|

|

市場調査レポート

商品コード

1285102

拘束性ペプチド薬市場 - 世界および地域別分析:ペプチドタイプ別、製品別、地域別 - 分析と予測(2024年~2040年)Constrained Peptide Drugs Market - A Global and Regional Analysis: Focus on Peptide Type, Product, and Region-Wise Analysis - Analysis and Forecast, 2024-2040 |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| 拘束性ペプチド薬市場 - 世界および地域別分析:ペプチドタイプ別、製品別、地域別 - 分析と予測(2024年~2040年) |

|

出版日: 2023年05月30日

発行: BIS Research

ページ情報: 英文 229 Pages

納期: 1~5営業日

|

- 全表示

- 概要

- 図表

- 目次

世界の拘束性ペプチド薬の市場規模は、2024年に6,000万米ドルになるとみられ、2040年には173億8,000万米ドルに達すると予測されています。

市場は、2025年から2040年にかけてCAGRで38.94%の成長が見込まれています。

当レポートでは、世界の拘束性ペプチド薬市場について調査し、市場の概要とともに、ペプチドタイプ別、製品別、地域別の動向、および市場に参入する企業のプロファイルなどを提供しています。

目次

第1章 定義

第2章 調査範囲

第3章 調査手法

第4章 市場の概要

- イントロダクション

- 拘束性ペプチドの構造と設計

- 拘束性ペプチドの種類

- 拘束性ペプチド薬企業への影響

- 臨床試験の中断と再開

第5章 構造的拘束性ペプチドの特徴

- 構造的拘束性ペプチドの特性

- 拘束性ペプチドの合成

- ペプチド技術の進歩

- ペプチド表示および選択システム

第6章 業界考察

- 概要

- 拘束性ペプチドの規制当局の承認経路における課題

- 拘束性ペプチドの規制シナリオ

- 米国の法的要件と枠組み

- 欧州の法的要件と枠組み

- アジア太平洋の法的要件と枠組み

- 償還シナリオ

第7章 市場力学

- 影響分析

- 市場促進要因

- 市場抑制要因

- 市場機会

第8章 競合情勢

- 競合情勢の概要

第9章 世界の拘束性ペプチド薬市場(パイプライン別)、100万米ドル、2024年~2040年

- 拘束性ペプチド薬の臨床試験デザイン

- 世界の拘束性ペプチド薬市場パイプライン分析、100万米ドル、2024年~2040年

第10章 世界の拘束性ペプチド薬市場(ペプチドタイプ別)、100万米ドル、2024年~2040年

- 世界の拘束性ペプチド薬市場(ペプチドタイプ別)、10億米ドル、2024年~2040年

- 概要

- 環状ペプチド

- ジスルフィドリッチペプチド(DRP)

第11章 世界の拘束性ペプチド薬市場(潜在的製品別)、100万米ドル、2024年~2040年

- 概要

- BT5528

- ジルコプラン(RA101495)

- ラスフェルチド(PTG-300)

- PN-943

- PN-235

第12章 世界の拘束性ペプチド薬市場(国別)、100万米ドル、2024年~2040年

- 世界の拘束性ペプチド薬市場(国別)、10億米ドル、2024年~2031年

- 北米

- 欧州

- アジア太平洋

第13章 企業プロファイル

- Aileron Therapeutics, Inc.

- Bicycle Therapeutics plc

- Spexis AG

- Protagonist Therapeutics Inc.

- Santhera Pharmaceuticals

- Union Chimique Belge S.A.(UCB)

- Creative Peptides

- Biosynth(Pepscan)

- Pepticom Ltd.

- PeptiDream, Inc.

- Bio-Synthesis Inc

- CPC Scientific Inc.

- 新興企業

List of Figures

- Figure 1: Total Number of Drugs Approved by the U.S. FDA, 2016-2021

- Figure 2: Global Constrained Peptide Drugs Market, $Billion, 2024-2031

- Figure 3: Global Constrained Peptide Drugs Market, $Billion, 2032-2040

- Figure 4: Global Constrained Peptide Drugs: Impact Analysis

- Figure 5: Revenue Contribution of Different Segments, 2024 and 2031

- Figure 6: Global Constrained Peptide Drugs Market (by Potential Product), $Billion, 2024-2040

- Figure 7: Global Constrained Peptide Drugs Market (by Region), $Billion, 2024-2040

- Figure 8: Global Constrained Peptide Drugs Market Segmentation

- Figure 9: Global Constrained Peptide Drugs Methodology

- Figure 10: Primary Research Methodology

- Figure 11: Epidemiology-Based Approach

- Figure 12: Inducing Conformational Effects

- Figure 13: Two Main Types of Constraints

- Figure 14: Methodology for Restricting Conformation in Peptides

- Figure 15: Types of Constrained Peptides

- Figure 16: Key Milestones in the Evolution of Constrained Peptides

- Figure 17: Major Factors Affecting Constrained Peptide Development

- Figure 18: Value Chain Analysis- Key Stakeholders

- Figure 19: Global Constrained Peptide Drugs Market (by Region), $Billion, 2024-2031

- Figure 20: Global Constrained Peptide Drugs Market (by Region), $Billion, 2032-2040

- Figure 21: Global Constrained Peptide Drugs Market, $Billion, 2024-2031

- Figure 22: Global Constrained Peptide Drugs Market, $Billion, 2032-2040

- Figure 23: Synthesis of Constrained Peptides using Chemical Peptide Ligation and Bridging

- Figure 24: Constrained Peptide Synthesis using CLIPS Technology

- Figure 25: Constrained Peptides Synthesis using Peptide Stapling

- Figure 26: Peptide Discovery Platform System (PDPS) Technology

- Figure 27: Synthesis of Peptides Using Liquid Phase Peptide Synthesis

- Figure 28: Synthesis of Peptides Using Solid Phase Peptide Synthesis

- Figure 29: Companies and Their Proprietary Technologies

- Figure 30: Features of Microflow Reaction for Peptide Synthesis

- Figure 31: Advantages of Microwave-Assisted Solid-Phase Peptide Synthesis

- Figure 32: Phage Display Technology

- Figure 33: Clinical Trial Authorization for Constrained Peptides in the U.S.

- Figure 34: Steps for Obtaining Marketing Authorization

- Figure 35: U.S. FDA Review Timeline

- Figure 36: EMA Review Timeline

- Figure 37: Factors Affecting Constrained Peptide Cellular Penetration

- Figure 38: Key Innovative Modern Technologies and Constraining Methods

- Figure 39: Properties of Traditional Peptides Vs. Constrained Peptides

- Figure 40: Share of Key Developments and Strategies, January 2018 to January 2023

- Figure 41: Share of Regulatory and Legal Activities (by Company), January 2018 to January 2023

- Figure 42: Share of Mergers and Acquisitions (by Company), January 2018 to January 2023

- Figure 43: Share of Synergistic Activities (by Company), January 2018 to January 2023

- Figure 44: Share of Funding Activities (by Company), January 2018 to January 2023

- Figure 45: Illustration of BT5528

- Figure 46: Tumors with EphA2 Over-Expression

- Figure 47: BT5528 Phase I/II Clinical Trial Design for Solid Tumors

- Figure 48: BT5528 Preclinical Studies Framework

- Figure 49: PN-943 Phase II IDEAL Study Intervention Model Design

- Figure 50: PN-943 Phase II Clinical Trial Design for Moderate-to-Severe Ulcerative Colitis (UC)

- Figure 51: Results from PN-943 Phase I Clinical Trial

- Figure 52: PN-235 Phase IIb Clinical Trial Design for Moderate-to-Severe Plaque Psoriasis

- Figure 53: Rusfertide (PTG-300) Mechanism of Action

- Figure 54: Rusfertide (PTG-300) Phase III clinical Design for Hereditary Hemochromatosis

- Figure 55: Zilucoplan (RA101495) Mechanism of Action

- Figure 56: Zilucoplan Phase III Clinical Trial Design for Generalized Myasthenia Gravis

- Figure 57: Zilucoplan Phase III Clinical Trial Design for Generalized Myasthenia Gravis

- Figure 58: Zilucoplan Safety and Efficacy Tolerability Profile

- Figure 59: Zilucoplan PK/PD Profile Results

- Figure 60: Rusfertide (PTG-300) Mechanism of Action

- Figure 61: Limited Current Treatment Options in Polycythemia Vera

- Figure 62: Rusfertide (PTG-300) Phase III Clinical Design for Polycythemia Vera

- Figure 63: Clinical Proof-of-Concept Study Intervention Model Design

- Figure 64: Cost of API Manufacturing (by Product), $Million, 2024-2031

- Figure 65: Cost of API Manufacturing (by Product), $Million, 2032-2040

- Figure 66: Revenue Contribution of Different Segments, 2024 and 2031

- Figure 67: Global Constrained Peptide Drugs Market (Cyclic Peptides), $Billion, 2024-2031

- Figure 68: Global Constrained Peptide Drugs Market (Cyclic Peptides), $Billion, 2032-2040

- Figure 69: Global Constrained Peptide Drugs Market (Disulfide-Rich Peptides), $Billion, 2024-2031

- Figure 70: Global Constrained Peptide Drugs Market (Disulfide-Rich Peptides), $Billion, 2032-2040

- Figure 71: Global Constrained Peptide Drugs Market (by Product), $Billion, 2024-2040

- Figure 72: Global Revenue for BT5528, $Billion, 2024-2031

- Figure 73: Global Revenue for BT5528, $Billion, 2032-2040

- Figure 74: BT5528.: API Manufacturing

- Figure 75: BT5528: API Demand Forecast, by Volume, Kilogram, 2024-2031

- Figure 76: BT5528: API Demand Forecast, by Volume, Kilogram, 2032-2040

- Figure 77: Global Revenue for Zilucoplan (RA101495), $Billion, 2024-2031

- Figure 78: Global Revenue for Zilucoplan (RA101495), $Billion, 2032-2040

- Figure 79: Zilucoplan (RA101495): API Manufacturing

- Figure 80: Zilucoplan (RA101495): API Demand Forecast, by Volume, Kilogram, 2024-2031

- Figure 81: Zilucoplan (RA101495): API Demand Forecast, by Volume, Kilogram, 2032-2040

- Figure 82: Global Revenue for Rusfertide (PTG-300), $Billion, 2024-2031

- Figure 83: Global Revenue for Rusfertide (PTG-300), $Billion, 2032-2040

- Figure 84: Rusfertide (PTG-300).: API Manufacturing

- Figure 85: Rusfertide (PTG-300): API Demand Forecast, by Volume, Kilogram, 2024-2031

- Figure 86: Rusfertide (PTG-300): API Demand Forecast, by Volume, Kilogram, 2032-2040

- Figure 87: Global Revenue for PN-943, $Billion, 2024-2031

- Figure 88: Global Revenue for PN-943, $Billion, 2032-2040

- Figure 89: PN-943.: API Manufacturing

- Figure 90: PN-943: API Demand Forecast, by Volume, Kilogram, 2024-2031

- Figure 91: PN-943: API Demand Forecast, by Volume, Kilogram, 2032-2040

- Figure 92: Global Revenue for PN-235, $Billion, 2024-2031

- Figure 93: Global Revenue for PN-235, $Billion, 2032-2040

- Figure 94: PN-325.: API Manufacturing

- Figure 95: PN-235: API Demand Forecast, by Volume, Kilogram, 2024-2031

- Figure 96: PN-235: API Demand Forecast, by Volume, Kilogram, 2032-2040

- Figure 97: Global Constrained Peptide Drugs Market (by Region)

- Figure 98: Global Constrained Peptide Drugs Market (by Region), $Billion, 2024-2040

- Figure 99: North America Constrained Peptide Drugs Market, $Billion, 2024-2031

- Figure 100: North America Constrained Peptide Drugs Market, $Billion, 2032-2040

- Figure 101: North America: Market Dynamics

- Figure 102: North America Constrained Peptide Drugs Market (by Country), $Billion, 2024 and 2040

- Figure 103: U.S. Constrained Peptide Drugs Market, $Billion, 2024-2031

- Figure 104: U.S. Constrained Peptide Drugs Market, $Billion, 2032-2040

- Figure 105: Canada Constrained Peptide Drugs Market, $Billion, 2024-2031

- Figure 106: Canada Constrained Peptide Drugs Market, $Billion, 2032-2040

- Figure 107: Europe Constrained Peptide Drugs Market, $Billion, 2024-2031

- Figure 108: Europe Constrained Peptide Drugs Market, $Billion, 2032-2040

- Figure 109: Europe: Market Dynamics

- Figure 110: Europe Constrained Peptide Drugs Market (by Country), $Billion, 2025 and 2040

- Figure 111: U.K. Constrained Peptide Drugs Market, $Billion, 2024-2031

- Figure 112: U.K. Constrained Peptide Drugs Market, $Billion, 2032-2040

- Figure 113: Germany Constrained Peptide Drugs Market, $Billion, 2024-2031

- Figure 114: Germany Constrained Peptide Drugs Market, $Billion, 2032-2040

- Figure 115: France Constrained Peptide Drugs Market, $Billion, 2024-2031

- Figure 116: France Constrained Peptide Drugs Market, $Billion, 2032-2040

- Figure 117: Italy Constrained Peptide Drugs Market, $Billion, 2024-2031

- Figure 118: Italy Constrained Peptide Drugs Market, $Billion, 2032-2040

- Figure 119: Spain Constrained Peptide Drugs Market, $Billion, 2024-2031

- Figure 120: Spain Constrained Peptide Drugs Market, $Billion, 2032-2040

- Figure 121: Japan Constrained Peptide Drugs Market, $Billion, 2024-2031

- Figure 122: Japan Constrained Peptide Drugs Market, $Billion, 2032-2040

- Figure 123: Total Number of Companies Profiled

- Figure 124: Aileron Therapeutics, Inc.: Product Portfolio

- Figure 125: Aileron Therapeutics, Inc.: Overall Financials, $Million, 2019-2021

- Figure 126: Aileron Therapeutics, Inc.: R&D Expenditure, $Million, 2019-2021

- Figure 127: Bicycle Therapeutics plc: Product Portfolio

- Figure 128: Bicycle Therapeutics plc: Overall Financials, $Million, 2019-2021

- Figure 129: Bicycle Therapeutics plc: Revenue (by Region), $Million, 2019-2021

- Figure 130: Bicycle Therapeutics plc: R&D Expenditure, $Million, 2019-2021

- Figure 131: Spexis AG: Product Portfolio

- Figure 132: Spexis AG: Overall Financials, $Million, 2019-2021

- Figure 133: Spexis AG: R&D Expenditure, $Million, 2019-2021

- Figure 134: Protagonist Therapeutics Inc.: Product Portfolio

- Figure 135: Protagonist Therapeutics Inc.: Overall Financials, $Million, 2019-2021

- Figure 136: Protagonist Therapeutics Inc.: R&D Expenditure, $Million, 2019-2021

- Figure 137: Santhera Pharmaceuticals: Product Portfolio

- Figure 138: Santhera Pharmaceuticals: Overall Financials, $Million, 2019-2021

- Figure 139: Union Chimique Belge S.A. (UCB): Product Portfolio

- Figure 140: Union Chimique Belge S.A. (UCB): Overall Financials, $Million, 2019-2021

- Figure 141: Union Chimique Belge S.A. (UCB): R&D Expenditure, $Million, 2019-2021

- Figure 142: Creative Peptides: Product Portfolio

- Figure 143: Biosynth (Pepscan): Product Portfolio

- Figure 144: Pepticom Ltd.: Product Portfolio

- Figure 145: PeptiDream, Inc.: Product Portfolio

- Figure 146: PeptiDream, Inc.: Overall Financials, $Million, 2019-2021

- Figure 147: Bio-Synthesis Inc Product Portfolio

- Figure 148: CPC Scientific Inc.: Product Portfolio

List of Tables

- Table 1: Potential Indications of Constrained Peptide Drugs

- Table 2: Potential Therapy Areas of Constrained Peptide Drugs

- Table 3: Route of Administration of Constrained Peptide Drugs

- Table 4: Impact of COVID-19 on Constrained Peptide Drug Companies

- Table 5: Properties of Conformationally Constrained Peptides

- Table 6: Display and Selection System Employed by Companies

- Table 7: Regulatory Scenario of Constrained Peptides

- Table 8: Autoimmune Diseases Reimbursement Scenario

- Table 9: Cancer Reimbursement Scenario

- Table 10: Funding by Private Companies

- Table 11: Rusfertide Phase II Baseline Characteristics Results

- Table 12: Zilucoplan Phase III Baseline Characteristics Results

- Table 13: Likeliness Scale for Probability of Success (Pre-Clinical)

- Table 14: Likeliness Scale for Probability of Success (Pre-Clinical)

- Table 15: Circle Drugs Pipeline

“Global Constrained Peptide Drugs Market to Reach $17.38 Billion by 2040.”

Industry Overview

The global constrained peptide drugs market revenue has been forecasted from 2024 to 2040, following the earliest launch of the first constrained peptide drug in the market. The market size is anticipated to be $0.06 billion in 2024 and is expected to reach $17.38 billion in 2040, growing at a CAGR of 38.94% during the forecast period 2025-2040.

Market Lifecycle Stage

The global constrained peptide drugs market is anticipated to witness tremendous growth during the forecast period 2025-2040, largely fuelled by the promise of a novel breakthrough constrained peptide pipeline, which is no longer restricted to receptor targets. Advancements in chemical technologies, the therapeutics' success of commercialized synthetic peptides in recent years, and the affordable pricing being realized by these biomolecules in a wide range of diseases are some additional factors attributing to the projected growth in the forecast period.

Impact

The impact analysis for the factors that significantly affect the market, namely, drivers, restraints, and opportunities, has been provided on a short-term and long-term basis. The short-term assessment considers the period between 2020 and 2025, and the long-term assessment considers the period between 2026 and 2040. Key developments and strategies that have been undertaken by some of the key players in this market have been accounted for evaluation of the impact analysis. Further, these key developments have been assessed to understand the future scope of integrating advancing technologies to enable superior outcomes. Additionally, approvals and launches from companies and patent bodies have also been considered while evaluating the dynamics of the global constrained peptide drugs market.

Impact of COVID-19

In December 2019, Wuhan, a city in the Hubei region of China, was the site of the first detection of the COVID-19 outbreak. Following the classification of COVID-19 as novel pneumonia due to a cluster of unexplained pneumonia cases, efforts to pinpoint the culprit causing the outbreak and outline its genomic sequence got underway right once. The virus has already spread to every country on the globe, and researchers, governments, and business leaders are working to find answers to the crisis at a scale and speed that has never been seen. Testing for SARS-CoV-2 in the populace is one of the main steps that has been put into place globally, among many other measures used to stop the spread of the disease.

The global constrained peptide drugs market is a research-oriented market, having a majority of products in clinical trial stages. It primarily consists of clinical-stage biopharmaceutical companies and global biopharmaceutical companies such as Bicycle Therapeutics PLC, Protagonist Therapeutics, Inc., Aileron Therapeutics, Inc., Polyphor, and Santhera Pharmaceuticals Holding. Since most of the products are in the clinical phase of drug development, constrained peptide drug companies had a low impact on the COVID-19 pandemic.

Although clinical trials were brought to pause because of the lockdowns imposed by governments across the world, causing a delay in the clinical trial timeline, and volunteers and patients were also not able to participate in the clinical trials due to the lockdown; however, few companies took the opportunity of the pandemic and initiated the development of potential drugs against COVID-19. For instance, UCB Pharma participated in the COVID-19 Moonshot, an initiative to expedite the development of an anti-viral for COVID-19. The company's Phase III investigational molecule Zilucoplan is being studied for acute respiratory distress syndrome associated with COVID-19. Another company, Polyphor Limited, is evaluating Balixafortide, a constrained peptide drug, against COVID-19 as it demonstrated strong efficacy in in-vitro models.

During the pre-COVID-19 period, the global constrained peptide drugs market observed 38 significant key developments. Out of the 38 key developments, the majority were funding activities, primarily focused on the development of novel antibiotics and support clinical trials of certain drugs in clinical phases. For example, in May 2019, Innosuisse awarded Polyphor Ltd. and the University of Zurich to escalate the development of novel antibiotics for treating infections caused by gram-negative bacteria. Furthermore, seven synergistic activities were undertaken in the global constrained peptide drugs market before COVID-19.

Market Segmentation:

Segmentation 1: by Peptide Type

- Disulfide-Rich Peptides (DRPs)

- Cyclic Peptides

Based on peptide type, the disulfide-rich peptides (DRPs) segment is anticipated to dominate the global constrained peptide drugs market in 2040 as the segment includes the pipeline-constrained peptide with either limited existing treatment options or no approved drugs for the disease.

Segmentation 2: by Region

- North America

- Europe

- Asia-Pacific

The North America region is anticipated to dominate the global constrained peptide drugs market (by region) during the forecast period 2025-2040. The reasons contributing to the high demand for constrained peptide drugs in North America are the increasing prevalence of target indications and the early launch of pipeline products in the U.S. and Canada.

Segmentation 3: by Potential Product

- BT5528

- Rusfertide (PTG-300)

- PN-943

- PN-235

- Zilucoplan (RA101495)

Segmentation 4: by Company

|

|

Based on the company, the global constrained peptide drugs market is dominated by 15 major companies.

Recent Developments in the Global Constrained Peptide Drugs Market

- In August 2021, Protagonist Therapeutics Inc. declared the resolution of its collaboration agreement with Zealand Pharma through the reduction of future milestone payments, sales milestones, and royalties owed to Zealand Pharma regarding Protagonist Therapeutics Inc.'s product candidate rusfertide under the terms of the 2012 collaboration agreement between the companies.

- In April 2021, Union Chimique Belge S.A. (UCB) anticipated the release of phase 3 key results for generalized myasthenia gravis (gMG) in the fourth quarter of 2021 and discontinued further development of zilucoplan for immune-mediated necrotizing myopathy (IMNM).

- In September 2021, Polyphor Limited and EnBiotix announced the successful closing of the purchase agreement for EnBiotix to acquire the inhaled antibiotic murepavadin.

- In November 2020, Pepscan Therapeutics B.V. was granted a license for the use of the proprietary CLIPS technology offered by Bicycle Therapeutics plc. The peptide-constraining technology would further help in the development of the company's products named BT1718 and THR-149.

- In June 2020, Santhera Pharmaceuticals secured a financing commitment of up to $22.1 million from a fund managed by Highbridge Capital Management.

Demand - Drivers and Limitations

The following are the demand drivers for the global constrained peptide drugs market:

- Enhanced Binding Affinity and Cellular Uptake

- Development of Synthetic Constraining Method

- Limitations with Conventional Peptides

- Increasing Government and Private Funding

The market is expected to face some limitations due to the following challenges:

- Increased Competition from Biologics

- Risk of Immunogenic Effects and Unsatisfactory ADME Properties

How can this report add value to an organization?

Workflow/Innovation Strategy: The global constrained peptide drugs market has been segmented (by product) into five candidates, i.e., BT5528, Rusfertide (PTG-300), Zilucoplan (RA101495), PN-235, and PN-943. Over the past decade, peptide drug discovery and development has witnessed a renaissance and scientific thrust as the industry has come to acknowledge the capability of peptide therapeutics in addressing unmet medical needs and the potential of this class of molecules to become a significant accompaniment or even favored alternative treatment to biologics and small molecules.

Peptide therapeutics have demonstrated a novel and selective yet safe mode of action for a wide range of indications. The existing and future development of constrained peptide drugs will continue to burgeon upon the strengths of constrained peptides and innovative technologies employed in the discovery and development, including peptide drug conjugates, multifunctional peptides, and cell-penetrating peptides. Furthermore, limitations associated with presently available peptides have resulted in an urgent need for new design, administration, and synthesis in peptide therapeutics, thereby leading to advancements in the development of constrained peptides.

Growth/Marketing Strategy: Constrained peptides provide noteworthy advantages over linear peptides. An increase in interest in the field of constrained peptides due to the properties they offer led to advancements in peptide synthesis technologies. Companies such as PeptiDream Inc., Pepticom Ltd., Bicycle Therapeutics plc, and Polyphor Limited offer proprietary drug development and constrained peptide synthesis technologies. PeptiDream Inc.'s proprietary Peptide Discovery Platform System (PDPS) technology is used to synthesize synthetic non-native peptide libraries expeditiously, which helps in identifying peptides that can be used as potential drugs for a disease.

Competitive Strategy: Key players in the global constrained peptide drugs market have been analyzed and profiled in the study, including manufacturers involved in new product development, acquisitions, expansions, and strategic collaborations. Moreover, a detailed competitive benchmarking of the players operating in the global constrained peptide drugs market has been done to help the reader understand how players stack against each other, presenting a clear market landscape. Additionally, comprehensive competitive strategies such as partnerships, agreements, and collaborations will aid the reader in understanding the untapped revenue pockets in the market.

Table of Contents

1 Definition

- 1.1 Inclusion and Exclusion Criteria

2 Research Scope

- 2.1 Target Audience

- 2.2 Key Questions Answered in the Report

3 Research Methodology

- 3.1 Constrained Peptides: Research Methodology

- 3.2 Primary Data Sources

- 3.3 Secondary Data Sources

- 3.4 Market Estimation Model

- 3.5 Criteria for Company Profiling

4 Markets Overview

- 4.1 Introduction

- 4.1.1 Structure and Design of Constrained Peptides

- 4.1.2 Types of Constrained Peptides

- 4.2 Evolution of Constrained Peptides

- 4.3 Development of Constrained Peptides as Drugs

- 4.4 Potential Therapy Areas

- 4.5 Value Chain-Key Stakeholders

- 4.6 Key Industry Trends (by Region)

- 4.7 Key Industry Trends by Route of Administration

- 4.8 Key Industry Trends-Technological Advancements

- 4.9 Current Market Size and Growth Potential, $Billion, 2024-2040

- 4.1 COVID-19 Impact on Global Constrained Peptides Drugs Market

- 4.10.1 Impact on Constrained Peptide Drugs Companies

- 4.10.2 Clinical Trial Disruptions and Resumptions

5 Characteristics of Conformationally Constrained Peptides

- 5.1 Properties of Conformationally Constrained Peptides

- 5.2 Synthesis of Constrained Peptides

- 5.2.1 Chemical Peptide Ligation and Bridging

- 5.2.2 Chemical Linkage of Peptides onto Scaffolds (CLIPS)

- 5.2.3 Peptide Stapling

- 5.2.4 Peptide Discovery Platform System (PDPS)

- 5.2.5 Liquid Phase Peptide Synthesis (LPPS)

- 5.2.6 Solid Phase Peptide Synthesis (SPPS)

- 5.3 Advances in Peptide Technology

- 5.3.1 Synthesis of Peptides Using Microflow Technology

- 5.3.2 Microwave-Assisted Solid-Phase Peptide Synthesis

- 5.4 Peptide Display and Selection System

6 Industry Insights

- 6.1 Overview

- 6.2 Challenges in Constrained Peptides Regulatory Approval Pathway

- 6.3 Regulatory Scenario of Constrained Peptides

- 6.4 Legal Requirements and Frameworks in the U.S.

- 6.4.1 Clinical Trial Authorization

- 6.4.2 Marketing Authorization

- 6.4.3 U.S. FDA Guidelines for NDA Submission

- 6.4.4 Post-Authorization Regulations

- 6.5 Legal Requirements and Frameworks in Europe

- 6.5.1 EMA Drug License Application Process

- 6.5.2 Centralized Procedure

- 6.5.3 Decentralized Procedure

- 6.5.4 Mutual-Recognition Procedure

- 6.5.5 National Procedure

- 6.6 Legal Requirements and Frameworks in Asia-Pacific

- 6.6.1 Legal Requirements and Frameworks in Japan

- 6.7 Reimbursement Scenario

- 6.7.1 Reimbursement Scenario for Autoimmune Diseases

- 6.7.2 Reimbursement Scenario for Cancer

- 6.7.3 Reimbursement Scenario for Rare Diseases

7 Market Dynamics

- 7.1 Impact Analysis

- 7.2 Market Drivers

- 7.2.1 Enhanced Binding Affinity and Cellular Uptake

- 7.2.2 Development of Synthetic Constraining Methods

- 7.2.3 Limitations with Conventional Peptides

- 7.2.4 Increasing Government and Private Funding

- 7.2.4.1 Funding by Private Companies

- 7.2.4.2 Funding by Public Companies

- 7.2.4.3 Funding by Government Institutions

- 7.3 Market Restraints

- 7.3.1 Increased Competition from Biologics

- 7.3.2 Risk of Immunogenic Effects and Unsatisfactory ADME Properties

- 7.4 Market Opportunities

- 7.4.1 Role of Constrained Peptides in Drug Discovery

- 7.4.2 Various Applications in CNS Disease Studies and Anti-Cancer Therapy

8 Competitive Landscape

- 8.1 Competitive Landscape Overview

- 8.1.1 Key Developments

- 8.1.2 Regulatory and Legal Activities

- 8.1.3 Mergers and Acquisitions

- 8.1.4 Synergistic Activities

- 8.1.5 Funding Activities

- 8.1.6 Clinical Developments

9 Global Constrained Peptides Drugs Market (by Pipeline), $Million, 2024-2040

- 9.1 Constrained Peptide Drugs Clinical Trial Design

- 9.1.1 Potential Phase II Drugs

- 9.1.2 BT5528

- 9.1.2.1 Product Profile

- 9.1.2.2 Study Design (Phase I/II)

- 9.1.2.3 Efficacy, Safety, and Tolerability Data (Phase I)

- 9.1.2.4 BT5528 Preclinical Studies

- 9.1.3 PN-943

- 9.1.3.1 Product Profile

- 9.1.3.2 Study Design (Phase II)

- 9.1.3.3 Efficacy, Safety, and Tolerability Data (Phase II)

- 9.1.4 PN-235

- 9.1.4.1 Product Profile

- 9.1.4.2 Study Design (Phase IIb)

- 9.1.4.3 Efficacy, Safety, and Tolerability Data (Phase IIb)

- 9.1.5 Rusfertide (PTG-300)

- 9.1.5.1 Product Profile

- 9.1.5.2 Study Design (Phase II)

- 9.1.5.3 Efficacy, Safety, and Tolerability Data (Phase IIa)

- 9.1.6 Potential Phase III drugs

- 9.1.7 Zilucoplan (RA101495)

- 9.1.7.1 Product Profile

- 9.1.7.2 Study Design (Phase III)

- 9.1.7.3 Efficacy, Safety, and Tolerability Data (Phase III)

- 9.1.7.4 Zilucoplan Pharmacokinetics and Pharmacodynamics Profile (Phase I)

- 9.1.8 Rusfertide (PTG-300)

- 9.1.8.1 Product Profile

- 9.1.8.2 Study Design (Phase III)

- 9.1.8.3 Efficacy, Safety, and Tolerability Data (Phase II)

- 9.2 Global Constrained Peptides Drugs Market Pipeline Analysis, $Million, 2024-2040

- 9.2.1 Pre-Clinical

- 9.2.1.1 Probability of Success

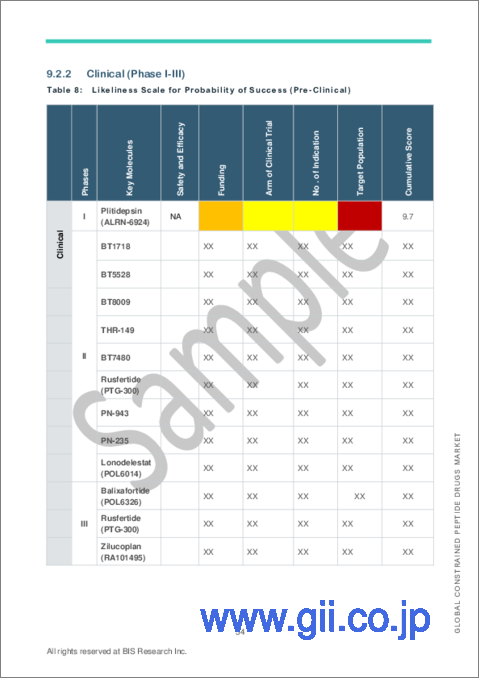

- 9.2.2 Clinical (Phase I-III)

- 9.2.2.1 Probability of Success

- 9.2.2.2 Cost of API Manufacturing (CDMOs)

- 9.2.1 Pre-Clinical

10 Global Constrained Peptides Drugs Market (by Peptide Type), $Million, 2024-2040

- 10.1 Global Constrained Peptide Drugs Market (by Peptide Type), $Billion, 2024-2040

- 10.1.1 Overview

- 10.1.2 Cyclic Peptides

- 10.1.3 Disulfide-Rich Peptides (DRPs)

11 Global Constrained Peptides Drugs Market (by Potential Products), $Million, 2024-2040

- 11.1 Overview

- 11.1.1 BT5528

- 11.1.1.1 API Manufacturing (Outsource)

- 11.1.1.2 API Demand Forecast 2024-2040

- 11.1.1.3 Cost of Outsourcing

- 11.1.2 Zilucoplan (RA101495)

- 11.1.2.1 API Manufacturing (In-House)

- 11.1.2.2 API Demand Forecast 2024-2040

- 11.1.3 Rusfertide (PTG-300)

- 11.1.3.1 API Manufacturing (Outsource)

- 11.1.3.2 API Demand Forecast 2024-2040

- 11.1.3.3 Cost of Outsourcing

- 11.1.4 PN-943

- 11.1.4.1 API Manufacturing (Outsource)

- 11.1.4.2 API Demand Forecast 2024-2040

- 11.1.4.3 Cost of Outsourcing

- 11.1.5 PN-235

- 11.1.5.1 API Manufacturing (Outsource)

- 11.1.5.2 API Demand Forecast 2024-2040

- 11.1.5.3 Cost of Outsourcing

- 11.1.1 BT5528

12 Global Constrained Peptides Drugs Market (by Country), $Million, 2024-2040

- 12.1 Global Constrained Peptide Drugs Market (by Country), $Billion, 2024-2031

- 12.1.1 North America

- 12.1.1.1 U.S.

- 12.1.1.2 Canada

- 12.1.2 Europe

- 12.1.2.1 U.K.

- 12.1.2.2 Germany

- 12.1.2.3 France

- 12.1.2.4 Italy

- 12.1.2.5 Spain

- 12.1.3 Asia-Pacific

- 12.1.3.1 Japan

- 12.1.1 North America

13 Company Profiles

- 13.1 Overview

- 13.2 Aileron Therapeutics, Inc.

- 13.2.1 Company Overview

- 13.2.2 Role of Aileron Therapeutics, Inc. in the Global Constrained Peptide Drugs Market

- 13.2.3 Current Status and Policies for Investigational Drugs

- 13.2.4 Key Competitors of the Company

- 13.2.5 Financials

- 13.2.6 Key Insights about the Financial Health of the Company

- 13.2.7 Corporate Strategies

- 13.2.7.1 Synergistic Activities

- 13.2.7.2 Funding Activity

- 13.2.8 Business Strategies

- 13.2.8.1 Clinical Development

- 13.2.9 Analyst Perspective

- 13.3 Bicycle Therapeutics plc

- 13.3.1 Company Overview

- 13.3.2 Role of Bicycle Therapeutics plc in the Global Constrained Peptide Drugs Market

- 13.3.1 Current Status and Policies for Investigational Drugs

- 13.3.2 Key Competitors of the Company

- 13.3.3 Financials

- 13.3.4 Key Insights about the Financial Health of the Company

- 13.3.5 Corporate Strategies

- 13.3.5.1 Synergistic Activities

- 13.3.5.2 Funding

- 13.3.6 Business Strategies

- 13.3.6.1 Clinical Developments

- 13.3.6.2 Regulatory and Legal

- 13.3.7 Analyst Perspective

- 13.4 Spexis AG

- 13.4.1 Company Overview

- 13.4.2 Role of Spexis AG in the Global Constrained Peptide Drugs Market

- 13.4.3 Current Status and Policies for Investigational Drugs

- 13.4.4 Key Competitors of the Company

- 13.4.5 Financials

- 13.4.6 Key Insights about the Financial Health of the Company

- 13.4.7 Corporate Strategies

- 13.4.7.1 Funding

- 13.4.7.2 Mergers and Acquisitions

- 13.4.7.3 Synergistic activities

- 13.4.8 Business Strategies

- 13.4.8.1 Regulatory and Legal

- 13.4.9 Analyst Perspective

- 13.5 Protagonist Therapeutics Inc.

- 13.5.1 Company Overview

- 13.5.2 Role of Protagonist Therapeutics Inc. in the Global Constrained Peptide Drugs Market

- 13.5.3 Current Status and Policies for Investigational Drugs

- 13.5.4 Key Competitors of the Company

- 13.5.5 Financials

- 13.5.6 Key Insights about the Financial Health of the Company

- 13.5.7 Corporate Strategies

- 13.5.7.1 Funding

- 13.5.7.2 Synergistic Activities

- 13.5.8 Business Strategies

- 13.5.8.1 Clinical Developments

- 13.5.8.2 Regulatory and legal

- 13.5.9 Analyst Perspective

- 13.6 Santhera Pharmaceuticals

- 13.6.1 Company Overview

- 13.6.2 Role of Santhera Pharmaceuticals in the Global Constrained Peptide Drugs Market

- 13.6.3 Current Status and Policies for Investigational Drugs

- 13.6.4 Key Competitors of the Company

- 13.6.5 Financials

- 13.6.6 Corporate Strategies

- 13.6.6.1 Funding

- 13.6.7 Business Strategies

- 13.6.7.1 Clinical Developments

- 13.6.8 Analyst Perspective

- 13.7 Union Chimique Belge S.A. (UCB)

- 13.7.1 Company Overview

- 13.7.2 Role of Union Chimique Belge S.A. (UCB) in the Global Constrained Peptide Drugs Market

- 13.7.3 Current Status and Policies for Investigational Drugs

- 13.7.4 Key Competitors of the Company

- 13.7.5 Financials

- 13.7.6 Key Insights about the Financial Health of the Company

- 13.7.7 Corporate Strategies

- 13.7.7.1 Mergers and Acquisitions

- 13.7.8 Business Strategies

- 13.7.8.1 Clinical Developments

- 13.7.8.2 Regulatory and legal

- 13.7.9 Analyst Perspective

- 13.8 Creative Peptides

- 13.8.1 Company Overview

- 13.8.2 Role of Creative Peptides in the Global Constrained Peptide Drugs Market

- 13.8.3 Key Competitors of the Company

- 13.8.4 Analyst Perspective

- 13.9 Biosynth (Pepscan)

- 13.9.1 Company Overview

- 13.9.2 Role of Biosynth (Pepscan) in the Global Constrained Peptide Drugs Market

- 13.9.3 Key Competitors of the Company

- 13.9.4 Corporate Strategies

- 13.9.4.1 License

- 13.9.5 Business Strategies

- 13.9.5.1 Product Launch

- 13.9.6 Analyst Perspective

- 13.1 Pepticom Ltd.

- 13.10.1 Company Overview

- 13.10.2 Role of Pepticom Ltd. in the Global Constrained Peptide Drugs Market

- 13.10.3 Analyst Perspective

- 13.11 PeptiDream, Inc.

- 13.11.1 Company Overview

- 13.11.2 Role of PeptiDream, Inc. in the Global Constrained Peptide Drugs Market

- 13.11.3 Key Competitors of the Company

- 13.11.4 Financials

- 13.11.5 Corporate Strategies

- 13.11.5.1 Synergistic Activities

- 13.11.6 Analyst Perspective

- 13.12 Bio-Synthesis Inc

- 13.12.1 Company Overview

- 13.12.2 Role of Bio-Synthesis Inc in the Global Constrained Peptide Drugs Market

- 13.12.3 Key Competitors of the Company

- 13.12.4 Analyst Perspective

- 13.13 CPC Scientific Inc.

- 13.13.1 Company Overview

- 13.13.2 Role of CPC Scientific Inc. in the Global Constrained Peptide Drugs Market

- 13.13.3 Key Competitors of the Company

- 13.13.4 Analyst Perspective

- 13.14 Emerging Companies

- 13.14.1 Circle Pharma

- 13.14.1.1 Platform

- 13.14.1.2 Pipeline Products

- 13.14.2 Zealand Pharma

- 13.14.2.1 ZP10000 (Preclinical)

- 13.14.2.1.1 Product Profile

- 13.14.2.1 ZP10000 (Preclinical)

- 13.14.3 Chugai Pharmaceutical Co., Ltd.

- 13.14.3.1 Mid-Size Molecule Technology

- 13.14.1 Circle Pharma