter 4 Point of Care Testing Market, By Product

- 4.1 Key segment trends

- 4.2 Glucose monitoring

- 4.2.1 Market size, by region, 2017 - 2030 (USD Million)

- 4.2.2 Strips

- 4.2.2.1 Market size, by region, 2017 - 2030 (USD Million)

- 4.2.3 Meters

- 4.2.3.1 Market size, by region, 2017 - 2030 (USD Million)

- 4.2.4 Lancets

- 4.2.4.1 Market size, by region, 2017 - 2030 (USD Million)

- 4.3 Cardiometabolic testing products

- 4.3.1 Market size, by region, 2017 - 2030 (USD Million)

- 4.3.2 Cardiac marker testing products

- 4.3.2.1 Market size, by region, 2017-2030 (USD Million)

- 4.3.2.2 High sensitivity troponin I (hsTnI)

- 4.3.2.2.1 Market size, by region, 2017-2030 (USD Million)

- 4.3.2.3 Brain natriuretic peptide (BNP)

- 4.3.2.3.1 Market size, by region, 2017-2030 (USD Million)

- 4.3.2.4 D-dimer

- 4.3.2.4.1 Market size, by region, 2017-2030 (USD Million)

- 4.3.2.5 Creatine kinase-MB (CK-MB)

- 4.3.2.5.1 Market size, by region, 2017-2030 (USD Million)

- 4.3.2.6 Myoglobin

- 4.3.2.6.1 Market size, by region, 2017-2030 (USD Million)

- 4.3.2.7 Others

- 4.3.2.7.1 Market size, by region, 2017-2030 (USD Million)

- 4.3.3 Blood Gas/Electrolytes testing products

- 4.3.3.1 Market size, by region, 2017-2030 (USD Million)

- 4.3.4 HBA1C testing products

- 4.3.4.1 Market size, by region, 2017-2030 (USD Million)

- 4.4 Infectious disease testing products

- 4.4.1 Market size, by region, 2017-2030 (USD Million)

- 4.4.2 Influenza testing products

- 4.4.2.1 Market size, by region, 2017-2030 (USD Million)

- 4.4.3 HIV testing products

- 4.4.3.1 Market size, by region, 2017-2030 (USD Million)

- 4.4.4 Hepatitis C testing products

- 4.4.4.1 Market size, by region, 2017-2030 (USD Million)

- 4.4.5 Sexually transmitted disease (STD) testing products

- 4.4.5.1 Market size, by region, 2017-2030 (USD Million)

- 4.4.6 Healthcare-associated Infection (HAI) testing products

- 4.4.6.1 Market size, by region, 2017-2030 (USD Million)

- 4.4.7 Respiratory infection testing products

- 4.4.7.1 Market size, by region, 2017-2030 (USD Million)

- 4.4.8 Tropical disease testing products

- 4.4.8.1 Market size, by region, 2017-2030 (USD Million)

- 4.4.9 Other infectious diseases testing products

- 4.4.9.1 Market size, by region, 2017-2030 (USD Million)

- 4.5 Coagulation testing products

- 4.5.1 Market size, by region, 2017-2030 (USD Million)

- 4.5.2 PT/INR testing products

- 4.5.2.1 Market size, by region, 2017-2030 (USD Million)

- 4.5.3 Activated clotting time (ACT/APTT) testing products

- 4.5.3.1 Market size, by region, 2017-2030 (USD Million)

- 4.6 Pregnancy & fertility testing products

- 4.6.1 Market size, by region, 2017-2030 (USD Million)

- 4.6.2 Pregnancy testing products

- 4.6.2.1 Market size, by region, 2017-2030 (USD Million)

- 4.6.3 Fertility testing products

- 4.6.3.1 Market size, by region, 2017-2030 (USD Million)

- 4.7 Tumor/Cancer marker testing products

- 4.7.1 Market size, by region, 2017-2030 (USD Million)

- 4.8 Cholesterol testing products

- 4.8.1 Market size, by region, 2017-2030 (USD Million)

- 4.9 Hematology testing products

- 4.9.1 Market size, by region, 2017-2030 (USD Million)

- 4.10 Drug-of-Abuse (DoA) testing products

- 4.10.1 Market size, by region, 2017-2030 (USD Million)

- 4.11 Fecal occult testing products

- 4.11.1 Market size, by region, 2017-2030 (USD Million)

- 4.12 Urinalysis testing products

- 4.12.1 Market size, by region, 2017-2030 (USD Million)

- 4.13 Other products

- 4.13.1 Market size, by region, 2017-2030 (USD Million)

Chapter 5 Point of Care Testing Market, By Technology

- 5.1 Key segment trends

- 5.2 Lateral flow assays

- 5.2.1 Market size, by region, 2017 - 2030 (USD Million)

- 5.3 Dipsticks

- 5.3.1 Market size, by region, 2017 - 2030 (USD Million)

- 5.4 Microfluidics

- 5.4.1 Market size, by region, 2017 - 2030 (USD Million)

- 5.5 Molecular diagnostics

- 5.5.1 Market size, by region, 2017 - 2030 (USD Million)

- 5.6 Immunoassays

- 5.6.1 Market size, by region, 2017 - 2030 (USD Million)

- 5.7 Agglutination assays

- 5.7.1 Market size, by region, 2017 - 2030 (USD Million)

- 5.8 Flow-through

- 5.8.1 Market size, by region, 2017 - 2030 (USD Million)

- 5.9 Solid phase

- 5.9.1 Market size, by region, 2017 - 2030 (USD Million)

- 5.10 Biosensors

- 5.10.1 Market size, by region, 2017 - 2030 (USD Million)

Chapter 6 Point of Care Testing Market, By Prescription

- 6.1 Key segment trends

- 6.2 OTC testing

- 6.2.1 Market size, by region, 2017 - 2030 (USD Million)

- 6.3 Prescription-based testing

- 6.3.1 Market size, by region, 2017 - 2030 (USD Million)

Chapter 7 Point of Care Testing Market, By Application

- 7.1 Key segment trends

- 7.2 Cardio metabolic testing

- 7.2.1 Market size, by region, 2017 - 2030 (USD Million)

- 7.3 Infectious disease testing

- 7.3.1 Market size, by region, 2017 - 2030 (USD Million)

- 7.4 Nephrology testing

- 7.4.1 Market size, by region, 2017 - 2030 (USD Million)

- 7.5 Drug-of-Abuse (DoA) testing

- 7.5.1 Market size, by region, 2017 - 2030 (USD Million)

- 7.6 Blood glucose testing

- 7.6.1 Market size, by region, 2017 - 2030 (USD Million)

- 7.7 Pregnancy testing

- 7.7.1 Market size, by region, 2017 - 2030 (USD Million)

- 7.8 Cancer biomarker testing

- 7.8.1 Market size, by region, 2017 - 2030 (USD Million)

- 7.9 Other applications

- 7.9.1 Market size, by region, 2017 - 2030 (USD Million)

Chapter 8 Point of Care Testing Market, By End-use

- 8.1 Key segment trends

- 8.2 Hospitals

- 8.2.1 Market size, by region, 2017 - 2030 (USD Million)

- 8.3 Diagnostic centers

- 8.3.1 Market size, by region, 2017 - 2030 (USD Million)

- 8.4 Research laboratories

- 8.4.1 Market size, by region, 2017 - 2030 (USD Million)

- 8.5 Home-care settings

- 8.5.1 Market size, by region, 2017 - 2030 (USD Million)

- 8.6 other

- 8.6.1 Market size, by region, 2017 - 2030 (USD Million)

Chapter 9 Point of Care Testing Market, By Region

- 9.1 Key regional trends

- 9.2 North America

- 9.2.1 Market size, by country, 2017 - 2030 (USD Million)

- 9.2.2 Market size, by product, 2017 - 2030 (USD Million)

- 9.2.2.1 Market size, by glucose monitoring, 2017-2030 (USD Million)

- 9.2.2.2 Market size, by cardiometabolic testing products, 2017-2030 (USD Million)

- 9.2.2.2.1 Market size, by cardiac marker testing product, 2017-2030 (USD Million)

- 9.2.2.3 Market size, by infectious disease testing products, 2017-2030 (USD Million)

- 9.2.2.4 Market size, by coagulation testing products, 2017-2030 (USD Million)

- 9.2.2.5 Market size, by pregnancy & fertility testing products, 2017-2030 (USD Million)

- 9.2.3 Market size, by technology, 2017 - 2030 (USD Million)

- 9.2.4 Market size, by prescription, 2017 - 2030 (USD Million)

- 9.2.5 Market size, by application, 2017 - 2030 (USD Million)

- 9.2.6 Market size, by end-use, 2017 - 2030 (USD Million)

- 9.2.7 U.S.

- 9.2.7.1 Market size, by product, 2017 - 2030 (USD Million)

- 9.2.7.1.1 Market size, by glucose monitoring, 2017-2030 (USD Million)

- 9.2.7.1.2 Market size, by cardiometabolic testing products, 2017-2030 (USD Million)

- 9.2.7.1.2.1 Market size, by cardiac marker testing product, 2017-2030 (USD Million)

- 9.2.7.1.3 Market size, by infectious disease testing products, 2017-2030 (USD Million)

- 9.2.7.1.4 Market size, by coagulation testing products, 2017-2030 (USD Million)

- 9.2.7.1.5 Market size, by pregnancy & fertility testing products, 2017-2030 (USD Million)

- 9.2.7.2 Market size, by technology, 2017 - 2030 (USD Million)

- 9.2.7.3 Market size, by prescription, 2017 - 2030 (USD Million)

- 9.2.7.4 Market size, by application, 2017 - 2030 (USD Million)

- 9.2.7.5 Market size, by end-use, 2017 - 2030 (USD Million)

- 9.2.7.1 Market size, by product, 2017 - 2030 (USD Million)

- 9.2.8 Canada

- 9.2.8.1 Market size, by product, 2017 - 2030 (USD Million)

- 9.2.8.1.1 Market size, by glucose monitoring, 2017-2030 (USD Million)

- 9.2.8.1.2 Market size, by cardiometabolic testing products, 2017-2030 (USD Million)

- 9.2.8.1.2.1 Market size, by cardiac marker testing product, 2017-2030 (USD Million)

- 9.2.8.1.3 Market size, by infectious disease testing products, 2017-2030 (USD Million)

- 9.2.8.1.4 Market size, by coagulation testing products, 2017-2030 (USD Million)

- 9.2.8.1.5 Market size, by pregnancy & fertility testing products, 2017-2030 (USD Million)

- 9.2.8.2 Market size, by technology, 2017 - 2030 (USD Million)

- 9.2.8.3 Market size, by prescription, 2017 - 2030 (USD Million)

- 9.2.8.4 Market size, by application, 2017 - 2030 (USD Million)

- 9.2.8.5 Market size, by end-use, 2017 - 2030 (USD Million)

- 9.2.8.1 Market size, by product, 2017 - 2030 (USD Million)

- 9.3 Europe

- 9.3.1 Market size, by country, 2017 - 2030 (USD Million)

- 9.3.2 Market size, by product, 2017 - 2030 (USD Million)

- 9.3.2.1 Market size, by glucose monitoring, 2017-2030 (USD Million)

- 9.3.2.2 Market size, by cardiometabolic testing products, 2017-2030 (USD Million)

- 9.3.2.2.1 Market size, by cardiac marker testing product, 2017-2030 (USD Million)

- 9.3.2.3 Market size, by infectious disease testing products, 2017-2030 (USD Million)

- 9.3.2.4 Market size, by coagulation testing products, 2017-2030 (USD Million)

- 9.3.2.5 Market size, by pregnancy & fertility testing products, 2017-2030 (USD Million)

- 9.3.3 Market size, by technology, 2017 - 2030 (USD Million)

- 9.3.4 Market size, by prescription, 2017 - 2030 (USD Million)

- 9.3.5 Market size, by application, 2017 - 2030 (USD Million)

- 9.3.6 Market size, by end-use, 2017 - 2030 (USD Million)

- 9.3.7 Germany

- 9.3.7.1 Market size, by product, 2017 - 2030 (USD Million)

- 9.3.7.1.1 Market size, by glucose monitoring, 2017-2030 (USD Million)

- 9.3.7.1.2 Market size, by cardiometabolic testing products, 2017-2030 (USD Million)

- 9.3.7.1.2.1 Market size, by cardiac marker testing product, 2017-2030 (USD Million)

- 9.3.7.1.3 Market size, by infectious disease testing products, 2017-2030 (USD Million)

- 9.3.7.1.4 Market size, by coagulation testing products, 2017-2030 (USD Million)

- 9.3.7.1.5 Market size, by pregnancy & fertility testing products, 2017-2030 (USD Million)

- 9.3.7.2 Market size, by technology, 2017 - 2030 (USD Million)

- 9.3.7.3 Market size, by prescription, 2017 - 2030 (USD Million)

- 9.3.7.4 Market size, by application, 2017 - 2030 (USD Million)

- 9.3.7.5 Market size, by end-use, 2017 - 2030 (USD Million)

- 9.3.7.1 Market size, by product, 2017 - 2030 (USD Million)

- 9.3.8 UK

- 9.3.8.1 Market size, by product, 2017 - 2030 (USD Million)

- 9.3.8.1.1 Market size, by glucose monitoring, 2017-2030 (USD Million)

- 9.3.8.1.2 Market size, by cardiometabolic testing products, 2017-2030 (USD Million)

- 9.3.8.1.2.1 Market size, by cardiac marker testing product, 2017-2030 (USD Million)

- 9.3.8.1.3 Market size, by infectious disease testing products, 2017-2030 (USD Million)

- 9.3.8.1.4 Market size, by coagulation testing products, 2017-2030 (USD Million)

- 9.3.8.1.5 Market size, by pregnancy & fertility testing products, 2017-2030 (USD Million)

- 9.3.8.2 Market size, by technology, 2017 - 2030 (USD Million)

- 9.3.8.3 Market size, by prescription, 2017 - 2030 (USD Million)

- 9.3.8.4 Market size, by application, 2017 - 2030 (USD Million)

- 9.3.8.5 Market size, by end-use, 2017 - 2030 (USD Million)

- 9.3.8.1 Market size, by product, 2017 - 2030 (USD Million)

- 9.3.9 France

- 9.3.9.1 Market size, by product, 2017 - 2030 (USD Million)

- 9.3.9.1.1 Market size, by glucose monitoring, 2017-2030 (USD Million)

- 9.3.9.1.2 Market size, by cardiometabolic testing products, 2017-2030 (USD Million)

- 9.3.9.1.2.1 Market size, by cardiac marker testing product, 2017-2030 (USD Million)

- 9.3.9.1.3 Market size, by infectious disease testing products, 2017-2030 (USD Million)

- 9.3.9.1.4 Market size, by coagulation testing products, 2017-2030 (USD Million)

- 9.3.9.1.5 Market size, by pregnancy & fertility testing products, 2017-2030 (USD Million)

- 9.3.9.2 Market size, by technology, 2017 - 2030 (USD Million)

- 9.3.9.3 Market size, by prescription, 2017 - 2030 (USD Million)

- 9.3.9.4 Market size, by application, 2017 - 2030 (USD Million)

- 9.3.9.5 Market size, by end-use, 2017 - 2030 (USD Million)

- 9.3.9.1 Market size, by product, 2017 - 2030 (USD Million)

- 9.3.10 Spain

- 9.3.10.1 Market size, by product, 2017 - 2030 (USD Million)

- 9.3.10.1.1 Market size, by glucose monitoring, 2017-2030 (USD Million)

- 9.3.10.1.2 Market size, by cardiometabolic testing products, 2017-2030 (USD Million)

- 9.3.10.1.2.1 Market size, by cardiac marker testing product, 2017-2030 (USD Million)

- 9.3.10.1.3 Market size, by infectious disease testing products, 2017-2030 (USD Million)

- 9.3.10.1.4 Market size, by coagulation testing products, 2017-2030 (USD Million)

- 9.3.10.1.5 Market size, by pregnancy & fertility testing products, 2017-2030 (USD Million)

- 9.3.10.2 Market size, by technology, 2017 - 2030 (USD Million)

- 9.3.10.3 Market size, by prescription, 2017 - 2030 (USD Million)

- 9.3.10.4 Market size, by application, 2017 - 2030 (USD Million)

- 9.3.10.5 Market size, by end-use, 2017 - 2030 (USD Million)

- 9.3.10.1 Market size, by product, 2017 - 2030 (USD Million)

- 9.3.11 Italy

- 9.3.11.1 Market size, by product, 2017 - 2030 (USD Million)

- 9.3.11.1.1 Market size, by glucose monitoring, 2017-2030 (USD Million)

- 9.3.11.1.2 Market size, by cardiometabolic testing products, 2017-2030 (USD Million)

- 9.3.11.1.2.1 Market size, by cardiac marker testing product, 2017-2030 (USD Million)

- 9.3.11.1.3 Market size, by infectious disease testing products, 2017-2030 (USD Million)

- 9.3.11.1.4 Market size, by coagulation testing products, 2017-2030 (USD Million)

- 9.3.11.1.5 Market size, by pregnancy & fertility testing products, 2017-2030 (USD Million)

- 9.3.11.2 Market size, by technology, 2017 - 2030 (USD Million)

- 9.3.11.3 Market size, by prescription, 2017 - 2030 (USD Million)

- 9.3.11.4 Market size, by application, 2017 - 2030 (USD Million)

- 9.3.11.5 Market size, by end-use, 2017 - 2030 (USD Million)

- 9.3.11.1 Market size, by product, 2017 - 2030 (USD Million)

- 9.4 Asia Pacific

- 9.4.1 Market size, by country, 2017 - 2030 (USD Million)

- 9.4.2 Market size, by product, 2017 - 2030 (USD Million)

- 9.4.2.1 Market size, by glucose monitoring, 2017-2030 (USD Million)

- 9.4.2.2 Market size, by cardiometabolic testing products, 2017-2030 (USD Million)

- 9.4.2.2.1 Market size, by cardiac marker testing product, 2017-2030 (USD Million)

- 9.4.2.3 Market size, by infectious disease testing products, 2017-2030 (USD Million)

- 9.4.2.4 Market size, by coagulation testing products, 2017-2030 (USD Million)

- 9.4.2.5 Market size, by pregnancy & fertility testing products, 2017-2030 (USD Million)

- 9.4.3 Market size, by technology, 2017 - 2030 (USD Million)

- 9.4.4 Market size, by prescription, 2017 - 2030 (USD Million)

- 9.4.5 Market size, by application, 2017 - 2030 (USD Million)

- 9.4.6 Market size, by end-use, 2017 - 2030 (USD Million)

- 9.4.7 China

- 9.4.7.1 Market size, by product, 2017 - 2030 (USD Million)

- 9.4.7.1.1 Market size, by glucose monitoring, 2017-2030 (USD Million)

- 9.4.7.1.2 Market size, by cardiometabolic testing products, 2017-2030 (USD Million)

- 9.4.7.1.2.1 Market size, by cardiac marker testing product, 2017-2030 (USD Million)

- 9.4.7.1.3 Market size, by infectious disease testing products, 2017-2030 (USD Million)

- 9.4.7.1.4 Market size, by coagulation testing products, 2017-2030 (USD Million)

- 9.4.7.1.5 Market size, by pregnancy & fertility testing products, 2017-2030 (USD Million)

- 9.4.7.2 Market size, by technology, 2017 - 2030 (USD Million)

- 9.4.7.3 Market size, by prescription, 2017 - 2030 (USD Million)

- 9.4.7.4 Market size, by application, 2017 - 2030 (USD Million)

- 9.4.7.5 Market size, by end-use, 2017 - 2030 (USD Million)

- 9.4.7.1 Market size, by product, 2017 - 2030 (USD Million)

- 9.4.8 India

- 9.4.8.1 Market size, by product, 2017 - 2030 (USD Million)

- 9.4.8.1.1 Market size, by glucose monitoring, 2017-2030 (USD Million)

- 9.4.8.1.2 Market size, by cardiometabolic testing products, 2017-2030 (USD Million)

- 9.4.8.1.2.1 Market size, by cardiac marker testing product, 2017-2030 (USD Million)

- 9.4.8.1.3 Market size, by infectious disease testing products, 2017-2030 (USD Million)

- 9.4.8.1.4 Market size, by coagulation testing products, 2017-2030 (USD Million)

- 9.4.8.1.5 Market size, by pregnancy & fertility testing products, 2017-2030 (USD Million)

- 9.4.8.2 Market size, by technology, 2017 - 2030 (USD Million)

- 9.4.8.3 Market size, by prescription, 2017 - 2030 (USD Million)

- 9.4.8.4 Market size, by application, 2017 - 2030 (USD Million)

- 9.4.8.5 Market size, by end-use, 2017 - 2030 (USD Million)

- 9.4.8.1 Market size, by product, 2017 - 2030 (USD Million)

- 9.4.9 Japan

- 9.4.9.1 Market size, by product, 2017 - 2030 (USD Million)

- 9.4.9.1.1 Market size, by glucose monitoring, 2017-2030 (USD Million)

- 9.4.9.1.2 Market size, by cardiometabolic testing products, 2017-2030 (USD Million)

- 9.4.9.1.2.1 Market size, by cardiac marker testing product, 2017-2030 (USD Million)

- 9.4.9.1.3 Market size, by infectious disease testing products, 2017-2030 (USD Million)

- 9.4.9.1.4 Market size, by coagulation testing products, 2017-2030 (USD Million)

- 9.4.9.1.5 Market size, by pregnancy & fertility testing products, 2017-2030 (USD Million)

- 9.4.9.2 Market size, by technology, 2017 - 2030 (USD Million)

- 9.4.9.3 Market size, by prescription, 2017 - 2030 (USD Million)

- 9.4.9.4 Market size, by application, 2017 - 2030 (USD Million)

- 9.4.9.5 Market size, by end-use, 2017 - 2030 (USD Million)

- 9.4.9.1 Market size, by product, 2017 - 2030 (USD Million)

- 9.4.10 Australia

- 9.4.10.1 Market size, by product, 2017 - 2030 (USD Million)

- 9.4.10.1.1 Market size, by glucose monitoring, 2017-2030 (USD Million)

- 9.4.10.1.2 Market size, by cardiometabolic testing products, 2017-2030 (USD Million)

- 9.4.10.1.2.1 Market size, by cardiac marker testing product, 2017-2030 (USD Million)

- 9.4.10.1.3 Market size, by infectious disease testing products, 2017-2030 (USD Million)

- 9.4.10.1.4 Market size, by coagulation testing products, 2017-2030 (USD Million)

- 9.4.10.1.5 Market size, by pregnancy & fertility testing products, 2017-2030 (USD Million)

- 9.4.10.2 Market size, by technology, 2017 - 2030 (USD Million)

- 9.4.10.3 Market size, by prescription, 2017 - 2030 (USD Million)

- 9.4.10.4 Market size, by application, 2017 - 2030 (USD Million)

- 9.4.10.5 Market size, by end-use, 2017 - 2030 (USD Million)

- 9.4.10.1 Market size, by product, 2017 - 2030 (USD Million)

- 9.5 Latin America

- 9.5.1 Market size, by country, 2017 - 2030 (USD Million)

- 9.5.2 Market size, by product, 2017 - 2030 (USD Million)

- 9.5.2.1 Market size, by glucose monitoring, 2017-2030 (USD Million)

- 9.5.2.2 Market size, by cardiometabolic testing products, 2017-2030 (USD Million)

- 9.5.2.2.1 Market size, by cardiac marker testing product, 2017-2030 (USD Million)

- 9.5.2.3 Market size, by infectious disease testing products, 2017-2030 (USD Million)

- 9.5.2.4 Market size, by coagulation testing products, 2017-2030 (USD Million)

- 9.5.2.5 Market size, by pregnancy & fertility testing products, 2017-2030 (USD Million)

- 9.5.3 Market size, by technology, 2017 - 2030 (USD Million)

- 9.5.4 Market size, by prescription, 2017 - 2030 (USD Million)

- 9.5.5 Market size, by application, 2017 - 2030 (USD Million)

- 9.5.6 Market size, by end-use, 2017 - 2030 (USD Million)

- 9.5.7 Brazil

- 9.5.7.1 Market size, by product, 2017 - 2030 (USD Million)

- 9.5.7.1.1 Market size, by glucose monitoring, 2017-2030 (USD Million)

- 9.5.7.1.2 Market size, by cardiometabolic testing products, 2017-2030 (USD Million)

- 9.5.7.1.2.1 Market size, by cardiac marker testing product, 2017-2030 (USD Million)

- 9.5.7.1.3 Market size, by infectious disease testing products, 2017-2030 (USD Million)

- 9.5.7.1.4 Market size, by coagulation testing products, 2017-2030 (USD Million)

- 9.5.7.1.5 Market size, by pregnancy & fertility testing products, 2017-2030 (USD Million)

- 9.5.7.2 Market size, by technology, 2017 - 2030 (USD Million)

- 9.5.7.3 Market size, by prescription, 2017 - 2030 (USD Million)

- 9.5.7.4 Market size, by application, 2017 - 2030 (USD Million)

- 9.5.7.5 Market size, by end-use, 2017 - 2030 (USD Million)

- 9.5.7.1 Market size, by product, 2017 - 2030 (USD Million)

- 9.5.8 Mexico

- 9.5.8.1 Market size, by product, 2017 - 2030 (USD Million)

- 9.5.8.1.1 Market size, by glucose monitoring, 2017-2030 (USD Million)

- 9.5.8.1.2 Market size, by cardiometabolic testing products, 2017-2030 (USD Million)

- 9.5.8.1.2.1 Market size, by cardiac marker testing product, 2017-2030 (USD Million)

- 9.5.8.1.3 Market size, by infectious disease testing products, 2017-2030 (USD Million)

- 9.5.8.1.4 Market size, by coagulation testing products, 2017-2030 (USD Million)

- 9.5.8.1.5 Market size, by pregnancy & fertility testing products, 2017-2030 (USD Million)

- 9.5.8.2 Market size, by technology, 2017 - 2030 (USD Million)

- 9.5.8.3 Market size, by prescription, 2017 - 2030 (USD Million)

- 9.5.8.4 Market size, by application, 2017 - 2030 (USD Million)

- 9.5.8.5 Market size, by end-use, 2017 - 2030 (USD Million)

- 9.5.8.1 Market size, by product, 2017 - 2030 (USD Million)

- 9.6 MEA

- 9.6.1 Market size, by country, 2017 - 2030 (USD Million)

- 9.6.2 Market size, by product, 2017 - 2030 (USD Million)

- 9.6.2.1 Market size, by glucose monitoring, 2017-2030 (USD Million)

- 9.6.2.2 Market size, by cardiometabolic testing products, 2017-2030 (USD Million)

- 9.6.2.2.1 Market size, by cardiac marker testing product, 2017-2030 (USD Million)

- 9.6.2.3 Market size, by infectious disease testing products, 2017-2030 (USD Million)

- 9.6.2.4 Market size, by coagulation testing products, 2017-2030 (USD Million)

- 9.6.2.5 Market size, by pregnancy & fertility testing products, 2017-2030 (USD Million)

- 9.6.3 Market size, by technology, 2017 - 2030 (USD Million)

- 9.6.4 Market size, by prescription, 2017 - 2030 (USD Million)

- 9.6.5 Market size, by application, 2017 - 2030 (USD Million)

- 9.6.6 Market size, by end-use, 2017 - 2030 (USD Million)

- 9.6.7 South Africa

- 9.6.7.1 Market size, by product, 2017 - 2030 (USD Million)

- 9.6.7.1.1 Market size, by glucose monitoring, 2017-2030 (USD Million)

- 9.6.7.1.2 Market size, by cardiometabolic testing products, 2017-2030 (USD Million)

- 9.6.7.1.2.1 Market size, by cardiac marker testing product, 2017-2030 (USD Million)

- 9.6.7.1.3 Market size, by infectious disease testing products, 2017-2030 (USD Million)

- 9.6.7.1.4 Market size, by coagulation testing products, 2017-2030 (USD Million)

- 9.6.7.1.5 Market size, by pregnancy & fertility testing products, 2017-2030 (USD Million)

- 9.6.7.2 Market size, by technology, 2017 - 2030 (USD Million)

- 9.6.7.3 Market size, by prescription, 2017 - 2030 (USD Million)

- 9.6.7.4 Market size, by application, 2017 - 2030 (USD Million)

- 9.6.7.5 Market size, by end-use, 2017 - 2030 (USD Million)

- 9.6.7.1 Market size, by product, 2017 - 2030 (USD Million)

- 9.6.8 Saudi Arabia

- 9.6.8.1 Market size, by product, 2017 - 2030 (USD Million)

- 9.6.8.1.1 Market size, by glucose monitoring, 2017-2030 (USD Million)

- 9.6.8.1.2 Market size, by cardiometabolic testing products, 2017-2030 (USD Million)

- 9.6.8.1.2.1 Market size, by cardiac marker testing product, 2017-2030 (USD Million)

- 9.6.8.1.3 Market size, by infectious disease testing products, 2017-2030 (USD Million)

- 9.6.8.1.4 Market size, by coagulation testing products, 2017-2030 (USD Million)

- 9.6.8.1.5 Market size, by pregnancy & fertility testing products, 2017-2030 (USD Million)

- 9.6.8.2 Market size, by technology, 2017 - 2030 (USD Million)

- 9.6.8.3 Market size, by prescription, 2017 - 2030 (USD Million)

- 9.6.8.4 Market size, by application, 2017 - 2030 (USD Million)

- 9.6.8.5 Market size, by end-use, 2017 - 2030 (USD Million)

- 9.6.8.1 Market size, by product, 2017 - 2030 (USD Million)

Chapter 10 Company Profiles

- 10.1 Competitive dashboard

- 10.2 Abaxis

- 10.2.1 Business overview

- 10.2.2 Financial data

- 10.2.3 Product landscape

- 10.2.4 Strategic outlook

- 10.2.5 SWOT analysis

- 10.3 Abbott

- 10.3.1 Business overview

- 10.3.2 Financial data

- 10.3.3 Product landscape

- 10.3.4 Strategic outlook

- 10.3.5 SWOT analysis

- 10.4 Accubiotech Co, Ltd.

- 10.4.1 Business overview

- 10.4.2 Financial data

- 10.4.3 Product landscape

- 10.4.4 Strategic outlook

- 10.4.5 SWOT analysis

- 10.5 ACON Laboratories, Inc

- 10.5.1 Business overview

- 10.5.2 Financial data

- 10.5.3 Product landscape

- 10.5.4 Strategic outlook

- 10.5.5 SWOT analysis

- 10.6 Becton, Dickinson and Company

- 10.6.1 Business overview

- 10.6.2 Financial data

- 10.6.3 Product landscape

- 10.6.4 Strategic outlook

- 10.6.5 SWOT analysis

- 10.7 bioLytical Laboratories Inc

- 10.7.1 Business overview

- 10.7.2 Financial data

- 10.7.3 Product landscape

- 10.7.4 Strategic outlook

- 10.7.5 SWOT analysis

- 10.8 BioMrieux SA

- 10.8.1 Business overview

- 10.8.2 Financial data

- 10.8.3 Product landscape

- 10.8.4 Strategic outlook

- 10.9 Bio-Rad Laboratories, Inc

- 10.9.1 Business overview

- 10.9.2 Financial data

- 10.9.3 Product landscape

- 10.9.4 Strategic outlook

- 10.9.5 SWOT analysis

- 10.10 HemoCue AB (Danaher Corporation)

- 10.10.1 Business overview

- 10.10.2 Financial data

- 10.10.3 Product landscape

- 10.10.4 Strategic outlook

- 10.10.5 SWOT analysis

- 10.11 Dexcom, Inc

- 10.11.1 Business overview

- 10.11.2 Financial data

- 10.11.3 Product landscape

- 10.11.4 Strategic outlook

- 10.11.5 SWOT analysis

- 10.12 Dragerwerk Ag & Co

- 10.12.1 Business overview

- 10.12.2 Financial data

- 10.12.3 Product landscape

- 10.12.4 Strategic outlook

- 10.12.5 SWOT analysis

- 10.13 LifeScan IP Holdings, LLC

- 10.13.1 Business overview

- 10.13.2 Financial data

- 10.13.3 Product landscape

- 10.13.4 Strategic outlook

- 10.13.5 SWOT analysis

- 10.14 Medtronic plc

- 10.14.1 Business overview

- 10.14.2 Financial data

- 10.14.3 Product landscape

- 10.14.4 Strategic outlook

- 10.14.5 SWOT analysis

- 10.15 Meridian Bioscience, Inc

- 10.15.1 Business overview

- 10.15.2 Financial data

- 10.15.3 Product landscape

- 10.15.4 Strategic outlook

- 10.15.5 SWOT analysis

- 10.16 Nova Biomedical

- 10.16.1 Business overview

- 10.16.2 Financial data

- 10.16.3 Product landscape

- 10.16.4 Strategic outlook

- 10.16.5 SWOT analysis

- 10.17 OraSure Technologies, Inc

- 10.17.1 Business overview

- 10.17.2 Financial data

- 10.17.3 Product landscape

- 10.17.4 Strategic outlook

- 10.17.5 SWOT analysis

- 10.18 F. Hoffmann-La Roche

- 10.18.1 Business overview

- 10.18.2 Financial data

- 10.18.3 Product landscape

- 10.18.4 Strategic outlook

- 10.18.5 SWOT analysis

- 10.19 Siemens Healthineers AG

- 10.19.1 Business overview

- 10.19.2 Financial data

- 10.19.3 Product landscape

- 10.19.4 Strategic outlook

- 10.19.5 SWOT analysis

- 10.20 Sysmex Corporation

- 10.20.1 Business overview

- 10.20.2 Financial data

- 10.20.3 Product landscape

- 10.20.4 Strategic outlook

- 10.20.5 SWOT analysis

- 10.21 Trinity Biotech

- 10.21.1 Business overview

- 10.21.2 Financial data

- 10.21.3 Product landscape

- 10.21.4 Strategic outlook

- 10.21.5 SWOT analysis