|

|

市場調査レポート

商品コード

1074638

PFAS:飲料水の処理規制、技術、浄化の予測 (2022年~2030年)PFAS: Drinking Water Treatment Regulations, Technologies, and Remediation Forecasts 2022-2030 |

||||||

|

|

|||||||

| PFAS:飲料水の処理規制、技術、浄化の予測 (2022年~2030年) |

|

出版日: 2022年05月11日

発行: Bluefield Research

ページ情報: 英文 75 Pages, 33 Company Profiles

納期: 即日から翌営業日

|

- 全表示

- 概要

- 目次

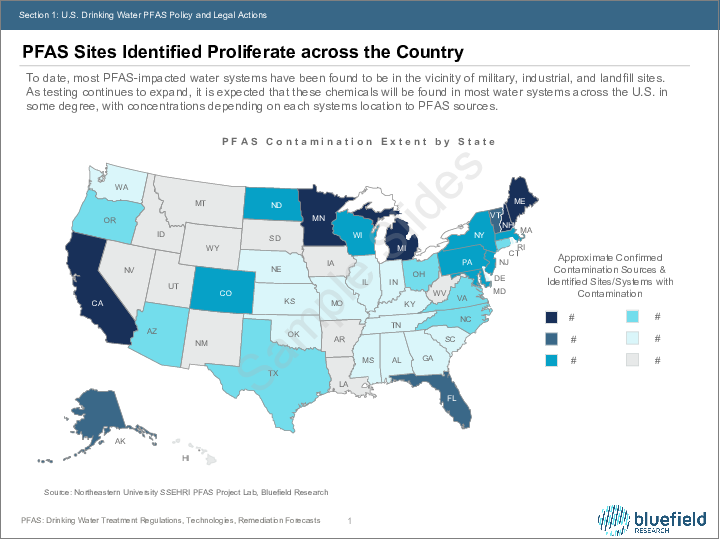

米国国内でもPFASの影響を特に強く受けた州 (ミシガン州、ニューヨーク州、ニュージャージー州など) では、飲料水中のPFAS濃度に対する独自の規制値を導入し、対応の遅れた連邦政府に先んじようとしています。米国政府も、2023年秋にPFOA・PFOSの飲料水向けMCL (最大汚染濃度) の制定を予定し、水資源中の化学物質を取り締まろうとしています。そして、全ての州でPFAS浄化の必要性が認識されています。他方、バイオソリッドの地上散布を通じて、PFASが地下水に戻ったり植物・動物に取り込まれたりする危険性について懸念が生じており、それがバイオソリッド市場を混乱させる可能性もあります。

当レポートでは、米国におけるPFAS (ペルフルオロアルキル物質およびポリフルオロアルキル化合物) 処理の技術および市場の見通しについて分析し、連邦・各州レベルでの規制・政策や、PFSAの処理技術と活用事例、関連市場の動向見通し (飲料水市場・バイオソリッド市場ほか)、世界全体でのPFSAへの対応状況、主要企業のプロファイル・戦略、といった情報を取りまとめてお届けいたします。

目次

第1章 米国の飲料水向けPFAS政策と法的措置

- 連邦の規制の推移

- 各州の飲料水向けPFAS政策

- 各州における飲料水向けMCL (最大汚染濃度) の提案・採用

- 各州の規制情勢の拡大

- PFASサイト:全国レベルでの急増

- PFASに伴う、サプライヤーへの法的措置

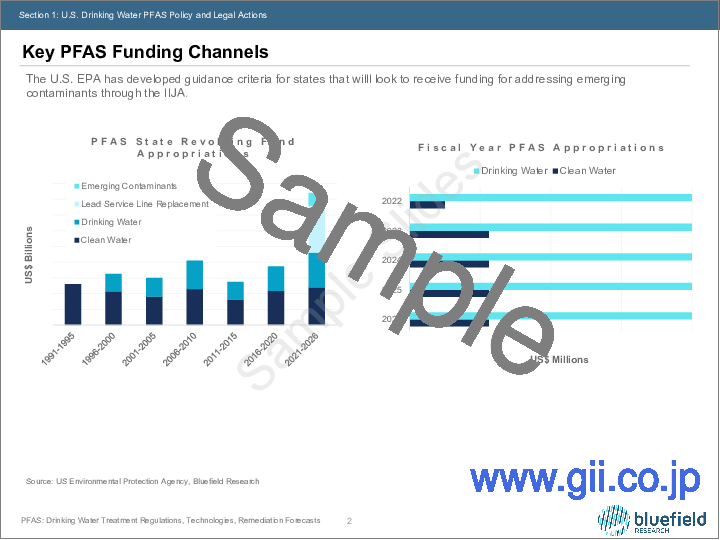

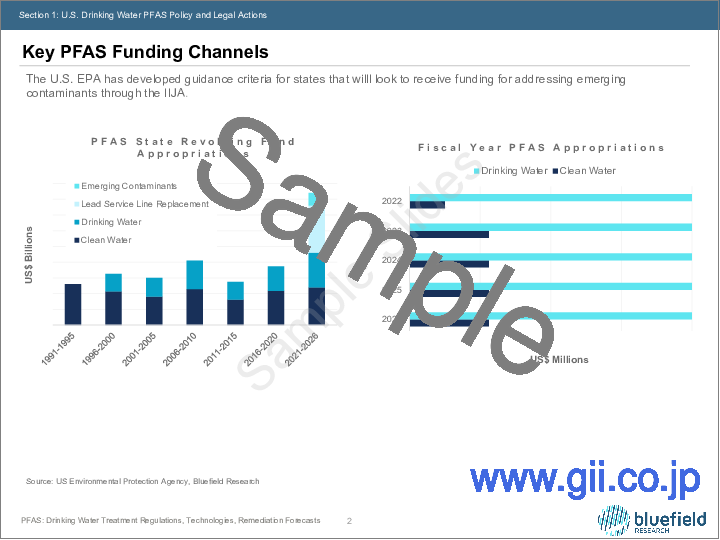

- インフラ向け資金調達によるPFAS投資の促進

- 主要なPFAS資金調達チャネル

- 技術革新への投資

- PFASアクション:投資家所有のユーティリティへの拡大

第2章 米国の飲料水市場の修正予測

- 市場の主な仮定:処理システムのアドレッサブル市場

- 飲料水市場:全体的な予測 (2022年~2030年)

- 飲料水市場:技術別の予測 (2022年~2030年)

- 飲料水市場:上位20州の予測 (2022年~2030年)

第3章 PFAS処理技術とケーススタディ

- PFAS処理:確立された新しい技術

- PFAS処理技術の成熟度

- 新たな飲料水技術の概要

- PFASの濃度・チェーンの長さ・除去能力

- 技術のケーススタディ:カリフォルニア州オレンジ郡 Placentia

- 技術のケーススタディ:カリフォルニア州オレンジ郡 Villa Park

- 技術のケーススタディ:ノースカロライナ州ウィルミントン

- 技術のケーススタディ:ニューハンプシャー州ポーツマス

- 技術のケーススタディ:ノースカロライナ州ブランズウィック郡

第4章 米国のバイオソリッド市場とビジネスモデル

- 米国の下水汚泥の生産

- 廃水処理の販売可能な副産物:危機的状態

- バイオソリッドの市場機会:米国全体での有効利用に依存

- 米国のバイオソリッド市場:埋立料金の高騰による市場促進

- バイオソリッドの焼却施設・設備:衰退傾向

- バイオソリッドの実用化コストと価格の比較

- バイオソリッド管理戦略:外注式・内製式

- スラッジの生成・廃棄・使用・コスト:PFASのリスク

第5章 PFASアクション:世界各国への拡大

- 世界のPFAS政策アプローチ

- PFAS汚染の抑制に向けた取り組み:世界各国への拡大

- 欧州連合 (EU が強力なPFASアクションを発表

第6章 企業プロファイル

分析対象の企業

技術プロバイダー:

- AECOM

- AqueosUS Tech

- Arcadis-Evocra

- Battelle

- BioLargo

- Biwater

- Calgon Carbon

- CycloPure

- ECT2

- Evoqua

- Filtra Systems

- H2O Innovate

- Koch

- Norit

- OPEC

- Pall

- Purolite

- Regenesis

- Resin Tech

- TIGG

- Toray

- Veolia Water Technologies

- Wigen

- 374Water

バイオソリッドの整備・サービスプロバイダー

- BCR Environmental

- Burch Hydro

- Casella Waste Systems

- Denali Water Solutions

- Lystek

- Mannco

- McGill

- Resource Mgt. Inc.

- Schwing Bioset

- Synagro

- Veolia Water Technologies

Highly affected U.S. states, such as Michigan, New York, and New Jersey have sought to implement their own regulatory limits on PFAS concentrations in drinking water ahead of a slower moving federal government. Now, with the U.S. Environmental Protection Agency in the position to crack down on these chemicals in various water sources, including implementing drinking water maximum contaminant levels for PFOA & PFOS by Fall 2023, all states find themselves in the position of growing PFAS remediation need. At the same time, concern over how PFAS makes its way back into groundwater or into plant and animal uptake through biosolid land applications is threatening to disrupt the biosolids market

This Insight Report supports water and wastewater utilities as well as PFAS technology providers with detailed data, market and policy trend analysis, and growth forecasts in U.S. PFAS remediation projects and biosolid market adjustments. Bluefield's analysis of the market includes examination of policy shifts, technology trends, and strategies influencing the deployment of their innovative solutions.

Companies Mentioned:

|

|

|

Table of Contents

Section 1: U.S. Drinking Water PFAS Policy and Legal Action

- Federal Regulatory Trajectory

- PFAS State Drinking Water Policy

- States Propose and Adopt Drinking Water MCLs

- Expanding State Regulation Landscape

- PFAS Sites Identified Proliferate across the Country

- PFAS Sparks Legal Action against Suppliers

- Infrastructure Funding Drives PFAS Investment

- Key PFAS Funding Channels

- Investment in Technology Innovation

- PFAS Action Expands to Investor-owned Utilities

Section 2: U.S. Drinking Water Remediation Forecasts

- Key Market Assumptions: Treatment System Addressable Market

- Total Drinking Water Market Forecast, 2022-2030

- Drinking Water Market Forecasts by Technology, 2022-2030

- Drinking Water Market Forecasts Top 20 States, 2022-2030

Section 3: PFAS Treatment Technologies and Case Studies

- PFAS Treatment: Established and Emerging Technologies

- Maturity of PFAS Treatment Technologies

- Emerging Drinking Water Technologies Overview

- PFAS Concentration, Chain Length, and Removal Capabilities

- Technology Case Study: Placentia, Orange County, California

- Technology Case Study: Villa Park, Orange County, California

- Technology Case Study: Wilmington, North Carolina

- Technology Case Study: Portsmouth, New Hampshire

- Technology Case Study: Brunswick County, North Carolina

Section 4: U.S. Biosolids Market and Business Models

- Sewage Sludge Production across the U.S.

- Wastewater Treatment Saleable Byproducts at Risk

- Biosolids Market Opportunity Dependent on Beneficial Use across the U.S.

- Rising Landfill Tipping Fees Drive Biosolids Market across the U.S.

- Biosolid Incineration Facilities and Equipment on the Decline

- Biosolid Commercial Costs and Value Comparison

- Outsourced v.s In-house Biosolids Management Strategies

- Sludge Production and Disposal Use and Costs: PFAS Risks

Section 5: PFAS Action Expands Globally

- Global PFAS Policy Approaches

- Efforts to Rein in PFAS Contamination Expands Globally

- European Union Puts Forth Strong PFAS Action

Section 6: Company Profiles

Companies Profiled

Technology Providers:

- AECOM

- AqueosUS Tech

- Arcadis-Evocra

- Battelle

- BioLargo

- Biwater

- Calgon Carbon

- CycloPure

- ECT2

- Evoqua

- Filtra Systems

- H2O Innovate

- Koch

- Norit

- OPEC

- Pall

- Purolite

- Regenesis

- Resin Tech

- TIGG

- Toray

- Veolia Water Technologies

- Wigen

- 374Water

Biosolids Maintenance and Service Provider

- BCR Environmental

- Burch Hydro

- Casella Waste Systems

- Denali Water Solutions

- Lystek

- Mannco

- McGill

- Resource Mgt. Inc.

- Schwing Bioset

- Synagro

- Veolia Water Technologies

List of Exhibits

- 1. The Utility Water Cycle and PFAS Impacts

- 2. Federal Regulatory Timeline

- 3. PFAS State Drinking Water Landscape Overview

- 4. State Water Infrastructure, Estimated PFAS Contamination,and MCLs for PFAS Compounds (ppt)

- 5. State Water Infrastructure, Estimated PFAS Contamination,and Regulations for PFAS Compounds (ppt)

- 6. PFAS Contamination Extent by State

- 7. Recent PFAS Litigation

- 8. IIJA PFAS Allocations

- 9. PFAS State Revolving Fund Appropriations, Fiscal Year PFASAppropriations

- 10. Emerging PFAS Technologies & Providers

- 11. PFAS Activity Among Leading Investor-Owned Utilities

- 12. Top-Down View of Addressable Market

- 13. Total Market Spend CAPEX + OPEX, 2022-2030

- 14. Combined CAPEX + OPEX by Technology, 2022-2030

- 15. CAPEX + OPEX Top 20 States, 2022-2030

- 16. PFAS Treatment Technology Landscape

- 17. Drinking Water PFAS Treatment Technology Timeline

- 18. Emerging Technology Descriptions

- 19. PFAS Treatment Technology Comparison

- 20. Sewage Sludge Production by State

- 21. Wastewater Treatment Processes & Byproducts

- 22. Biosolids Use & Disposal Mechanisms

- 23. Year- over- Year Tipping Fees by Region

- 24. Number of Incineration Facilities by State

- 25. Economics of Biosolids Applications

- 26. Biosolids Management Operating Models

- 27. Sludge Production and Disposal Costs

- 28. PFAS Nationwide Growth Markets

- 29. ECHA Major PFAS Actions

- 30. European Union PFAS Action Summary

- 31. PFAS Technology Portfolios of Representative Companies

- 32. PFAS Technology Portfolios of Representative Companies, Emerging

- 33. Service Offerings of Biosolid Providers